Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

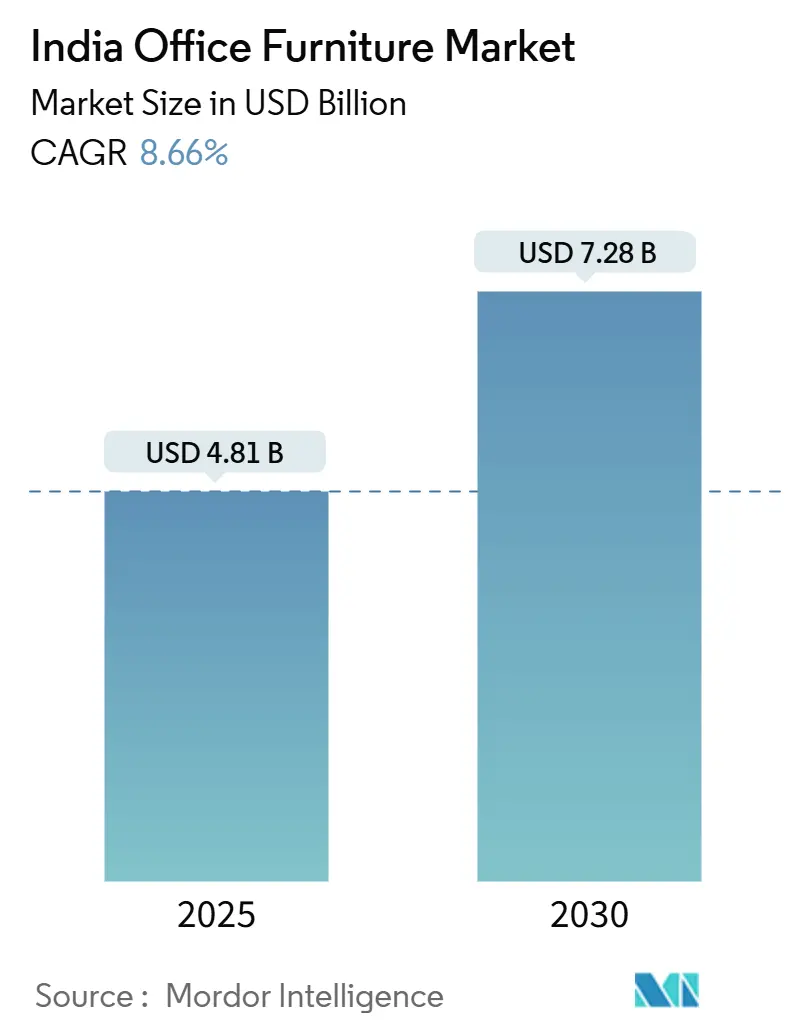

| Market Size (2025) | USD 4.81 Billion |

| Market Size (2030) | USD 7.28 Billion |

| Growth Rate (2025 - 2030) | 8.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Office Furniture Market Analysis by Mordor Intelligence

The India office furniture market size stood at USD 4.81 billion in 2025 and is forecast to reach USD 7.28 billion by 2030, expanding at an 8.66% CAGR. Continued momentum comes from hybrid working models, government manufacturing incentives, and rising ergonomic awareness that together reshape workplace procurement behaviour. Chair demand stays resilient because firms replace seating more often than other fixtures, while tables surge on the back of collaborative space fit-outs. Material preferences are shifting as polymer innovation challenges wood’s long-held dominance, offering lighter products that meet BIS quality norms at lower cost. Price-sensitive customers still drive high volumes in the economy tier, yet premium lines accelerate as multinationals elevate branding and employee-well-being needs. A moderate concentration top five brands command 52% creates headroom for regional challengers that can meet certification requirements and deliver nationwide project execution.

Key Report Takeaways

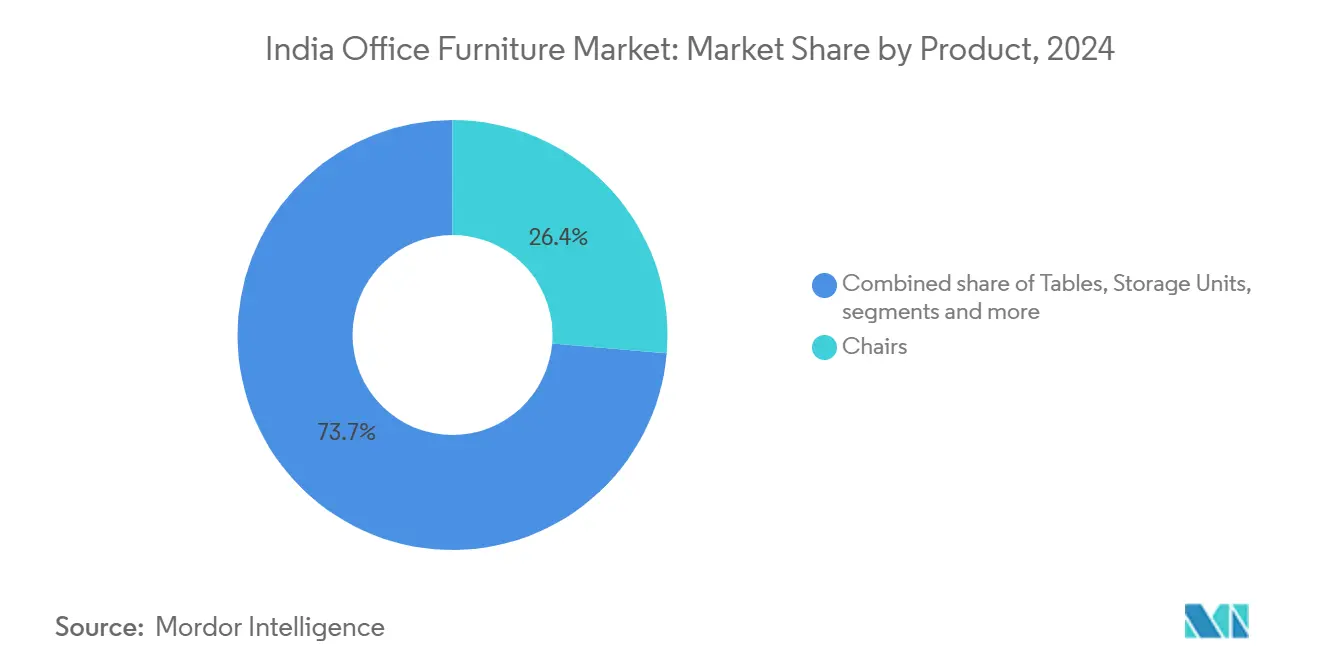

- By product, chairs led with 26.35% of the India office furniture market share in 2024; tables are projected to grow fastest at a 9.02% CAGR through 2030.

- By material, wood captured 42.91% of the India office furniture market share in 2024, while plastic and polymer segments are forecast to expand at an 8.98% CAGR to 2030.

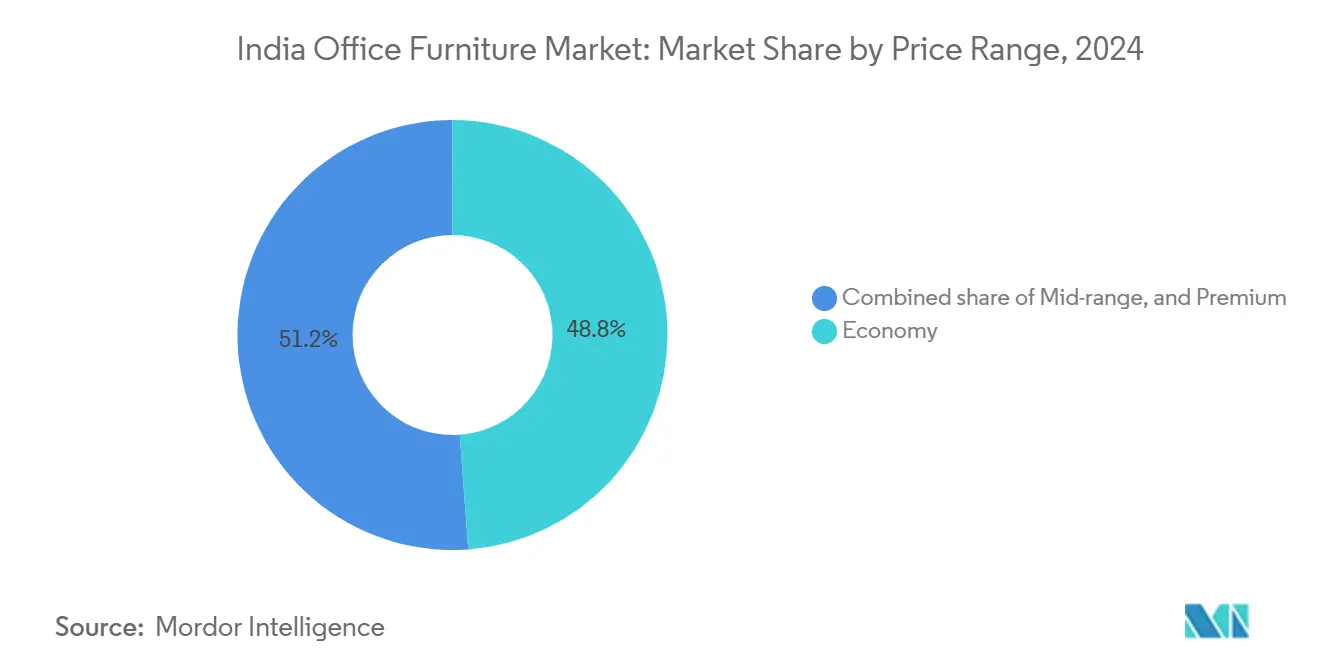

- By price range, the economy tier accounted for 48.84% of the India office furniture market share in 2024; premium products record the highest expected CAGR at 8.67% through 2030.

- By end-user, corporate offices contributed 39.83% of the India office furniture market share in 2024; government and public offices post the strongest 9.18% CAGR outlook.

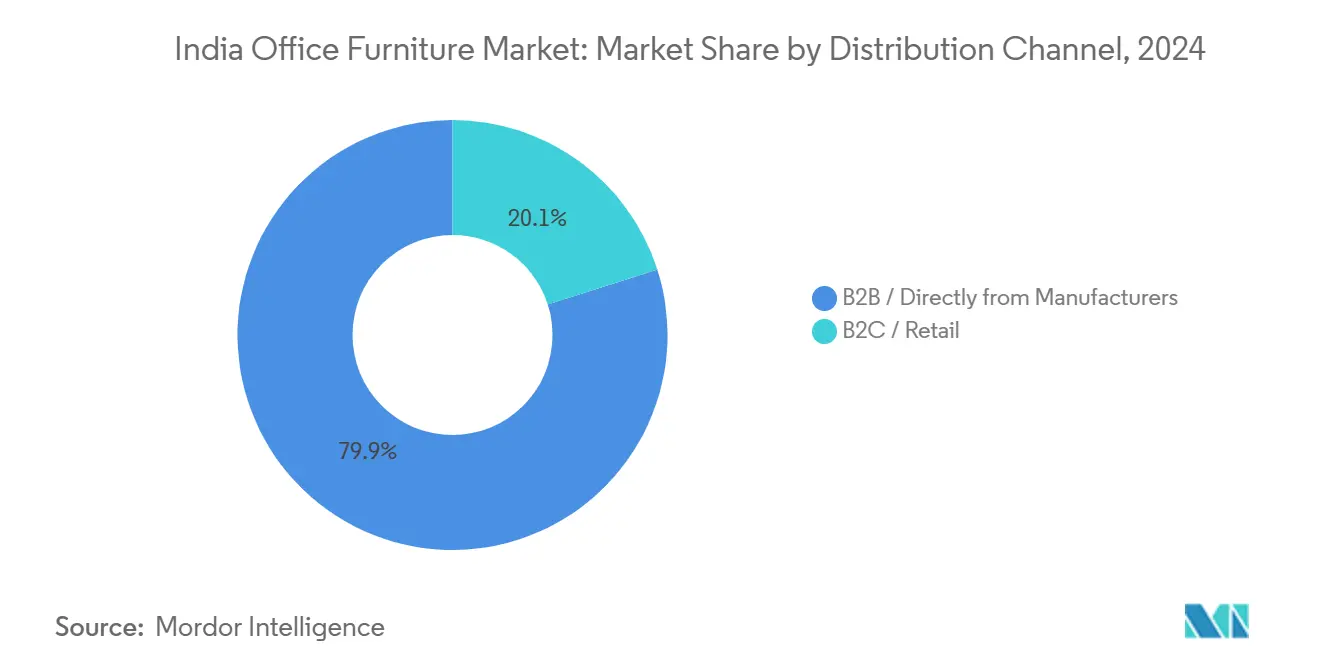

- By distribution channel, B2B direct sales held 79.93% of the India office furniture market share in 2024, underscoring the sector’s project-based selling model.

- By geography, West India generated 25.52% of 2024 revenues; North India is projected to deliver the highest 8.78% CAGR to 2030.

India Office Furniture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid working models driving demand for flexible furniture | +1.8% | National, with early adoption in metros | Medium term (2-4 years) |

| Expansion of corporate real estate footprint | +1.5% | West India, North India, South India | Long term (≥ 4 years) |

| Government "Make in India" incentives for furniture manufacturing | +1.2% | National, concentrated in manufacturing hubs | Long term (≥ 4 years) |

| Rising ergonomic and employee-well-being focus | +1.0% | National, led by IT/corporate sectors | Medium term (2-4 years) |

| Tier-II & III co-working boom | +0.9% | Tier-2/3 cities across all regions | Medium term (2-4 years) |

| Modular demountable partitions shorten fit-out cycles | +0.7% | National, concentrated in commercial hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hybrid Working Models Driving Demand for Flexible Furniture

Corporate occupancy now averages 60-70% on any given day, prompting companies to prioritize modular desks, height-adjustable workstations, and movable storage that can be reconfigured quickly when teams alternate between office and home. Demand for such adaptive solutions caused manufacturers to ship more than 100,000 home-office kits during the pandemic transition. Smart desks embedded with occupancy sensors mark the next wave, allowing facility managers to monitor space utilization in real time. As certification under BIS QCO 2025 tightens, vendors able to combine flexibility with compliance win larger multi-city rollout contracts. This preference for modularity feeds directly into the India office furniture market, reinforcing growth momentum across both premium and mid-range price bands.

Expansion of Corporate Real Estate Footprint

Rapid scaling of Global Capability Centres, which already employ 1.9 million people in 1,950 facilities, underpins sustained demand for quality furniture that meets global standards[1]Business Wire India, “India’s Largest Workplace Furniture Manufacturing Firm AFC Furniture Solutions Acquires the Brands Xbench, Vibrant and Livo,” businesswireindia.com. . Large occupiers increasingly engage single-vendor partners to furnish multiple sites, rewarding suppliers with nationwide installation and after-sales capacity. Premium finishes, collaborative tables, and acoustic booths dominate new fit-outs as technology and financial services firms elevate employee experience. Continuous growth in floor space across tier-1 cities and the rise of managed office operators in satellite towns keep the India office furniture market firmly on an upward trajectory.

Government “Make in India” Incentives for Furniture Manufacturing

Production-linked incentives encourage local sourcing, helping brands cut lead times and tailor products to project-specific requirements. Domestic plants equipped with German and Italian machinery now replicate global quality at competitive cost, reducing reliance on imports subject to long shipping cycles and currency risk. Manufacturers receive faster GST refunds and preferential procurement in public projects when they qualify as local content suppliers, directly boosting order books in the India office furniture market. Implementation hurdles remain land allotment delays in clusters hamper capacity additions but overall policy direction favors scaling indigenous capability[2]FDT Bureau, “Delay in Land Allotment for Furniture Cluster Jeopardises Investment Plans,” furnituredesignindia.com. .

Rising Ergonomic and Employee-Well-Being Focus

Ergonomic chairs certified to BIFMA or EN-1335 have moved from optional to mandatory in corporate RFPs. Height-adjustable desks, monitor arms, and footrests now appear on standard equipment lists, reflecting the link between posture support and productivity. Procurement teams weigh warranty terms and recyclability credentials alongside price, adopting lifecycle costing frameworks that reinforce demand for higher-grade materials. As wellness KPIs enter ESG reporting, furniture that supports biophilic design integrating planters and acoustic felt made from recycled PET gains traction. This premiumization trend elevates average selling prices within the India office furniture market, even while volumes grow in the value tier.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile wood, steel and polymer prices | -1.4% | National, acute in manufacturing regions | Short term (≤ 2 years) |

| Price pressure from unorganised manufacturers | -0.8% | National, concentrated in tier-2/3 cities | Medium term (2-4 years) |

| Lengthy municipal fire-safety certification | -0.6% | National, severe in metros | Medium term (2-4 years) |

| Sustainability audits limiting VOC-heavy finishes | -0.4% | National, led by corporate sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Wood, Steel and Polymer Prices

Input cost swings force suppliers to shorten quotation validity and build price-escalation clauses into contracts. Steel frames used in modular cubicles have seen double-digit quarterly adjustments, while imported veneer prices fluctuate with shipping rates and currency moves. Manufacturers hedge inventories but margin compression persists, particularly on long-cycle government orders. Some vendors redesign products to reduce metal content and incorporate engineered panels that lower exposure to commodity volatility. Although raw-material turbulence dents immediate profitability, sustained demand keeps the India office furniture market expanding.

Price Pressure from Unorganised Manufacturers

Smaller workshops command 60-70% of volumes in the economy tier by leveraging low overheads and flexible labor. They undercut organized players by 20-30%, challenging brands to justify premiums through service quality and certifications. Established companies counter by launching entry-price collections and offering three-year warranties even on value lines, a proposition many informal outfits cannot match. Government moves to enforce GST compliance and the forthcoming BIS QCO 2025 may gradually squeeze non-compliant producers, yet for now price competition remains intense across most regional hubs of the India office furniture market.

Segment Analysis

By Product: Chairs Retain Leadership While Tables Accelerate

Chairs generated a 26.35% slice of 2024 revenues as enterprises refreshed seating stock to meet ergonomic guidelines. Within the segment, high-back task chairs and mesh models see consistent replacement cycles of three to four years, stabilizing base demand. Tables, however, exhibit the fastest 9.02% CAGR outlook, buoyed by breakout zones and hot-desk layouts that multiply worksurface requirements. The India office furniture market size for tables is projected to expand from USD 1.05 billion in 2025 to USD 1.62 billion by 2030.

Growth also stems from wider adoption of conference pods and sit-stand stations that blend table and divider functions. Mobile pedestal units bundle with benching systems, raising ticket size per workstation. Meanwhile, storage units confront digitalization headwinds, although lockable modular cubes gain favor in flexible offices. Soft seating and acoustic booths carve niches as employers add focus pods to open plans. Suppliers that offer coordinated chair-table packages with rapid lead times capture larger project awards, reinforcing their presence in the India office furniture market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Wood Dominance Faces Polymer Challenge

Wood preserved a 42.91% share in 2024 on the strength of executive cabins and boardroom suites, yet its position erodes as polymers replicate timber aesthetics at lighter weight. The India office furniture market share for polymers is slated to reach 28% by 2030 after rising at an 8.98% CAGR.

Polypropylene and glass-fiber blends allow complex geometries while meeting the 60 kg load standard for desks under BIS QCO 2025. Metal remains critical for healthcare and industrial settings that demand easy disinfection, though inflationary steel prices restrain its advance. Manufacturers investing in automated powder-coating lines and recycled PET felt panels gain an edge with sustainability-minded buyers. Wood suppliers, for their part, pivot to FSC-certified tropical hardwood substitutes and water-based lacquers to align with low-VOC mandates.

By Price Range: Economy Drives Volume, Premium Accelerates

Economy-tier products delivered 48.84% of receipts in 2024 thanks to SME roll-outs and public-sector bulk tenders. Vendors differentiate through knock-down packaging that minimizes freight and enables self-assembly. Even so, the premium bracket is forecast to clock an 8.67% CAGR, lifting the India office furniture market size for premium lines to USD 1.46 billion by 2030.

Premium buyers seek veneer-clad desks with integrated cable management, proprietary ergonomic mechanisms, and five-year warranties. Bundled design consultancy and virtual reality walkthroughs further justify elevated prices. Mid-range collections grow steadily by balancing BIFMA compliance with competitive cost, often leveraging laminated engineered boards to cap material spend.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: Corporate Offices Remain Core While Government Procurement Accelerates

Corporate occupiers commanded 39.83% of 2024 spending as multinationals standardized fit-outs across captive centres and third-party campuses. The India office furniture market share for government and public offices is smaller today yet set to rise fastest at 9.18% CAGR through 2030.

Central agencies fast-track modernization to comply with safety norms and disability access rules, fuelling orders for height-adjustable desks and fire-retardant partitions. Educational institutions, hospitality back-offices, and healthcare admin wings each follow distinct specification checklists antibacterial laminates for hospitals, compact footprint desks for colleges but collectively bolster demand variety.

By Distribution Channel: B2B Direct Sales Dominate Project-Based Buying

Direct engagements accounted for 79.93% of 2024 revenue as clients valued single-window delivery from design to after-sales maintenance. Long-term annual rate contracts lock in pricing for national rollouts, securing predictable volume for established suppliers. Retail formats and e-commerce cater to small firms and freelancers, yet complex installation requirements keep their penetration modest in large projects.

Online marketplaces still influence brand discovery; configurable 3D planners allow customers to visualize layouts before sending purchase requisitions. Showrooms supplement the consultant network by displaying product ergonomics first-hand, especially in tier-2 cities where digital adoption climbs more gradually. Together these channels widen the catchment for the India office furniture market while preserving the primacy of direct project selling.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

West India generated 25.52% of 2024 sales, anchored by Maharashtra’s financial sector and Gujarat’s manufacturing base. Mumbai drives premium demand with global banks outfitting high-rise offices, whereas Pune’s IT corridor selects modular benching and acoustic pods to suit agile teams. Supply clusters around Pune and Ahmedabad shorten delivery cycles, a key advantage when projects specify tight handover timelines.

North India delivers the highest 8.78% CAGR outlook as Delhi NCR updates government complexes and corporates shift headquarters to Gurugram’s Grade-A towers. The India office furniture market size for North India is expected to climb from USD 1.13 billion in 2025 to USD 1.72 billion by 2030. Chandigarh, Lucknow and Jaipur add incremental demand via co-working hubs that target startups migrating from metros.

South India remains the single largest consumption zone by floor-space addition, propelled by technology clusters in Bengaluru, Hyderabad and Chennai. Diversified demand spans premium task chairs for software developers, corrosion-resistant steel desks for coastal R&D centres, and reception lounges for global capability campuses. East India lags on absolute value but benefits from public-sector refurbishments in Kolkata and resource-industry offices in Odisha. Suppliers forging dealer partnerships in these emerging pockets tap new growth lanes within the India office furniture market.

Competitive Landscape

The market’s moderate concentration creates opportunities for mid-tier players to grow by focusing on niche segments and regional strengths. Godrej Interio holds the leading position, driven by its comprehensive product range and a network of 1,000 omnichannel stores that combine retail presence with corporate project showcases. Featherlite follows closely, known for its expertise in mesh-chair design and a strong dealer network across southern India. Nilkamal stands out for its polymer molding capabilities, which support both its office seating and value-oriented storage product lines.

Strategic moves center on portfolio expansion and vertical integration. AFC Furniture Solutions’ 2024 purchase of Wipro’s Xbench, Vibrant and Livo brands expanded its addressable range from budget cubicles to premium desking, enabling cross-selling to existing enterprise accounts[3]Business Wire India, “India’s Largest Workplace Furniture Manufacturing Firm AFC Furniture Solutions Acquires the Brands Xbench, Vibrant and Livo,” businesswireindia.com. . Durian and Spacewood invest in robotic panel-processing to lift output consistency and cut turnaround on custom orders. Many firms embed IoT sensors in desks and lockers, allowing corporate clients to track occupancy and asset utilization through cloud dashboards.

Compliance with BIS QCO 2025 separates organized players from informal workshops by requiring in-house testing labs or certified third-party audits. Brands advertise E1-grade panels and GREENGUARD coatings to pass multinational sustainability audits. Distribution alliances with architects and interior design studios remain critical to securing early specification, while direct-to-consumer e-stores extend reach to freelancers and hybrid workers. These dynamics reinforce steady consolidation in the India office furniture market without stifling innovation.

India Office Furniture Industry Leaders

Feather Lite

Durian

Nilkamal

Godrej Interio

HNI India

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2024: HTL Group invested Rs 170 crore in production facilities and announced plans to open 10 exclusive stores in metro cities, targeting premium furniture segments.

- October 2024: Zuari Industries acquired an additional 50.85% stake in Forte Furniture Products India, strengthening its position in the modular furniture market.

- September 2024: HomeLane acquired DesignCafe in a landmark deal valued at Rs 3,000 crore, with the combined entity raising Rs 225 crore in funding to accelerate growth in the modular furniture and interior design market.

- August 2024: Godrej Interio achieved the milestone of 1,000 furniture stores across India, representing a significant expansion of retail presence and market accessibility for office and home furniture solutions.

India Office Furniture Market Report Scope

This report aims to provide a detailed analysis of the India office furniture market. It focuses on the market dynamics, emerging trends in the segments and regional markets, and insights into the various product and application types. Also, it analyzes the key players and the competitive landscape.

By Product

| Chairs | Employee Chairs |

| Meeting Chairs | |

| Guest Chairs | |

| Tables | Conference Tables |

| Desks | |

| Other Tables | |

| Storage Units | Filing Cabinets |

| Bookcases & Shelving | |

| Sofas/Soft Seating | |

| Booths and Office Dividers | |

| Other Office Furniture (Stools, Reception Area Furniture, Accessories, Others) |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By Price Range

| Economy |

| Mid-range |

| Premium |

By End-user

| Corporate Offices |

| Healthcare Offices |

| Educational Institutions |

| Government & Public Offices |

| Hospitality & Retail Back-office |

| Others |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Directly from Manufacturers |

By Geography

| North India |

| West India |

| South India |

| East India |

| By Product | Chairs | Employee Chairs |

| Meeting Chairs | ||

| Guest Chairs | ||

| Tables | Conference Tables | |

| Desks | ||

| Other Tables | ||

| Storage Units | Filing Cabinets | |

| Bookcases & Shelving | ||

| Sofas/Soft Seating | ||

| Booths and Office Dividers | ||

| Other Office Furniture (Stools, Reception Area Furniture, Accessories, Others) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Price Range | Economy | |

| Mid-range | ||

| Premium | ||

| By End-user | Corporate Offices | |

| Healthcare Offices | ||

| Educational Institutions | ||

| Government & Public Offices | ||

| Hospitality & Retail Back-office | ||

| Others | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Directly from Manufacturers | ||

| By Geography | North India | |

| West India | ||

| South India | ||

| East India | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How fast is demand growing for premium office desks in India?

Premium categories are projected to advance at an 8.67% CAGR to 2030, outpacing the overall market as multinationals upgrade workspace aesthetics.

Which region is projected to expand quickest in corporate furniture purchases?

North India shows the fastest 8.78% CAGR through 2030, spurred by Delhi NCR office expansions and government modernization.

Why do direct B2B channels dominate sales?

Large projects require layout design, on-site installation and after-sales service, making manufacturer-to-client engagements the preferred model with 79.93% share.

What materials are gaining share against traditional wood?

Polymers such as polypropylene-glass blends are growing at an 8.98% CAGR due to cost, weight and design flexibility advantages under BIS load norms.

How is hybrid work shaping procurement choices?

Organizations increasingly select modular, height-adjustable and sensor-enabled furniture that adapts to fluctuating office occupancy levels.