Market Trends of India Payments Industry

Point-of-Sale is Expected to Drive Market Growth

- Merchants and businesses are increasingly deploying new point-of-sale (PoS) terminals, driven by the growing popularity of credit card payments and the need to accommodate various customer payment preferences. However, there is a significant shift toward QR code-based UPI transactions. The emergence of contactless payments, QR code-based payments, and buy now pay later (BNPL) options continuously enhanced the convenience and security of PoS transactions, attracting more users and retailers to adopt these payment terminals to accept payments.

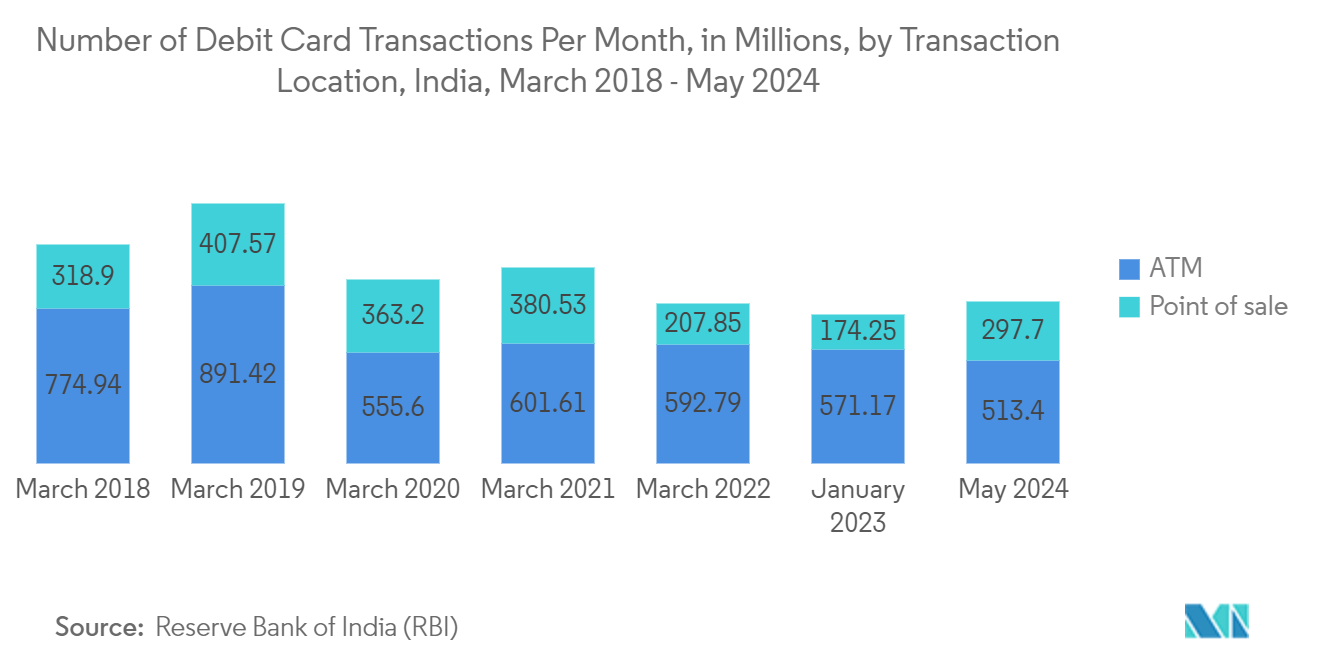

- The growth of e-commerce has established online shopping as a standard practice, with digital payments becoming the primary transaction method. This behavior has also influenced physical retail, where consumers increasingly prefer using digital wallets or cards at the time of payment. According to the Reserve Bank of India (RBI), in May 2024, nearly 298 million point-of-sale transactions were made through debit cards across India, compared to 174.25 million transactions in January 2023.

- Moreover, the mPOS trends in India are improving because of various initiatives of POS companies. For instance, RapiPay established hybrid micro-ATMs that can function as mobile point-of-sale (mPOS) machines. As a result, customers will be able to swipe credit cards in addition to debit cards for any transaction or purchase at a RapiPay station.

- The rising popularity of point-of-sale transactions using digital wallets, cards, and other modes is a key driver of the Indian payments market. Convenience, security, wider customer reach, and government initiatives are fueling this growth, along with continuous advancements in technology and a focus on financial inclusion. As PoS transactions become more seamless and accessible, they are poised to further drive market growth over the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

Retail Industry Expected to Hold Major Market Share

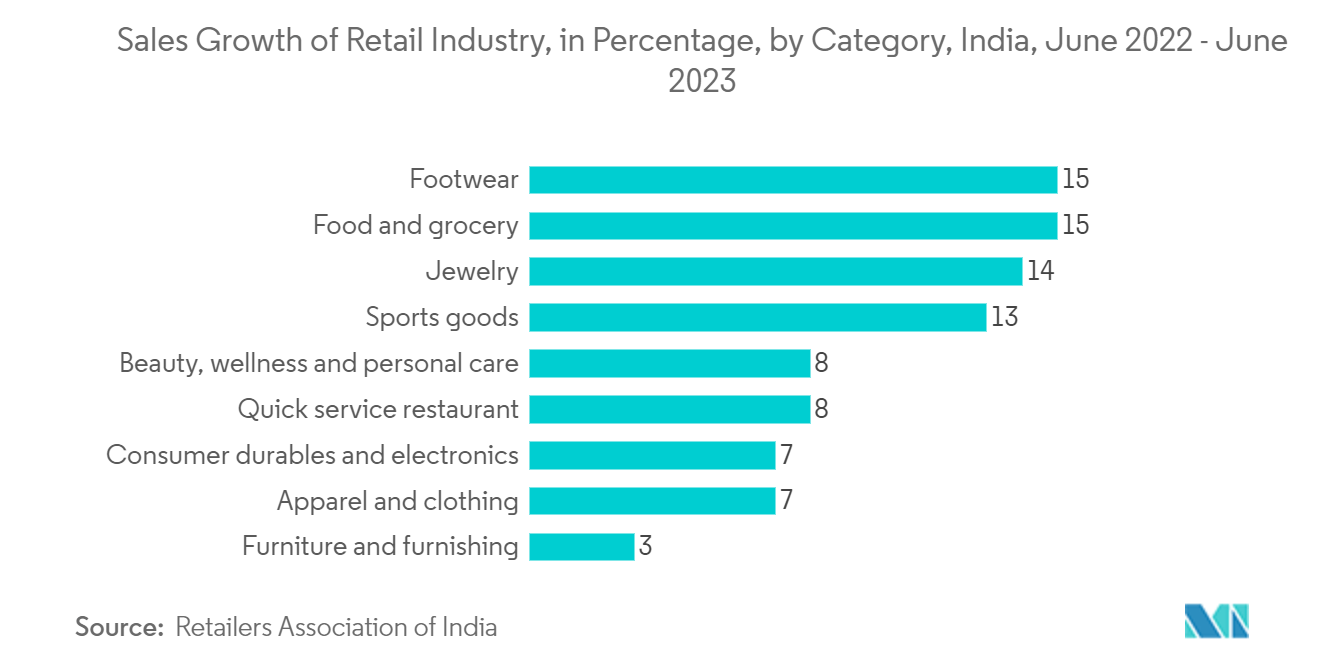

- As retail sales rise, there is a corresponding increase in the number of transactions. This translates to a higher demand for efficient and secure payment methods, including digital wallets, mobile payments, and point-of-sale (POS) systems. For instance, according to the Retailers Association of India, from June 2022 to June 2023, the retail industry experienced substantial growth across various categories. The food, grocery, and footwear categories experienced the highest sales growth at 15%, while jewelry followed closely with a 14% increase in sales. Furthermore, sports goods witnessed a 13% growth in sales across India.

- The Government of India’s initiatives to promote digitalization and cashless transactions are encouraging consumers to move away from cash. This fuels the adoption of digital payment methods within the retail industry. The government launched several initiatives to fuel digital payments in retail, including promoting digital wallets like BHIM and UPI, offering zero-transaction charges for RuPay debit cards and UPI payments, and setting up the Bharat QR code systems. These initiatives have made digital payments cheaper, faster, and more accessible for both consumers and retailers, leading to a significant increase in cashless transactions within India's retail industry.

- Furthermore, the Indian Ministry of Electronics and Information Technology has reported a significant expansion in the retail digital payment industry, which achieved a compound annual growth rate (CAGR) of 50.84% in transaction volume from 2017 to 2023. According to data from the Reserve Bank of India (RBI), it covers retail credit transfers, debit transfers, direct debits, prepaid payment instruments (PPI), and card payments. During the FY 2022–2023, India processed approximately 368.82 million digital transactions daily. Remarkably, by December 2023, the country had already exceeded 100 billion digital transactions for the FY 2023-2024. Several factors aided in market growth, with key contributors being advancements in payment infrastructure, significant progress in information and communications technology, and the implementation of a dynamic regulatory framework.

- The convenience of digital payments has significantly driven their adoption, leading to a surge in customer demand for digital transaction options at offline retail outlets. In response to the cash shortages at ATMs and bank branches following demonetization, many merchants, influenced by their customers' preferences, transitioned to accepting card and QR code payments.