Market Trends of India Real Time Payments Industry

This section covers the major market trends shaping the India Real Time Payments Market according to our research experts:

P2B Segment Will Hold Significant Market Share

- The real-time payment solutions for P2B transactions in India are majorly governed by the National Payments Corporation of India (NPCI). The retail payments space developed and matured with various systems operated and introduced by NPCI. To touch the lives of every Indian, NPCI has rolled out a variety of innovative retail payment products such as RuPay card scheme, IMPS, UPI, National Automated Clearing House (NACH), Aadhaar-enabled Payments System (AePS), Aadhaar Payments Bridge System (APBS), National Electronic Toll Collection(NETC), and Bharat bill pay system(BBPS). In addition, NPCI's alliance with international network partners (Japan Credit Bureau, Discover Financial Services, and China Union Pay) has paved the way for a global solution provider for the Indian real-time payment system.

- Aadhaar, a unique identification number in India issued to over 127 crore individuals Since its launch in 2009 in the country. Aadhaar-enabled e-KYC (electronic-Know Your Customer) has resulted in exponential growth of real-time payments in India. The use of Aadhaar also has leveraged authentication and processing of payments to merchants (P2B) and transactions made through Business Correspondents (BCs) (B2B) segments.

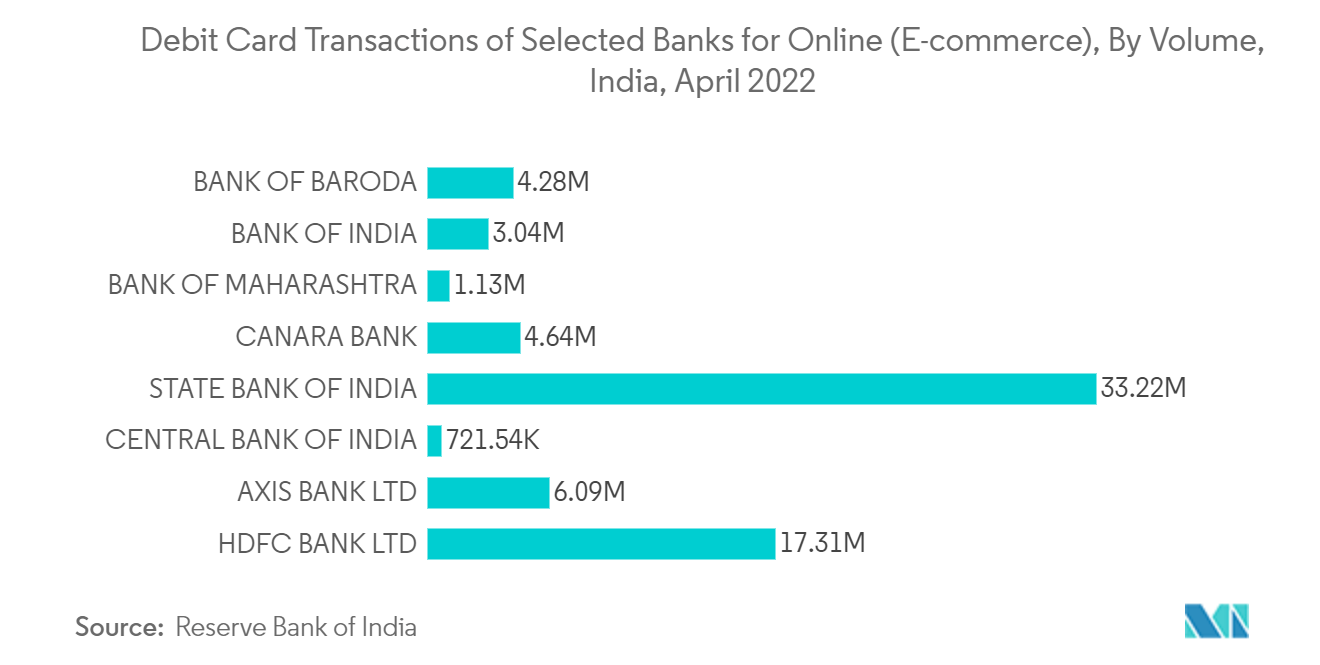

- India's UPI payment system has become the most inclusive mode of payment in India. As per the RBI data, over 26 crore unique users and five crore merchants are onboarded on the UPI platform. In May 2022, approximately 594.63 crores of transactions (INR 10.40 lakh crore) were processed through UPI, which includes (P2B) and (P2C) transactions. UPI facilitates transactions by linking Savings / Current Accounts through Debit Cards of users and is one of the key factors for developing real-time payment solutions in India.

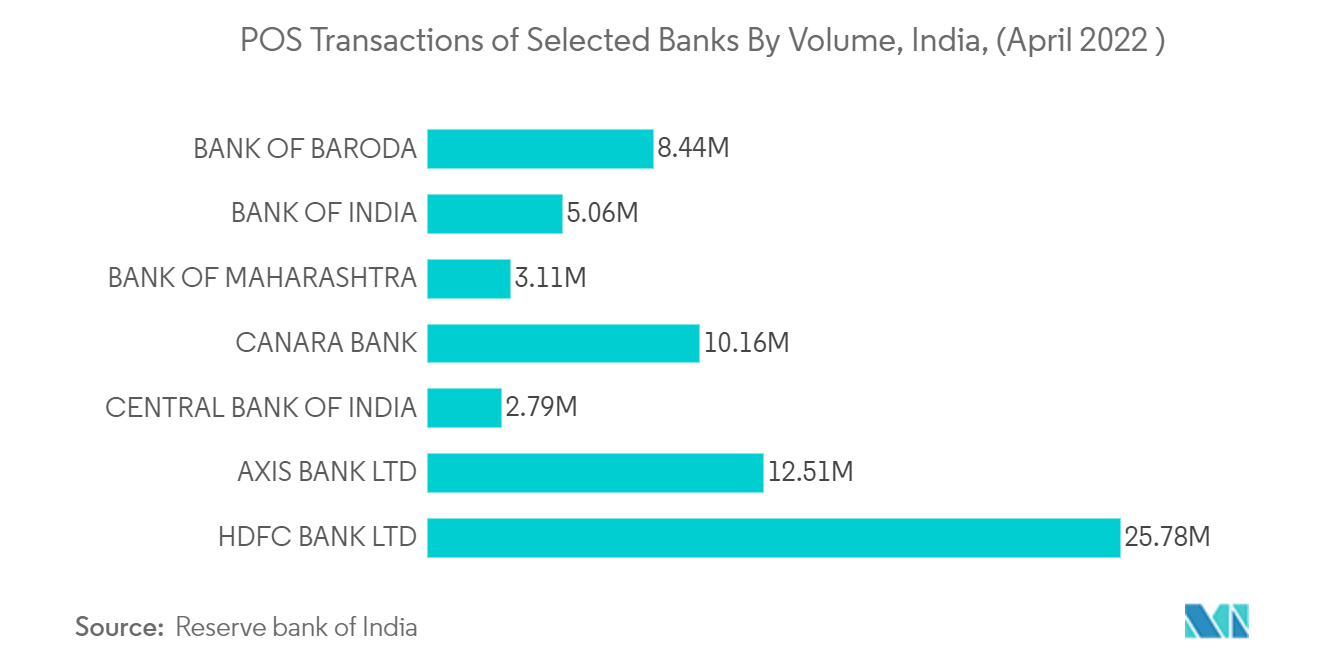

- Further, the Reserve Bank of India operationalized the Payments Infrastructure Development Fund (PIDF) Scheme in January 2021 to incentivize the deployment of payment acceptance infrastructures such as mPoS (mobile PoS), physical Point of Sale (PoS), Quick Response (QR) codes in the North Eastern States and Tier-3 to 6 centers. The Scheme had targeted 90 lakh Points of Sale (PoS) terminals and Quick Response (QR) codes to be deployed over three years (till end-2023) in response to the rise in number of P2B transactions, aiming to ease the payment mode for merchants.

- According to the report published by ACI Worldwide, India is leading the world in real-time payment transactions in the year 2021, with 48.6 billion transactions representing more than 40% of the global commerce emerging from the country. The number of real-time transactions in India was almost 2.6 times higher than that of China and approximately seven times higher than the combined real-time payments volume of the US, France, the UK, Canada, and Germany.

Understand The Key Trends Shaping This Market

Download PDF

Technological advancement will Further Drive the Real Time Payment Transfer

- With the rise in smartphone users and much-awaited 5G technology, India has been driving the real-time mobile payment market. For instance, The National Payments Corporation of India (NPCI) launched the UPI Lite service on-device wallet to enable people to conduct offline payments. In February 2022, UPI processed 4,527.49 million online transactions worth Rs 8,26,843. UPI Lite providing offline services will further boost the instant payment market in India.

- To upgrade the country's payment systems, RBI provided a communication backbone in the form of the satellite-based Indian Financial Network( INFINITE) using VSAT technology to the financial and banking sectors. IDRBT was entrusted with the task of designing and developing the communication network. The Closed User Group (CUG) Network uses VSAT technology. It is Time-division multiple access (TDMA)/Time-division multiplexing (TDM) network with STAR topology for Data and with Demand Assigned Multiple Access-Single Channel Per Carrier (DAMASCPC) overlaying with mesh topology for video and voice traffic.

- Indian Financial system uses contactless technology, one of the innovations in the card payments ecosystem which allows cardholders to "Tap and Go." These cards are becoming increasingly popular. To provide convenience in the use of such cards, RBI permitted relaxation in Additional Factor of Authentication (AFA) in case of Card Present (CP) transactions using Near Field Communication (NFC)-enabled EMV Chip and PIN cards for small values(INR 2,000). The limit was revised to INR 5,000, effective from January 01, 2021.

- IMPS is a 24*7 'fast payments' system introduced in 2010 and has become a widely accepted payment method between P2P modes. India was the fourth country after the UK, South Korea, and South Africa to introduce such a payment system. The system provides real-time funds transfer between the beneficiary and remitter with a deferred net settlement between banks. The system facilitates push transactions with a per-transaction limit of INR 2 lakhs.

- Unified Payments Interface (UPI) facilitates immediate money transfer through push and pull payments, utility bill payments, QR code (scan and pay) based payments, merchant payments, etc. While transacting, the UPI PIN is encrypted using Public Key Infrastructure (PKI) technology. UPI's framework comprises NPCI as network and settlement service provider, banks as Payment System Providers (PSPs), and issuer banks and beneficiary banks, apart from TPAPs such as Google Pay and WhatsApp. Non-bank PPI issuers have also provided this facility in the Indian market.