India Waterproofing Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

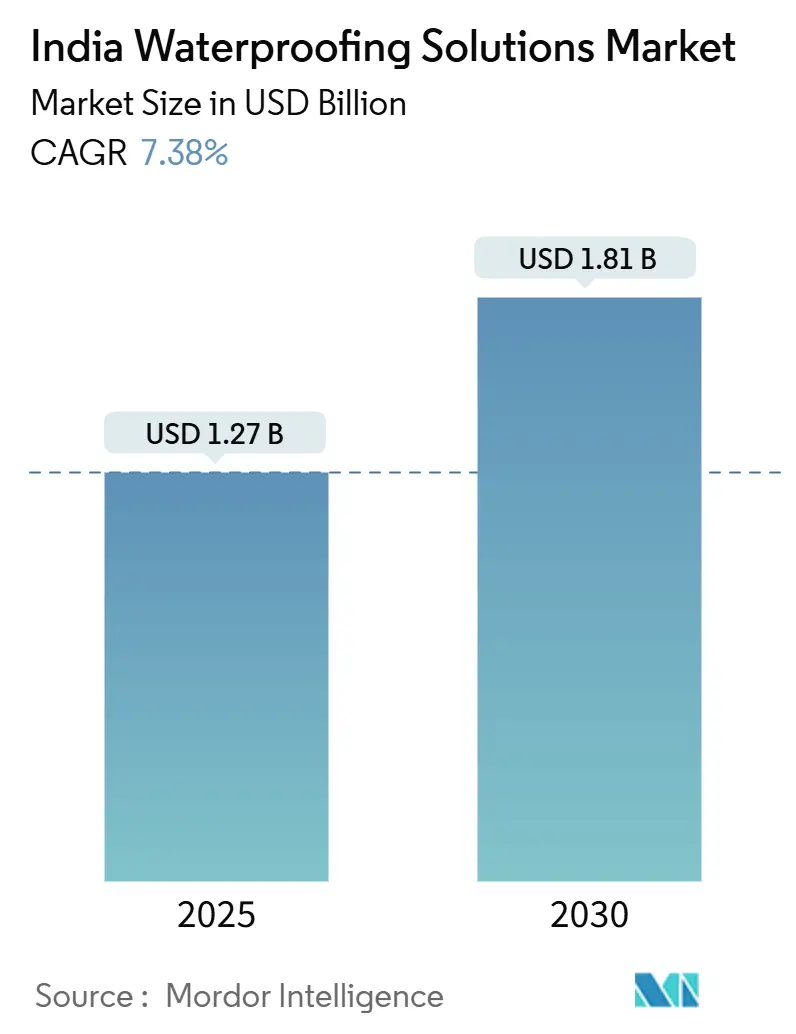

| Market Size (2025) | USD 1.27 Billion |

| Market Size (2030) | USD 1.81 Billion |

| Growth Rate (2025 - 2030) | 7.38% CAGR |

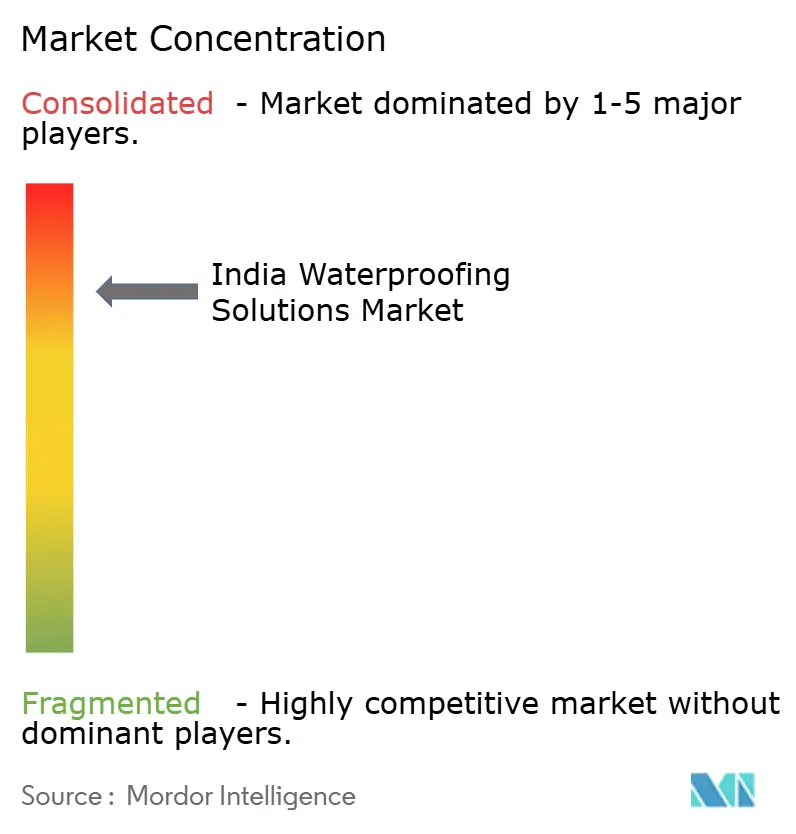

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Waterproofing Solutions Market Analysis by Mordor Intelligence

The India Waterproofing Solutions Market size is estimated at USD 1.27 billion in 2025, and is expected to reach USD 1.81 billion by 2030, at a CAGR of 7.38% during the forecast period (2025-2030). Robust public spending under the National Infrastructure Pipeline, stricter building codes focused on climate resilience, and a clear customer pivot toward preventive maintenance keep the India Waterproofing Solutions market on a stable growth path despite raw-material cost swings. Membranes remain the favored technology because they combine proven performance in aggressive monsoon conditions with the extended warranties demanded by developers and affluent homeowners. Residential construction drives premiumization, while commercial, industrial, and infrastructure projects create scale for advanced systems such as heat-reflective hybrid membranes. Competitive intensity is high as diversified paint majors and specialized chemical suppliers race to improve reseaarch and development, strengthen applicator networks, and comply with the Bureau of Indian Standards’ upgraded waterproofing specifications.

Key Report Takeaways

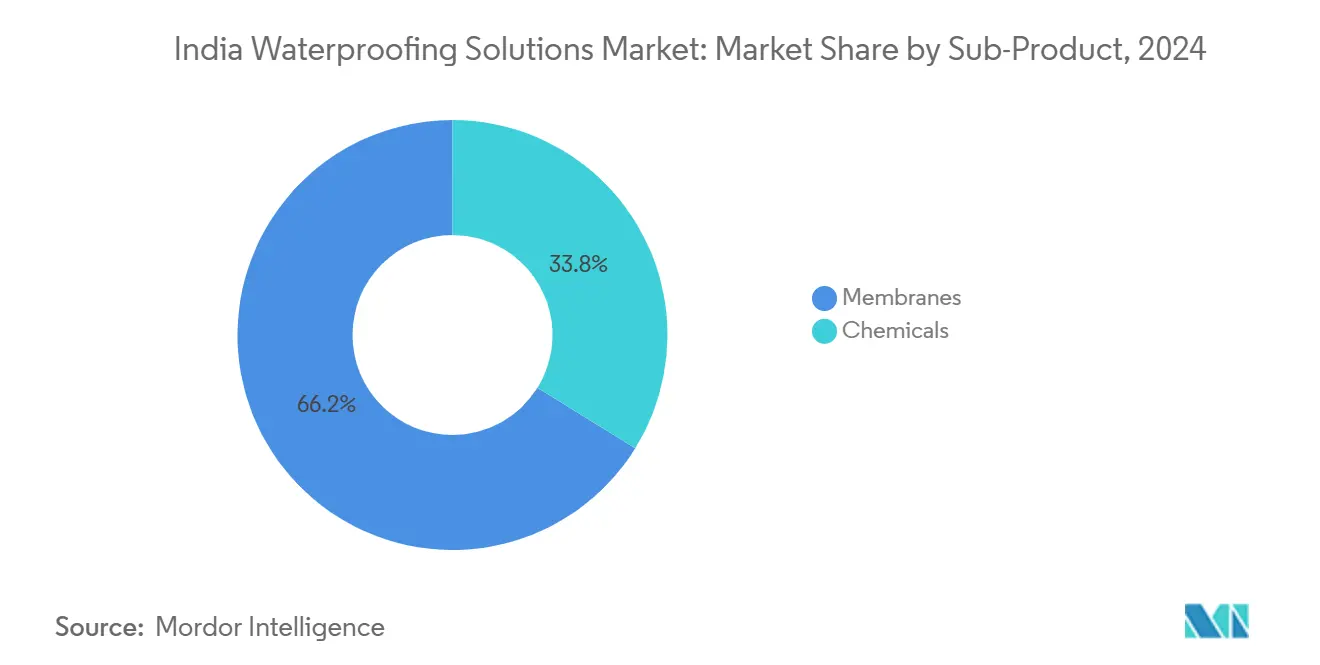

- By sub-product, membranes led with 66.16% of the India Waterproofing Solutions market share in 2024, and the segment is advancing at a 7.59% CAGR through 2030.

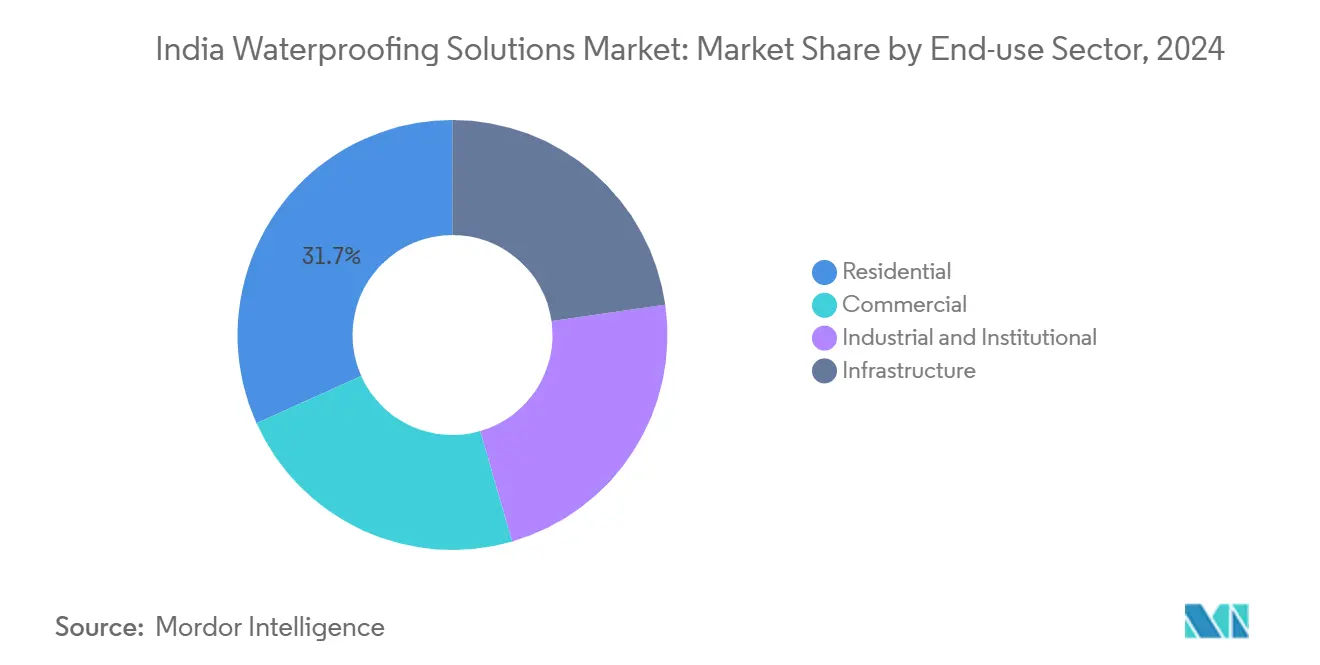

- By end-use sector, residential applications captured 31.73% of the India Waterproofing Solutions market size in 2024 and are expanding at the fastest 7.85% CAGR to 2030.

India Waterproofing Solutions Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization and affordable-housing stimulus | +1.8% | National; tier-1 and tier-2 cities | Medium term (2-4 years) |

| Adoption of hybrid liquid membranes with heat-reflectivity | +1.2% | Urban centers and industrial zones | Long term (≥ 4 years) |

| Intensifying monsoons prompting climate-resilient codes | +1.5% | Coastal and high-rainfall states | Short term (≤ 2 years) |

| Home-owner premiumization and 10-year warranty demand | +0.9% | Metropolitan residential clusters | Medium term (2-4 years) |

| Shift toward low-VOC nano-penetrating technologies | +0.7% | Green-building and commercial projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Affordable-Housing Stimulus

India adds more than 10 million urban residents each year, and the Pradhan Mantri Awas Yojana alone targets 20 million new affordable units by 2025[1]Ministry of Housing and Urban Affairs, “Pradhan Mantri Awas Yojana,” MOHUA.GOV.IN. Developers increasingly specify preventive waterproofing at the design stage because retrofits cost up to five times more than original installation. Budget 2024-25 earmarked USD 144 billion for climate-resilient infrastructure, a move that directly links funding to BIS-compliant waterproofing. Smart-City projects in 100 municipalities have elevated demand for membranes that perform in underground metro stations, multilevel parking structures, and mixed-use towers. Vertical construction in dense urban cores favors cold liquid applied membranes, which adapt to complex geometries without joints that could fail under differential settlement.

Adoption of Hybrid Liquid Membranes with Heat-Reflectivity

Hybrid liquid membranes that combine waterproofing with near-infrared reflectance reduce rooftop temperatures by as much as 15 °C during peak summer, lowering HVAC energy loads and helping buildings qualify for IGBC and LEED points. Asian Paints and Sika AG have scaled polymer research and development to address durability and color-fastness concerns in India’s ultraviolet-intense climate. Early adopters include data centers and manufacturing plants where energy savings compound quickly across large roof areas. The technology has begun penetrating residential high-rise projects, where reduced heat gain adds marketing value for developers targeting mid-premium buyers. Over the long term, broader rollout depends on lowering product cost through local raw-material sourcing and higher manufacturing volumes.

Intensifying Monsoons Prompting Climate-Resilient Codes

Extreme rainfall events have risen 75% in the last two decades, and the Bureau of Indian Standards now mandates that membrane systems in high-rainfall zones survive hydrostatic pressure equal to a 2m water column[2]India Meteorological Department, “Monsoon Data and Analysis,” MAUSAM.IMD.GOV.IN. Coastal states such as Kerala and Maharashtra have moved ahead of the national code, making enhanced waterproofing a prerequisite for building permits in districts with annual precipitation above 2,000 mm. Insurance underwriters also price policies based on documented waterproofing performance, linking compliance to lower premiums. Developers consequently shift budgets toward premium polyurethane and modified-bitumen membranes that last longer under sustained ponding. Early arrival of the 2024 monsoon exposed vulnerabilities in older roofs, accelerating retrofit programs across commercial real estate portfolios.

Shift Toward Low-VOC Nano-Penetrating Technologies

Low-VOC nano-penetrating treatments form molecular-level bonds with concrete, delivering waterproofing without surface build-up and meeting indoor-air-quality thresholds critical in hospitals and schools. The India Waterproofing Solutions market increasingly specifies these formulations for retrofit projects where existing surfaces cannot accommodate thick membranes. Application time drops by 30% because extensive surface grinding is unnecessary, reducing labor costs on congested urban job sites. Green building assessors favor nano-penetrating systems because they emit fewer than 50 g VOC per liter, well below the 2024 national limit of 120 g VOC. Manufacturers also highlight enhanced freeze-thaw resistance, an attribute gaining relevance in northern states with wide diurnal temperature swings.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented applicator base driving workmanship failures | -1.1% | National; intensified in tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Crude-linked raw-material volatility hitting PU and bitumen | -0.8% | Nationwide manufacturing and supply chains | Short term (≤ 2 years) |

| Limited tier-3/rural awareness for preventive waterproofing | -0.6% | Rural districts and smaller urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Applicator Base Driving Workmanship Failures

Small contractors with limited formal training install about 80% of waterproofing systems nationwide, leading to inconsistent workmanship and premature failures.Urban developers increasingly mandate OEM-certified applicators, yet reaching India’s sprawling construction market remains challenging. Manufacturers fund regional training centers, but retention of skilled labor is low because workers migrate between short-term projects. In the immediate term, workmanship failures erode end-user confidence and slow the shift toward premium membranes that require meticulous installation.

Limited Tier-3/Rural Awareness for Preventive Waterproofing

In markets where masonry still dominates and budgets are tight, builders treat waterproofing as an optional add-on rather than a core building envelope component. Penetration of organized retail is shallow, and technical advice rarely reaches individual house owners. Waterproofing adds 2-3% to initial construction cost, a premium many rural customers forego despite escalating rainfall intensity. Although government housing schemes channel some demand, individual self-constructions in tier-3 towns still rely on traditional lime plaster or tar coatings. The India Waterproofing Solutions market therefore under-indexes in territories representing roughly 40% of new residential floor space.

Segment Analysis

By Sub Product: Membranes Sustain Performance Leadership

Membranes represented 66.16% of the India Waterproofing Solutions market share in 2024 and will maintain a 7.59% CAGR to 2030, reinforcing their status as the functional benchmark for demanding applications. Cold liquid applied membranes attract residential builders because they form seamless barriers over complex roof lines and cure without torches, enhancing job-site safety. Fully adhered sheet systems dominate large-format commercial roofs and podium slabs where proven 20-year field performance matters. Hot liquid variants address chemical plants and refineries, while loose-laid sheets support fast-track infrastructure projects by enabling pre-fabricated installation sequences.

Advanced elastomeric chemistry helps membranes bridge cracks up to 2 mm, a critical advantage in high-rise structures subject to differential movement. Warranties now extend to 12 years in premium residential segments, and digital inspection tools allow manufacturers to audit installations before issuing coverage. While chemicals retain relevance for localized repairs and niche substrates, the India Waterproofing Solutions market size for membranes keeps increasing as cost per square meter falls with scale. Strategic raw-material backward integration by major suppliers further cushions membrane pricing against crude-driven volatility.

By End-Use Sector: Residential Premiumization Sets the Pace

Residential buildings accounted for 31.73% of the India Waterproofing Solutions market size in 2024 and are tracking a 7.85% CAGR, ahead of every other sector. Individual homeowners favor liquid membranes that can be roller-applied on terraces without heavy equipment, while apartment developers specify layered sheet assemblies for podium waterproofing. The up-market shift is visible in metros, where 10-year guarantees have moved from luxury towers to mid-income projects.

Commercial real estate imposes stricter downtime penalties for leakage, so facility managers invest in hybrid liquid systems that combine waterproofing and heat reflectance, thereby lowering HVAC expenses. Industrial campuses add demand for chemical-resistant coatings in effluent zones. Infrastructure sites such as metro tunnels and flyovers adopt multi-layer membrane sandwiches to resist hydrostatic pressure and cyclic loading. Yet the India Waterproofing Solutions market continues to see residential activity as its volume anchor, with government credit subsidies and stable mortgage rates keeping project pipelines healthy.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Coastal states like Maharashtra, Karnataka, Tamil Nadu, and West Bengal generate a major revenue, a premium driven by extreme humidity and heavy monsoons that force selection of higher-grade membranes. Mumbai’s real-estate density spurs vertical projects that specify cold liquid membranes for podiums and terraces; Chennai’s automotive corridors demand chemical-resistant solutions around paint shops and effluent tanks.

Northern India is a growing regional cluster as the Delhi National Capital Region channels federal spending into metro extensions, expressways, and smart-city housing. Temperature swings from 4 °C in winter nights to 46 °C in summer afternoons stress building envelopes, prompting developers to favor membranes with high elongation and low modulus. Waterproofing for below-grade structures in the Delhi Metro averages 1 million m² annually, anchoring supplier income streams.

Southern metros showcase India’s most mature green-building culture. Bengaluru’s IT parks adopt LEED Platinum targets that require low-VOC, heat-reflective membranes. Hyderabad’s pharma SEZs specify polyurethane elastomers that resist aggressive cleaning chemicals. The region’s higher adoption of applicator certification reduces warranty claims versus national averages.

Eastern states lag in penetration because disposable incomes are lower and conventional construction practices persist. However, accelerated highway and port development under the Sagarmala program is opening strategic pockets of demand. Over the forecast horizon, suppliers that place technical support teams in Kolkata and Bhubaneswar stand to capture early-mover advantage as private investment flows eastward.

Competitive Landscape

The India Waterproofing Solutions market is consolidated in nature. Asian Paints leverages its paint dealer network to cross-sell membranes and installation services, while Pidilite Industries uses the Dr. Fixit master brand to build homeowner trust through mass-media campaigns. Strategic vertical integration is rising. Several leading manufacturers set up SBS-modified bitumen sheet plants near western ports for feedstock access and quicker deliveries. Applicator academies in Mumbai, Chennai, and Ahmedabad issue competency cards that developers increasingly list as tender prerequisites. Birla Opus, launched in 2024, plans capex outlays aimed at backward integrating emulsions and strengthening nationwide distribution within three years.

India Waterproofing Solutions Industry Leaders

-

Asian Paints

-

Berger Paints India Limited

-

Saint-Gobain

-

Pidilite Industries Ltd.

-

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: TIKIDAN introduced Revestidan Protect Max, a polyurethane-hybrid roof membrane designed for enhanced UV resistance and long-term crack bridging.

- July 2024: Saint-Gobain completed the global acquisition of Fosroc, adding its full waterproofing portfolio to Saint-Gobain India’s construction-chemicals division.

India Waterproofing Solutions Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Chemicals, Membranes are covered as segments by Sub Product.| Chemicals | Epoxy-based |

| Polyurethane-based | |

| Water-based | |

| Other Technologies | |

| Membranes | Cold Liquid Applied |

| Fully Adhered Sheet | |

| Hot Liquid Applied | |

| Loose-Laid Sheet |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

| By Sub Product | Chemicals | Epoxy-based |

| Polyurethane-based | ||

| Water-based | ||

| Other Technologies | ||

| Membranes | Cold Liquid Applied | |

| Fully Adhered Sheet | ||

| Hot Liquid Applied | ||

| Loose-Laid Sheet | ||

| By End-Use Sector | Commercial | |

| Industrial and Institutional | ||

| Infrastructure | ||

| Residential | ||

Market Definition

- END-USE SECTOR - Waterproofing solutions consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of waterproofing solutions such as membranes, coatings, and chemicals are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms