| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 198.17 Million |

| Market Size (2030) | USD 348.30 Million |

| CAGR (2025 - 2030) | 11.94 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Indium Phosphide Wafer Market Analysis

The Indium Phosphide Wafer Market size is estimated at USD 198.17 million in 2025, and is expected to reach USD 348.30 million by 2030, at a CAGR of 11.94% during the forecast period (2025-2030).

The semiconductor industry is undergoing a significant transformation driven by increasing investments in manufacturing capabilities and technological advancements. According to the Semiconductor Industry Association, 39 new semiconductor fabrication projects were announced in 2023, demonstrating the industry's commitment to expanding production capacity. The focus has shifted towards developing more sophisticated compound semiconductors, with indium phosphide emerging as a crucial material for next-generation applications. Major semiconductor manufacturers are investing heavily in research and development to improve wafer manufacturing processes, particularly in advancing the production of larger diameter wafers to enhance efficiency and reduce costs.

The rapid evolution of data center infrastructure and telecommunications networks is reshaping the demand for specialized semiconductor materials. As of January 2024, over 2,750 data centers are operational in the United States alone, with significant deployments across other major markets. The industry is witnessing a shift towards advanced optical communications, with companies increasingly adopting indium phosphide semiconductor components for high-speed data transmission and processing. The integration of silicon photonics and co-packaged optics is gaining momentum, with major technology companies announcing strategic collaborations to develop next-generation data center solutions.

Consumer electronics manufacturers are increasingly incorporating advanced sensing and communication capabilities in their devices, particularly in wearable technology. According to recent industry data, the number of connected wearable devices globally is projected to exceed one billion by 2024, driving demand for sophisticated semiconductor materials. The trend towards miniaturization and improved functionality has led to increased adoption of indium phosphide-based components in smartphones, smartwatches, and other consumer devices. Manufacturers are particularly focused on developing 3D sensing technologies and improved camera functionality, creating new opportunities for indium phosphide wafer applications.

The automotive and healthcare sectors are emerging as significant growth drivers for specialized semiconductor materials. The increasing adoption of LiDAR technology in autonomous vehicles and advanced driver assistance systems has created new opportunities for indium phosphide wafers. In the healthcare sector, the growing demand for high-precision medical imaging and diagnostic equipment has led to increased utilization of indium phosphide semiconductor components. The development of biosensors and other medical devices requiring advanced semiconductor materials has accelerated, with manufacturers focusing on creating more sensitive and accurate diagnostic tools. These applications demonstrate the versatility of indium phosphide wafers in supporting critical technological advancements across multiple industries.

Indium Phosphide Wafer Market Trends

Increasing Use of Optoelectronic Devices

The growing adoption of optoelectronic devices across various industries is driving significant demand for indium phosphide wafers. These electronic components are crucial in detecting and regulating light while converting electrical information into infrared or visible energy. Recent technological advancements in the field, including plasmonic nanostructures, perovskite transistors, optically active quantum dots, microscopic light bulbs, low-cost 3D imaging, laser-powered 3D display technology, and Laser Li-Fi, are revolutionizing the applications of optoelectronic apparatus. This evolution is supported by substantial investments, as evidenced by the National Science Foundation's $25 million Science and Technology Center grant for establishing the Center for Integration of Modern Optoelectronic Materials on Demand (IMOD), a partnership of scientists and engineers from 11 universities led by the University of Washington.

The expansion of optoelectronic applications is further accelerated by continuous product innovations from industry players. For instance, Transfer Multisort Elektronik (TME) expanded its Everlight line of optoelectronic devices in 2023, introducing new IR LEDs capable of producing up to 150mW of output power. These components support various input voltages up to 4.0V and offer emission angles between 20 and 160 degrees, available in both through-hole variants with can diameters from 1.5mm to 5.0mm and surface-mount packages. The versatility of these devices in photovoltaic power supply, optical fiber communication systems, monitor and control circuits, and electric eyes demonstrates the growing market potential for indium phosphide wafers in optoelectronic applications.

Understand The Key Trends Shaping This Market

Download PDF

Growth of Datacom Business and 5G

The explosive growth in data consumption and the rapid deployment of 5G networks are creating unprecedented demand for indium phosphide wafers. According to Ericsson's projections, global mobile data traffic is expected to grow by a factor of 4.5 to reach 226 exabytes per month by 2026, with North American users anticipated to consume an average of 49GB per month per smartphone. This surge in data usage is complemented by the widespread adoption of cloud services, with the Cloud Infrastructure Report 2021 revealing that 57% of organizations now have more than half of their infrastructure in the cloud, and 64% anticipating complete migration to the public cloud within five years. Furthermore, Cisco's forecasts indicate that cloud data center traffic may account for 19.5 zettabytes per year, representing 95% of total data center traffic.

The advancement of 5G technology is creating new opportunities for indium phosphide semiconductor applications in wireless communication infrastructure. The material's unique properties make it ideal for manufacturing high-speed transceivers, modulators, and sensitive photodetectors essential for 5G networks. This is particularly significant as telecommunications providers continue to expand their 5G coverage and capabilities, driving demand for components that can support higher frequencies and faster data transmission rates. The integration of InP semiconductor devices in 5G infrastructure is crucial for achieving the promised improvements in network speed, latency, and capacity, while also supporting emerging applications such as augmented reality, autonomous vehicles, and industrial IoT deployments.

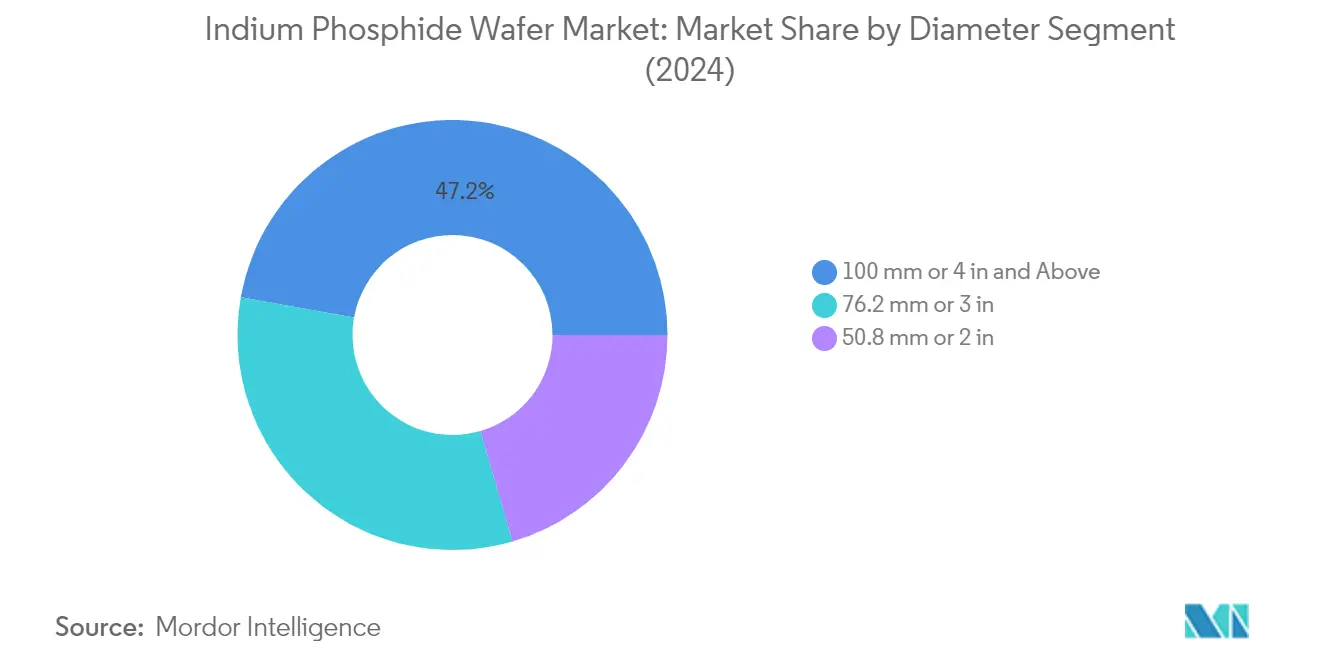

Segment Analysis: By Diameter

100 mm or 4" and Above Segment in Indium Phosphide Wafer Market

The 100 mm or 4" and Above segment has emerged as the dominant force in the global indium phosphide wafer market, commanding approximately 47% market share in 2024. This segment's leadership position is driven by the increasing adoption of larger diameter InP wafers in high-performance electronic and optoelectronic integrated circuits manufacturing. The segment's growth is particularly notable in applications such as high-speed optical communication systems, HBTs (Heterojunction Bipolar Transistors), and OEIC (Optoelectronic Integrated Circuits) manufacturing. The trend toward larger wafer sizes is primarily motivated by improved efficiency in process time and material usage, as larger wafers can accommodate more microchips per wafer. Additionally, the development of 6-inch indium phosphide single crystal substrate wafer technology is progressing towards mass production, particularly targeting telecommunications, data transmission, and photo electronic circuit applications.

76.2 mm or 3" Segment in Indium Phosphide Wafer Market

The 76.2 mm or 3" segment represents a crucial intermediate option in the indium phosphide wafer market, offering a balance between manufacturing efficiency and cost-effectiveness. These InP wafers are widely utilized in high-performance large-scale photonic integrated circuits (PICs), which find extensive applications in coherent transmitters, receivers, wavelength conversion, and packet-switching applications. The vertical gradient freeze (VGF) technique has become increasingly prevalent for growing these wafers, enabling the production of uniform crystals to precise specifications. The manufacturing process involves multiple sophisticated steps including crystal growth, precise slicing, edge rounding, and careful polishing in class 100/1000 clean room environments. The segment continues to maintain its significance in applications requiring a balance between performance and economic considerations.

50.8 mm or 2" Segment in Indium Phosphide Wafer Market

The 50.8 mm or 2" segment continues to serve specific niche applications in the indium phosphide wafer market, particularly in optoelectronics, laser devices, diodes, photodetectors, and microelectronics chips. Despite being the smallest diameter segment, these wafers maintain their relevance due to their comparatively lower fabrication costs and less stringent specifications. The segment particularly excels in applications requiring wavelength-division multiplexing and photovoltaic applications, where its high sensitivity to radiation proves advantageous. The manufacturing process for these wafers involves specialized techniques including chloride vapor-phase epitaxy and precise substrate preparation methods.

Segment Analysis: By End-User Industry

Telecommunications Segment in Indium Phosphide Wafer Market

The telecommunications segment continues to dominate the global indium phosphide wafer market, commanding approximately 94% market share in 2024. This substantial market presence is driven by the extensive use of InP wafers in critical telecommunications applications such as long-haul optical fiber connections, data centers, wireless connections for 5G base stations, and satellite communication systems. The segment's dominance is further strengthened by the increasing deployment of 5G infrastructure worldwide and the growing demand for high-speed data transmission capabilities. InP-based telecommunications systems offer significantly higher energy efficiencies and lower environmental impact compared to traditional copper-based systems, making them essential for supporting the exponential growth in data storage requirements and transmission needs. The ability to produce highly efficient lasers, sensitive photodetectors, and modulators for optical communication systems has made InP wafers indispensable in modern telecommunication infrastructure.

Consumer Electronics Segment in Indium Phosphide Wafer Market

The consumer electronics segment is emerging as the fastest-growing segment in the indium phosphide wafer market, with an expected growth rate of approximately 56% during the forecast period 2024-2029. This remarkable growth is primarily driven by the increasing adoption of advanced optoelectronic devices in consumer products, particularly in wearable technology and smartphones. The segment's growth is further accelerated by the rising demand for 3D sensing applications, OLED smartphone screens, and advanced camera functionalities that utilize InP-based components. The integration of indium phosphide wafers in consumer electronics is revolutionizing features such as facial recognition, augmented reality applications, and high-speed data transmission capabilities. The segment is witnessing substantial investments in research and development, particularly in areas such as consumer-grade 3D sensing products and advanced sensor solutions for health monitoring in wearable devices.

Remaining Segments in End-User Industry

The medical and other end-user industry applications segments play crucial roles in shaping the indium phosphide wafer market landscape. The medical segment is witnessing increased adoption in applications such as biosensors, surgical equipment control, and vital sign monitoring systems. The advancement in medical imaging technologies and the growing need for high-precision diagnostic equipment continue to drive demand in this sector. Meanwhile, the other end-user applications segment, encompassing industrial, automotive, and defense applications, is seeing expanded use in areas such as LiDAR systems, military guidance systems, and industrial automation. These segments are particularly benefiting from the increasing integration of optoelectronic devices in various specialized applications, contributing to the overall market diversification.

Indium Phosphide Wafer Market Geography Segment Analysis

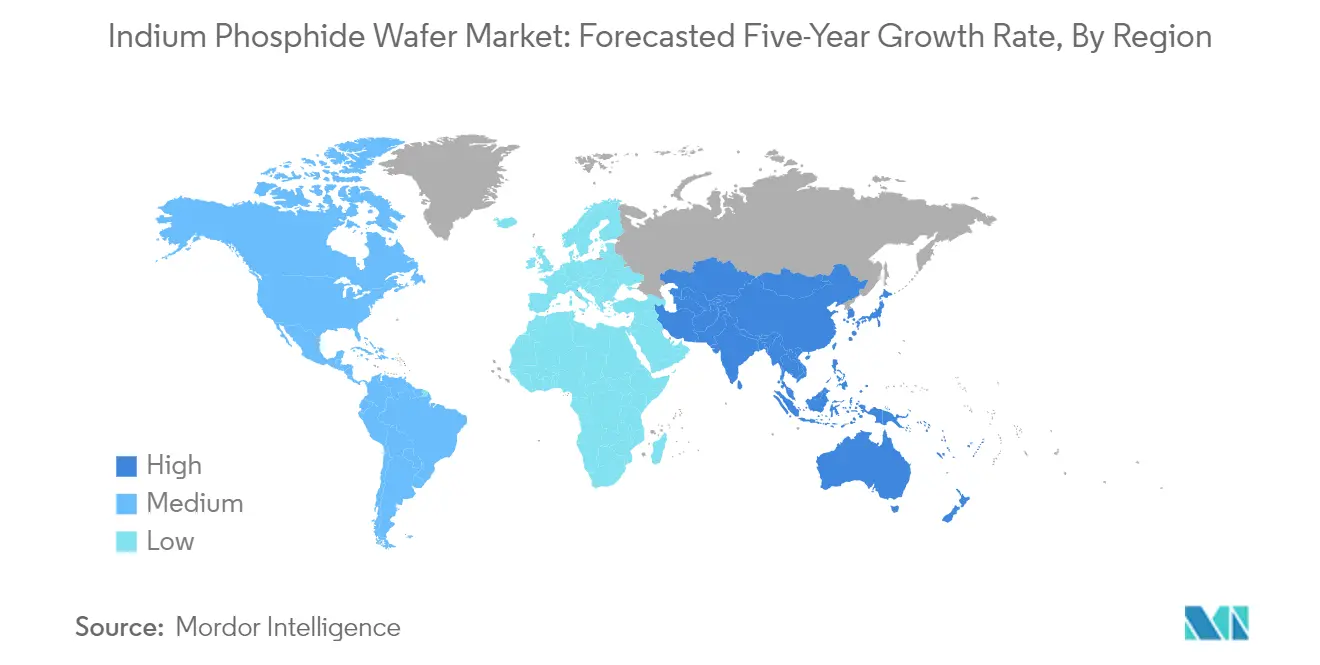

Indium Phosphide Wafer Market in North America

The North American indium phosphide wafer market, commanding approximately 24% of the global market share in 2024, continues to be driven by robust semiconductor manufacturing capabilities and advanced technological infrastructure. The region's dominance is reinforced by substantial government initiatives to strengthen domestic semiconductor production and reduce dependency on foreign suppliers. The presence of major research institutions and technology companies has created a favorable environment for innovation in optoelectronic devices and photonic integrated circuits. The market is particularly strong in applications related to 5G infrastructure, data center networking, and high-performance computing. The United States leads the regional market with its extensive network of semiconductor fabrication facilities and research centers, while Canada contributes significantly through its photonics research capabilities and emerging semiconductor initiatives. The region's focus on developing advanced semiconductor technologies, coupled with increasing investments in quantum computing and artificial intelligence applications, continues to drive demand for high-quality indium phosphide wafers.

Indium Phosphide Wafer Market in Europe

The European indium phosphide wafer market has demonstrated robust growth, with an approximate growth rate of 13% from 2019 to 2024, driven by significant investments in semiconductor manufacturing capabilities and photonics research. The region's market is characterized by strong collaboration between research institutions and industry players, particularly in countries like Germany, France, and the Netherlands. Europe's strategic focus on developing autonomous semiconductor capabilities has led to increased investment in manufacturing facilities and research centers. The market benefits from strong government support through initiatives aimed at reducing dependency on external suppliers and establishing a robust semiconductor ecosystem. The region's emphasis on sustainable technologies and energy-efficient solutions has created additional demand for indium phosphide wafers in photovoltaic applications and green technologies. The presence of leading automotive and telecommunications companies has further strengthened the market, particularly in applications related to autonomous vehicles and 5G infrastructure development.

Indium Phosphide Wafer Market in Asia-Pacific

The Asia-Pacific indium phosphide wafer market is projected to grow at approximately 14% during 2024-2029, establishing itself as the most dynamic region in the global market. The region's market is characterized by the presence of major semiconductor manufacturing facilities, particularly in countries like Taiwan, South Korea, Japan, and China. The robust ecosystem of electronic component manufacturers and growing investments in 5G infrastructure development continue to drive market growth. The region benefits from advanced manufacturing capabilities, a skilled workforce, and supportive government policies promoting semiconductor industry development. The increasing adoption of advanced technologies in consumer electronics, telecommunications, and automotive sectors has created substantial demand for indium phosphide wafers. The presence of major foundries and integrated device manufacturers has established Asia-Pacific as a crucial hub for semiconductor production, with continuous investments in expanding manufacturing capabilities and developing new technologies.

Indium Phosphide Wafer Market in Rest of the World

The Rest of the World region, encompassing Latin America, the Middle East, and Africa, represents an emerging market for indium phosphide wafers with growing potential in telecommunications and data center applications. While the region currently lacks significant fabrication facilities, increasing investments in digital infrastructure and telecommunications networks are creating new opportunities for market growth. The expansion of data center facilities and the implementation of 5G networks across these regions are driving the demand for semiconductor components. Countries in the Middle East are making strategic investments in technology sectors, while Latin American nations are focusing on developing their digital infrastructure. The region's market is characterized by growing awareness of advanced semiconductor applications and increasing investments in technological advancement, particularly in countries looking to diversify their economies beyond traditional sectors.

Get Analysis on Important Geographic Markets

Download PDF

Indium Phosphide Wafer Industry Overview

Top Companies in Indium Phosphide Wafer Market

The indium phosphide wafer market is characterized by the presence of established players like AXT Inc., Sumitomo Electric Industries, JX Nippon Mining & Metals Corporation, and Wafer World Inc., who have demonstrated strong capabilities in product development and market expansion. Companies are increasingly focusing on technological advancements in wafer manufacturing processes, particularly in developing larger diameter wafers and improving surface quality specifications. Strategic investments in research and development have become paramount, with companies working on enhancing crystal growth techniques and wafer processing technologies. Market players are also expanding their manufacturing capabilities, particularly in regions with growing semiconductor industries, while simultaneously strengthening their supply chain networks to ensure consistent raw material availability. The industry has witnessed a trend toward vertical integration, with companies seeking to control more aspects of the production process to maintain quality standards and reduce dependencies on external suppliers.

Market Structure Shows Regional Manufacturing Dominance

The indium phosphide wafer market exhibits a relatively concentrated structure, dominated by large conglomerates with established semiconductor manufacturing capabilities, particularly in Asia-Pacific and North America. These major players possess significant advantages in terms of technological expertise, manufacturing scale, and established relationships with key customers in telecommunications, data centers, and consumer electronics sectors. The market has witnessed limited merger and acquisition activity, with companies instead focusing on organic growth through capacity expansion and technological advancement in existing facilities.

The competitive dynamics are influenced by regional manufacturing strengths, with Japanese and American companies holding significant market positions due to their advanced manufacturing capabilities and strong intellectual property portfolios. Local players, particularly in emerging markets, are gradually gaining ground by focusing on specific product segments and building relationships with regional customers. The industry's high entry barriers, including substantial capital requirements and complex technological requirements, have contributed to maintaining the existing competitive structure while limiting new entrant threats.

Innovation and Customer Relations Drive Success

Success in the indium phosphide wafer market increasingly depends on companies' ability to innovate while maintaining cost competitiveness. Incumbent players are strengthening their market positions by investing in next-generation wafer technologies, particularly in developing larger diameter wafers and improving quality specifications to meet evolving customer requirements. Companies are also focusing on building long-term relationships with key customers in high-growth sectors like 5G infrastructure and data centers, while simultaneously diversifying their customer base to reduce dependency on specific market segments.

For emerging players and contenders, the path to market share growth lies in identifying and serving niche applications while building technological capabilities gradually. The industry faces moderate substitution risks from alternative semiconductor materials, particularly in specific applications where performance requirements can be met by more cost-effective solutions. Regulatory compliance, particularly regarding environmental standards and quality certifications, continues to play a crucial role in shaping competitive dynamics. Companies that can effectively balance innovation, cost management, and regulatory compliance while maintaining strong customer relationships are likely to succeed in this evolving market landscape.

Indium Phosphide Wafer Market Leaders

-

AXT Inc.

-

Wafer World Inc.

-

Logitech Ltd.

-

Western Minmetals (sc) Corporation

-

Century Goldray Semiconductor Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

.webp)

Need More Details on Market Players and Competiters?

Download PDF

Indium Phosphide Wafer Market News

- May 2022: A 200 mm (8) epiwafer for vertical-cavity surface-emitting laser (VCSEL) diodes was created by IQE in Wales. The cost of the laser for 3D sensors is expected to be drastically reduced by switching to a 200 mm compound semiconductor epi wafer. New foundry relationships may result from this, particularly those with high-volume silicon-based foundries that use 200 mm machinery. This may make it possible for compound semiconductors to be integrated into silicon, opening up a wider choice of devices and applications.

- May 2022 - JX Nippon Mining & Metals Corporation company concluded a financing agreement with the Japan Bank for International Cooperation to procure the funding needed to strengthen its business in the manufacturing of sputtering targets for semiconductors in the United States of America.

Indium Phosphide Wafer Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot

- 4.5 Assessment of the Impact of COVID-19 on the Industry

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Use of Optoelectronic Devices

- 5.1.2 Growth of Datacom Business and 5G

-

5.2 Market Restraints

- 5.2.1 Competition from Other Substitutes

6. MARKET SEGMENTATION

-

6.1 By Diameter

- 6.1.1 50.8 mm or 2 "

- 6.1.2 76.2 mm or 3 "

- 6.1.3 100 mm or 4" and Above

-

6.2 By End-user Industry Application

- 6.2.1 Consumer Electronics

- 6.2.2 Telecommunications

- 6.2.3 Medical

- 6.2.4 Other End-user Industry Applications

-

6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Rest of the world

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 AXT Inc.

- 7.1.2 Wafer World Inc.

- 7.1.3 Logitech Ltd.

- 7.1.4 Western Minmetals (SC) Corporation

- 7.1.5 Century Goldray Semiconductor Co. Ltd

- 7.1.6 Semiconductor Wafer Inc.

- 7.1.7 Ding Ten Industrial Inc.

- 7.1.8 Sumitomo Electric Semiconductor Materials Inc. (Sumitomo Electric Industries Ltd)

- 7.1.9 Xiamen Powerway Advanced Material Co. Ltd

- 7.1.10 JX Nippon Mining & Metals Corporation (Eneos Holdings Inc.)

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Indium Phosphide Wafer Industry Segmentation

Indium phosphide, a binary semiconductor, is used to create indium phosphide wafers. It provides a better electron velocity than most common semiconductors, including silicon. Hence, it is the most practical compound for optoelectronic applications, fast transistors, and resonance tunneling diodes.

The scope of the study focuses on the market analysis of indium phosphide wafer products sold across the globe. The market sizing encompasses the revenue generated through indium phosphide wafer products sold by various market players. The study also tracks key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports market estimations and growth rates over the forecast period. The study further analyzes the overall impact of the COVID-19 pandemic on the ecosystem. The scope of the report encompasses market sizing and forecast for segmentation by diameter, end-user industry application, and geography.

| By Diameter | 50.8 mm or 2 " |

| 76.2 mm or 3 " | |

| 100 mm or 4" and Above | |

| By End-user Industry Application | Consumer Electronics |

| Telecommunications | |

| Medical | |

| Other End-user Industry Applications | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Rest of the world |

Need A Different Region or Segment?

Customize Now

Indium Phosphide Wafer Market Research FAQs

How big is the Indium Phosphide Wafer Market?

The Indium Phosphide Wafer Market size is expected to reach USD 198.17 million in 2025 and grow at a CAGR of 11.94% to reach USD 348.30 million by 2030.

What is the current Indium Phosphide Wafer Market size?

In 2025, the Indium Phosphide Wafer Market size is expected to reach USD 198.17 million.

Who are the key players in Indium Phosphide Wafer Market?

AXT Inc., Wafer World Inc., Logitech Ltd., Western Minmetals (sc) Corporation and Century Goldray Semiconductor Co. Ltd. are the major companies operating in the Indium Phosphide Wafer Market.

Which is the fastest growing region in Indium Phosphide Wafer Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Indium Phosphide Wafer Market?

In 2025, the Asia-Pacific accounts for the largest market share in Indium Phosphide Wafer Market.

What years does this Indium Phosphide Wafer Market cover, and what was the market size in 2024?

In 2024, the Indium Phosphide Wafer Market size was estimated at USD 174.51 million. The report covers the Indium Phosphide Wafer Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Indium Phosphide Wafer Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Indium Phosphide Wafer Market Research

Mordor Intelligence provides a comprehensive analysis of the indium phosphide and compound semiconductors industry. We leverage decades of expertise in semiconductor research. Our latest report examines the evolving landscape of InP semiconductor technologies. This includes a detailed analysis of InP wafers and indium phosphide wafer applications. The study offers extensive coverage of phosphide-based technologies, InP substrate developments, and emerging applications in the semiconductor sector. We focus particularly on indium phosphide technology advancements through 2024-2025.

Stakeholders can access detailed insights through our report PDF, available for download. It covers crucial aspects of the InP ecosystem, including indium phosphide substrates manufacturing processes and technological innovations. The analysis includes a comprehensive evaluation of InP HEMT epitaxial developments, GaAs integration, and emerging applications in photonics and telecommunications. Our report provides actionable intelligence for InP company strategies, substrate manufacturing optimization, and technology implementation roadmaps. This enables informed decision-making in this rapidly evolving sector.