Indonesia Mortgage/Loan Brokers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

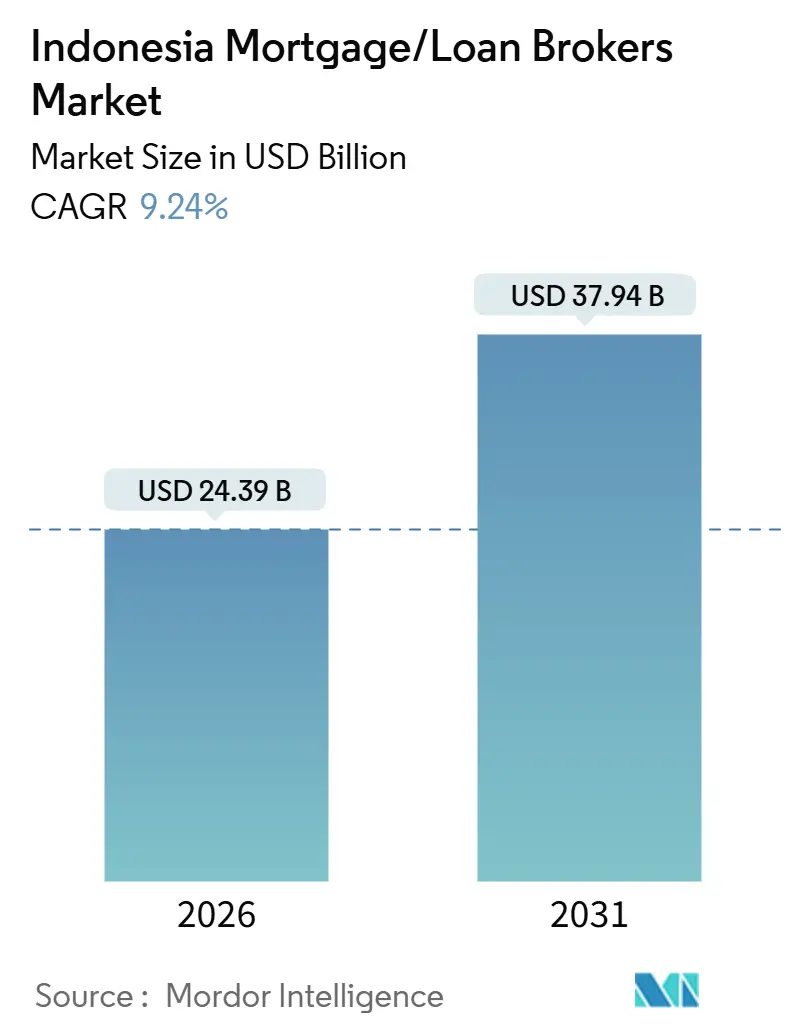

| Market Size (2026) | USD 24.39 Billion |

| Market Size (2031) | USD 37.94 Billion |

| Growth Rate (2026 - 2031) | 9.24% CAGR |

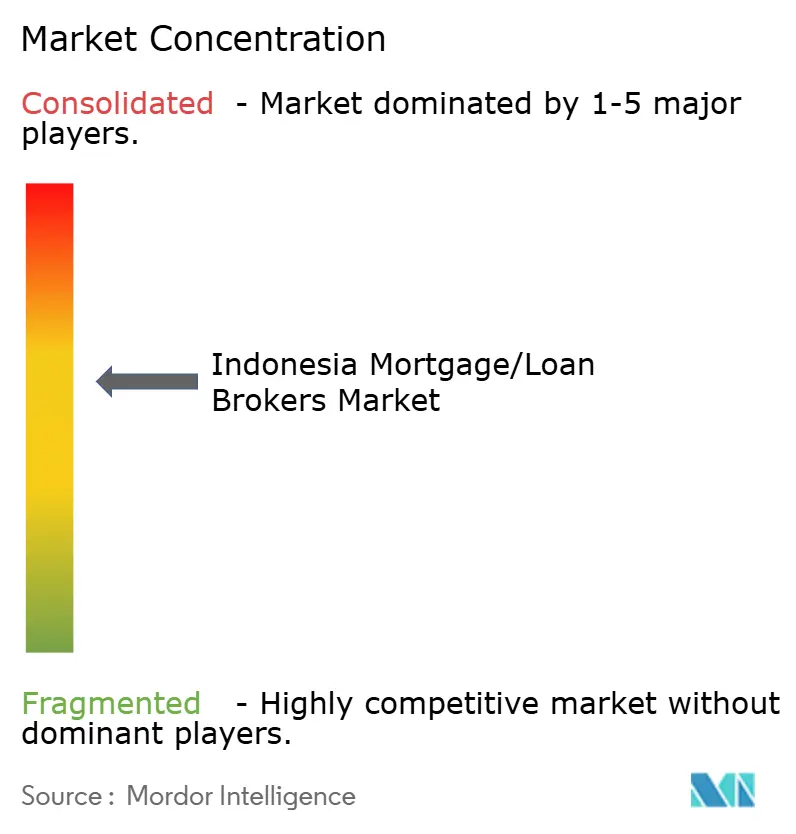

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Mortgage/Loan Brokers Market Analysis by Mordor Intelligence

The Indonesia mortgage/loan brokers market size reached USD 24.39 billion in 2026 and is forecast to reach USD 37.94 billion by 2031, reflecting a 9.24% CAGR. Growth is shaped by the interaction of subsidized housing finance through FLPP, the measured transmission of Bank Indonesia’s easing cycle into mortgage rates, and the rapid shift of origination and servicing toward bank-owned and partner-led digital channels. Subsidy-backed fixed-rate offers and zero-to-low down-payment options keep affordability in reach for first-time buyers while risk controls from lenders have tightened amid consumer NPL normalization and selective LTV implementation at the bank level[1]Source: OJK, “Press Release: Financial System Stability Maintained, Supporting Economic Growth through Vigilance Against Global Risks,” Otoritas Jasa Keuangan, ojk.go.id. The Indonesia mortgage/loan brokers market continues to consolidate around state-owned banks that distribute a large share of subsidized loans and use mortgage entry products to cross-sell retail and ecosystem services. Momentum also reflects policy coordination, including OJK measures to preserve high LTV ceilings where appropriate, BI’s macroprudential liquidity incentives to real estate and public housing, and targeted inclusion initiatives for informal workers within the subsidized pipeline.

Key Report Takeaways

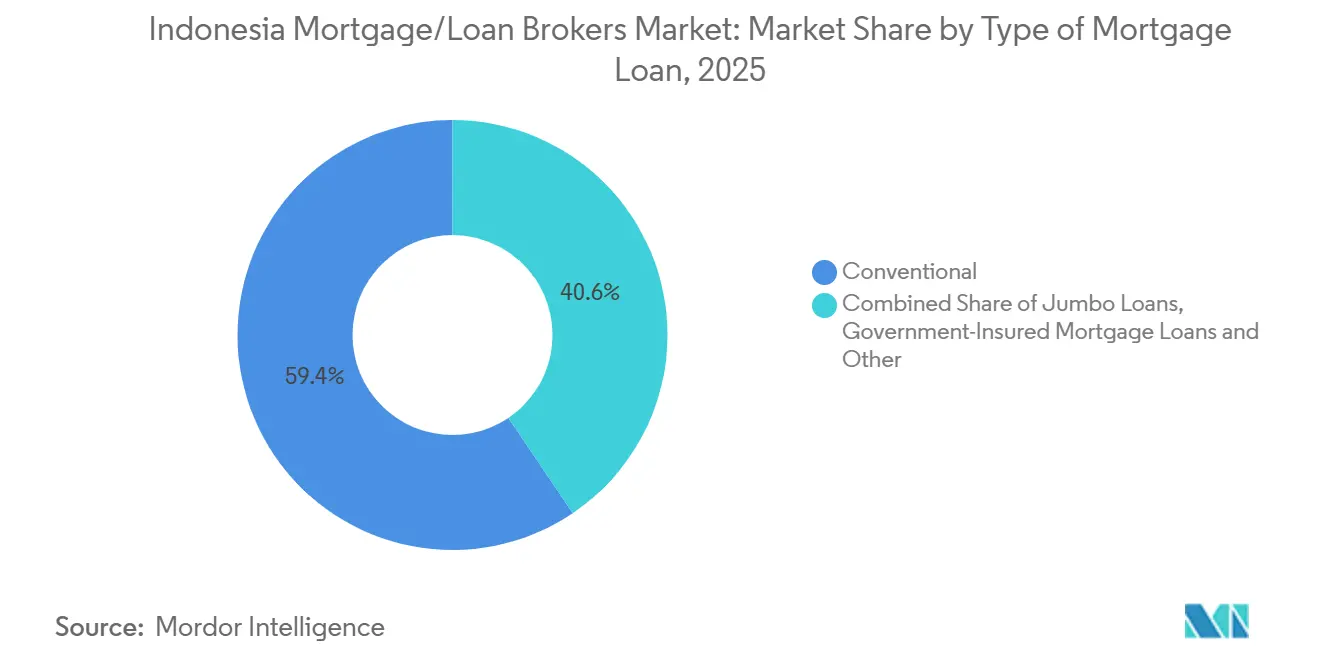

- By type of mortgage loan, conventional products led with 59.44% of the Indonesia mortgage/loan brokers market share in 2025, while government-insured mortgages are projected to expand at a 13.47% CAGR through 2031.

- By mortgage loan terms, 30-year tenors held 66.38% of the Indonesia mortgage/loan brokers market share in 2025, and 15-year maturities recorded the fastest growth at 14.38% annually.

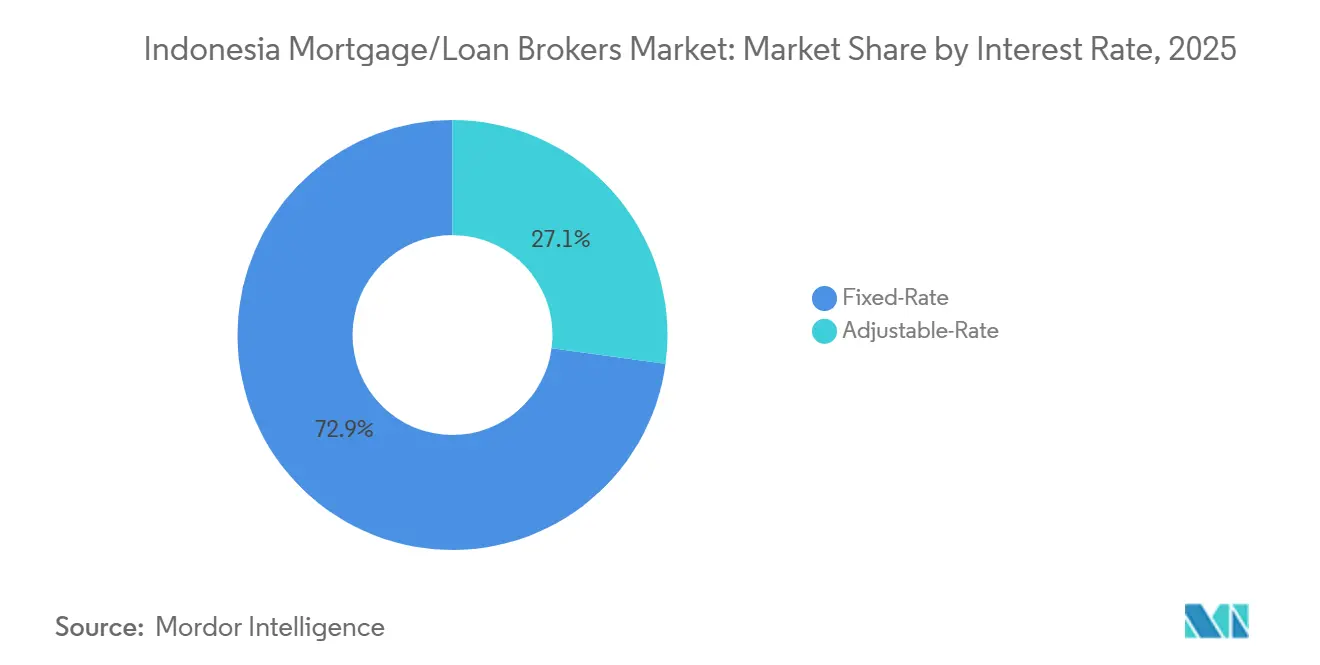

- By interest rate, fixed-rate mortgages accounted for 72.87% of the Indonesia mortgage/loan brokers market share in 2025, while adjustable-rate instruments posted an 11.27% growth rate.

- By provider, primary lenders represented 78.74% of the Indonesia mortgage/loan brokers market share in 2025, and secondary lenders grew the fastest at a 14.36% CAGR.

- By geography, Java captured a 57.85% of the Indonesia mortgage/loan brokers market share in 2025, while Sulawesi is the fastest-growing region with a projected 13.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Mortgage/Loan Brokers Market Trends and Insights

Drivers Impact Analysis

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class household income & first-time buyer demand | +2.1% | Java, Bali & Nusa Tenggara, with spillover to urban Sumatra | Medium term (2-4 years) |

| Government FLPP interest-subsidy program | +3.2% | National, concentrated in secondary cities such as Jember, Malang, Semarang, Surabaya | Short term (≤ 2 years) |

| Expansion of digital mortgage / fintech platforms | +1.8% | Greater Jakarta (Jabodetabek), urban Sumatra corridors | Medium term (2-4 years) |

| Declining Bank Indonesia benchmark rates | +1.5% | National with global context, rapid pass-through via primary lenders | Short term (≤ 2 years) |

| Urbanisation in secondary cities boosting broker coverage | +1.4% | Sulawesi, Kalimantan, Papua with early gains in Makassar, Manado, Balikpapan | Long term (≥ 4 years) |

| Growth of sharia-compliant mortgage offerings | +0.9% | National, with higher adoption in Aceh, West Java, West Sumatra | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Middle-Class Household Income and First-Time Buyer Demand

The Indonesia mortgage/loan brokers market benefits from a growing first-time buyer cohort that responds strongly to fixed-rate subsidies and simplified onboarding journeys that banks and partners deliver through digital simulators and prequalification tools. Subsidized mortgages structured at 5% fixed rates over long tenors have enabled the conversion of creditworthy households that might otherwise delay purchases, anchoring a steady origination base for brokers and lenders[2]Source: Bank Negara Indonesia, “Supporting the 3 Million Houses Program, BNI Distributes 109,000 Subsidized Mortgages,” Bank BNI, bni.co.id. Banks are scaling outreach by embedding mortgage offers within their super-app ecosystems, keeping early-stage leads engaged through calculators, document checklists, and branchless verification flows that cut the time to approval. Policy incentives, including high LTV flexibility where risk allows and liquidity incentives for housing credit, support purchasing power for younger buyers beyond Tier-1 cities. For the Indonesia mortgage/loan brokers market, the combination of targeted subsidies and digital origination has created a repeatable first-time buyer funnel that is less sensitive to small rate moves and more responsive to journey speed and certainty of approval.

Government FLPP Interest-Subsidy Program

The FLPP program continues to act as the single largest throughput engine for subsidized origination by locking a 5% fixed rate for eligible borrowers and channeling volume through distributing banks with defined quotas. BTN and other state-owned banks operationalize the pipeline at national scale and have used mass contract signings to secure future disbursements across dozens of provinces, enabling brokers to align with developers on predictable closings [3]Source: BP Tapera, “Pemerintah Percepat Akses Rumah Subsidi Lewat Sosialisasi Kredit Program Perumahan di Jawa Timur,” BP Tapera, tapera.go.id. The subsidy structure narrows the affordability gap relative to market-rate mortgages and encourages long-tenor selections, which reduces monthly installment burdens for first-time owners. Participating banks are building cross-sell programs around subsidized buyers, bundling insurance and payments to improve retention and life-time value within the Indonesia mortgage/loan brokers market. Policy continuity signaled by sector regulators and the social-housing mandate sustains multi-year visibility, which supports broker capacity planning and regional coverage models.

Expansion of Digital Mortgage and Fintech Platforms

Digital channels have moved from auxiliary to central for origination, documentation, and servicing, with leading banks integrating mortgage journeys into their retail apps that already handle the majority of customer transactions. BCA’s myBCA platform added NFC Tap capabilities and cross-border QR features, signaling deeper reliance on mobile identity and payments rails that can also support mortgage verification and fee collection steps within the same interface. Aggregation models and property platforms are embedding prequalification and lender comparisons, improving lead quality for brokers while reducing duplicate processing. The Bank Indonesia Macroprudential Liquidity Incentive has steered sizable liquidity toward housing and related sectors, strengthening the economics of co-lending and bank-fintech origination partnerships within the Indonesia mortgage/loan brokers market. OJK’s supervisory stance codifies the broader digital financing ecosystem and supports technology adoption by licensed intermediaries that work directly with property developers and agents.

Declining Bank Indonesia Benchmark Rates

Bank Indonesia cut the policy rate cumulatively by 150 bps from September 2024 through December 2025, and the policy stance in late 2025 supported liquidity and credit expansion objectives while maintaining stability [4]Source: Bank Indonesia Communication Department, “BI-Rate Held at 4.75%: Maintaining Stability, Strengthening Economic Growth,” Bank Indonesia, bi.go.id. BI lifted the maximum KLM incentive to 5% of third-party funds and earmarked a larger allocation for housing, which reinforced lenders’ willingness to grow mortgage books in line with risk appetite. KSSK guidance maintained favorable LTV ceilings into 2026 subject to bank-level risk assessment, and that framework enabled zero-to-low down-payment mortgages when banks deemed borrower profiles sound. For the Indonesian mortgage/loan brokers market, rate stability combined with macroprudential incentives places more weight on journey speed, documentation readiness, and refinancing advisories as differentiators rather than on headline rate moves alone.

Restraints Impact Analysis

| Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent loan-to-value caps from OJK | -0.7% | National, with heightened enforcement in Java for non-subsidized loans | Medium term (2-4 years) |

| High informal-sector employment complicates underwriting | -1.3% | National, particularly acute in Papua, Kalimantan, Sulawesi | Long term (≥ 4 years) |

| Limited credit-bureau penetration raises risk costs | -0.9% | National; regulatory push via SLIK expansion underway | Medium term (2-4 years) |

| Slow building-permit process and land-bank issues | -0.6% | Jakarta, Jabodetabek; supply-side bottleneck | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Loan-to-Value Caps from OJK

OJK and KSSK maintained accommodative LTV ceilings into 2026, but individual banks set stricter internal thresholds in response to rising consumer risk indicators, which raised effective down-payment burdens for non-subsidized borrowers. BCA disclosed tighter underwriting during 2025 and raised select LTV requirements for non-subsidized channels, aligning origination with risk-adjusted return goals. Bank Indonesia’s Q3 2025 Banking Survey signaled more cautious lending standards industry-wide, with tighter collateral and ceiling requirements echoing through broker pipelines. In the Indonesia mortgage/loan brokers market, higher rejection rates and longer application cycles become more likely when borrower credit files are thin or debt-service profiles are borderline, despite policy headroom for LTV at the macro level. Brokers respond by pre-screening applicants more intensively and coaching on documentation to ensure a cleaner first submission that aligns with lender risk thresholds.

High Informal-Sector Employment Complicates Underwriting

A large share of the labor force earns income outside formal payroll systems, challenging legacy credit models that rely on regular payslips and consistent tax documentation. OJK has advanced inclusion measures that allow alternative documentation and promote partnerships with credit-guarantee and alternative scoring institutions to expand responsible access to housing finance. BTN and other state-owned banks have piloted savings-linked and cooperative structures for gig workers and micro-entrepreneurs, channeling regular deposits and transaction histories into mortgage eligibility while preserving prudent risk management. The FLPP framework further supports dedicated allocations for lower-income and non-salaried borrowers through bank quotas and standardized origination protocols that brokers can navigate at scale. The Indonesia mortgage/loan brokers market adapts by integrating prequalification APIs and document-coaching workflows that turn heterogeneous earnings data into formats that align with lender underwriting engines.

Segment Analysis

By Type of Mortgage Loan: Government guarantees outpace conventional volume growth

Conventional mortgage loans held 59.44% share in 2025, reflecting the entrenched role of market-rate products across urban and suburban borrower segments within the Indonesia mortgage/loan brokers market. Government-insured mortgages are positioned as the growth engine, with a projected 13.47% CAGR through 2031, due to sustained FLPP quotas that support fixed-rate pricing and predictable closing cycles for developers and banks. BTN anchors the subsidized pipeline and has built operational capacity to distribute down-payment assistance and interest subsidies, which has encouraged brokers to align buyer funnels with bank quota timetables. Jumbo loans remain a niche among affluent buyers in Greater Jakarta and select tourism corridors, where price levels and cash-flow profiles support larger tickets without subsidy reliance, and brokers match borrowers to premium lender service lines. Refinancing and top-up products have benefited from BI’s cumulative 150 bps easing cycle since late 2024, creating windows for rate and tenor optimization that brokers monetize via retention or lender-switch strategies.

As FLPP quotas move into secondary cities, brokers can direct buyer flows toward projects with faster handovers and clearer title conditions, which also lowers fall-through risk. Conventional volumes continue to supply the base of the Indonesia mortgage/loan brokers industry, and lenders differentiate with bundled insurance, fee waivers, and loyalty features to defend share against subsidized pull. Brokers bridge these paths by segmenting buyers early and routing them to the most efficient track, which improves approval rates and reduces the cycle time from property search to bank agreement. With macroprudential liquidity support in place, the balance between subsidized growth and conventional depth is likely to persist, preserving demand across diverse borrower profiles within the Indonesia mortgage/loan brokers market.

Note: Segment shares of all individual segments available upon report purchase

By Mortgage Loan Terms: Longer tenors dominate, yet mid-duration options gain traction

Thirty-year tenors commanded 66.38% share in 2025, reflecting borrower preferences for affordability through lower monthly installments in a market where income smoothing matters for first-time owners. Subsidized frameworks and public savings schemes have enabled durable long-tenor adoption, and brokers standardize these choices for buyers that prioritize payment stability over accelerated equity build. The Indonesia mortgage/loan brokers market has also seen mid-duration options gain visibility as banks promote structured fixed windows with clear reprice rules, which appeal to emerging affluent households. Banks’ digital channels present tenor tradeoffs transparently at the prequalification stage, improving decision confidence and reducing rework from late-stage tenor changes. The combination of standardized subsidy tenors and flexible conventional offers keeps the funnel broad, with brokers guiding households toward the tenor that fits income trajectories and rate views.

The Indonesia mortgage/loan brokers market size for 15-year maturities is advancing at a 14.38% CAGR, supported by bank campaigns that pair shorter tenors with promotional fixed windows to accelerate principal reduction. Twenty-year products remain important among salaried borrowers with steady income visibility, and brokers use lender calculators to show total-interest differences that inform tenor selection without introducing adverse payment shocks. Where buyers anticipate income step-ups, brokers sometimes position mid-tenor paths with refinancing checkpoints that keep long-run costs aligned with household preferences. Rate stability and policy clarity further lower uncertainty around tenor decisions, narrowing the gap between affordability and equity speed within the Indonesia mortgage/loan brokers market. Journey management at the broker level has become essential, since tenor selection influences underwriting routes, documentation stacks, and time to bank agreement.

By Interest Rate: Fixed-rate subsidies anchor share, adjustable instruments catch repricing wave

Fixed-rate mortgages held 72.87% of 2025 originations, anchored by the FLPP’s 5% fixed structure and bank promotions that guarantee rate certainty for an initial period before any reset. The subsidy’s pricing advantage versus market rates helps first-time buyers lock in affordability and reduces default risk related to payment shocks, reinforcing broker recommendations for fixed paths in subsidy-eligible cases. Banks have also introduced one-to-three-year fixed promotions within conventional KPR lines to attract customers early in the rate cycle, a strategy that brokers use to monetize pre-approvals into timely closings. Adjustable-rate mortgages are growing as lenders reprice legacy books following BI’s easing moves and as some borrowers position for future repricing windows with lower initial monthly costs. Hybrid structures, which combine a short fixed window followed by floating, remain a middle path that brokers explain in detail to align expectations with rate scenarios and repayment capacity.

The Indonesia mortgage/loan brokers market benefits from rate option diversity, and brokers have built rate-education steps into their flows so first-time buyers understand tradeoffs between predictability and potential savings over the full term. Where subsidy eligibility is absent, banks’ promotional fixed windows often become the default path to reduce early-stage payment strain and increase approval likelihood. As BI maintains a stable stance, lenders can balance growth with risk controls, and brokers can time refinancing advisories where rate resets approach and household income visibility has improved. Sharia-compliant profit-sharing contracts have tracked broader housing finance expansion and cater to regions with higher Islamic finance adoption, adding another option set to broker playbooks. The net effect is a rate landscape where fixed anchors subsidized demand, and floating instruments and hybrids add flexibility within the Indonesia mortgage/loan brokers market.

By Provider: Primary lenders leverage branch reach; secondary players scale through digital channels

Primary lenders accounted for 78.74% of 2025 origination, reflecting the branch reach, legacy customer bases, and quota-driven subsidy distribution capacity of state-owned banks and leading private banks. BRI and BCA reported healthy mortgage books through 2025, with underwriting calibrated to risk-adjusted returns and digital channels handling the majority of retail transactions supporting ancillary mortgage workflows. Bank Mandiri’s digital platform has scaled user adoption and embedded prequalification in its broader retail journey, creating a path for integrated origination and servicing that brokers can tap. Secondary lenders, including digital aggregators and P2P-linked originators working under tightened prudential standards, continue to take share by focusing on speed, transparency, and specialized borrower segments. The BI KLM facility, which directed substantial liquidity toward priority sectors including housing through 2025, has supported collaboration across lender tiers in the Indonesia mortgage/loan brokers market.

Secondary channels deploy prequalification APIs, document coaching, and marketplace integrations that surface lender choices to consumers at the search stage, reducing time-to-approval and improving match quality for bank underwriters. OJK’s ongoing framework for digital financing and information systems has clarified the roles and standards for technology-based originators and aggregators, which strengthens consumer protections and data sharing while expanding origination capacity. For primary lenders, partnership models with credible aggregators reduce acquisition costs and extend reach into secondary cities without duplicating physical branches. The Indonesia mortgage/loan brokers market shows that branch presence, digital funnels, and subsidy quotas are complementary rather than mutually exclusive when orchestrated through bank and broker ecosystems. As lenders refine underwriting automation and data pipelines, broker value shifts toward advisory, documentation quality, and routing efficiency within both subsidized and conventional lanes of the Indonesia mortgage/loan brokers industry.

Geography Analysis

Java accounted for 57.85% of 2025 originations, reflecting metropolitan density and the concentration of developers and lender networks in Jakarta, Surabaya, Bandung, and Semarang within the Indonesia mortgage/loan brokers market. BTN’s footprint in East Java, including subsidized units distributed under the FLPP umbrella, underscores the island’s scale and the operational predictability that brokers seek when closing volumes at pace. BCA’s portfolio data highlight regional loan exposure concentrated around Jakarta, reflecting the gravity of the Greater Jakarta region in lender strategies and broker routing. Outside Java, urban corridors in Sumatra and industrial hubs in Kalimantan continue to create pockets of stable demand that brokers engage using digital prequalification and developer partnerships. The Indonesia mortgage/loan brokers market remains anchored in Java for volume, while growth rotates to regions with targeted infrastructure and branch expansions.

Sulawesi is projected to expand at a 13.47% CAGR through 2031, reflecting sustained urbanization and logistics expansion in cities like Makassar where broker coverage and bank presence have increased. OJK’s TPAKD operates across all districts and cities, and that institutional presence supports financial access programs that brokers rely on to reach underserved provinces cost-effectively. Urbanization has advanced nationally and continues to shape housing demand in secondary cities where relative affordability and new projects align with subsidy eligibility and lender appetite. In Kalimantan and eastern provinces, brokers balance pipeline ambition with local land-title diligence and project stage certainty to reduce fall-through risks. Aggregation models help maintain lead quality where physical branches are sparse by collecting standardized documents and managing borrower communications centrally.

The Indonesia mortgage/loan brokers market size for Java reflects a 57.85% share in 2025, while regions like Sulawesi are positioned as growth leaders through 2031, creating a two-speed map for origination strategies. In Bali and Nusa Tenggara, specialized segments serve tourism-linked and expatriate-adjacent demand, with Islamic financing also present in line with demographic preferences. Papua remains the smallest segment given land-tenure complexities and limited bank presence outside key cities, reinforcing the role of digital funnels in early-stage screening. As banks and brokers coordinate quotas and campaigns, the emphasis shifts toward outreach, documentation quality, and project selection that align with policy signals and local infrastructure plans.

Competitive Landscape

The Indonesia mortgage/loan brokers market is characterized by medium concentration, with state-owned banks and BCA leading primary origination, especially in subsidized channels where quota allocations and operational scale matter most for throughput. BCA reported mortgage balances and digital usage that underline the centrality of its mobile ecosystem to customer engagement and product cross-sell, including service upgrades that support mortgage journey steps. BRI disclosed solid growth in its mortgage book through 1H 2025, supported by subsidized programs and promotional offers for premium segments, showing a dual-track approach to portfolio building. Bank Mandiri’s digital platform processed the vast majority of retail transactions by 2025, and the bank integrated mortgage prequalification and ecosystem payments to streamline acquisition and servicing. BTN remains a policy anchor for subsidized housing finance through its distribution capabilities and sustainable finance framework, which supported a structured approach to green and social housing credits.

Competition has shifted from pure price-based tactics to orchestrating end-to-end ecosystems that bundle insurance, payments, and developer relationships into a single journey that increases conversion and retention within the Indonesia mortgage/loan brokers market. OJK rules have tightened prudential and operational standards for digital financing, data use, and system control, which lifted sector discipline and clarified the role of aggregators as licensed partners within lender workflows. Bank Indonesia’s liquidity incentives for housing have reinforced co-lending and partnership economics by lowering effective funding frictions for priority segments. As lenders automate more of underwriting and monitoring, brokers differentiate on documentation quality, cycle-time management, and advisory that aligns loan structure with household income stability and rate outlooks. The rise of embedded finance within property search portals tightens collaboration between brokers, developers, and banks, and shifts acquisition economics toward lower-cost, higher-certainty channels.

Inclusion policies are broadening sustainable access while preserving risk controls, with OJK’s frameworks for UMKM, guarantees, and sustainable finance aligning banks and brokers around responsible growth in subsidized and conventional tiers. Sharia banking continues to add depth, and ESG-linked structures have mobilized capital for green and social housing projects that connect with mortgage pipelines across regions. The Indonesia mortgage/loan brokers market integrates these policy and technology vectors as competitive levers rather than constraints, producing a field where incumbents and digital-centric players collaborate and compete simultaneously. Execution quality in documentation, quota alignment, and post-origination servicing is steadily becoming the decisive factor for share capture across product and regional lines. As lenders keep a close watch on NPL trends and margin discipline, brokers that deliver stronger files and shorter cycles are better positioned to negotiate preferred routing and service levels within partner banks.

Indonesia Mortgage/Loan Brokers Industry Leaders

PT Bank Mandiri (Tbk)

PT Bank Rakyat Indonesia (Tbk)

PT Bank Central Asia (Tbk)

PT Bank Negara Indonesia (Tbk)

PT Bank Tabungan Negara (Tbk)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: PT Bank Central Asia (BCA) reported that its mortgage loans outstanding reached Rp 138.8 trillion as of September 2025, supported by overall loan growth and solid asset quality performance through the first nine months of the year.

- December 2025: Bank Central Asia expanded NFC-enabled QRIS Tap payments on the myBCA app for use across public transportation and parking services (e.g., TransJakarta, MRT, LRT), enhancing contactless digital payment experiences within Greater Jakarta and beyond.

- September 2024: Otoritas Jasa Keuangan (OJK) issued Peraturan OJK No. 19 Tahun 2025 on Facilitating Access to Financing for Micro, Small, and Medium Enterprises (UMKM), requiring banks and financial firms to simplify and accelerate MSME credit processes available to a broad range of institutions.

- September 2024: A pilot of cross-border QR payment linkage between China and Indonesia was launched under the guidance of both nations’ central banks, enabling QRIS-based transactions with UnionPay and Alipay apps at over 40 million Indonesian merchants during the sandbox phase.

Indonesia Mortgage/Loan Brokers Market Report Scope

A mortgage is a loan used to purchase or maintain a home, land, or other real estate types; the property then serves as collateral to secure the loan. The mortgage loan market is an area that needs to be focussed in indonesia, with some factors lying in favor of the market and some against it.

Indonesia mortgage/loan brokers market is segmented by type of mortgage loan, mortgage loan terms, interest rate, and provider. By type of mortgage loan, the market is sub-segmented into conventional mortgage loans, jumbo loans, government-insured mortgage loans, and other types of mortgage loans. By mortgage loan terms, the market is sub-segmented into 30-year mortgages, 20-year mortgages, 15-year mortgages, and other mortgage loan terms. By interest rate, the market is sub-segmented into fixed-rate mortgage loans and adjustable-rate mortgage loans. By provider, the market is sub-segmented into primary mortgage lenders and secondary mortgage lenders. The report offers market size and forecasts for the Indonesia mortgage/loan brokers market in value (USD) for all the above segments.

| Conventional Mortgage Loan |

| Jumbo Loans |

| Government-Insured Mortgage Loans |

| Other Types of Mortgage Loan |

| 30-Year Mortgage |

| 20-Year Mortgage |

| 15-Year Mortgage |

| Other Mortgage Loan Terms |

| Fixed-Rate |

| Adjustable-Rate |

| Primary Mortgage Lender |

| Secondary Mortgage Lender |

| Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Bali & Nusa Tenggara |

| Papua |

| By Type of Mortgage Loan | Conventional Mortgage Loan |

| Jumbo Loans | |

| Government-Insured Mortgage Loans | |

| Other Types of Mortgage Loan | |

| By Mortgage Loan Terms | 30-Year Mortgage |

| 20-Year Mortgage | |

| 15-Year Mortgage | |

| Other Mortgage Loan Terms | |

| By Interest Rate | Fixed-Rate |

| Adjustable-Rate | |

| By Provider | Primary Mortgage Lender |

| Secondary Mortgage Lender | |

| By Geography | Java |

| Sumatra | |

| Kalimantan | |

| Sulawesi | |

| Bali & Nusa Tenggara | |

| Papua |

Key Questions Answered in the Report

What is the size and growth outlook for the Indonesia mortgage/loan brokers market through 2031?

The Indonesia mortgage/loan brokers market size is USD 24.39 billion in 2026 and is projected to reach USD 37.94 billion by 2031 at a 9.24% CAGR

Which loan types are leading and which are growing fastest in the Indonesia mortgage/loan brokers market?

Conventional products led with 59.44% share in 2025 while government-insured mortgages are the fastest-growing at a 13.47% CAGR through 2031

How are interest rates shaping borrower choices within the Indonesia mortgage/loan brokers market?

Fixed-rate mortgages held 72.87% of 2025 originations due to the FLPP 5% structure and bank fixed-window promotions, while adjustable-rate products are growing on the back of BI’s easing cycle

Which regions should lenders and brokers prioritize for growth?

Java captured 57.85% share in 2025 for scale, but Sulawesi is the fastest-growing with a 13.47% projected CAGR, supported by urbanization and expanding bank coverage

What policy programs most influence origination volumes today?

The FLPP subsidy program anchors fixed-rate affordability and quotas, and BI’s Macroprudential Liquidity Incentive channels liquidity to housing, which together stabilize origination pipelines