Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

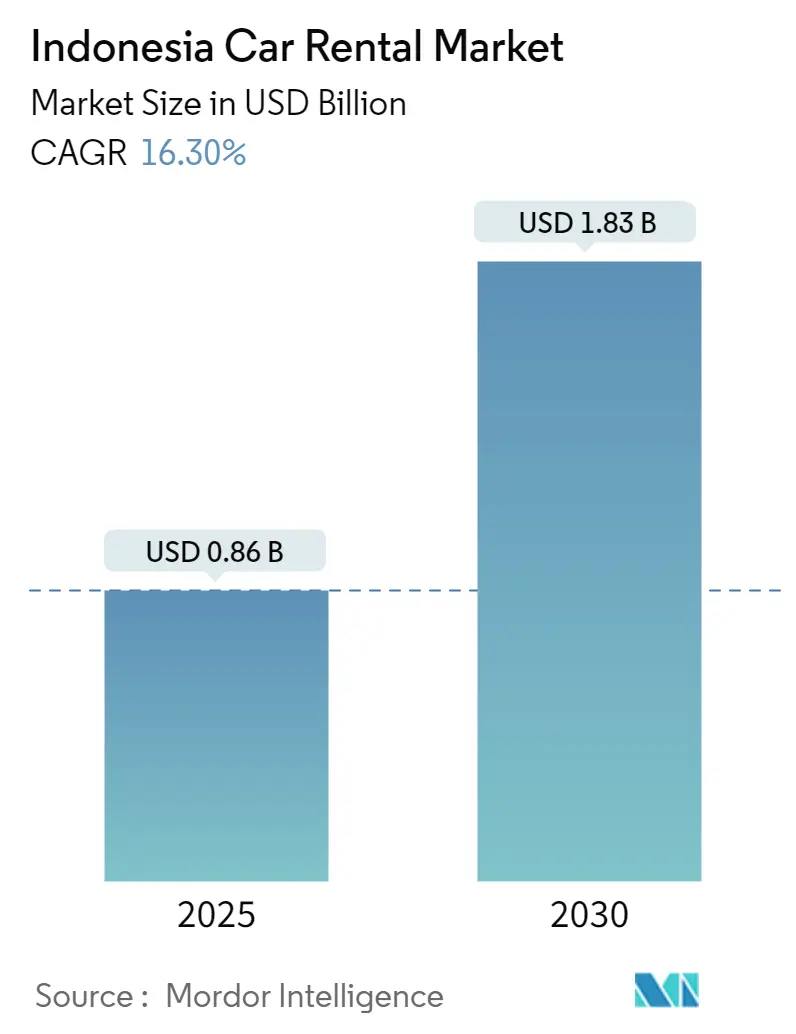

| Market Size (2025) | USD 0.86 Billion |

| Market Size (2030) | USD 1.83 Billion |

| Growth Rate (2025 - 2030) | 16.30% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia Car Rental Market Analysis by Mordor Intelligence

The Indonesian car rental market size stood at USD 0.86 billion in 2025 and is forecast to reach USD 1.83 billion by 2030, advancing at a 16.3% CAGR. Over the next five years, rising disposable incomes, expanding middle-class travel budgets, and widespread smartphone adoption set a favorable backdrop for sustained double-digit growth. The government’s target of welcoming between 14.6 and 16 million foreign visitors in 2025, up from 13.9 million in 2024, signals resilient tourism demand even as business travel rebounds on the back of Indonesia’s 5.05% GDP growth in 2024. Online platforms are redefining customer expectations around transparency, on-demand availability, and digital payments, while new incentives for battery-electric vehicles (BEVs) position electrification as a future profit pool. Competitive pressure intensifies as app-based mobility ecosystems blur the line between ride-hailing and daily rentals, prompting traditional operators to accelerate fleet modernization and data-driven pricing strategies.

Key Report Takeaways

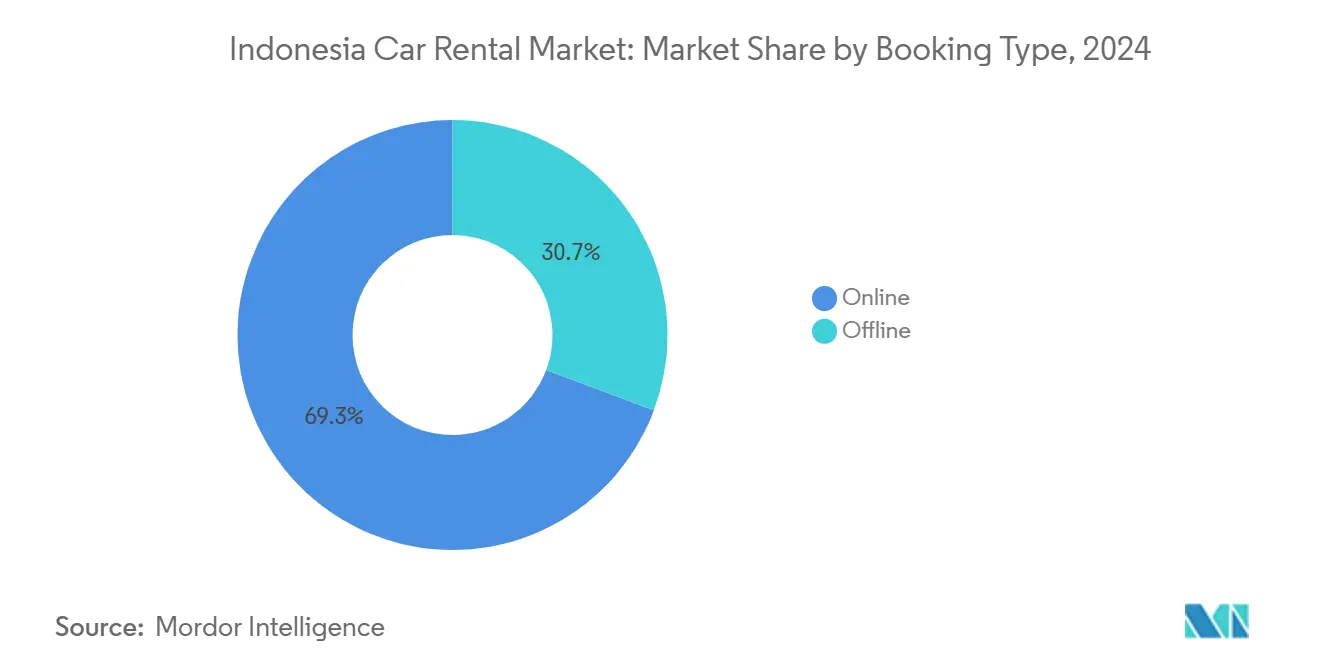

- By booking type, online channels held a 69.33% share of the Indonesia car rental market in 2024 and are expected to post the fastest growth at a 17.14% CAGR through 2030.

- By rental duration, the short-term segment captured 58.41% share of the Indonesia car rental market in 2024, yet long-term contracts are projected to accelerate at a 17.48% CAGR to 2030.

- By application, tourism and leisure dominated the Indonesia car rental market in 2024, with a 64.46% share, whereas corporate mobility is forecast to grow at an 18.04% CAGR over the same horizon.

- By vehicle type, economy and hatchback models led with 45.33% share in the Indonesia car rental market in 2024; SUVs are the fastest-growing category, expanding at a 17.86% CAGR to 2030.

- By fuel type, Petrol ICE cars accounted for 79.56% share in the Indonesia car rental market in 2024, while BEVs are projected to surge at a 19.15% CAGR.

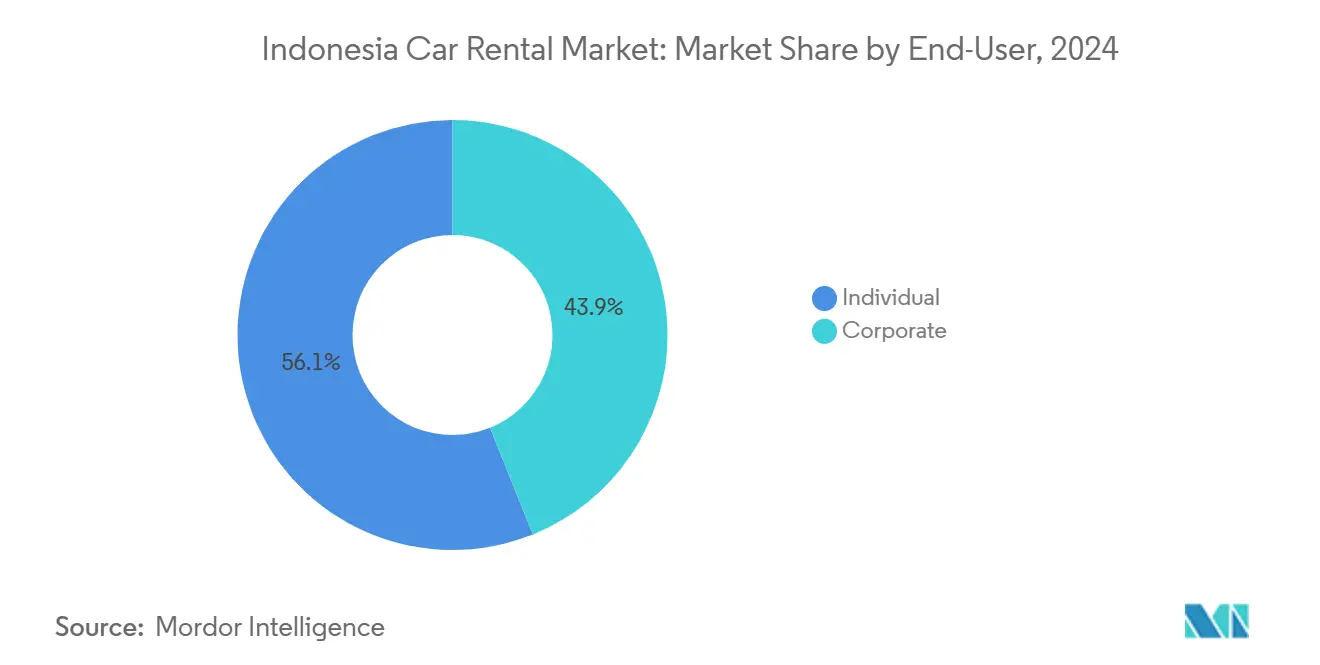

- By end-user, individuals represented 56.13% share in the Indonesia car rental market in 2024; corporate accounts will log the highest growth, rising at an 18.44% CAGR through 2030.

- By rental channel, aggregators controlled 72.44% share in the Indonesia car rental market in 2024, but super-app bundles will see the quickest lift with a 17.8% CAGR.

- By region, Java account for 62.16% share in the Indonesia car rental market in 2024; Bali and Nusa Tenggara are poised for the fastest expansion at an 18.87% CAGR.

Indonesia Car Rental Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Tourist Arrivals | +3.2% | Java, Bali, and emerging leisure corridors | Medium term (2-4 years) |

| Digital Booking Platforms Surge | +2.8% | National, with highest penetration in major metro areas | Short term (≤2 years) |

| Firms Drive Leasing Demand | +2.5% | Jakarta, Surabaya, and secondary business hubs | Medium term (2-4 years) |

| EV Roadmap Accelerates Electrification | +2.1% | Jakarta and other provincial capitals | Long term (≥4 years) |

| Halal Packages Boost Niche Tourism | +1.9% | Nationwide, especially Islamic heritage destinations | Long term (≥4 years) |

| Airports Expanding Connectivity | +1.7% | Emerging tourism corridors around upgraded regional airports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising International and Domestic Tourist Arrivals

In 2024, Indonesia welcomed around 13.9 million international visitors and recorded over 1 billion domestic journeys, marking a swift rebound in its tourism sector following the easing of border restrictions. The Ministry of Tourism projects inbound visitors will rise to between 14.6 and 16 million in 2025, supported by visa-on-arrival expansion and marketing of the “10 New Balis” destinations. Significant capital investment in Komodo, Lombok, and other regional airports increases seat capacity and disperses travel flows beyond Java. The World Travel & Tourism Council projects the sector will contribute 4.6% to GDP in 2025[1]“Indonesia 2024 Annual Research,” World Travel & Tourism Council, wttc.org. A larger tourist base directly lifts self-drive rentals and chauffeured packages, particularly in islands where public transport is limited.

Surge in Digital-First Booking Platforms

In 2024, Indonesia's digital economy hit the USD 90 billion mark, buoyed by a surge in e-commerce transactions, with projections indicating further growth[2]“e-Commerce Statistics of Asia Pacific 2024,” Asian Development Bank, adb.org. Online rental bookings accounted for a substantial share of the overall transactions in 2024 and are growing significantly annually as consumers gravitate to super-apps offering instant price comparison, cashless payments, and loyalty rewards. Partnerships like Blue Bird taxis integrating with Gojek allow legacy fleets to unlock a nationwide customer base while cutting acquisition costs. Aggregators use rich data to fine-tune dynamic pricing, optimize fleet utilization, and upsell insurance or ancillary services in real time.

Growing Corporate Demand for Long-Term Operational Leasing

Large domestic firms and multinational subsidiaries increasingly outsource vehicle ownership to avoid capital outlays and residual-value risk. Government entities like Keerom District pioneered annual operating leases instead of purchasing official cars, citing lower lifecycle costs. Foreign direct investors, able to complete licensing within 1.5 months after the Omnibus Law reforms, require immediate fleet availability for executives and expatriates. Long-term contracts lock in predictable monthly fees while bundling insurance, preventive maintenance, and driver management, creating high-margin recurring revenue for fleet operators.

Government EV Roadmap Accelerating Fleet Electrification

Numerous manufacturers now offer various BEV models at varying price points to Indonesian car consumers. The surge in this market can be traced back to Presidential Regulation No. 55/2019, which introduced fiscal and non-fiscal incentives to bolster domestic electric vehicle production. Building on this momentum, Presidential Regulation No. 79/2023 expanded these incentives and made BEVs more wallet-friendly for consumers. Further sweetening the deal, the Ministry of Finance Regulation No.38/2023 slashed the value-added tax on new passenger electric vehicles from 11% to 1%. Due to these tax breaks, both the value-added tax reduction and the luxury tax exemption, BEV prices have seen a dip, leading to a surge in sales of battery electric passenger cars, buses, and motorcycles [3]Tenny Kristiana, “Policies to help Indonesia’s new president champion electric vehicles,” International Council on Clean Transportation, theicct.org. The national plan targets 600,000 BEVs and 2.45 million electric two-wheelers by 2030, backed by a public-charging build-out of 846 car stations and 1,401 battery-swap depots for motorcycles. Rental agencies introducing BEVs gain access to preferential parking and bus-lane exemptions in Jakarta, while corporate clients use low-emission vehicles to burnish ESG credentials and trim fuel costs.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short-Term Rental Market Cannibalized | -2.3% | Jakarta, Surabaya, Medan, and other large metropolitan areas | Medium term (2-4 years) |

| Competitors Wage Intense Price War | -1.8% | National, highest intensity in Java and major urban centers | Short term (≤2 years) |

| Congestion Deters Self-Driving Options | -1.5% | Jakarta metropolitan area and other densely populated cities | Long term (≥4 years) |

| Regulatory Burden Fragments Regional Markets | -1.2% | Nationwide, with variations across provincial jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ride-Hailing Super-Apps Cannibalizing Short-Term Rentals

Grab and Gojek processed a significant number of on-demand rides in Indonesia during 2024. A proposed Grab-GoTo tie-up could deepen network effects, bundling deliveries, payments, and ride-sharing into a single wallet. Urban consumers prefer door-to-door rides over self-drive rentals to avoid congestion fees and parking scarcity. Corporate travelers also book ride-hailing through expense-management dashboards, bypassing traditional airport pickup counters. To stay relevant, rental firms are exploring hourly packages, loyalty linkage with airlines, and premium SUVs to serve niches less exposed to app-based commoditization.

Intensifying Price-Led Competition Among Incumbents

Indonesia hosts hundreds of registered rental firms and many operating fleets. As online aggregators standardize price displays, operators undercut one another, weakening margins. Blue Bird Group has responded with tiered pricing and value-added chauffeur packages, but still reports downward pressure on daily rates in Jabodetabek. Smaller regional players lack scale for fleet renewal and must absorb rising VAT, which climbs to a considerable share in 2025, squeezing net profit. Consolidation is expected, with larger fleets leveraging bulk procurement discounts and telematics to extract operating efficiencies.

Segment Analysis

By Booking Type: Online Penetration Redefines the Experience

Online channels generated 69.33% of the Indonesian car rental market revenue in 2024, climbing at a 17.14% CAGR. The dominance reflects deep smartphone penetration, a cashless payment boom, and consumer comfort with super-apps integrating trip planning, mapping, and digital wallets. Indonesia's car rental market size, attributed to offline travel-agency counters, remained at significant revenue in 2024 but is losing share as small operators list fleets on aggregator portals to reach price-sensitive tourists.

Super-app ecosystems combine ride-hailing, food delivery, and digital banking, encouraging cross-selling day-long rental packages. Legacy brands adopt cloud-based reservation engines, push-notification discounts, and AI-enabled customer-service chatbots to match the user experience of tech platforms. Data captured online allows segmentation by nationality, trip purpose, and spend, enabling operators to A/B test mileage caps or bundle Wi-Fi routers for incremental revenue.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Rental Duration: Long-Term Leasing Gains Corporate Favor

Short-term bookings, defined as rentals lasting 1–30 days, held a 58.41% share in the Indonesian car rental market in 2024 due to seasonal tourism peaks. Long-term contracts generated notable revenue in the Indonesian car rental market in 2024 and are projected to grow at a 17.48% CAGR. Corporations adopt operating leases to preserve capital and shift maintenance responsibilities to service providers.

Long-term packages typically include driver salaries, periodic servicing, and full insurance, insulating clients from residual-value swings. Fleet managers deploy telematics to monitor fuel consumption and preventive maintenance, reducing downtime. The trend also anchors used-vehicle disposal channels, where cars aged three to five years are auctioned or sold to ride-hailing drivers, recouping capital faster than private resales.

By Application: Corporate Mobility Catches Up with Tourism

Tourism accounted for 64.46% of revenue in 2024; however, business mobility is on course to become the next growth engine, expanding at an 18.04% CAGR. Indonesia’s investment-grade rating and quick licensing approvals spur multinational relocations, raising demand for executive transfers, project-site shuttles, and expatriate family transport. Daily commuting packages for factory staff and shared vans for BPO workers also widen addressable volumes.

Tourism bookings concentrate in Bali, Yogyakarta, and Lombok, where self-drive packages include itinerary curation and GPS navigation in multiple languages. Car rental firms tailor airport meet-and-greet services, fast-track SIM card kits, and 24/7 roadside assistance, leveraging Indonesia’s archipelagic geography and limited inter-city rail. In parallel, corporate contracts diversify income, cushioning seasonality and yielding predictable fleet-utilization ratios.

By Vehicle Type: SUV Momentum Amid Economy Dominance

Economy cars and hatchbacks delivered 45.33% of revenue in 2024, due to competitive daily rates and fuel efficiency. SUVs, however, are the fastest climbers, expanding to 17.86% CAGR as middle-income families seek higher ground clearance for varied road conditions and enhanced safety features. Indonesia's car rental market held by SUVs will keep growing as domestic tourism shifts toward adventure destinations.

The rise of premium SUVs supports higher daily tariffs and bundled driver packages, widening gross margins. MPVs remain popular for group travel, while luxury sedans see niche demand from corporate executives and diplomatic missions. Fleet managers optimize model mix using demand-prediction algorithms that weigh seasonality, regional terrain, and traveler demographics.

By Fuel Type: EV Uptake Accelerating from a Small Base

Petrol ICE vehicles dominated 79.56% share of the Indonesia car rental market in 2024. Battery-electric vehicles, though still small, are ramping quickest at a 19.15% CAGR. Indonesian Jakarta’s exemption of BEVs from odd-even traffic restrictions provides a tangible consumer benefit, translating into higher weekday utilization.

Rental firms partner with utility PLN to install depot chargers and negotiate bulk electricity tariffs. Hybrids gain traction among inter-city travelers wary of charging infrastructure gaps but keen to cut fuel bills. Diesel remains relevant for high-torque commercial vans servicing logistics and plantation sites, yet government roadmaps indicate a gradual phase-down beyond 2030.

By End-User: Corporates Steer Growth

Individuals accounted for 56.13% of bookings in 2024, reflecting leisure travel dominance. Corporate rental services will expand at an 18.44% CAGR, lifted by outsourcing trends. Indonesia car rental industry leaders negotiate framework agreements that bundle multi-year leases, driver management, and roadside assistance, sparing CFOs the burden of fleet depreciation forecasting.

Expatriate demand is particularly sticky; packages include registration, driver licensing, and cultural-orientation add-ons. SMEs join pool-leasing programs offering shared access to a common fleet, trimming idle time and aligning car availability with project cycles.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Rental Channel: Aggregators Maintain the Lead

Aggregator platforms such as Traveloka and Tiket.com aggregated 72.44% of the Indonesia car rental market revenue in 2024, projected to expand at a 16.76% CAGR, benefitting from SEO dominance and bundled flight-plus-car packages. Direct-to-consumer websites of large fleets retained a significant share, relying on brand equity and bespoke corporate portals.

Aggregators leverage user reviews, price alerts, and 24-hour cancellation to build trust, while fleet owners capture higher yields on direct channels via cross-selling insurance and GPS add-ons. The prospect of a Grab–GoTo alliance may merge ride-hailing and short-term rental inventories, prompting independent operators to differentiate through chauffeur quality, multilingual hotlines, and optional in-car Wi-Fi.

Geography Analysis

Java generated 62.16% of 2024 revenue, anchored by the Jabodetabek megapolitan, where international tourists land and a corporate headquarters cluster. Daily utilization, though, is tempered by Jakarta’s heavy congestion, odd-even license-plate restrictions, and steep parking fees, encouraging operators to rotate surplus units to Bandung or Semarang on weekends. Government efforts to boost public transport ridership have not stemmed private-vehicle dependency, ensuring steady baseline demand for rentals.

Bali and Nusa Tenggara will outpace all islands at an 18.87% CAGR through 2030. Under the “10 New Balis” initiative, new runways and terminal upgrades expand direct international connectivity, channeling tourists to Labuan Bajo, Mandalika, and Lake Toba. First movers in these locations secure airport counter exclusivity and long-term concessions for on-site charging bays, positioning fleets ahead of rivals.

Sumatra logged a significant share in 2024, driven by industrial provinces such as Riau and North Sumatra, while Kalimantan, Sulawesi, Maluku, and Papua collectively accounted for the remainder. Relocating the national capital to East Kalimantan is expected to spur corporate-fleet demand and public-sector vehicle leasing starting in 2026, though infrastructure bottlenecks and complex licensing slow immediate take-up.

Competitive Landscape

Indonesia’s car rental arena features a mix of national champions, regional specialists, and app-native aggregators, yielding a moderate level of fragmentation. Astra International’s TRAC division leverages exclusive Toyota distribution rights to secure volume discounts and maintain high fleet-rotation speed, while Blue Bird Group emphasizes service quality, centralized dispatch, and chauffeur professionalism in the premium segment. At the same time, International entrants like Sumitomo Mitsui Auto Service launched ventures in 2024 to tap into the accelerating long-term lease demand, banking on Japanese OEM relationships.

Technology investment differentiates winners. Fleet leaders deploy IoT devices for predictive maintenance and geofencing, cutting downtime significantly. AI-driven yield management adjusts rates hourly to match search traffic, seasonality, and competitor pricing. Smaller players unable to fund such systems risk relegation to fleet-subcontractor roles or face acquisition.

The looming Grab–GoTo consolidation threatens to forge a mobility super-app with scale advantages in data, payments, and marketing, potentially squeezing traditional rental profits unless they ally with the platform or carve out specialized niches such as halal tourism or electric minibuses. Foreign operators eyeing market entry benefit from Omnibus Law rule changes that allow a notable share of foreign equity in transportation services, provided the minimum paid-in capital of IDR 2.5 billion (~0.15 million) is met.

Indonesia Car Rental Industry Leaders

-

TRAC Astra Rent A Car

-

Blue Bird Group

-

Adi Sarana Armada (ASSA Rent)

-

Mitra Pinasthika Mustika Rent

-

Avis Budget Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2024: ST International successfully acquires Indonesian Car Rental Company for approximately 30 billion Won (roughly USD 23 million)

- December 2023: Sumitomo Mitsui Auto Service and Sumitomo Corporation jointly established PT SMAS Mobility Indonesia to provide short- and long-term leasing plus fleet management services.

Indonesia Car Rental Market Report Scope

By Booking Type

| Online |

| Offline |

By Rental Duration

| Short-term (Less than/Equals 30 days) |

| Medium-term (1 to 12 months) |

| Long-term (Above 12 months) |

By Application

| Tourism and Leisure |

| Daily Commuting |

| Corporate Fleet / Business Mobility |

| Airport Transfer |

By Vehicle Type

| Economy / Hatchback |

| Multi-Purpose Vehicle (MPV) |

| Sports Utility Vehicle (SUV) |

| Luxury / Executive |

By Fuel Type

| ICE - Petrol |

| ICE - Diesel |

| Hybrid-Electric |

| Battery-Electric (BEV) |

By End-user

| Corporate |

| Individual |

By Rental Channel

| Aggregator Platforms |

| Direct-to-Consumer (Rental Co.) |

| Super-App-Based Bundles |

By Region

| Java | Greater Jakarta (Jabodetabek) |

| West Java (ex-Jakarta) | |

| Central and East Java | |

| Bali and Nusa Tenggara | |

| Sumatra | |

| Kalimantan | |

| Sulawesi | |

| Papua and Maluku |

| By Booking Type | Online | |

| Offline | ||

| By Rental Duration | Short-term (Less than/Equals 30 days) | |

| Medium-term (1 to 12 months) | ||

| Long-term (Above 12 months) | ||

| By Application | Tourism and Leisure | |

| Daily Commuting | ||

| Corporate Fleet / Business Mobility | ||

| Airport Transfer | ||

| By Vehicle Type | Economy / Hatchback | |

| Multi-Purpose Vehicle (MPV) | ||

| Sports Utility Vehicle (SUV) | ||

| Luxury / Executive | ||

| By Fuel Type | ICE - Petrol | |

| ICE - Diesel | ||

| Hybrid-Electric | ||

| Battery-Electric (BEV) | ||

| By End-user | Corporate | |

| Individual | ||

| By Rental Channel | Aggregator Platforms | |

| Direct-to-Consumer (Rental Co.) | ||

| Super-App-Based Bundles | ||

| By Region | Java | Greater Jakarta (Jabodetabek) |

| West Java (ex-Jakarta) | ||

| Central and East Java | ||

| Bali and Nusa Tenggara | ||

| Sumatra | ||

| Kalimantan | ||

| Sulawesi | ||

| Papua and Maluku | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Indonesia car rental market in 2025?

The Indonesia car rental market size reached USD 0.86 billion in 2025 and is projected to almost double by 2030.

What is the expected growth rate of car rentals in Indonesia?

The market is forecast to post a 16.30% CAGR between 2025 and 2030, led by online bookings and corporate leasing demand.

Which booking channel is gaining the most traction?

Online aggregators dominate with a 69.33% share in 2024 and continue to outpace offline counters due to mobile-first consumer habits.

Why are long-term leases becoming popular among companies?

Operating leases transfer maintenance, depreciation, and compliance burdens to service providers, offering predictable monthly costs and fleet flexibility.

Which regions offer the highest rental growth opportunities beyond Java?

Bali and Nusa Tenggara lead with an 18.87% CAGR through 2030, buoyed by airport upgrades and government promotion of new tourism hubs.

Page last updated on: