India Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

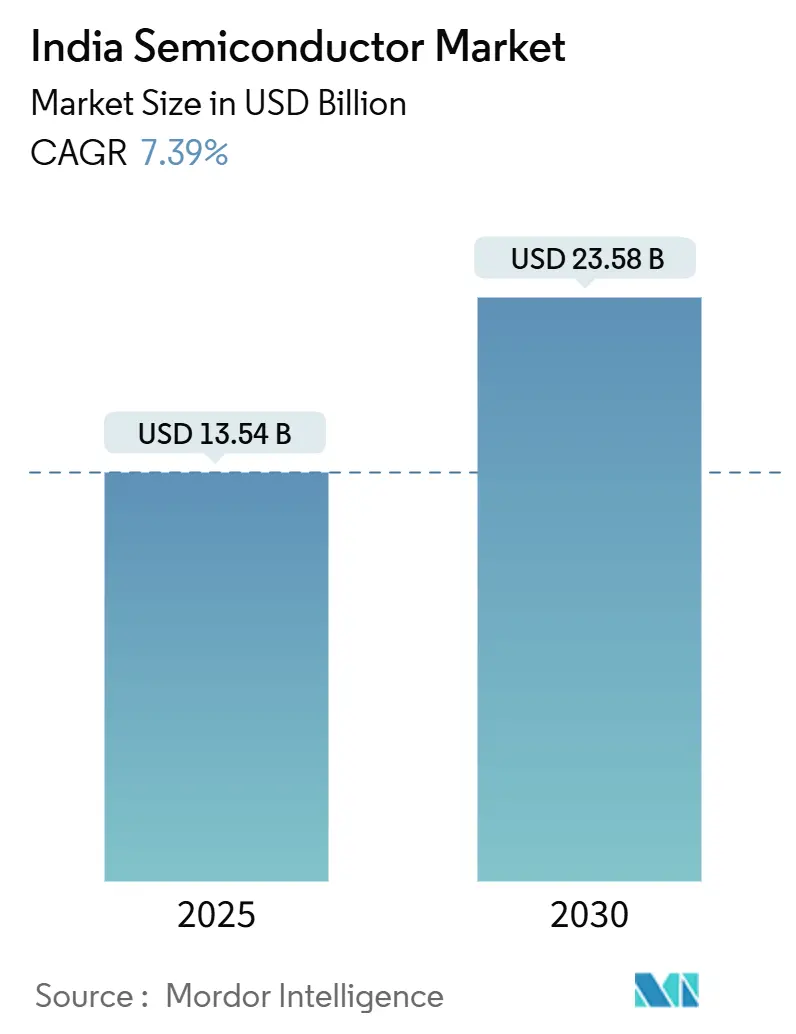

| Market Size (2025) | USD 13.54 Billion |

| Market Size (2030) | USD 23.58 Billion |

| Growth Rate (2025 - 2030) | 7.39% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Semiconductor Market Analysis by Mordor Intelligence

India’s semiconductor market size is valued at USD 13.54 billion in 2025 and is projected to reach USD 23.58 billion by 2030, advancing at a 7.39% CAGR. Capacity expansions supported by the Production Linked Incentive (PLI) and Design Linked Incentive (DLI) schemes, coupled with over INR 1.46 lakh crore of announced capital investment, continue to reposition India as a credible manufacturing alternative to traditional East Asian hubs.[1]Press Information Bureau, “India’s Semiconductor Revolution: Powering the Future of Electronics,” pib.gov.in Foreign technology collaborations have accelerated fabs, assembly plants, and advanced packaging lines, while policy certainty has encouraged vertically integrated supply-chain investments. At the same time, soaring domestic consumption of mobile devices, electric vehicles, and AI-enabled data-center services sustains a broad demand base that underpins revenue visibility for new entrants. Competitive intensity is moderate as global majors ally with Indian conglomerates to localize production, yet supply-side bottlenecks around utilities and talent remain decisive variables that could reshape cost structures over the forecast horizon.

Key Report Takeaways

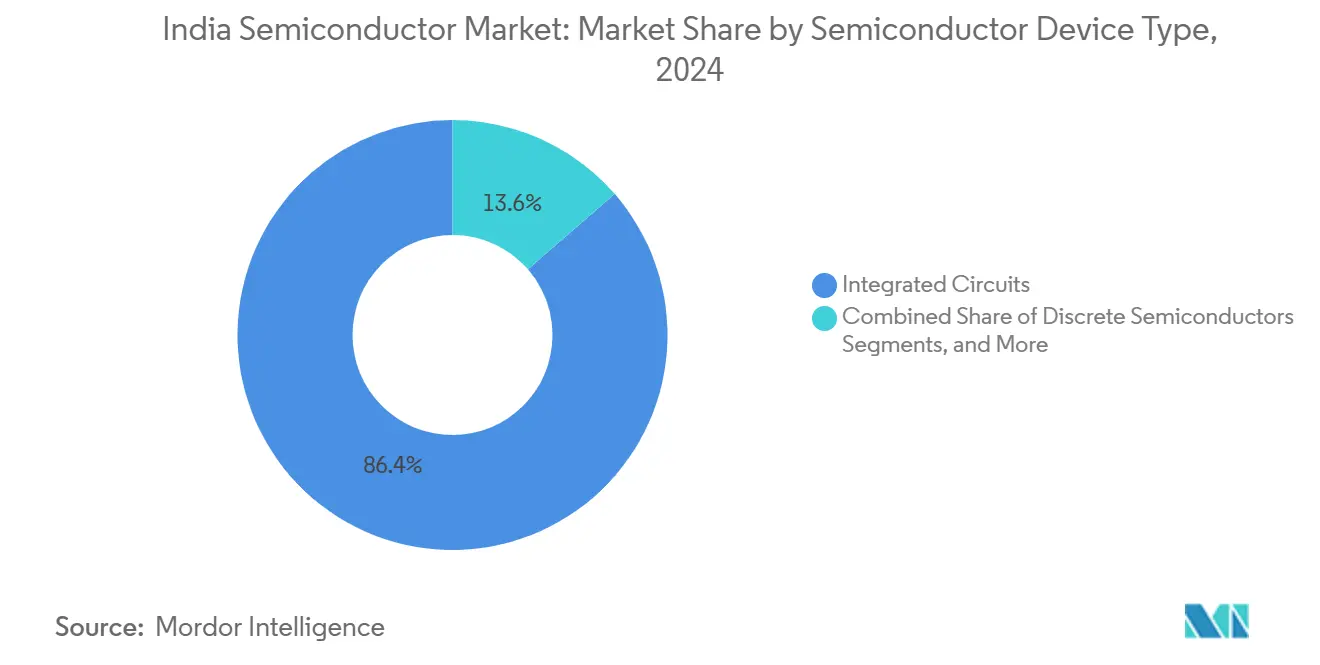

- By device type, integrated circuits held 86.4% of the India semiconductor market share in 2024.

- By business model, the design/fabless vendor segment accounted for 65.9% of the India semiconductor market size in 2024.

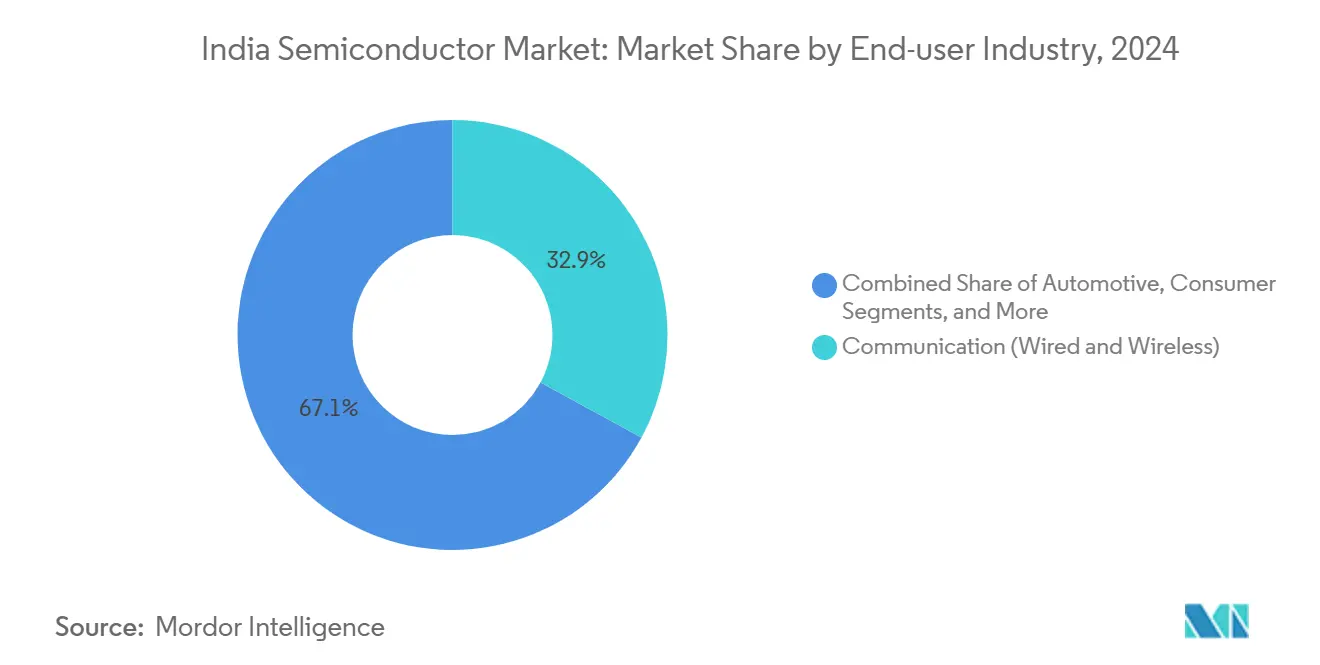

- By end-user industry, communication applications led with 32.9% revenue share in 2024, while AI workloads are expanding at a 9.6% CAGR through 2030.

India Semiconductor Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentive schemes (PLI, DLI) accelerate domestic manufacturing | +2.1% | Gujarat, Assam | Medium term (2-4 years) |

| Rapid electrification of transport boosting power and MCU demand | +1.8% | Maharashtra, Tamil Nadu, Karnataka | Long term (≥ 4 years) |

| Data-center and AI workloads driving advanced-node imports | +1.5% | Mumbai, Chennai, Delhi NCR, Bengaluru | Short term (≤ 2 years) |

| 5G roll-out and BharatNet fiber expansion lifting RF/analog IC needs | +1.2% | National, rural and semi-urban | Medium term (2-4 years) |

| PLI-linked consumer-electronics localization expanding TAM | +0.9% | Gujarat, Tamil Nadu | Medium term (2-4 years) |

| Supply-chain resilience and import substitution mandate | +0.7% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Incentive Schemes (PLI, DLI) Accelerate Domestic Manufacturing

The 56% budget jump to INR 9,000 crore for PLI in FY 2025-26 signals unwavering fiscal backing for semiconductor projects. Central subsidies covering 50% of capital outlay enable Tata Electronics to proceed with its USD 11 billion Dholera fab without eroding global price competitiveness. Complementary DLI funds support 22 design houses, ensuring an IP pipeline that feeds local fabs and outsourced assembly lines. Single-window clearance and deemed-approval timelines further lower project uncertainty, allowing investors to compress time-to-market. As a result, committed private investments surpassed INR 1.52 lakh crore across five approved units, evidencing the multiplier effect of coordinated fiscal policy.

Rapid Electrification of Transport Boosting Power and MCU Demand

Electric-vehicle penetration is forecast to cross 40% of new-vehicle sales by 2030, lifting demand for power management ICs, silicon-carbide MOSFETs, and automotive-grade microcontrollers.[2]ET Manufacturing, “From imports to Made-in-India: Why localising EV manufacturing is key,” manufacturing.economictimes.indiatimes.com Battery packs and traction motors, currently at 10-20% domestic content, represent immediate substitution opportunities for Indian fabs targeting legacy 28-nm and 40-nm nodes. Automotive OEMs are also localizing charging infrastructure, which shares semiconductor BOMs with renewable-energy inverters, thereby creating stacked demand across mobility and energy segments. State EV policies in Maharashtra and Tamil Nadu add procurement incentives that ripple downstream into semiconductor orders. Over the long term, the convergence of automotive, grid, and storage electronics is expected to lock in base-load demand for domestically produced power devices.

Data-Center and AI Workloads Driving Advanced-Node Imports

Data-center installed capacity is on track to add 500 MW between 2025 and 2026, a 26% compound expansion that translates into high-volume orders for GPUs, high-bandwidth memory, and switch ASICs. NVIDIA has already deployed tens of thousands of Hopper GPUs through partnerships with Reliance Industries and Yotta Data Services, delivering an aggregate 180 exaflops of compute power. Government outlays of INR 10,732 crore (USD 1.22 billion) for AI infrastructure further solidify near-term import demand for 7-nm and below devices. While silicon will continue to come from overseas foundries, domestic OSAT firms gain an entry point into advanced packaging, high-density organic substrates, and testing services that capture value before final system integration.

5G Roll-out and BharatNet Fiber Expansion Lifting RF/Analog IC Needs

India completed nationwide 5G coverage across 779 districts by October 2024, commissioning more than 460,000 base stations that incorporate RF front-end modules, GaN power amplifiers, and beam-forming ASICs. Parallel BharatNet fiber backhaul has reached 4 million km, supporting both consumer and industrial 5G use-cases. The Telecom Technology Development Fund allocates 5% of Universal Services Obligation corpus to domestic R&D, encouraging indigenous RF chip design. Newly launched local start-ups such as Ananant Systems are already sampling base-band silicon for BSNL trials, indicating early traction for homegrown telecomm components that can progressively displace imports.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited ultrapure water and power infrastructure raising costs | -1.4% | Gujarat, Assam, Karnataka | Medium term (2-4 years) |

| IP protection and design-ecosystem gaps deter foreign foundries | -1.1% | Nationwide | Long term (≥ 4 years) |

| Skill shortage in advanced-node process engineering | -0.9% | Bengaluru, Chennai, Pune | Medium term (2-4 years) |

| Global foundry over-capacity clouds ROI in India | -0.8% | Global, domestic fabs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Ultrapure Water and Power Infrastructure Raising Costs

Tata’s Dholera project alone requires 4-6 million gallons per day of 18-megohm-cm ultrapure water, stressing local water grids and necessitating dedicated desalination as well as polishing plants.[3]Machine Maker, “The Role of Ultrapure Water in India's Semiconductor Industry,” themachinemaker.com Continuous 24/7 power supply within 1% voltage tolerance adds expensive redundant sub-stations and energy-storage systems, inflating capex by 15-20%. Although Gujarat’s plug-and-play industrial parks offset part of the burden, water-treatment outlays, wastewater recycling mandates, and backup power still elevate fixed operating costs relative to established hubs such as Hsinchu and Dongguan. Until common-utility corridors mature, new entrants must factor a higher total cost of ownership into capital budgeting.

Skill Shortage in Advanced-Node Process Engineering

India needs 250,000-300,000 semiconductor specialists by 2027, yet current availability skews toward design rather than sub-28-nm process control. Clean-room tool engineers, lithography technicians, and yield-analysis scientists remain scarce, commanding premium salaries exceeding INR 2.5 crore (USD 0.29 million), which compress margins for start-up fabs. The Chips-to-Startup program aims to train 85,000 professionals via partnerships with IISc and Purdue University, but knowledge-transfer gaps persist in areas such as EUV tool calibration and advanced defect metrology. Without sustained talent development, fabs risk lower utilization and slower yield-ramp, eroding projected returns on multibillion-dollar investments.

Segment Analysis

By Device Type: Integrated Circuits Drive Market Dominance

Integrated circuits contributed 86.4% of India's semiconductor market revenue in 2024 and are forecast to grow at an 8.3% CAGR through 2030, keeping the India semiconductor market size heavily weighted toward logic, memory, and mixed-signal devices. Smartphone proliferation, 5G base-station rollouts, and AI accelerators in hyperscale data centers collectively underpin volume growth for high-pin-count SOCs and DRAM. The India semiconductor market share for ICs benefits further from Tata’s planned 28-nm line, which will focus on application processors and power-management chips for mobiles and EVs. Memory suppliers such as Micron are expected to produce first-generation LPDDR modules at the Sanand plant by late 2024, addressing latency-sensitive consumer and industrial applications.

Discrete devices, optoelectronics, and sensors constitute the remaining 13.6% share, yet each niche aligns with high-growth national priorities. Discrete power semiconductors serve solar inverters and EV fast-chargers, while LED drivers and image sensors enjoy tailwinds from smart-city investment and ADAS adoption. Sensor and MEMS suppliers tap IoT deployments across manufacturing and agriculture, often shipping alongside gateway SOCs designed domestically. Government incentives worth INR 22,919 crore under the Electronics Component Manufacturing Scheme specifically target such sub-assemblies, reinforcing backward integration aims. Over the forecast period, import substitution of discretes and MEMS is expected to shave nearly USD 2 billion off annual component bills, strengthening the value proposition for full-stack manufacturing.

By Business Model: Design/Fabless Vendors Lead Market Structure

Design and fabless enterprises owned 65.9% of 2024 revenue, highlighting India’s 20-year head start in chip architecture and IP design. More than 200 captive R&D centers operated by multinationals such as Intel and Qualcomm employ 125,000 engineers who deliver tape-outs across CPU, GPU, and modem portfolios. The India semiconductor industry further benefits from DLI grants that reimburse up to 50% of verified design costs, nurturing local fabless houses developing AI inference engines and automotive microcontrollers. Consequently, the India semiconductor market size will continue to skew toward royalty-rich design revenues even as wafer output scales.

Integrated Device Manufacturer (IDM) presence remains nascent yet significant. Tata-Powerchip’s joint venture introduces India’s first unified design-to-package chain, serving both captive automotive demand and third-party fabless clients. Micron’s assembly plant and CG Power’s OSAT venture with Renesas expand the local outsourcing landscape, allowing fabless startups to access domestic backend capacity. Capital barriers still limit rapid IDM proliferation: a leading-edge 12-inch fab costs USD 12-15 billion, and financial de-risking relies on sustained government subsidies and long-term customer pre-payments. Nevertheless, gradual integration of wafer fabs, packaging houses, and test facilities will recalibrate value capture away from pure design royalties toward balanced manufacturing revenues.

By End-user Industry: Communication Dominance with AI Acceleration

Communication networks accounted for 32.9% of India semiconductor market revenue in 2024, reflecting the nation’s 1.18 billion-subscriber base and its 779-district 5G footprint. Base-band processors, RF front-ends, and power-amplifier modules are replenished continuously as operators densify small-cell coverage and switch to 6 GHz mid-band. Meanwhile, the India semiconductor market share for AI workloads braces for a 9.6% CAGR on the back of hyperscale data-center build-outs fueled by public-sector AI funds and private cloud expansions. GPU demand currently supplied by overseas foundries opens avenues for local OSAT service providers to capture downstream value in high-density substrate attachment and burn-in testing.

Automotive remains the next hotbed of growth as semiconductor content per vehicle climbs from USD 500 in 2024 to USD 800 by 2030, driven by electrified drivetrains and advanced driver-assistance features. Consumer electronics persist as a volume anchor, with 310 million handsets produced domestically in 2024, leveraging locally packaged application processors and PMICs. Industrial IoT and factory automation uptake adds steady mid-single-digit growth, particularly for low-power MCUs and analog sensors. Finally, space and defense programs centered around ISRO’s reusable launch vehicles and MoD’s indigenization roadmap create niche but high-margin demand for radiation-hardened logic and secure FPGAs.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Gujarat’s Dholera Special Investment Region anchors the India semiconductor market with three sanctioned facilities that represent 61% of the approved project outlays. State policies grant up to 75% land-acquisition subsidies and ready-built utility corridors, allowing Tata’s USD 11 billion fab and Micron’s USD 2.75 billion assembly plant to advance on accelerated schedules.[4]Economic Times, “Gujarat announces Semiconductor Policy to attract new investments,” economictimes.indiatimes.com Rapid housing construction for 20,000 employees demonstrates the cluster’s self-contained ecosystem, supported by port proximity for chemical imports and device exports. Complementary photomask and specialty-gas suppliers are negotiating tenancy, signaling forward integration.

Assam’s Jagiroad cluster adds geographic diversity and energy security. Tata’s USD 3 billion OSAT facility will run entirely on renewable hydro power, making it India’s first carbon-neutral semiconductor plant. Lower land costs and Northeast industrial incentives offset logistical challenges, while local universities partner with national institutes to supply technician talent. Production of 48 million chips daily from 2025 positions the region as a strategic redundancy node that de-risks over-concentration in the West.

Karnataka sustains its role as design nerve-center. Bengaluru houses two-thirds of India’s semiconductor startups and 40% of captive global design centers, leveraging proximity to IISc and a robust venture-capital network. Although land and power costs deter mega-fabs, multiple advanced-packaging pilots are underway, including Kaynes Semicon’s fan-out line in Mysuru. Tamil Nadu and Telangana compete for Foxconn-HCL’s proposed assembly plant, with dual focus on consumer-electronics packaging and industrial sensor modules. Meanwhile, Maharashtra and Odisha publish new semiconductor policies offering capex reimbursements and tariff exemptions, signaling future geographic broadening as first-wave clusters approach full capacity.

Competitive Landscape

The India semiconductor market exhibits moderate concentration. Top global suppliers such as Intel, Samsung, and TSMC leverage partnerships with Tata Electronics, HCL Technologies, and CG Power to localize either wafer or backend stages. Micron’s Sanand campus already commands 12% of domestic assembly output, while Tata-Powerchip aims for 15% wafer-fabrication share by 2030. CG Power-Renesas targets automotive MCU and power-device verticals, diversifying the competitive set beyond memory and logic.

Competition is heating up in advanced packaging. Micron, Kaynes Semicon, and the Tata-Himax partnership are racing to secure substrate supplies and high-density interposer know-how, critical for AI accelerators and HPC devices. Market entrants' position on technology differentiation: Kaynes bets on silicon-photonics modules, while Tata aligns with ultralow-power display and AI edge sensors. Domestic fabless innovators such as Ananant Systems capture cross-layer value by co-optimizing software stacks with RF chipsets for telco clients. Overall, collaborative joint ventures remain the dominant mode of entry, but rising local IP portfolios hint at gradual power shifts toward indigenous design houses over the next decade.

India Semiconductor Industry Leaders

-

Tata Electronics Pvt Ltd

-

Vedanta-Foxconn Semiconductor Ltd.

-

MosChip Semiconductor Tech

-

Bharat Electronics Ltd

-

Applied Materials India Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: India Semiconductor Mission projected market value of USD 100-110 billion by 2030 and allocated additional AI infrastructure and talent funds targeting 85,000 trainees.

- June 2025: Micron’s Sanand plant hit clean-room validation, after USD 825 million first-phase investment.

- June 2025: Gujarat began constructing 1,500 residential units to house Tata’s fab workforce.

- May 2025: Government cleared Electronics Component Manufacturing Scheme with INR 22,919 crore outlay to lift domestic value-addition to 35% by 2030.

India Semiconductor Market Report Scope

The market is defined by the revenue accrued from the sales of various types of semiconductor devices in the Indian market, such as discrete semiconductors, optoelectronics, sensors and actuators, and integrated circuits (analog, micro, logic, and memory) in various end-user industries, such as computer, communication (wireline and wireless), automotive, and consumer.

The Indian semiconductor market is segmented by semiconductor device type ((discrete semiconductor, optoelectronics, sensors, and actuators, integrated circuits (analog, micro, logic, and memory)), end-user industry ((computer, communication (wireline and wireless), automotive, consumer, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3nm | ||

| 3nm | |||

| 5nm | |||

| 7nm | |||

| 16nm | |||

| 28nm | |||

| > 28nm | |||

| IDM |

| Design/ Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing/Data Storage |

| Data Center |

| AI |

| Government (Aerospace and Defense) |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By Integrated Circuit Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3nm | |||

| 3nm | ||||

| 5nm | ||||

| 7nm | ||||

| 16nm | ||||

| 28nm | ||||

| > 28nm | ||||

| By Business Model | IDM | |||

| Design/ Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing/Data Storage | ||||

| Data Center | ||||

| AI | ||||

| Government (Aerospace and Defense) | ||||

Key Questions Answered in the Report

How large is the India semiconductor market in 2025?

It is valued at USD 13.54 billion in 2025.

What CAGR will India’s semiconductor sector log through 2030?

The forecast CAGR is 7.39% over 2025-2030.

Which device category leads revenue?

Integrated circuits hold 86.4% market share and remain the largest category.

Which Indian state hosts the most semiconductor fabs?

Gujarat hosts three of five sanctioned units, making it the primary cluster.

Why is AI important for future chip demand in India?

AI data centers expanding by 500 MW and public funding of INR 10,732 crore are driving high-performance semiconductor imports and packaging opportunities.

Page last updated on: