Market Size of India Semiconductor Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

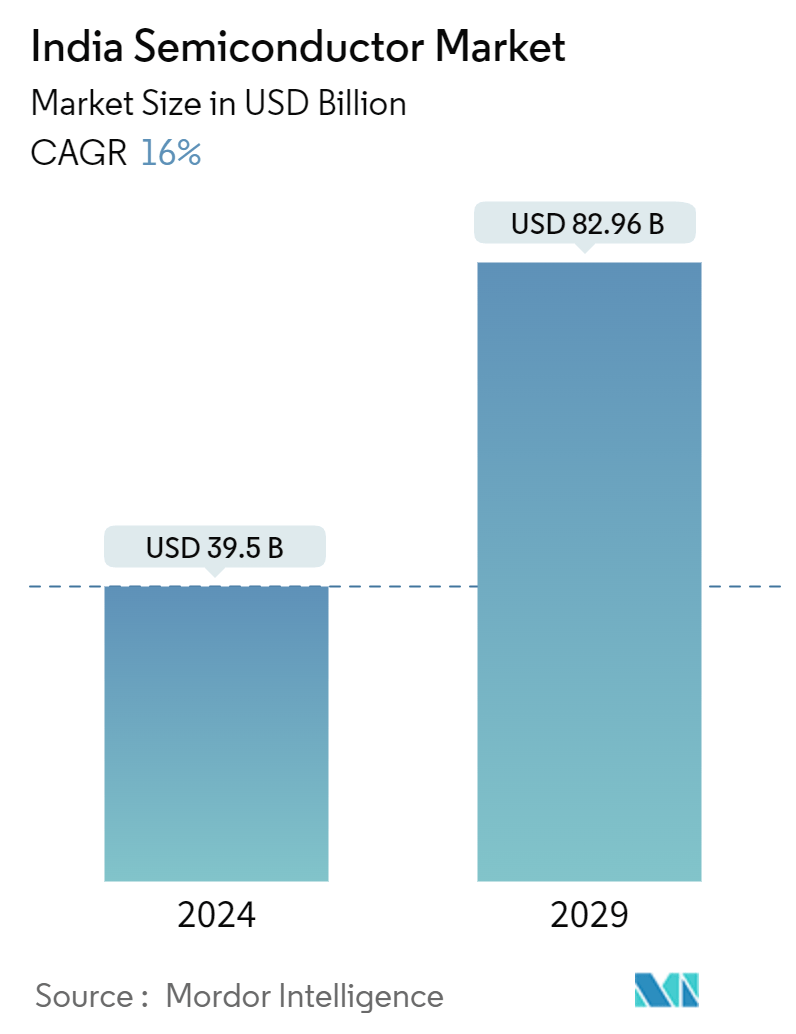

| Market Size (2024) | USD 39.5 Billion |

| Market Size (2029) | USD 82.96 Billion |

| CAGR (2024 - 2029) | 16.00 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

India Semiconductor Market Analysis

The India Semiconductor Market size is estimated at USD 39.5 billion in 2024, and is expected to reach USD 82.96 billion by 2029, growing at a CAGR of 16% during the forecast period (2024-2029).

- Semiconductors like silicon are essential for creating transistors, diodes, and integrated circuits, forming the foundation of modern electronics. They are crucial for managing electrical signals and facilitating the advancement of various electronic technologies. As the demand for data-driven applications grows, there is a noticeable trend toward using solid-state drives (SSDs) instead of traditional hard disk drives (HDDs). The adoption of non-volatile memory express (NVMe) technology is rapidly increasing, improving data transfer speeds.

- Furthermore, there is a noticeable trend in consumer electronics in India toward embracing advanced technologies and digitalization. This includes a growing preference for smart home devices such as IoT-enabled products like smart TVs, speakers, and appliances. The smartphone market is also seeing a shift toward affordable yet feature-packed models, leading to an increase in smartphone usage.

- The use of smartphones and digitalization efforts are also driving the demand for high-capacity RAM modules. The gaming industry's growth is also sparking interest in faster and more efficient memory solutions. An example of this is the upcoming production of India's first domestically made memory chip in Gujarat due to a lucrative deal with South Korea's Simmtech.

- Mumbai and Pune are becoming important hubs for semiconductor design and manufacturing, with a strong emphasis on innovation, research, and development. The regions are experiencing growth in startups and collaborations, leading to a thriving ecosystem. The increasing use of cutting-edge technologies like AI, IoT, and 5G is fueling the need for advanced semiconductor products.

- India has the potential to greatly enhance its participation in global semiconductor value chains if the government continues to support investment policies, fosters a favorable regulatory and business environment, and refrains from implementing measures that may cause uncertainty. Over the next five years, India could potentially increase its presence in the semiconductor assembly, test, and packaging (ATP) sector by establishing up to five facilities and attracting fabs that manufacture older-generation semiconductors at 28 nm or higher.

- In addition, India and the United States announced a collaborative initiative on Critical and Emerging Technology (CET) aimed at expanding strategic technology partnerships and defense industrial cooperation between businesses, academic institutions, and government agencies of both nations. In 2023, the Semiconductor Industry Association (SIA) in the United States and the India Electronics and Semiconductor Association (IESA) agreed to work together on a "readiness assessment" to identify industry opportunities and promote the strategic development of their semiconductor ecosystem.

- India is also currently experiencing a significant moment and opportunity. The aftermath of the COVID-19 pandemic, along with global efforts to adjust supply chains, rising costs in China, advancements in technologies like AI and EVs, demographic changes, and various other factors have prompted multinational companies to reevaluate their global value chain structures in search of improved diversification, resilience, sustainability, and cost efficiency.

- In addition to this, India is currently actively seeking foreign investments to support its domestic semiconductor industry for the advancement and design of fabs, ATMP, and other related technologies. One example of this is the Government of Assam’s efforts to fast-track the establishment of a semiconductor unit in Morigaon, achieved through a 60-year lease agreement with the Tata Group for more than 170 acres of land and an investment of INR 270 billion (USD 3.22 billion). Furthermore, approval has been granted for Tata's semiconductor chip fabrication unit in Gujarat with a budget of nearly INR 500 billion (USD 5.97 billion)

- India is fortunate to have a significant number of design engineers. However, there is a noticeable shortage of semiconductor engineers with expertise in device physics and process technology, which is crucial for chip fabrication and manufacturing and is significantly hindering market growth. It is anticipated that the semiconductor industry in India will encounter a deficit of 250,000 to 300,000 professionals in various sectors, such as research and development, manufacturing, design, and advanced packaging, by 2027.

India Semiconductor Industry Segmentation

The market is defined by the revenue accrued from the sales of various types of semiconductor devices in the Indian market, such as discrete semiconductors, optoelectronics, sensors and actuators, and integrated circuits (analog, micro, logic, and memory) in various end-user industries, such as computer, communication (wireline and wireless), automotive, and consumer.

The Indian semiconductor market is segmented by semiconductor device type ((discrete semiconductor, optoelectronics, sensors, and actuators, integrated circuits (analog, micro, logic, and memory)), end-user industry ((computer, communication (wireline and wireless), automotive, consumer, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Semiconductor Device Type | ||||||

| Discrete Semiconductor | ||||||

| Optoelectronics | ||||||

| Sensors and Actuators | ||||||

|

| By End-user Industry | |

| Computer | |

| Communication (Includes Wireline and Wireless) | |

| Automotive | |

| Consumer | |

| Other End-user Industries (Industrial, Government, etc.) |

India Semiconductor Market Size Summary

The Indian semiconductor market is poised for significant growth, driven by the increasing demand for advanced electronic technologies and digitalization. Semiconductors, essential for modern electronics, are witnessing a shift towards solid-state drives and non-volatile memory express technology, enhancing data transfer speeds. The consumer electronics sector is embracing IoT-enabled smart home devices and affordable smartphones, further fueling the demand for high-capacity RAM modules. The gaming industry's expansion is also contributing to the need for faster memory solutions. Regions like Mumbai and Pune are emerging as hubs for semiconductor design and manufacturing, supported by innovation and research. The government's supportive investment policies and strategic collaborations, such as the initiative with the United States on Critical and Emerging Technology, are expected to bolster India's position in the global semiconductor value chain.

India's semiconductor industry is experiencing a transformative phase, with significant investments and initiatives aimed at enhancing domestic capabilities. The 'Make in India' initiative and the establishment of semiconductor units, such as Tata Group's fabrication plant, are pivotal in achieving self-reliance in chip production. The automotive and EV sectors are also driving demand for semiconductors, with government policies and industry investments promoting local production and adoption of electric vehicles. The market is characterized by the presence of key players like Tata Group, HCL Technologies, and global entities such as AMD and Foxconn, who are actively investing in strategic partnerships and product developments. The expansion of the sensor market, driven by automation and IoT advancements, further complements the growth trajectory of the semiconductor industry in India.

India Semiconductor Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Buyers/Consumers

-

1.2.2 Bargaining Power of Suppliers

-

1.2.3 Threat of Substitute Products

-

1.2.4 Intensity of Competitive Rivalry

-

1.2.5 Threat of New Entrants

-

-

1.3 Assessment of the Impact of COVID-19 and Macroeconomic Factors on the Market

-

1.4 Semiconductor Industry Value Chain Analysis

-

1.4.1 Supply Chain Analysis

-

1.4.2 Focus Areas in the Value Chain and Type of Projects Currently Encouraged by India

-

-

1.5 Global Semiconductor Industry Analysis

-

1.6 Largest Semiconductor Clusters in India and Expected Largest Manufacturing Hubs

-

1.7 Analysis of Government Regulations and Incentive Programs

-

1.7.1 Government Initiatives/Schemes in India and Ways to Access the Schemes

-

-

1.8 Eligibility Criteria and Fiscal Support for Various Categories (Silicon Semiconductor Fab, Display Fab, Compound Semiconductor/SiPh/Sensors Fab and OSAT/Assembly/Testing)

-

1.9 SWOT Analysis of Semiconductor IC Industry in India (IC Design, IC Fabrication, and Assembly/Test/Packaging)

-

1.10 Workforce Analysis for the Indian Semiconductor Industry

-

1.11 Semiconductor Component Sourcing Analysis

-

1.12 Semiconductor Design Market Analysis

-

1.13 List of Key Stakeholders and Their Role in Shaping the Semiconductor Industry in India

-

1.14 Challenges in Setting up a Semiconductor Manufacturing Plant in India

-

-

2. MARKET SEGMENTATION

-

2.1 By Semiconductor Device Type

-

2.1.1 Discrete Semiconductor

-

2.1.2 Optoelectronics

-

2.1.3 Sensors and Actuators

-

2.1.4 Integrated Circuits

-

2.1.4.1 Analog

-

2.1.4.2 Micro

-

2.1.4.3 Logic

-

2.1.4.4 Memory

-

-

-

2.2 By End-user Industry

-

2.2.1 Computer

-

2.2.2 Communication (Includes Wireline and Wireless)

-

2.2.3 Automotive

-

2.2.4 Consumer

-

2.2.5 Other End-user Industries (Industrial, Government, etc.)

-

-

India Semiconductor Market Size FAQs

How big is the India Semiconductor Market?

The India Semiconductor Market size is expected to reach USD 39.5 billion in 2024 and grow at a CAGR of 16% to reach USD 82.96 billion by 2029.

What is the current India Semiconductor Market size?

In 2024, the India Semiconductor Market size is expected to reach USD 39.5 billion.