Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

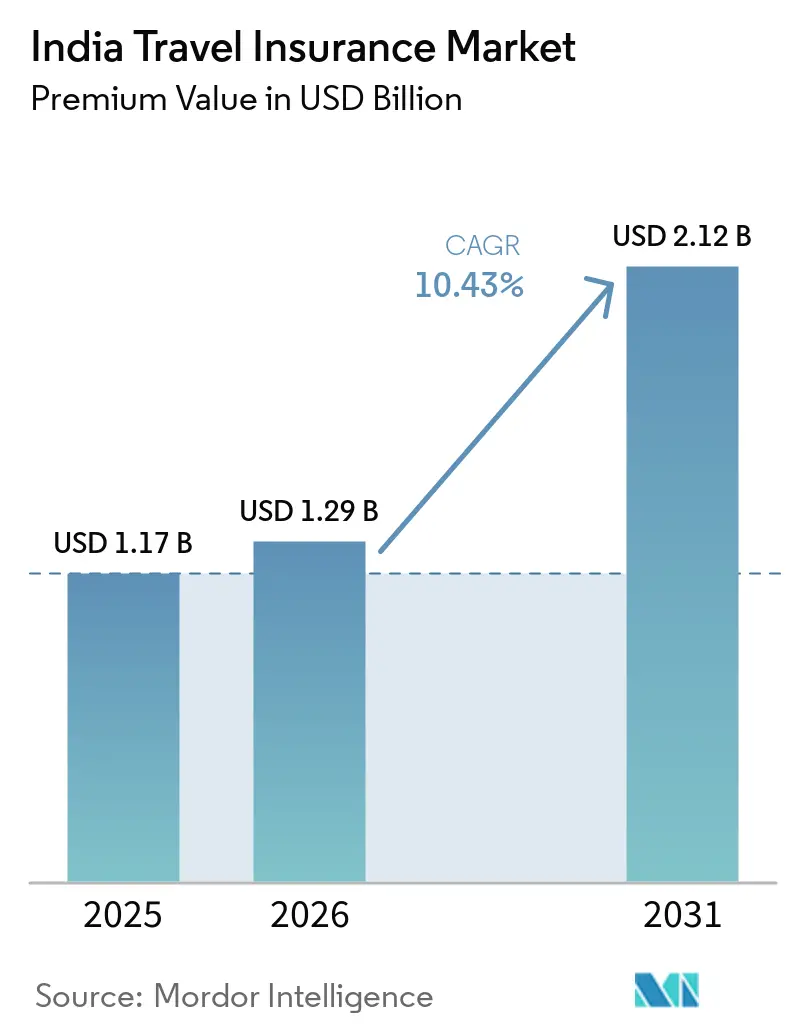

| Base Year Market Size (2025) | USD 1.17 Billion |

| Market Size (2026) | USD 1.29 Billion |

| Market Size (2031) | USD 2.12 Billion |

| Growth Rate (2026 - 2031) | 10.43% CAGR |

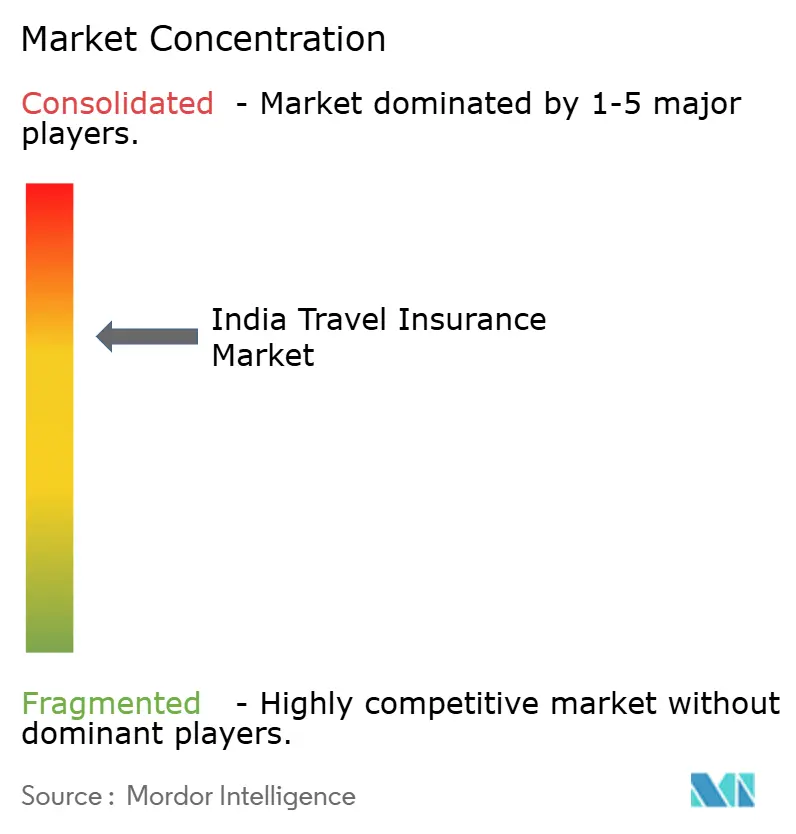

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Travel Insurance Market Analysis by Mordor Intelligence

The India Travel Insurance Market size in terms of premium value is expected to increase from USD 1.17 billion in 2025 to USD 1.29 billion in 2026 and reach USD 2.12 billion by 2031, growing at a CAGR of 10.43% over 2026-2031.

A resurgence in outbound leisure trips, mandatory insurance for visa issuance, and rising digital distribution have collectively pushed the India travel insurance market to the forefront of Asia-Pacific growth stories. Steady premium innovations, from cruise-specific covers to micro-duration plans, have broadened the addressable base, while the escalating frequency of business travel is shifting consumer focus from price to benefits. Competitive intensity is built as incumbents integrate with online travel agencies (OTAs) and banks embed insurance within broader financial offerings, creating new cross-sell and upsell opportunities. Meanwhile, IRDAI’s regulatory sandbox and the centralized Bima Sugam platform are reducing time-to-market for new products and unlocking data-driven underwriting efficiencies that can sustain margins despite heightened rivalry.

Key Report Takeaways

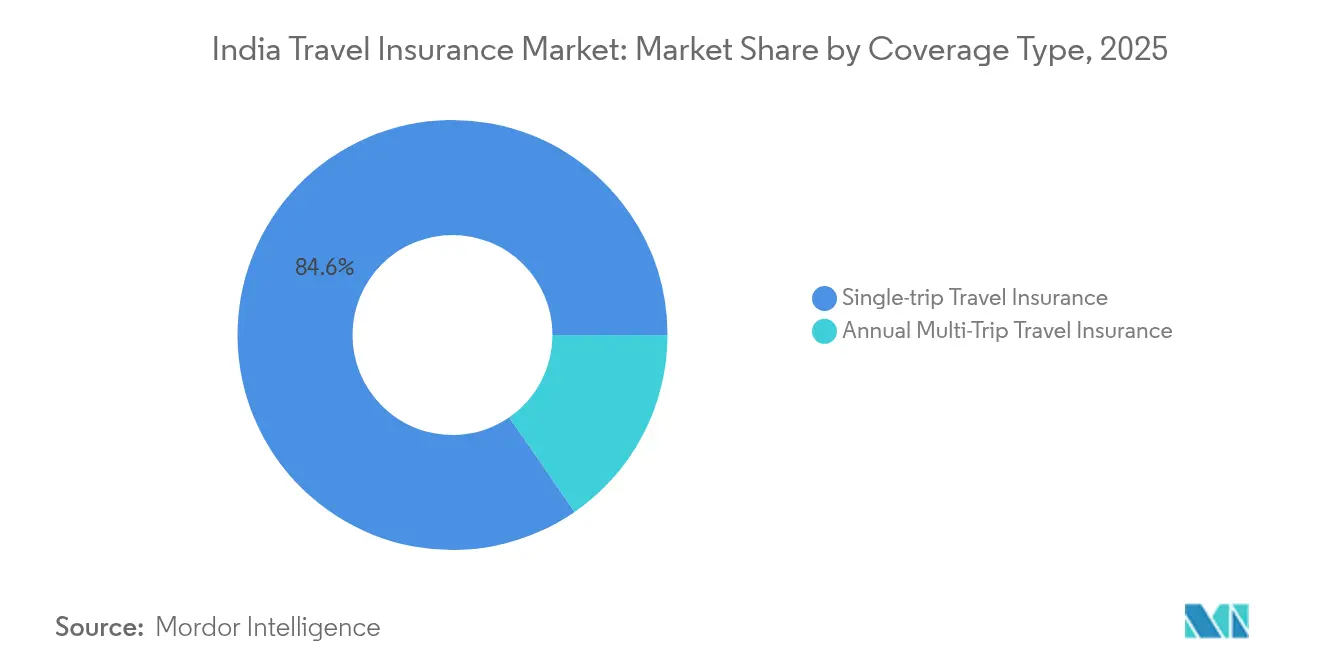

- Single-trip Travel Insurance commanded 84.62% of the India travel insurance market share in 2025, whereas Annual Multi-Trip policies are expanding at a 10.74% CAGR toward 2031, making them the fastest-growing coverage type.

- Family Travelers accounted for 41.36% revenue in 2025 and continues to anchor demand, while the Senior Citizen segment is on track to post a 10.68% CAGR through 2031, aided by cruise tourism and affluent retiree mobility.

- Insurance Intermediaries held a 46.62% slice of the India travel insurance market size in 2025, yet Insurance Aggregators are racing ahead at a 10.55% CAGR, propelled by 77 million PolicyBazaar users and expanding phygital reach.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Travel Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID rebound in outbound leisure & VFR travel | 2.8% | National, with a concentration in metro cities | Medium term (2-4 years) |

| Mandatory insurance for Schengen & other visas | 2.1% | National, with higher impact in Delhi, Mumbai, Bangalore | Long term (≥ 4 years) |

| Growth of digital aggregators & OTA-embedded sales | 1.9% | National, with early adoption in Tier-1 cities | Short term (≤ 2 years) |

| Airline ticketing portals launching embedded cover | 1.2% | National, concentrated at major airports | Medium term (2-4 years) |

| Rapid rise in senior-citizen cruise tourism | 0.8% | National, with concentration in affluent urban centers | Long term (≥ 4 years) |

| UPI-enabled pay-as-you-go micro-duration policies | 0.6% | National, with higher penetration in digital-first demographics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-COVID Rebound in Outbound Leisure & VFR Travel

Indian passport holders logged 15 million international departures in H1 2024, surpassing pre-pandemic baselines and reinforcing the upward trajectory of the India travel insurance market[1]Business World, “Indian Seniors Power Cruise Boom,” bwbusinessworld.com.. Travelers now view insurance as indispensable infrastructure for medical contingencies, flight disruptions, and geopolitical risks that previously went uninsured. Corporate travel is forecast to hit USD 35 billion in 2025, intensifying demand for real-time claims support, emergency evacuation benefits, and pandemic-related covers. As risk awareness grows, insurers differentiate through value-added services like multilingual telemedicine and airport concierge assistance that resonate with seasoned travelers. The market’s pivot from price competition to benefits-driven propositions positions comprehensive coverage as the new norm rather than a premium add-on.

Mandatory Visa Insurance Requirements Reshape Product Design

The Schengen area’s USD 31,246.8 (EUR 30,000) minimum coverage rule has entrenched protection buying among Europe-bound Indians, effectively hard-coding travel insurance into the visa checklist[2]Directorate-General for Migration & Home Affairs, “Schengen Visa Code Amendments,” europa.eu. . April 2024 brought multi-year Schengen visas that require renewal-aligned coverage, creating a predictable recurring revenue stream for insurers. Parallel mandates in Canada, Australia, and Gulf nations are widening this compliance-led customer funnel, encouraging insurers to craft modular, multi-destination policies that meet diverse embassy standards. Digital issuance and API-based validation now allow instant embassy-ready documents, trimming customer effort and boosting satisfaction. Aggregators benefit by funneling this captive demand through one-click purchase paths that elevate attach rates and lifetime value.

Growth of Digital Aggregators & OTA-Embedded Sales

PolicyBazaar aggregates 250+ policies from 53 insurers, enabling transparent comparison that accelerates decision-making and compresses the sales funnel from days to minutes[3] PB Fintech, “PolicyBazaar Investor Presentation Q1 FY25,” pbfintech.com.. Phygital strategies, digital journeys backed by offline agent assistance, have unlocked Tier-2/3 uptake, accounting for a 30% jump in new users outside metros. OTAs such as MakeMyTrip and EaseMyTrip embed insurance at checkout, lifting attach rates above 15% for international tickets and funneling incremental premiums to underwriting partners. Competitive pressure is steering insurers toward API-first architectures that support real-time underwriting, dynamic pricing, and seamless claims triggers. The resulting data trove informs actuarial refinement and targeted cross-selling, reinforcing the India travel insurance market’s digital flywheel.

Rapid Rise in Senior-Citizen Cruise Tourism

Cruise bookings among Indians aged 60 plus surged 40% year-on-year in 2024, elevating premium cover demand for extended voyages that can cost upward of USD 5,846.9 (INR 500,000) per traveler. Specialized policies now cover cabin confinement, missed port calls, and helicopter evacuation, risks unique to maritime itineraries. Insurers are offering higher sum-insured limits, simplified underwriting for pre-existing conditions, and 24×7 multilingual medical hotlines to attract affluent retirees. Cruise lines promoting India-centric routes further amplify visibility, nudging seniors toward pre-trip financial safeguards. The segment’s high-ticket size enhances profitability, making it a strategic arena for differentiation via concierge-style claims handling and cross-border care coordination.

Restraints Impact Analysis*

| Restraint | % (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low awareness among first-time international travellers | -1.7% | National, with concentration in Tier-2/3 cities | Medium term (2-4 years) |

| Complex & time-consuming claims settlement | -1.4% | National, with pronounced impact in non-metro regions | Short term (≤ 2 years) |

| Gaps in adventure-sports coverage hurt brand trust | -0.9% | National, more acute in youth and adventure segments | Short term (≤ 2 years) |

| RBI forex-card rules limiting bundled insurance add-ons | -0.6% | National, especially among frequent business travelers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Awareness Among First-Time International Travellers Constrains Market Penetration

International travel is spreading into Tier-2/3 cities, yet insurance literacy lags among debut travelers who weigh policy premiums against perceived destination safety. Traditional mass-media campaigns rarely translate coverage features into relatable stories, leaving misconceptions unaddressed and leakage high. Local agents often push visa-compliant products without explaining post-departure benefits, limiting upsell to comprehensive covers. Aggregators have begun deploying vernacular explainer videos and influencer testimonials, but early results show modest conversion owing to digital trust gaps. Sustained growth, therefore, hinges on hyper-local education that links real-world anecdotes, such as medical emergencies abroad, to tangible financial outcomes.

Complex & Time-Consuming Claims Settlement Undermines Confidence

Public-sector leader New India Assurance posts a 98.74% settlement ratio, yet private-sector satisfaction scores swing between 1.8 and 4.5 on consumer forums, exposing inconsistency.[4]Moneycontrol Editorial, “Travel Insurance Claims: Why Satisfaction Scores Diverge Widely,” moneycontrol.com. Pain points include document-heavy processes, coordination with overseas hospitals, and opaque status updates that fuel anxiety during crises. Delayed reimbursements erode goodwill, prompting negative word-of-mouth that reverberates across joint-family networks and social media. Insurers are piloting AI-driven fraud checks and one-click documentation uploads, which have cut processing time by 30% in early trials. Achieving parity in claims experience across the board is essential for sustaining the India travel insurance market’s reputation as a reliable safety net.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: Single-trip Dominance Gives Way to Multi-Trip Emergence

Single-trip policies held an 84.62% stake in the India travel insurance market in 2025, reflecting the nation’s episodic travel culture anchored in leisure, VFR, and purpose-defined business journeys. Visa-aligned offerings and duration-flexible add-ons further cemented single-trip popularity among travelers who book well in advance and prefer tailor-made protection. Annual multi-trip products, however, are accelerating at a 10.74% CAGR, benefiting from corporate mobility, student exchanges, and the rise of “workations.” The India travel insurance market size for the multi-trip segment is forecast to widen materially as insurers introduce auto-renewing plans and app-based trip activations that eliminate administrative friction.

Multi-trip holders exhibit higher insurance literacy and cross-buy propensity; students frequently add gadget covers, while business executives upgrade to higher medical limits. Digital dashboards enable customers to manage upcoming journeys, download embassy letters, and file claims, enhancing engagement loops that anchor loyalty. Insurers are using usage analytics to adjust pricing, rewarding low-risk frequent flyers with premium discounts that further tilt the value equation. As air connectivity densifies and visa-free corridors expand, the India travel insurance market will likely see a narrowing gap between single- and multi-trip penetration rates, especially within the urban affluent cohort.

By End User: Family Travelers Anchor Demand; Seniors Propel Premium Growth

Family Travelers contributed 41.36% of overall premiums in 2025, underscoring the collectivist ethos that drives group holiday and VFR itineraries. Policies optimized for nuclear and multigenerational groups bundle child-specific benefits, emergency family assistance, and group discounts, positioning insurers as holistic guardians of trip wellbeing. Word-of-mouth within extended families amplifies brand visibility, fostering repeat purchase loops that buttress the India travel insurance market.

Senior Citizens form the fastest-growing cohort at a 10.68% CAGR, spurred by rising life expectancy, greater disposable income, and cruise-led experiential tourism. Enhanced covers provide no-age-limit entry, pre-existing condition waivers, and concierge medical evacuation, commanding premium pricing that lifts margins. The India travel insurance market share for senior-specific products is consequently expanding as retirees prioritize health security over cost. Technology solutions, voice-enabled claim filing, and caregiver notifications further reduce friction, making insurance a seamless companion to globe-trotting retirement lifestyles.

By Distribution Channel: Intermediaries Hold Sway While Aggregators Surge

Agency networks and bancassurance channels retained 46.62% control of distribution in 2025, leveraging face-to-face advisory and cross-selling within bundled financial products such as forex cards and travel loans. High-trust relationships remain pivotal for first-time buyers who value personalized guidance. Nonetheless, aggregators are racing ahead at a 10.55% CAGR, propelled by transparent comparison engines, instant policy issuance, and mobile claim tracking that resonate with digital-native consumers.

The India travel insurance market size captured through online aggregators is projected to more than double by 2031 as PolicyBazaar and peers deepen AI-driven personalization and vernacular interfaces. Embedded sales on airline and OTA portals compress the purchase journey, nudging price-sensitive shoppers toward instant decisions without human intervention. Traditional intermediaries are responding by launching co-branded microsites and deploying video-chat advisors to preserve relevance in a channel-agnostic future.

Geography Analysis

Metropolitan clusters like Delhi NCR, Mumbai, Bangalore, Chennai, and Pune account for around 64.25% of total premium volume, buoyed by international gateway airports, higher per-capita incomes, and sophisticated distribution ecosystems. These cities exhibit outsized uptake of annual multi-trip and high-sum-insured products, reflecting cosmopolitan travel patterns and risk awareness. Tier-2 hubs such as Ahmedabad, Kochi, Indore, and Bhubaneswar are the fastest risers, benefiting from improved air connectivity, vernacular marketing, and aggregator-enabled digital penetration. The India travel insurance market size in these emerging cities is poised for double-digit expansion as outbound charters and Gulf employment lanes intensify.

Digital payment ubiquity supports nationwide scale-up: over 80% of smartphone users leverage UPI, enabling frictionless premium payment even where bank branches are sparse. Regional travel archetypes shape product demand: southern states demonstrate a stronger appetite for student and Gulf-bound worker covers, whereas northern states skew toward Schengen-compliant leisure policies. IRDAI’s forthcoming Bima Sugam marketplace promises a uniform digital infrastructure, narrowing urban-rural access gaps and standardizing KYC and policy issuance across geographies.

In frontier markets of the Northeast and smaller Himalayan states, awareness drives by local tourism boards and banks are seeking early adoption. The India travel insurance market will likely tap diaspora-linked travel corridors, Punjab-to-Canada and Kerala-to-Gulf, as cultural ties and remittance flows spawn recurring journeys. As domestic LCCs expand international routes from secondary airports, localized insurance kiosks and regional language chatbots will become a decisive factor in capturing first-time buyers.

Competitive Landscape

The India travel insurance market exhibits high concentration, with ICICI Lombard, Bajaj Allianz, Tata AIG, and HDFC ERGO forming the vanguard of premium collection. ICICI Lombard posted USD 0.84 million (INR 7.24 million) net profit in Q3 FY25, exemplifying the financial headroom these incumbents’ field for R&D and channel expansion. Strategic alliances are becoming pivotal: Bajaj Allianz’s August 2024 tie-up with HSBC India unlocked affluent NRIs, while ICICI Bank’s co-branded credit card with MakeMyTrip embeds trip insurance into broader travel finance ecosystems.

Technology investment is the sharpest competitive blade. API-native underwriting, AI-driven fraud detection, and chatbot claim lodgement compress service timelines, bolstering satisfaction metrics that directly influence repurchase. Settlement ratios serve as a public scoreboard; New India Assurance’s 98.74% benchmark sets industry expectations, forcing laggards to overhaul legacy workflows or risk attrition. Regulatory reforms, 100% FDI allowance, and use-and-file product approvals invite global carriers such as Generali to scale via joint ventures, intensifying rivalry and catalyzing product innovation.

Digital-first challengers leverage nimble tech stacks to undercut incumbents on turnaround time and niche risk covers, adventure sports, pet travel, and gadget protection. However, scale remains king; distribution reach through bank branches, travel agencies, and OTA integrations often determines ultimate share capture in the India travel insurance market. Cost-to-serve efficiency and omnichannel experience consistency will dictate competitive positioning as premium volumes migrate online.

India Travel Insurance Industry Leaders

ICICI Lombard General Insurance

Tata AIG General Insurance

HDFC ERGO General Insurance

Bajaj Allianz General Insurance

Reliance General Insurance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: IRDAI launched the Bima Sugam one-stop digital marketplace, slated for nationwide rollout by Dec 2025, to streamline policy comparison, purchase, and claims through UPI-like rails and standardized APIs.

- June 2025: Generali secured Central Bank of India as its joint-venture partner, retaining 74% ownership and gaining access to 80 million customers across 4,500 branches, thereby multiplying distribution touchpoints for travel protection bundles.

- July 2025: Thomas Cook India and NPCI introduced a RuPay prepaid forex card bundled with travel insurance, piloted in the UAE ahead of a global rollout, signaling further convergence of payments and protection.

- April 2025: Regency for Expats lifted customer satisfaction to 84%, with 44% attributing gains to faster claims and 41% to improved support, underscoring the payoff from AI-enabled service automation.

India Travel Insurance Market Report Scope

The report focuses on the complete background of the Indian Travel Insurance Market, which comprises an assessment of the developing market trends by segments, important changes in the market dynamics, and a market overview. India's Travel Insurance Market is Segmented By Insurance Coverage (Single-Trip Travel Insurance, Annual Multi-trip Travel Insurance, and Others), By Distribution channels (Direct Sales, Online Travel Agents, Airports And Hotels, Brokers, and Other Insurance Intermediaries) and By End-User (Senior Citizens, Business Travelers, Family Travelers, and Others (Education Travelers, etc). The report offers market size and forecast values for the India Travel Insurance Market in USD million for the above segments.

By Coverage Type

| Single-trip Travel Insurance |

| Annual Multi-Trip Travel Insurance |

By End User

| Senior Citizens |

| Education Travelers |

| Business Travelers |

| Family Travelers |

| Other End-Users |

By Distribution Channel

| Insurance Intermediaries |

| Insurance Companies |

| Banks |

| Insurance Brokers |

| Insurance Aggregators |

| By Coverage Type | Single-trip Travel Insurance |

| Annual Multi-Trip Travel Insurance | |

| By End User | Senior Citizens |

| Education Travelers | |

| Business Travelers | |

| Family Travelers | |

| Other End-Users | |

| By Distribution Channel | Insurance Intermediaries |

| Insurance Companies | |

| Banks | |

| Insurance Brokers | |

| Insurance Aggregators |

Key Questions Answered in the Report

What is the current value of the India travel insurance market?

The India travel insurance market size is USD 1.29 billion in 2026 and is projected to rise to USD 2.12 billion by 2031.

Which coverage type is expanding fastest?

Annual Multi-Trip policies are the fastest growing, registering a 10.74% CAGR through 2031 as frequent travelers seek continuous protection.

Why is mandatory visa insurance important for Indian travelers?

Visa-linked mandates, especially in the Schengen area, make insurance a non-negotiable purchase and drive recurring demand for compliant policies.

How are digital aggregators reshaping distribution?

Platforms like PolicyBazaar offer instant comparisons and one-click purchasing, accelerating online adoption and pushing insurers toward API-first integration.

What challenges impede claims satisfaction?

Documentation hurdles, overseas provider coordination, and slow reimbursements create customer frustration, prompting industry-wide investment in AI-driven claims automation.

How will Bima Sugam affect the market?

The centralized marketplace will standardize digital KYC, lower distribution costs, and widen access to insurance products across urban and rural India.

Page last updated on: