| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 13.72 Billion |

| Market Size (2030) | USD 18.92 Billion |

| CAGR (2025 - 2030) | 6.63 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

India Paper and Paperboard Packaging Market Analysis

The India Paper And Paperboard Packaging Market size is worth USD 13.72 Billion in 2025, growing at an 6.63% CAGR and is forecast to hit USD 18.92 Billion by 2030.

The Indian paper and packaging industry has witnessed significant transformation driven by changing consumer preferences and technological advancements. With India's overall size of the packaging industry market in India valued at over USD 70 billion in 2023, paper packaging has emerged as a crucial segment gaining prominence across various sectors. The industry's structure is characterized by approximately 600 paper mills, with twelve major players dominating the market landscape. Despite the growing market, India's per capita paper consumption remains relatively low at 15 kg compared to the global average of 57 kg, indicating substantial growth potential in the domestic market.

Technological innovation and product development have become cornerstone strategies for industry players seeking competitive advantages. Paper-based packaging solutions have advanced significantly, particularly in food preservation applications, with corrugated board packaging gaining popularity for fresh produce transportation. The industry has witnessed the emergence of sophisticated manufacturing processes, including high-temperature bonding techniques for bacterial elimination and the implementation of aseptic packaging technologies utilizing hydrogen peroxide sterilization methods to enhance product shelf life.

Recent industry developments highlight the increasing focus on sustainable and innovative solutions. In October 2023, Pakka's collaboration with Brawny Bear to launch India's first compostable flexible packaging marked a significant milestone in sustainable packaging innovation. Similarly, in December 2023, Andhra Paper's investment in barrier-coated products and modernization initiatives, including the development of niche products like carry bags and straw paper, demonstrates the industry's commitment to diversification and technological advancement.

The paper sector in India is experiencing a shift toward value-added products and specialized solutions. Companies are increasingly investing in research and development to create innovative packaging solutions that address specific industry needs while maintaining environmental sustainability. The industry has seen the introduction of various specialized products, including cup stock, pharma print, and high BF virgin kraft, catering to diverse end-user requirements. This evolution is supported by automated manufacturing processes and quality control systems, enabling producers to meet international standards while maintaining cost-effectiveness and environmental responsibility.

India Paper and Paperboard Packaging Market Trends

Rapidly Growing Food Packaging Sector in India

The food packaging paper sector in India is experiencing substantial growth, driven by evolving consumer preferences and expanding food service infrastructure. The dairy industry serves as a prime example, with exports reaching 67,572.99 MT valued at USD 284.65 million in 2022-2023, necessitating advanced paper packaging solutions for maintaining product integrity. The rapid expansion of food service chains, exemplified by Domino's Pizza's presence across 393 cities with 1,816 stores as of March 2023, has created increased demand for specialized paper and paperboard packaging solutions. These paperboard packaging materials are particularly crucial for handling moist or greasy items, with specialized boards including white line chipboard and solid bleached surface board providing essential grease-resistant properties.

The health food segment is emerging as another significant driver for paper packaging innovation, with high-fiber breakfast products generating a market value of USD 0.3 billion in 2023. Paper packaging has become instrumental in various food industry sectors, including bakeries, snacks, and dry goods such as spices and tea. The cylindrical paper in packaging tubes offer efficient storage and transportation capabilities while maximizing shelf space utilization. Food producers, particularly prominent FMCG brands, are actively transitioning towards paper-based packaging materials, driven by the materials' versatility in protecting product freshness, ensuring safety, and maintaining nutritional value while offering customization options for brand visibility and consumer appeal.

Understand The Key Trends Shaping This Market

Download PDF

Growing Adoption of Environmentally Sustainable Packaging Across Different Industrial Sectors

The shift towards environmentally sustainable packaging solutions is gaining significant momentum across India's industrial landscape, particularly in the e-commerce sector, which generated USD 103 billion in online retail sales in 2023. This transition is characterized by the increasing adoption of corrugated boxes, which offer superior product protection through their fluted, structured interior while maintaining eco-friendly credentials. The sustainability drive is particularly evident in the Direct-to-Consumer (D2C) segment, which is projected to reach USD 60 billion by 2027, where brands are actively seeking packaging solutions that align with environmental consciousness while ensuring product protection.

The adoption of sustainable packaging is further reinforced by the material's inherent recyclability and its alignment with modern business sustainability goals. Packaging paper materials are becoming increasingly popular due to their eco-friendly properties and ability to be easily recycled and reused. This trend is particularly visible in the food and beverage industry, where manufacturers are setting ambitious targets to reduce plastic usage in favor of paper-based alternatives. The industry's commitment to sustainability is reflected in the development of innovative solutions, such as paper in packaging tubes for dry goods and specialized cartons for dairy products, which combine environmental responsibility with functional efficiency in protecting and preserving product quality.

Segment Analysis: By Product Type

Corrugated Boxes Segment in India Paper and Paperboard Packaging Market

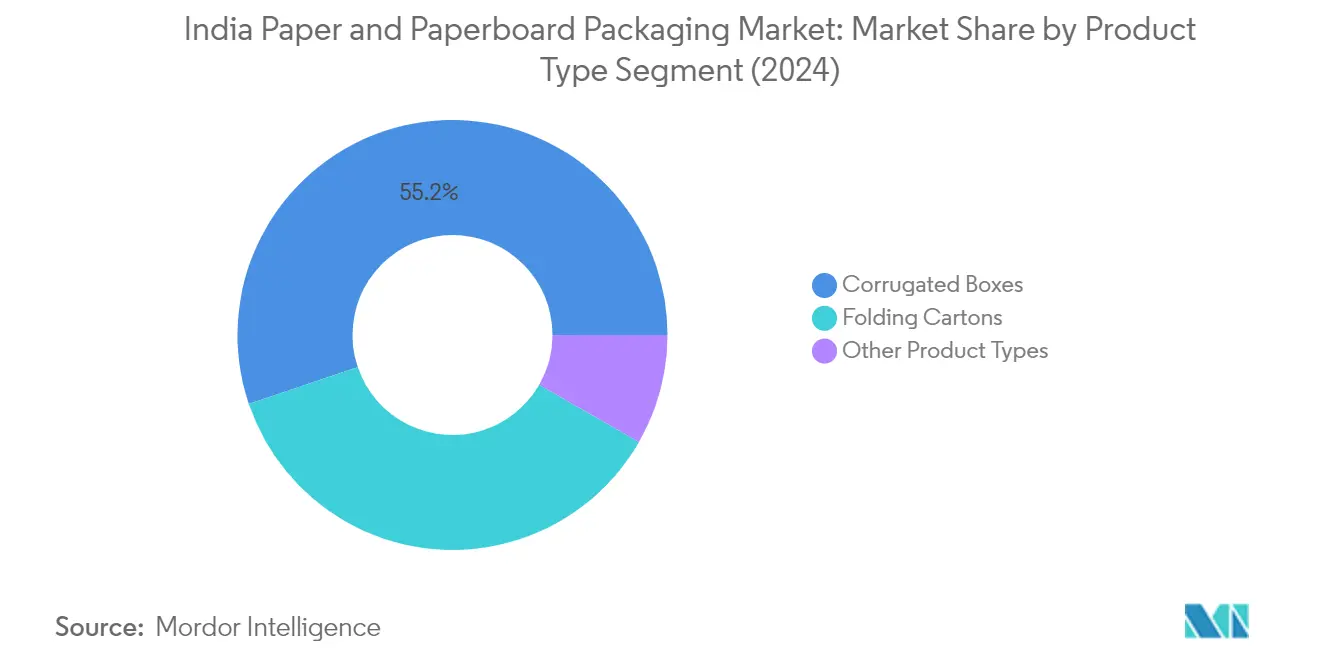

The corrugated box market size in India continues to dominate the Indian paper and paperboard packaging market, holding approximately 55% market share in 2024. This significant market position is driven by the explosive growth of e-commerce and advancements in digital printing technologies, as corrugated boxes represent about 80% of packaging demand in the e-commerce sector. The segment's strength is further reinforced by its versatility across various industries, from food and beverages to electronics and pharmaceuticals. Modern die-cut corrugated containers have gained immense recognition for their durability and customization capabilities, particularly in shipping specific items. The industry's eco-friendly nature, consuming about 7.5 million MT per year of recycled kraft paper, has also contributed to its market leadership.

Folding Cartons Segment in India Paper and Paperboard Packaging Market

The folding cartons segment is projected to experience robust growth at approximately 7% CAGR from 2024 to 2029, driven by increasing consumption of packaged foods and beverages in India. The segment's growth is characterized by significant technological advancements in manufacturing processes and rising demand for sustainable packaging solutions. The market is witnessing substantial investments in new capacities and expansion of existing capabilities by both local and international players. The growth is further supported by the increasing adoption of recycled-grade packaging in non-contact categories such as breakfast cereals and tea, along with the rising emphasis on innovative labeling and smart packaging solutions. The segment's expansion is also bolstered by the pharmaceutical sector's growing demand for paperboard cartons.

Remaining Segments in Product Type Segmentation

Other product types in the market, including flexible paper packaging and liquid cartons, play a crucial role in serving specific industry needs. These specialized packaging solutions are gaining traction due to their unique capabilities in addressing particular packaging requirements, especially in the food and beverage sector. The segment encompasses various innovative solutions such as paper pouches, kraft paper packaging, and aseptic liquid cartons, which are becoming increasingly popular due to their sustainability features. The versatility of these alternative packaging solutions, combined with their eco-friendly characteristics, makes them particularly attractive for businesses looking to differentiate their products while maintaining environmental responsibility.

Segment Analysis: By End-User Industry

Food Segment in India Paper and Paperboard Packaging Market

The food segment continues to dominate the Indian paper and paperboard packaging market, holding approximately 30% market share in 2024. This significant market position is driven by the rapidly growing food packaging sector in India, particularly in areas like packaged foods, bakery products, ready-to-eat meals, and processed foods. The segment's growth is further supported by increasing consumer awareness about sustainable packaging solutions and the shift from plastic to paper-based packaging materials. Major food manufacturers are making substantial efforts to provide sustainable materials and packaging, functional and convenient displays, and healthier food options, while paper bags are becoming increasingly popular in restaurants, hotels, and cafes.

Personal Care and Household Care Segment in India Paper and Paperboard Packaging Market

The personal care and household care segment is emerging as the fastest-growing segment in the Indian paperboard packaging market, with an expected growth rate of approximately 7% during 2024-2029. This growth is primarily driven by easier access, growing awareness, and changing lifestyles in the personal care sector. The segment is witnessing significant innovation in terms of sustainable packaging solutions, with manufacturers increasing the production of lightweight packaging solutions that have lower carbon footprints and are recyclable. The expansion of the cosmetics, personal hygiene, and household care industries, coupled with the increasing focus on eco-friendly packaging solutions, is providing significant growth prospects for industry participants.

Remaining Segments in End-User Industry

The other significant segments in the market include beverages, healthcare, and hardware and electrical products, each serving distinct packaging needs. The beverage segment is driven by the increasing demand for sustainable packaging solutions for fruit juices, alcoholic drinks, and meal replacement shakes. The healthcare segment benefits from India's position as a major pharmaceutical manufacturer and exporter, requiring specialized packaging solutions for medical products. The hardware and electrical products segment caters to the growing electronics and electrical equipment industry, with a focus on protective packaging solutions. These segments collectively contribute to the market's diversity and overall growth, each adapting to increasing sustainability requirements and changing consumer preferences.

India Paper and Paperboard Packaging Industry Overview

Top Companies in India Paper and Paperboard Packaging Market

The Indian paper market is characterized by companies focusing on sustainable innovation and technological advancement in their product offerings. Major players are investing heavily in expanding their manufacturing capabilities through state-of-the-art facilities and automated production lines to meet growing demand. Companies are increasingly adopting digital printing technologies and developing eco-friendly packaging solutions to align with environmental regulations and changing consumer preferences. Strategic partnerships and collaborations, particularly in the e-commerce sector, have become crucial for market expansion. The industry has witnessed significant investments in research and development centers for creating next-generation packaging solutions, while also emphasizing quality control systems and value-added services like design ideation and customization capabilities.

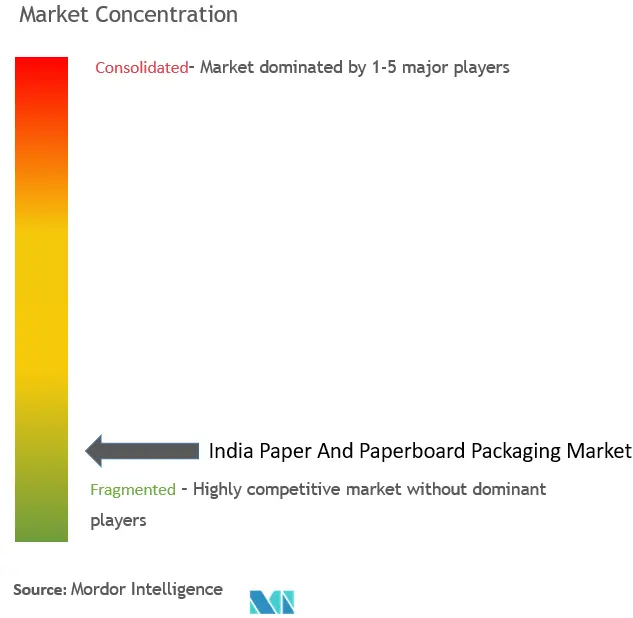

Market Fragmentation Drives Strategic Consolidation Moves

The Indian paper and paperboard packaging landscape exhibits a fragmented structure with a mix of global conglomerates and local specialists competing for market share. International players like WestRock and Oji Holdings have established strong footholds through strategic acquisitions and greenfield investments, while domestic players such as Parksons Packaging and TCPL Packaging maintain significant market presence through their extensive manufacturing networks and long-standing customer relationships. The market has witnessed increased consolidation through mergers and acquisitions, as larger players seek to expand their geographical presence and enhance their product portfolios.

The industry is experiencing a transformation with several companies focusing on vertical integration to better control their supply chains and maintain cost competitiveness. Major players are establishing multiple manufacturing units across different regions of India to ensure better market coverage and reduced logistics costs. The market has also seen the emergence of specialized players focusing on specific segments such as food packaging, pharmaceutical packaging, or e-commerce solutions, creating a diverse competitive landscape that caters to various end-user requirements. Paper packaging industries are particularly focusing on these niche segments to gain a competitive edge.

Innovation and Sustainability Drive Future Growth

Success in the Indian paper market increasingly depends on companies' ability to innovate while maintaining environmental sustainability. Market leaders are investing in advanced manufacturing technologies and developing recyclable packaging solutions to meet growing environmental concerns. Companies are also focusing on building strong relationships with e-commerce platforms and retail chains, while simultaneously developing specialized solutions for different industry verticals. The ability to provide end-to-end packaging solutions, including design services and logistics support, has become crucial for maintaining competitive advantage.

Future market success will require companies to balance cost efficiency with product innovation while addressing the growing demand for sustainable packaging solutions. Players need to focus on developing strong distribution networks and maintaining close relationships with key end-user industries such as food and beverages, pharmaceuticals, and e-commerce. The regulatory environment, particularly regarding plastic substitution and recycling requirements, is expected to play a crucial role in shaping future market dynamics. Companies that can effectively combine technological innovation with sustainable practices while maintaining cost competitiveness are likely to emerge as market leaders. Paper Packaging Pvt Ltd and other key players are at the forefront of this transformation, emphasizing the importance of sustainability in the overview of the paper and packaging industry.

India Paper and Paperboard Packaging Market Leaders

-

Trident Paper Box Industries

-

TGI Packaging Pvt. Ltd.

-

Kapco Packaging

-

OJI India Packaging Pvt. Ltd

-

Westrock India (Westrock Company)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

India Paper and Paperboard Packaging Market News

- January 2024: ITC Sunfeast Farmlite, a range of biscuits from ITC Foods, launched its new offering, Sunfeast Farmlite Digestive Biscuit Family Pack, in 100% outer paper bag packaging. It is available in 800 g SKU on the e-commerce platform Flipkart.

- January 2024: Ansa Folding Carton (AFC) has acquired a strategic stake in Rich Printers Private Limited (RPL) for INR 1,170 million (USD 14.17 million). This acquisition results in the combined entity operating five paper conversion manufacturing plants in India, positioning it as one of the country's largest pharmaceutical folding carton producers.

- December 2023: State Bank of India (SBI) has invested INR 499.9 million (USD 6.05 million) in Canpac Trends Private Limited, an Ahmedabad-based company specializing in paper-based packaging solutions. This strategic move into the paper packaging industry aims at capital appreciation, highlighting SBI's recognition of the sector's growth potential and profitability.

India Paper Packaging Industry Research- Table of Contents

1. INTRODUCTION

- 1.1 Study Assumption and Market Defintion

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis with Emphasis on Circular Economy

- 4.3 India Paper & Paperboard Packaging Market - PESTEL Analysis

- 4.4 Packaging Industry Landscape in India and Key Trends

- 4.5 Packaging Regulations, Policies, and Subsidies in India and Key Changes Impacting the Packaging Operations

5. MARKET DYNAMICS

- 5.1 Market Drivers & Restraints Analysis

- 5.2 Demand Analysis and Industry Trends

-

5.3 Demand Split for Flexible Packaging (%)

- 5.3.1 Organized vs. Unorganized

- 5.3.2 Direct vs. Indirect/Dealers Sales

- 5.4 Printing Technology Trends for Paper & Paperboard Packaging

- 5.5 Production Trends over the Past Three Years for Key Paper & Paperboard Packaging Formats

- 5.6 Raw Material Analysis for Paper & Paperboard

- 5.7 Trade Scenario for Paper & Paperboard Packaging - Corrugated Boxes, Folding Cartons, and Others

6. INDIA PAPER INDUSTRY STATISTICS

- 6.1 Domestic Paper Demand

- 6.2 Total Containerboard Capacity (Virgin and Recycled)

- 6.3 Import of Virgin and Recycled Container Board

-

6.4 Corrugated Paper or Paperboard

- 6.4.1 Import Value and Quantity

- 6.4.2 Export Value and Quantity

-

6.5 Cartonboard

- 6.5.1 Carton Board - Production Value and Volume

- 6.5.2 Carton Board - Import Quantity and Value

- 6.5.3 Carton Board - Export Quantity and Value

7. QUALITATIVE ANALYSIS BY PAPER GRADE

-

7.1 Cartonboard - By Grade

- 7.1.1 WLC - White Lined Chipboard (GD/UD and GT/UT)

- 7.1.2 FBB - Folding Boxboard (GC1/UC1 and GC2/UC2)

- 7.1.3 SBB - Solid Bleached Sulphate Board (SBS)

- 7.1.4 SUB - Solid Unbleached Sulphate Board (SUS)

-

7.2 Containerboard - By Grade

- 7.2.1 White Top Kraftliner

- 7.2.2 Unbleached Kraftliner

- 7.2.3 White Top Testliner

- 7.2.4 Unbleached Testliner

- 7.2.5 Waste-based Fluting

- 7.2.6 Semi-chemical Fluting

8. MARKET SEGMENTATION

-

8.1 By End-user Industry

- 8.1.1 Corrugated Packaging

- 8.1.1.1 Processed Food

- 8.1.1.2 Fresh Produce

- 8.1.1.3 Beverage

- 8.1.1.4 Personal Care & Cosmetics

- 8.1.1.5 Household Care

- 8.1.1.6 E-commerce

- 8.1.1.7 Other End-user Industries (Transportation & Logistics, Healthcare, and Consumer Durables, among Others)

- 8.1.2 Folding Cartons

- 8.1.2.1 Food & Beverage

- 8.1.2.2 Personal Care & Cosmetics

- 8.1.2.3 Healthcare & Pharmaceuticals

- 8.1.2.4 Tobacco

- 8.1.2.5 Electrical & Hardware

- 8.1.2.6 Other End-user Industries (Toy, Apparel, Automotive, and Household, among Others)

- 8.1.3 Liquid Cartons

- 8.1.3.1 Milk

- 8.1.3.2 Juices

- 8.1.3.3 Energy Drinks

- 8.1.3.4 Other End-user Industries (Dairy Products such as Buttermilk, Cream, Smoothies, etc.)

-

8.2 By Region

- 8.2.1 East

- 8.2.2 West

- 8.2.3 North

- 8.2.4 South

9. COMPETITIVE LANDSCAPE

-

9.1 Company Profiles*

- 9.1.1 TCPL Packaging Ltd

- 9.1.2 KCL Limited

- 9.1.3 Borkar Packaging Pvt. Ltd

- 9.1.4 Canpac Trends Pvt. Ltd

- 9.1.5 Trident Paper Box Industries

- 9.1.6 Westrock India (Westrock Company)

- 9.1.7 TGI Packaging Pvt. Ltd

- 9.1.8 Asepto (Uflex)

- 9.1.9 Tetra-pak India Private Limited

- 9.1.10 Parksons Packaging Ltd

- 9.1.11 Kapco Packaging

- 9.1.12 OJI India Packaging Pvt. Ltd

- 9.2 List of Customers by Region in India

- 9.3 List of Major Unorganized Market Players in India by Region

10. SUSTAINABILITY TRENDS FOR INDIA PACKAGING INDUSTRY

11. FUTURE OUTLOOK OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

India Paper and Paperboard Packaging Industry Segmentation

The study tracks the demand for paper and paperboard packaging products like folding cartons, corrugated boxes, and others, which are frequently used for packaging food and beverage products, such as juices, milk, and cereals. There are numerous grades of paperboard packaging. Paperboard is the most common material used to make containers, like folding cartons. Paperboard requires pulping, optional bleaching, refining, sheet forming, drying, calendaring, and winding to manufacture paper.

The paper packaging industry in India is segmented by end-user industry (corrugated packaging [processed food, fresh produce, beverage, personal care & cosmetics, household care, e-commerce, other end-user industries (transportation & logistics, healthcare, and consumer durables, among others)], folding cartons [food & beverage, personal care & cosmetics, healthcare & pharmaceuticals, tobacco, electrical & hardware, other end-user industries (toy, apparel, automotive, and household, among others)], liquid cartons [milk, juices, energy drinks, other end-user industries (dairy products such as buttermilk, cream, smoothies, etc.)]), by region (east, west, north, south). The report offers market forecasts and size in value (USD) for all the above segments.

| By End-user Industry | Corrugated Packaging | Processed Food | |

| Fresh Produce | |||

| Beverage | |||

| Personal Care & Cosmetics | |||

| Household Care | |||

| E-commerce | |||

| Other End-user Industries (Transportation & Logistics, Healthcare, and Consumer Durables, among Others) | |||

| Folding Cartons | Food & Beverage | ||

| Personal Care & Cosmetics | |||

| Healthcare & Pharmaceuticals | |||

| Tobacco | |||

| Electrical & Hardware | |||

| Other End-user Industries (Toy, Apparel, Automotive, and Household, among Others) | |||

| Liquid Cartons | Milk | ||

| Juices | |||

| Energy Drinks | |||

| Other End-user Industries (Dairy Products such as Buttermilk, Cream, Smoothies, etc.) | |||

| By Region | East | ||

| West | |||

| North | |||

| South | |||

Need A Different Region or Segment?

Customize Now

India Paper Packaging Market Research FAQs

How big is the India Paper And Paperboard Packaging Market?

The India Paper And Paperboard Packaging Market size is worth USD 13.72 billion in 2025, growing at an 6.63% CAGR and is forecast to hit USD 18.92 billion by 2030.

What is the current India Paper And Paperboard Packaging Market size?

In 2025, the India Paper And Paperboard Packaging Market size is expected to reach USD 13.72 billion.

What years does this India Paper And Paperboard Packaging Market cover, and what was the market size in 2024?

In 2024, the India Paper And Paperboard Packaging Market size was estimated at USD 12.81 billion. The report covers the India Paper And Paperboard Packaging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the India Paper And Paperboard Packaging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

India Paper And Paperboard Packaging Market Research

Mordor Intelligence provides a comprehensive analysis of the paper and paperboard packaging market in India. We leverage our extensive expertise in the packaging industry to deliver this research. Our detailed report examines the paper industry in India, covering crucial aspects from paper manufacturing market dynamics to emerging trends in paper packaging industries. The analysis offers deep insights into the growth of paper industry in India, with a particular focus on the packaging industry market size in India and the evolving paper products market size.

This strategic report, available as an easy-to-download PDF, offers stakeholders valuable insights into paper industry growth rate projections and the market size of paper industry in India. We thoroughly analyze paper packaging companies in India and their competitive strategies. Additionally, we examine the corrugated box market size in India and the broader paper sector in India. The report benefits investors, manufacturers, and decision-makers by providing actionable intelligence on paper industry growth in India. This is supported by robust data on the paper market size in India and comprehensive industry forecasts.