Market Size of India Smart TV and OTT Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

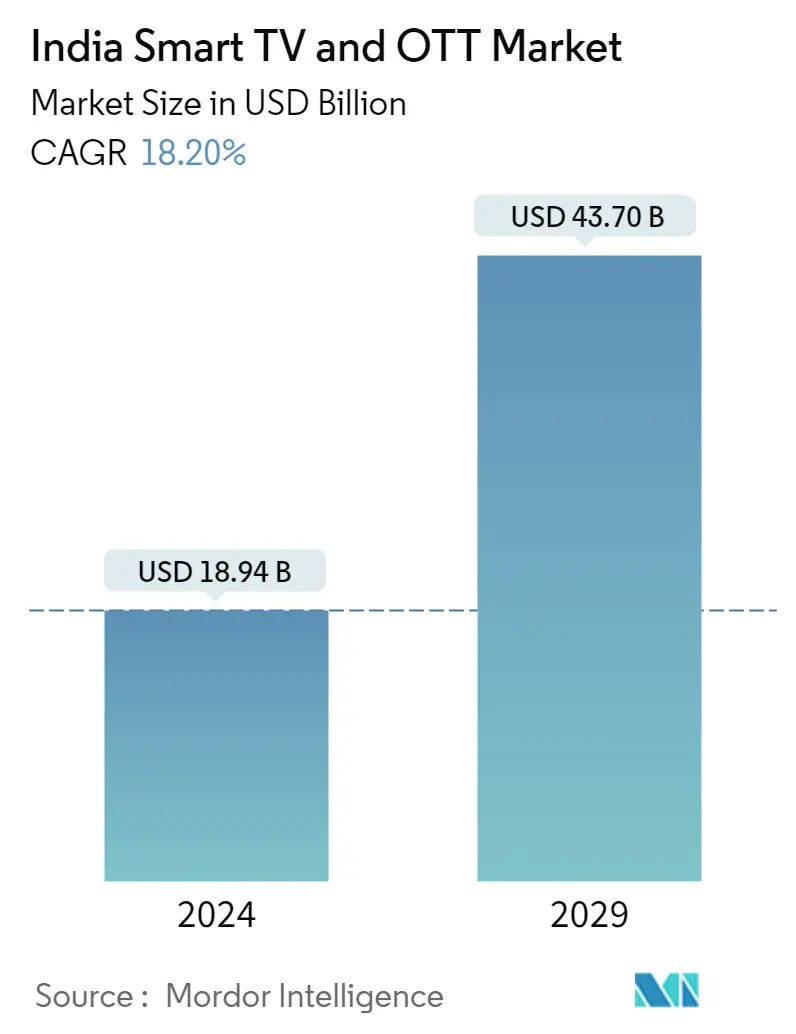

| Market Size (2024) | USD 18.94 Billion |

| Market Size (2029) | USD 43.70 Billion |

| CAGR (2024 - 2029) | 18.20 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

India Smart TV & OTT Market Analysis

The India Smart TV and OTT Market size is estimated at USD 18.94 billion in 2024, and is expected to reach USD 43.70 billion by 2029, growing at a CAGR of 18.20% during the forecast period (2024-2029).

As high-speed internet has become easily affordable, viewers/audiences that prefer good quality content prefer smart TVs over other television systems. Also, the increasing admiration for OTT streaming in audiovisual content is impacting the overall smart TV market in a positive manner in India.

- The shifting consumer preferences toward online content due to the increasing proliferation of high-speed internet in most parts of India provides an impetus to market growth. Substantial investment flows by video streaming media companies, like Netflix, Amazon Prime, and Hotstar, led to an increase in Pay-TV subscribers.

- Furthermore, a rise in disposable income levels and growing internet penetration in the country also contribute to an increase in sales of smart TVs and hence fuelling the market growth. Moreover, according to IBEF, the market size of the OTT video streaming market of India is forecasted to reach USD 5 billion by 2023, and India is projected to become one of the top 10 global OTT markets to reach USD 823 million by 2022.

- Households in India are at a cusp of transition, and a shift in preference has been witnessed from conventional TV sets to smart TV sets. Changing the lifestyle of the middle-income population is attributed to rising income levels, increasing awareness, adoption of new technology, and growing internet penetration. Additionally, government initiatives, primarily in tier-II and tier-III cities, are some of the key factors likely to bolster the growth of the Indian smart TV market during the forecast period.

- On the other hand, the growing demand for online streaming has opened opportunities for service providers to venture into the OTT space and distribute content via the internet. OTT content players, such as Netflix, Amazon, Hotstar, Sony Liv, and several other streaming services, are increasing their spending on marketing and local content to expand their customer base by luring them away from DTH and TV Cable services. Many of these platforms also partner with broadband providers to get the existing data users onboard by offering free bundled subscriptions. These continued efforts, coupled with changing consumer behavior, are driving the increased demand for the market.

- The COVID-19 outbreak affected the display industry negatively, with manufacturing operations temporarily suspended across major manufacturing hubs, leading to a substantial slowdown in production. Various key manufacturers, including Samsung, LG Display, and Xiaomi, suspended their manufacturing operations in China, India, South Korea, and Europe. However, the market has witnessed considerable growth in consumer demand during the pandemic as people stayed at their homes for extended periods. Further, the increased tendency to watch television due to the pandemic is also expected to continue impacting the market, resulting in its growth.

India Smart TV & OTT Industry Segmentation

Smart TV is a concurrence between computers and social TV, allowing users to use all features of computers or smartphones. Smart TV offers various features, such as internet accessibility, storage capacity, GPS system, and other entertainment features, such as games, music, and others. Smart TV is integrated with an internet connection that allows access to several popular websites, including Netflix, YouTube, Amazon Prime, and Hulu. The scope of the report is comprehensive and limited to India.

An over-the-top (OTT) application is an app or service that avails a product over the Internet and bypasses traditional distribution practices. Services that are available over the top are most typically related to media and communication and are generally, if not always, lower in cost than the traditional method of delivery.

The Indian smart TV and OTT market is segmented by OS type and price range (Tizen, WebOS, Android TV, etc.).

The market sizes and forecasts are provided in terms of value (USD billion) for all the above segments.

India Smart TV and OTT Market Size Summary

The Indian smart TV and OTT market is experiencing significant growth, driven by the increasing affordability of high-speed internet and a shift in consumer preferences towards online content. This transition is bolstered by substantial investments from major streaming companies like Netflix, Amazon Prime, and Hotstar, which have expanded their subscriber base by enhancing Pay-TV offerings. The rise in disposable income and growing internet penetration further fuel the demand for smart TVs, as households move from traditional TV sets to more advanced smart systems. Government initiatives, particularly in tier-II and tier-III cities, also play a crucial role in supporting market expansion. The COVID-19 pandemic, while initially disrupting manufacturing, ultimately led to increased consumer demand for smart TVs as people spent more time at home, a trend that continues to influence market dynamics.

The market is characterized by strategic investments and partnerships among key players, such as Samsung, Xiaomi, and Sony, aiming to capture significant market shares through innovative products and technologies. The integration of IoT technologies into smart TVs, along with features like ambient intelligence, enhances their appeal, contributing to market growth. The popularity of video-on-demand services and the rise of IPTV, supported by government digital transformation initiatives, further drive the adoption of smart TVs and OTT platforms. As India positions itself as a leading global OTT market, the industry presents lucrative opportunities for investment, with companies focusing on future technologies to maintain a competitive edge.

India Smart TV and OTT Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Threat of New Entrants

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Bargaining Power of Suppliers

-

1.2.4 Threat of Substitute Products

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Assessment of Impact of COVID-19 on the market

-

1.4 Industry Value Chain Analysis

-

-

2. MARKET SEGMENTATION

-

2.1 OS Type (Tizen, WebOS, Android TV, etc.)

-

2.2 Price Range

-

India Smart TV and OTT Market Size FAQs

How big is the India Smart TV and OTT Market?

The India Smart TV and OTT Market size is expected to reach USD 18.94 billion in 2024 and grow at a CAGR of 18.20% to reach USD 43.70 billion by 2029.

What is the current India Smart TV and OTT Market size?

In 2024, the India Smart TV and OTT Market size is expected to reach USD 18.94 billion.