India Medical Tourism Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

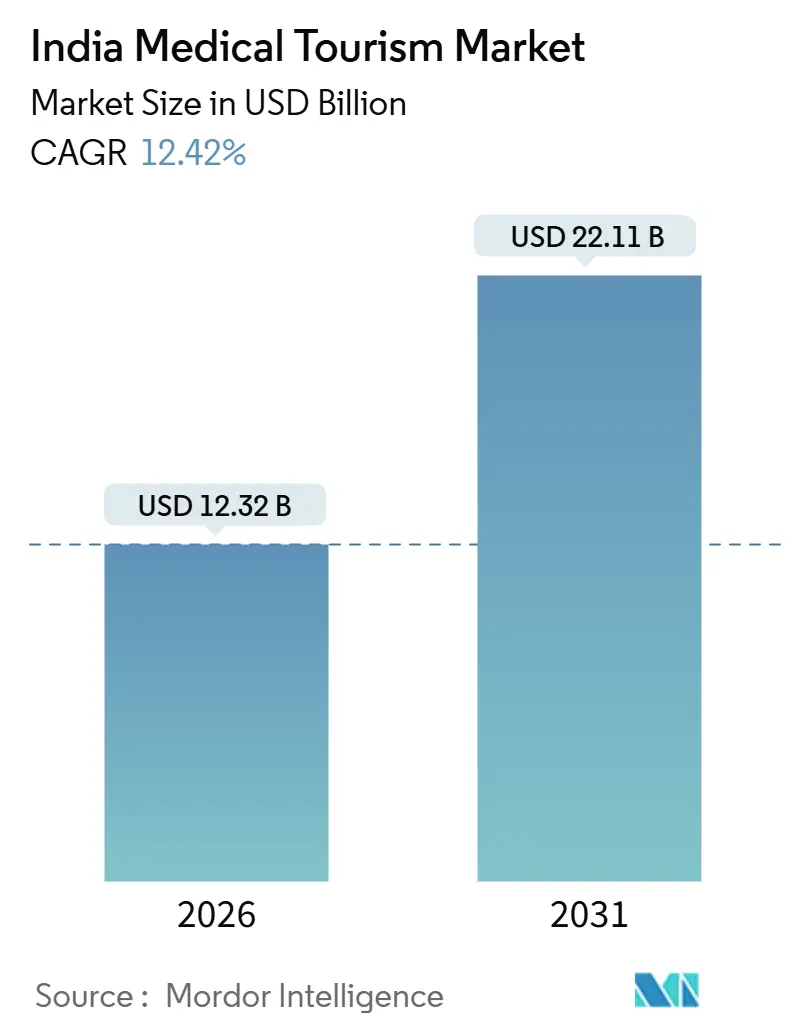

| Market Size (2026) | USD 12.32 Billion |

| Market Size (2031) | USD 22.11 Billion |

| Growth Rate (2026 - 2031) | 12.42% CAGR |

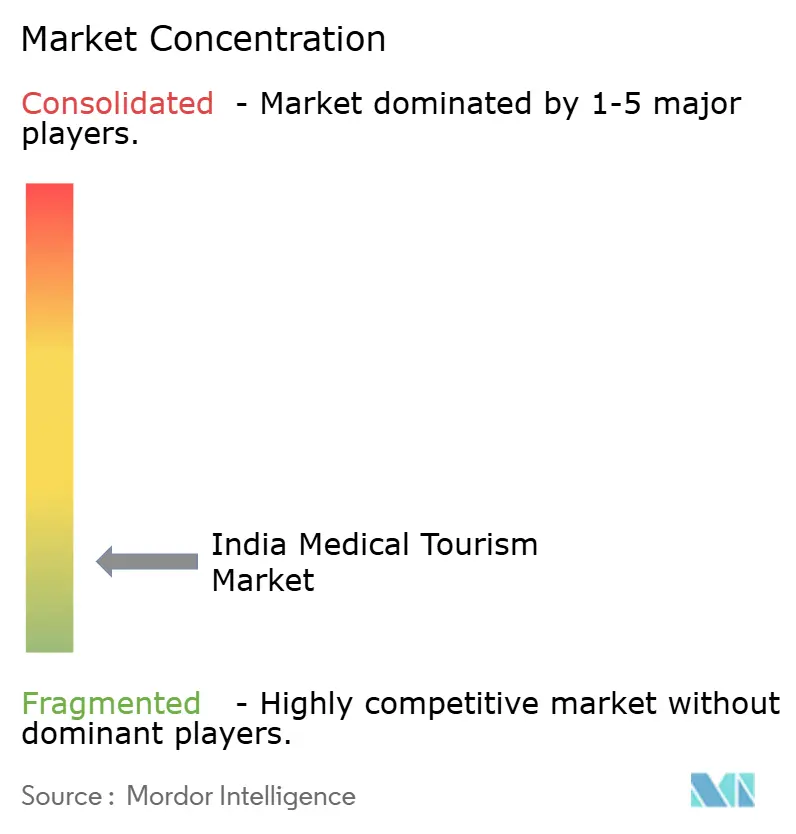

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Medical Tourism Market Analysis by Mordor Intelligence

The India Medical Tourism Market size is estimated at USD 12.32 billion in 2026, and is expected to reach USD 22.11 billion by 2031, at a CAGR of 12.42% during the forecast period (2026-2031).

The growth rests on a sizeable cost gap versus OECD providers, wider access to JCI- and NABH-accredited hospitals, and faster e-Medical Visa clearance that now covers 167 countries. Foreign tourist arrivals for treatment jumped from 182,945 in 2020 to 6,44,387 in 2024, indicating a decisive post-pandemic rebound.[1]Ministry of Tourism, “Heal in India Campaign and Medical Value Travel Portal,” tourism.gov.in Oncology, transplant, and robotic surgery volumes are accelerating as public and private centers invest in proton therapy, CAR-T platforms, and da Vinci systems. Overseas insurance tie-ups with Maldives, Oman, and Mauritius further de-risk out-of-pocket spending. At the same time, the India medical tourism market capitalizes on digital tele-follow-up models that shorten stays and build patient confidence.

Key Report Takeaways

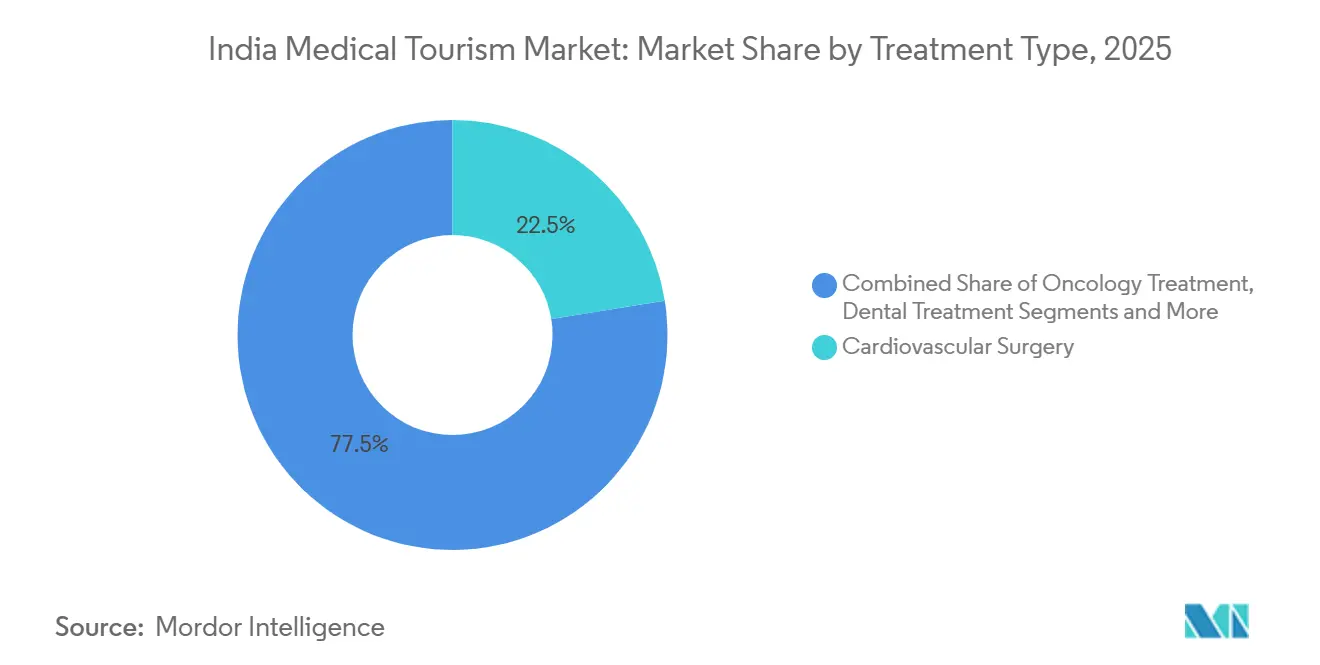

- By treatment type, cardiovascular surgery held 22.46% revenue share of the India medical tourism market in 2025 and oncology is advancing at a 16.73% CAGR to 2031.

- By service provider, private multi-specialty hospitals led with 66.22% of the India medical tourism market share in 2025, while facilitator platforms are growing at a 15.18% CAGR through 2031.

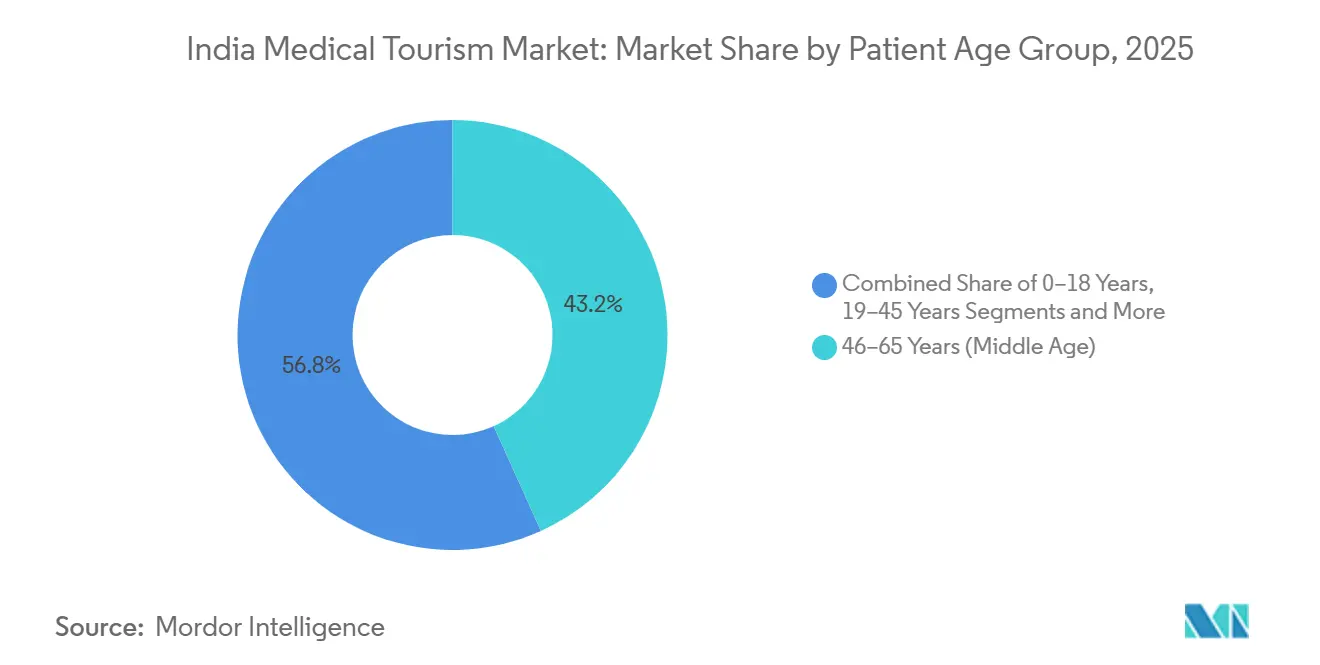

- By patient age, the 46-65 cohort accounted for 43.25% of the India medical tourism market size in 2025 and the 66-plus segment is expanding at a 13.32% CAGR to 2031.

- By patient gender, male cases dominated at 55.73% volume in 2025, whereas female-focused treatments are rising at a 13.58% CAGR through 2031.

- By Indian region, South India generated 33.26% revenue in 2025 and East-Northeast is on track for a 14.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Medical Tourism Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost advantage of complex surgeries | +2.8% | Global, pronounced in South Asia, Middle East, Africa | Long term (≥ 4 years) |

| Expanding network of JCI/NABH hospitals | +2.1% | National, stronger in South and West India | Medium term (2-4 years) |

| ‘Heal in India’ and streamlined e-Medical Visa | +1.9% | Global, early gains from Bangladesh, Iraq, Maldives | Short term (≤ 2 years) |

| Robotics and transplant technology adoption | +1.7% | National, led by metro clusters | Medium term (2-4 years) |

| Overseas insurance tie-ups | +1.4% | Global, Maldives, Mauritius, Oman, Qatar | Medium term (2-4 years) |

| Tele-follow-up models | +1.2% | Global, useful across all source markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost Advantage Of Complex Surgeries Vs OECD Nations

India medical tourism market beneficiaries pay 60-80% less than OECD rates, with bypass grafts starting at USD 5,000 against USD 100,000 in the United States. Lower labor costs, high generic-drug penetration, and dense patient throughput sustain the edge. Growing African and Central Asian middle-income populations, now backed by international insurers, are choosing accredited Indian centers over pricier Southeast Asian hubs. This enduring pricing gap secures long-term volume inflows and positions the India medical tourism market for sustained double-digit expansion.

Expanding Network Of JCI/NABH-Accredited Hospitals

India hosts 57-61 JCI institutions and more than 46,50 NABH hospitals as of May 2025.[2]Ministry of Health and Family Welfare, “NABH Accreditation Statistics 2024,” mohfw.gov.in While 100 facilities received NABH digital health certification by September 2024Accreditation boosts insurer confidence, validates telemedicine systems, and attracts facilitator referrals. Corporate chains spread audit costs across multi-site footprints, and tier-2 providers in Coimbatore, Visakhapatnam, and Jaipur seek the seal to stand apart from unaccredited rivals. The pipeline suggests over 2,000 NABH hospitals by 2028, deepening the India medical tourism market capacity.

‘Heal In India’ Campaign & Streamlined E-Medical Visa

The medical value travel portal slashed visa approval to 48-72 hours and opened access to 167 countries. Early uptake includes 123 regular Ayush visas and 221 e-Ayush visas between July 2023 and December 2024.[3]Ministry of External Affairs, “Ayush Visa Statistics July 2023 – December 2024,” mea.gov.in Multilingual listings in Arabic, French, and Swahili narrow information gaps, while multiple entries over 60 days support staged care. As real-time bed availability goes live in 2026, the portal will convert into a direct marketplace, likely trimming facilitator commissions and lowering overall India medical tourism market prices.

Advanced Robotics & Transplant Technology Adoption

More than 170 da Vinci systems serve Indian hospitals, with 850-plus trained surgeons by 2025. Public sites such as NIMS Hyderabad completed 300 robotic surgeries within 12 months of launch. Apollo’s NexCAR19 CAR-T therapy and Tata Memorial’s proton unit widen oncology options at sub-USD 30,000, compared with USD 150,000-250,000 in the United States. Robotic kidney transplants at Fortis Noida cost USD 10,800-12,000 and cut hospital stay, elevating throughput. Domestic robot makers may drop system prices 20-25% by 2028, boosting India medical tourism market penetration into tier-2 cities.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hygiene and safety perception issues | -1.3% | Global, severe in Europe and North America | Short term (≤ 2 years) |

| Airport and surface-transport bottlenecks | -0.9% | National, acute in Delhi, Mumbai, Bangalore | Medium term (2-4 years) |

| Rupee volatility eroding cost edge | -0.7% | Global, affects all source markets | Short term (≤ 2 years) |

| Bed-capacity squeeze in high-demand specialties | -0.6% | National, concentrated in metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hygiene And Safety Perception Issues Post-COVID-19

Media reports of outbreaks in unaccredited facilities fueled Western skepticism. Accredited centers post infection rates below 2%, yet some tier-2 units record 8-10%. Hospitals now publish live dashboards, pursue ISO 9001 certification, and welcome third-party audits to rebuild trust. The restraint weighs on near-term Europe- and U.S.-origin flows but is expected to ease as data transparency improves within the India medical tourism market.

Airport And Surface-Transport Bottlenecks

International passenger traffic reached 66.8 million in FY 2023-24, straining Delhi, Mumbai, and Bangalore, where immigration queues exceed 90 minutes. Surface trips to city hospitals add up to 90 minutes at peak time, and limited flights to Guwahati or Coimbatore restrict flexibility. New terminals and Digi Yatra have added capacity, yet lag growth. Better connectivity remains crucial for seamless India medical tourism market access.

Segment Analysis

By Treatment Type: Cardiac Base, Oncology Upswing

Cardiovascular surgery contributed 22.46% revenue to the India medical tourism market in 2025, anchored by USD 5,000 bypass grafts that beat OECD prices by 70-80%. Oncology outpaces others with a 16.73% CAGR through 2031, led by proton therapy at Tata Memorial and Apollo’s CAR-T cell platform. Orthopedic and spine work attracts aging Gulf patients, while neurosurgery draws tumors and epilepsy cases from Africa. Robotic kidney transplants, fertility services, bariatric procedures, and cosmetic surgery widen the clinical mix, balancing cyclical dips in any one specialty.

India medical tourism market size for oncology treatments is set to climb sharply as proton therapy slots rise and CAR-T becomes mainstream. Cardiac centers will keep core volume but face price compression from subsidy programs at government sites. Elective aesthetic care serves younger, social-media-savvy travelers and raises average margins. Segment diversity maintains overall resilience.

Note: Segment shares of all individual segments available upon report purchase

By Service Provider: Corporate Chains And Digital Facilitators

Private multi-specialty chains captured 66.22% of India medical tourism market revenue in 2025, supported by 200-plus tertiary sites, multilingual liaisons, and insurer links. Facilitator platforms are growing at 15.18% CAGR as Vaidam and peers bundle visas, cost quotes, and tele-follow-up into user-friendly packages. Public hospitals such as AIIMS Guwahati and NIMS Hyderabad offer subsidized robotics and transplant work, undercutting private rates by up to 50%.

Corporate groups rely on facilitators for low-cost distribution into Africa and Central Asia, creating symbiosis rather than rivalry. Single-specialty clinics target ophthalmology or fertility niches with shorter wait times and deeper expertise. The India medical tourism market size for facilitator services is likely to expand as cross-border patients with limited India familiarity value full-service logistics.

By Patient Age Group: Middle-Age Core, Geriatric Wave

The 46-65 segment represented 43.25% of India medical tourism market size in 2025 owing to cardiac and orthopedic demand. The 66-plus cohort will rise at a 13.32% CAGR to 2031 as chronic multi-morbidity spreads. Hospitals are building geriatric wards with fall-safe rooms and elder-care nurses. Young adults drive fertility, bariatric, and cosmetic cases and choose providers through social media. Pediatric flows revolve around congenital heart and oncology care, where parents seek global benchmarks.

Geriatric growth boosts average revenue per case but needs specialized rehab and palliative facilities. Providers that invest early will dominate an age-skewed future India medical tourism market.

Note: Segment shares of all individual segments available upon report purchase

By Patient Gender: Female Treatments Ascend

Male patients accounted for 55.73% volume in 2025, topping cardiovascular and orthopedic procedures. Female-centric care—IVF, cosmetic, bariatric, gynecologic oncology—grows at 13.58% CAGR through 2031. Hospitals respond with women’s wellness centers, female surgeons, and private recovery suites. Gender-affirmation inquiries, still small, signal expanding inclusivity.

Targeted marketing distinguishes female decision drivers of testimonials and peer advice from male focus on clinical metrics, helping providers fine-tune outreach in the India medical tourism market.

Geography Analysis

South India’s entrenched clinical ecosystem keeps international infection control and outcomes on par with OECD benchmarks. Tamil Nadu alone welcomes about 1.5 million treatment seekers yearly and staffs 48 government medical colleges, ensuring low labor costs and high surgeon availability. Kerala layers Ayurveda and yoga programs to attract wellness travelers, aided by simplified e-visa rules. Multilingual coordinators fluent in Arabic, French, and Swahili smooth patient journeys.

East-Northeast advances on geographic closeness to Bangladesh, which supplied 54% of arrivals in 2023. AIIMS Guwahati intends to double beds to 750, while private projects add 1,000-plus beds. Although flight frequencies remain low, UDAN has opened 619 new routes to underserved airports, gradually closing the access gap.

West, North, and Central India make up the remainder. Maharashtra’s new accreditation scheme aims to curb quality variations. Delhi-NCR’s heavy traffic lengthens patient transfers despite brand recognition. Central India lacks accredited capacity but may rally as corporate chains evaluate Nagpur expansions. These dynamics reveal a diversifying India medical tourism market, with competition based on outcomes, cost, and logistics rather than legacy reputation alone.

Competitive Landscape

Apollo, Fortis, Manipal, Narayana, and Max hold major share of organized India medical tourism market revenue. Apollo grew international revenue 18% in FY 2023-24 after scaling proton therapy and CAR-T. Max recorded 27% growth, backed by new lounges and insurer ties. Manipal and Fortis emphasize cashless treatment networks and robotic transplant milestones. Chains are vertically integrating diagnostics and pharmacies to keep ancillary revenue in-house.

Facilitator platforms such as Vaidam use AI chatbots and virtual tours to cut traditional broker commissions to 8-12%, improving price transparency. Public centers like AIIMS Guwahati underprice private peers but lack marketing budgets. Market entry by insurers via provider joint ventures could intensify price competition and force greater outcome disclosure, reshaping the India medical tourism market.

India Medical Tourism Industry Leaders

Apollo Hospitals

Fortis Healthcare

Max Healthcare

Narayana Health

Manipal Hospitals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: NewEra Hospitals opened a dental care department in Navi Mumbai, adding modern oral-maxillofacial services.

- September 2025: AIIMS Delhi installed a da Vinci system to train surgeons nationwide, accelerating robotic adoption in smaller cities.

- June 2025: Smile in Hour Spalon Dental Clinic franchised in New Delhi, expanding access to same-day cosmetic dental work

- May 2025: SPARSH Group opened a 300-bed quaternary facility in Bengaluru, reinforcing the city’s transplant and orthopedic stature.

India Medical Tourism Market Report Scope

Medical tourism is traveling to another country to obtain medical treatment or procedures. It may be done for various reasons, such as seeking lower costs for medical care, accessing treatments or procedures that may not be available in one's home country, or avoiding long waiting lists for certain medical procedures.

India's Medical Tourism Market is segmented by treatment type, service provider, patient age group, patient gender, and Indian region. By Treatment Type, market is segmented into Dental, Cosmetic & Aesthetic, Cardiovascular, Orthopedic & Spine, Neurology & Neurosurgery, Oncology, Transplant, Fertility, Bariatric, and More. By Service Provider, Market is segmented into Public, Private Multi-Specialty, Private Single-Specialty, Facilitators. By Patient Age, market is segmented into 0–18 Years (Pediatrics), 19–45 Years (Young Adults), 46–65 Years (Middle Age) and 66+ Years (Geriatrics). By Patient Gender, market is segmented into Male, Female and Others. By Indian Region, market is segmented into North India, West India, South India, East & Northeast India, and Central India. The report offers market size and forecasts in value (USD) for the above segments.

| Dental Treatment |

| Cosmetic & Aesthetic Procedures |

| Cardiovascular Surgery |

| Orthopedic & Spine Surgery |

| Neurology & Neurosurgery |

| Oncology Treatment |

| Organ & Tissue Transplant |

| Fertility & Reproductive Treatment |

| Bariatric & Metabolic Surgery |

| Ophthalmology Procedures |

| Others |

| Public Hospitals |

| Private – Multi-Specialty Corporate Hospitals |

| Private – Single-Specialty Hospitals & Clinics |

| Medical Tourism Facilitators |

| 0–18 Years (Pediatrics) |

| 19–45 Years (Young Adults) |

| 46–65 Years (Middle Age) |

| 66+ Years (Geriatrics) |

| Male |

| Female |

| Other / Non-Binary |

| North India |

| West India |

| South India |

| East & Northeast India |

| Central India |

| By Treatment Type | Dental Treatment |

| Cosmetic & Aesthetic Procedures | |

| Cardiovascular Surgery | |

| Orthopedic & Spine Surgery | |

| Neurology & Neurosurgery | |

| Oncology Treatment | |

| Organ & Tissue Transplant | |

| Fertility & Reproductive Treatment | |

| Bariatric & Metabolic Surgery | |

| Ophthalmology Procedures | |

| Others | |

| By Service Provider | Public Hospitals |

| Private – Multi-Specialty Corporate Hospitals | |

| Private – Single-Specialty Hospitals & Clinics | |

| Medical Tourism Facilitators | |

| By Patient Age Group | 0–18 Years (Pediatrics) |

| 19–45 Years (Young Adults) | |

| 46–65 Years (Middle Age) | |

| 66+ Years (Geriatrics) | |

| By Patient Gender | Male |

| Female | |

| Other / Non-Binary | |

| By Indian Region | North India |

| West India | |

| South India | |

| East & Northeast India | |

| Central India |

Key Questions Answered in the Report

How large is the India medical tourism market in 2026?

It is valued at USD 12.32 billion and is projected to grow at a 12.42% CAGR to USD 22.11 billion by 2031.

Which specialty is growing fastest for international patients in India?

Oncology services are expanding at a 16.73% CAGR, driven by proton therapy and CAR-T cell treatments.

What share do private multi-specialty hospitals hold?

They commanded 66.22% of India medical tourism market revenue in 2025.

Why is South India the leading region?

The region hosts more than 50 accredited hospitals, streamlined visa support, and specialized cardiac and transplant centers.

How are hospitals addressing post-treatment follow-up for overseas patients?

Providers use regulated telemedicine platforms, WhatsApp, and video consultations funded by state schemes to manage recovery without repeat travel.

What factors could restrain future growth?

Hygiene perception gaps, transport bottlenecks, currency volatility, and limited oncology bed capacity can temper near-term expansion.