Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

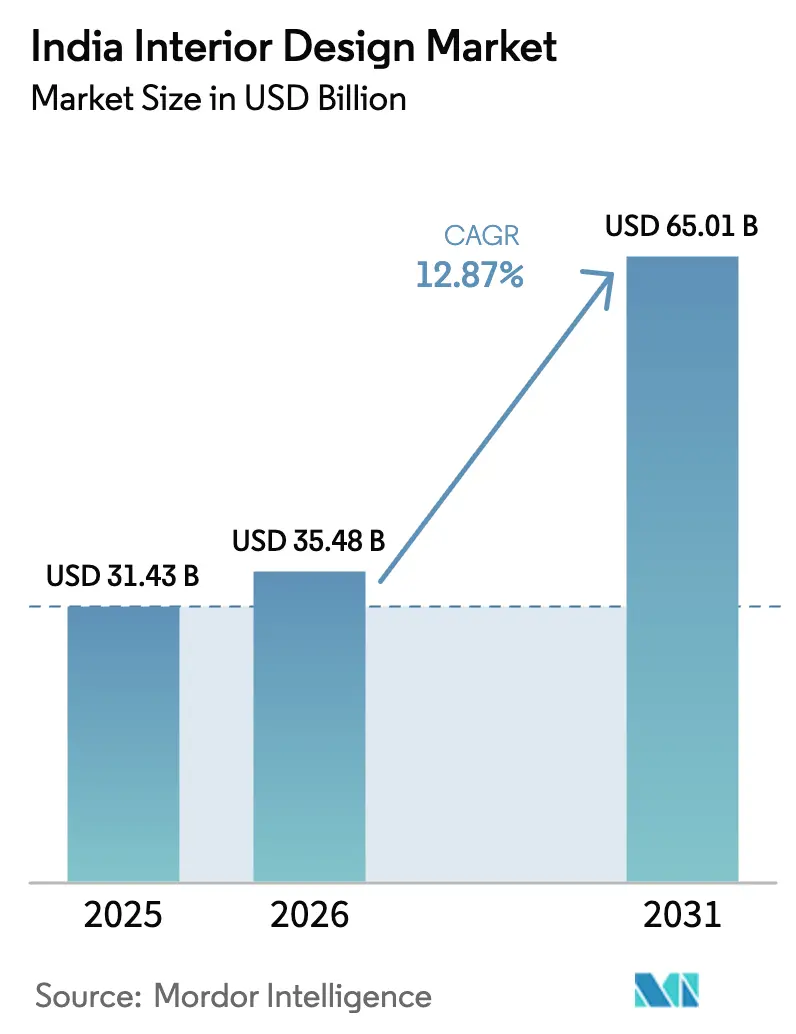

| Base Year Market Size (2025) | USD 31.43 Billion |

| Market Size (2026) | USD 35.48 Billion |

| Market Size (2031) | USD 65.01 Billion |

| Growth Rate (2026 - 2031) | 12.87% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Interior Design Market Analysis by Mordor Intelligence

The India Interior Design Market size is projected to be USD 31.43 billion in 2025, USD 35.48 billion in 2026, and reach USD 65.01 billion by 2031, growing at a CAGR of 12.87% from 2026 to 2031.

Commercial projects accounted for a clear majority in 2025, while residential work is accelerating on the back of rising disposable incomes and ongoing housing programs that convert latent demand into executed interiors. New construction remains larger than renovation, although retrofit-led specifications are spreading through Grade-A office stock, where refresh cycles align with ESG and wellness standards. Mid-range price points continue to command the largest share, yet economy-tier packages are growing faster as turnkey e-commerce models reach customers in tier-2 and tier-3 cities. North India leads by regional share, with the East and North-East expanding the fastest as connectivity, retail formats, and platform-led execution combine to formalize spending that previously favored unorganized contractors.

Key Report Takeaways

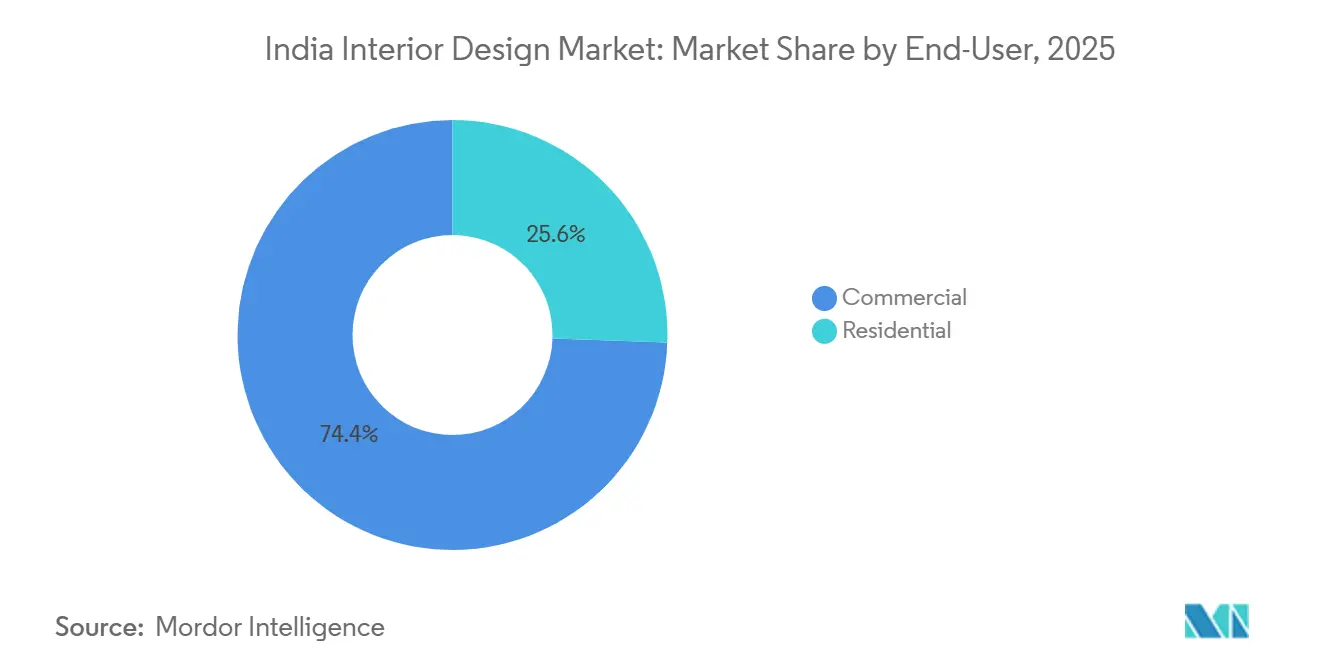

- By end-user, commercial held 74.44% of revenue in 2025, while residential is expected to advance at a 16.47% CAGR through 2031.

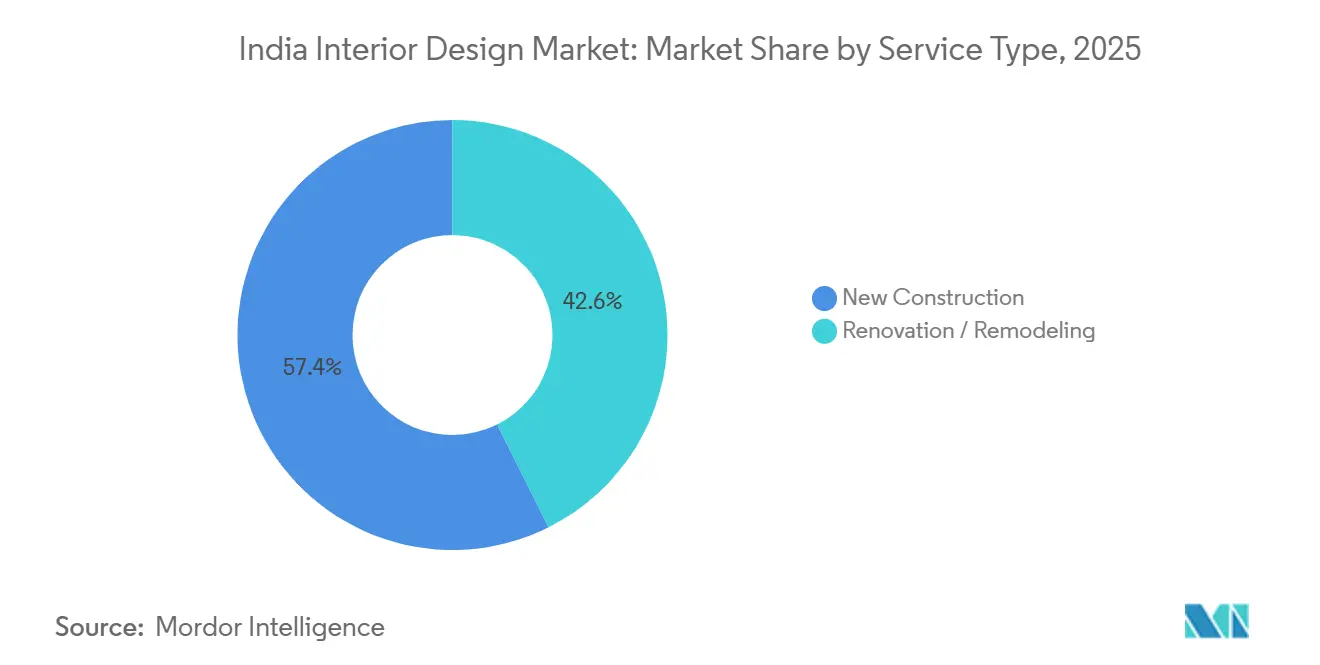

- By service type, new construction accounted for 57.39% of revenue in 2025, while renovation and remodeling are forecast to grow at a 13.35% CAGR through 2031.

- By price tier, mid-range captured 52.35% in 2025, while the economy segment is set to grow at a 14.76% CAGR through 2031.

- By geography, North India commanded 39.87% in 2025, while East and North-East India are projected to expand at an 11.87% CAGR during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Interior Design Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization & rising disposable incomes | +3.2% | National, strongest in tier-1 cities | Medium term (2-4 years) |

| Government housing & infrastructure programmes (PMAY, Smart Cities) | +2.8% | National, with spillover to rural areas | Long term (≥ 4 years) |

| Commercial real-estate boom in office, retail & hospitality | +3.5% | Metros and tier-1 cities (Bengaluru, Mumbai, Delhi-NCR) | Short term (≤ 2 years) |

| Digital design visualisation (VR/AI) is accelerating customer acquisition | +1.9% | National, early gains in tier-1 & 2 cities | Short term (≤ 2 years) |

| Specialised interiors for senior & assisted-living facilities | +0.8% | South India (60% market share), urban metros | Medium term (2-4 years) |

| Tier-2/3 e-commerce turnkey packages for middle-income homes | +1.9% | Tier-2/3 cities (Jaipur, Lucknow, Indore, Chandigarh) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization & Rising Disposable Incomes

India’s consumption tailwinds are translating into more design-led spending in both premium and mass segments, with metros absorbing larger ticket sizes and non-metros adopting platform-based services for the first time. Urban households are prioritizing space optimization and modular interventions as dual-income families expand, which lifts the adoption of integrated design-and-execution packages. Organized platforms are using store and studio expansion to capture these cohorts, with Livspace and HomeLane scaling city footprints alongside online visualization that reduces friction[1]Editorial Team, “Livspace Revenue Grows 23% to USD 164.8m in FY25,” Tech in Asia, techinasia.com. As more households cross key income thresholds, preference shifts from unbranded carpentry toward warranties, service-level agreements, and branded modular systems. These shifts are strengthening conversion funnels and pipeline predictability for organized channels in the India interior design market.

Government Housing & Infrastructure Programmes

PMAY-G and PMAY-U 2.0 are sustaining basic interior product demand at scale by standardizing kitchens, washrooms, and core fixtures across sanctioned units and completed homes[2]Ministry of Rural Development, “Department of Rural Development: Year Ender 2025,” Press Information Bureau, pib.gov.in. PMAY-U 2.0 operational guidelines place clear requirements on finishing quality and installed fittings, which translates into steady volumes for branded suppliers and turnkey installers. The Technology & Innovation Sub-Mission under PMAY promotes innovative construction and passive design, which nudges affordable segments toward better materials and greener specifications. Smart city projects and related urban upgrades catalyze fit-out cycles for Grade-A office, retail spaces, and mixed-use developments, feeding commercial interior pipelines across mission cities. These policies extend the demand runway for the India interior design market through a mix of public funding, mandated specifications, and private investment signals.

Commercial Real-Estate Boom in Office, Retail & Hospitality

India crossed 70 million sq ft of office leasing in 2025, with multinational GCCs anchoring a large share, and this is now translating into multi-quarter fit-out momentum. Refurbishment and retrofits are rising in importance as aging Grade-A stock responds to wellness standards, ESG ratings, and hybrid work needs. Retail leasing surged during 2025 with new mall supply and category shifts boosting store buildouts, experiential design, and brand-led specifications across key metros. As retail footprints expand, hospitality and entertainment formats are renewing interiors to differentiate and improve yields in high-traffic districts. This commercial activity strengthens near-term visibility for the India interior design market, particularly in Bengaluru, Mumbai, and Delhi-NCR.

Digital Design Visualisation, Accelerating Customer Acquisition

Design-tech is compressing the concept-to-contract journey as 3D visualization, AR, and VR walkthroughs enable customers to finalize layouts and materials faster. Platforms integrate machine learning into configurators that produce real-time pricing and automated layouts, improving conversion across online and in-store channels. Omnichannel incumbents are enriching discovery through AR experiences and planned interactive kiosks that extend browsing beyond store hours and raise engagement quality. Technology also reduces rework and site visits by improving expectation alignment, which matters in cost-sensitive markets and multi-city franchise models. These gains support scale economics and help organized players extend reach in the India interior design market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highly fragmented & price-competitive supply side | -1.8% | National, most acute in tier-2/3 cities | Long term (≥ 4 years) |

| Compliance cost of building / green regulations | -1.2% | National, concentrated in metros with stricter ESG norms | Medium term (2-4 years) |

| Pandemic-induced project delays & cash-flow pressures | -0.9% | National, lingering effects in tier-2/3 markets | Short term |

| Shortage of accredited designers outside metros | -1.4% | Tier-2/3 cities and rural areas, acute in East & North-East | Long term |

| Source: Mordor Intelligence | |||

Highly Fragmented and Price-Competitive Supply Side

Many transactions still flow through unorganized carpenters and small workshops that compete on price without standardized processes or compliance controls. This fragmentation raises execution risks in complex projects that need assured timelines, multi-vendor coordination, and formal warranties. Organized platforms that do not vertically integrate face margin pressure when material costs and logistics are not under tight control. Vertical integration moves, including investments in component manufacturing and centralized fulfillment, are attempts to stabilize margins and shorten lead times. Until quality norms become universal, mid-market households will continue to evaluate rental and subscription options to avoid large upfront spends and reduce project complexity, which adds a distinct alternative pathway within the India interior design market.

Compliance Cost of Building and Green Regulations

As ESG adoption deepens, projects targeting Grade-A tenants or government contracts must comply with IGBC, LEED, or comparable standards, which lift costs in material choices and documentation. State-level requirements on emissions monitoring, water management, and hazardous substances translate into tighter vendor qualification and on-site processes. SEBI’s BRSR trajectory expands Scope 3 tracking and reporting expectations that flow into procurement and audit routines across supply chains[3]Editors, “Real Estate 2025 – India, Trends and Developments,” Chambers and Partners, chambers.com. While green-certified spaces can command rental premiums, smaller suppliers need to upgrade their capabilities to meet documentation and performance thresholds. These dynamics reshape bidding and specification strategies in the India interior design market as compliance readiness becomes a differentiator[4]Puravankara Limited Editorial Team, “Green Building Certification in India: Shaping the Future of Infrastructure,” Puravankara, puravankara.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Organized Platforms Capture Commercial Share, Residential Volumes Surge

The commercial segment held 74.44% of India's interior design market share in 2025, with leasing momentum across Grade-A office and retail rolling into multi-quarter fit-out pipelines. Office demand is reinforced by multinational GCCs and technology tenants, which require high-spec interiors aligned to global wellness, energy, and accessibility benchmarks. Retail categories are expanding footprints and upgrading stores with experiential fixtures that elevate dwell time and conversion rates in top city markets. Corporate specifications drive consistent volumes in modular workstations, acoustic systems, and integrated lighting, which organized players deliver with predictable quality. This mix of steady corporate demand and formalized procurement supports repeatable project economics across the India interior design market.

Residential demand is the fastest-growing end-user, expected to expand at a 16.47% CAGR through 2031, energized by rising incomes and government housing programs with explicit finishing requirements. Platforms are differentiating through AI-enabled visualization, warranties, and end-to-end installation that de-risk projects for homeowners who once relied on multiple contractors. Residential throughput has scaled as networks spread across more cities, aided by store openings and franchise formats that lower entry barriers in regional markets. Standardized interior requirements within PMAY-U 2.0 and PMAY-G sustain baseline demand for essential fixtures, further deepening suppliers’ addressable volumes. This evolution strengthens the role of organized channels in the India interior design industry, broadening access to design services while improving project reliability.

By Service Type: New Construction Leads, But Renovation Captures ESG Retrofit Demand

New construction accounted for 57.39% of the India interior design market size in 2025, supported by large office and retail developments as well as policy-driven housing programs that specify finishing stages. Office additions and mixed-use projects generate broad demand for fit-outs across corporate floors, common areas, and retail frontages with strict timelines. Public capital expenditure and private investment pipelines create predictable order books for general contractors and design partners across major corridors. This sustains scale for procurement and logistics, enabling platforms and manufacturers to consolidate demand into centralized production and distribution. The cumulative effect supports steady utilization in the India interior design market when combined with urban renewal activity.

Renovation and remodeling are the fastest-growing service line at a 13.35% CAGR through 2031 as owners pursue retrofits that improve tenant appeal, energy efficiency, and space reconfiguration. A sizable share of office inventory is ready for refurbishment, with targeted upgrades supporting higher rents and asset value improvements for landlords. Organized platforms are piloting fast-turnaround packages for small spaces, a format that addresses time-sensitive residential and commercial requirements. Green certification targets and wellness features are now common in renovation briefs, aligning older stock with updated occupational needs. The upshot is a richer mix of new-build and retrofit work that stabilizes the project flow in the India interior design market.

By Price Tier: Mid-Range Holds, Economy Climbs on E-Commerce Turnkey Packages

The mid-range tier commanded 52.35% in 2025 as urban households balanced modular functionality with budget discipline, favoring organized installers for predictable outcomes. Omnichannel brands expanded stores and service models to deepen reach and improve customer experience before the final purchase. As visualization quality improved, mid-range customers upgraded to integrated solutions that include design, manufacturing, and installation under one warranty umbrella. This bracket proves resilient as brands add specialized rooms, gaming lines, and kids’ categories that lock in share-of-wallet. These moves consolidate mid-range leadership across the India interior design market.

The economy tier is the fastest-growing price band at a 14.76% CAGR as platform bundles deliver standard modules at clear price points, assisted by online discovery and faster installations. Franchise models allow rapid city additions while sharing local marketing and sales costs with partners in smaller cities. Rental subscriptions are gaining traction for customers who want flexibility and minimal upfront costs, reshaping entry-level furnishing choices. As BIS quality controls tighten, branded economy offerings can differentiate on safety and durability credentials relative to unorganized alternatives. These signals reinforce an accessible on-ramp into organized interiors, which broadens market coverage while raising quality baselines in the India interior design market.

Geography Analysis

North India held 39.87% in 2025, with Delhi-NCR’s commercial concentration and large-format retail footprints anchoring fit-out demand across categories. The region benefits from ongoing mall, office, and mixed-use developments that sustain pipelines for organized brands and general contractors. IKEA continues its multi-format strategy with smaller studios augmenting flagship outlets, while new “meeting place” investments in the NCR cluster expand retail-led interior work. Platform store plans reflect this density, with omnichannel service models leveraging both physical and online engagement in the India interior design market.

The East and North-East are the fastest-growing regions at an 11.87% CAGR through 2031, as connectivity and organized retail expansion narrow the adoption gap. Franchise expansions by furniture and interior brands into cities like Guwahati and Siliguri are unlocking new store and studio formats. South India leads specialized segments such as senior living, supported by city ecosystems that favor wellness-oriented interiors and tech-enabled conveniences. This mix of regional dynamics expands the addressable base for organized offers in the India interior design market.

West India continues to premiumize with Mumbai and Pune attracting international retailers and high-spec office tenants that demand experiential buildouts. Store rollouts by omnichannel brands and franchise partners show the region’s capacity to absorb organized capacity at scale. Coworking and managed office formats are broadening workspace typologies, pulling through interior solutions that emphasize modularity, acoustics, and collaborative zones. These trends sustain a diverse project mix that reinforces regional resiliency across the India interior design market.

Regulatory Landscape

India does not have a mandatory national licensing regime specifically for interior designers, but adjacent statutory requirements affect how projects are delivered and who can sign off on approvals. Building plan approvals and structural submissions fall under the Architects Act, 1972, administered by the Council of Architecture (COA). As a result, interior design firms typically partner with COA-registered architects for workstreams that touch sanctioned drawings, fire and life-safety coordination, or approval-linked documentation.

On specifications and quality, project requirements often reference the National Building Code of India 2016 (NBC 2016) and applicable Bureau of Indian Standards (BIS) codes used for drawings and performance parameters, alongside municipal and state building byelaws that embed NBC-aligned provisions. BIS codes used in interiors-related documentation include IS 962:1989 (building drawings) and IS 3646 (interior illumination), while the BIS ecosystem and standardized development and building regulations (such as SP 73, aligned to NBC 2016) reinforce documentation discipline for commercial and institutional interiors. In addition to these statutory anchors, voluntary bodies such as the Institute of Indian Interior Designers (IIID, founded 1972) and policy institutions such as the India Design Council (formed under the National Design Policy, 2007) shape professional norms even where statutory licensing is not mandated.

Value Chain Analysis

The value chain covers (i) client acquisition and brief development (developers, corporates, homeowners, brokers), (ii) design and documentation (interior designers, architects, MEP and specialist consultants), (iii) sourcing and fabrication (modular furniture makers, carpentry workshops, surface and lighting vendors, hardware and fittings suppliers), (iv) execution (general contractors, specialized trade contractors, installers), and (v) handover and after-sales (snag closure, warranties, AMC/maintenance). Organized platforms increasingly bundle design-to-build with centralized procurement, standardized catalogs, and project management layers, while the unorganized contractor base remains important for local execution capacity, particularly outside tier-1 markets.

Operational bottlenecks and key differentiation points center on quality consistency, lead times, and compliance-led documentation. From April 1, 2026, the Environment (Construction and Demolition) Waste Management Rules, 2025 apply to renovation and repair activities, pushing contractors and platforms to formalize waste plans and site processes, which can favor players with repeatable SOPs and vendor governance. On sustainability and specifications, frameworks such as GRIHA for Interior Spaces (InS) V1.0 (launched January 2026) offer a structured pathway for material and resource-efficiency choices, while BIS-aligned product standards and state building rules shape procurement screens for modular components, boards, lighting, and on-site workmanship.

Competitive Landscape

The India interior design market is bifurcating between organized platforms that scale omnichannel networks and unorganized vendors that compete on price in non-metro pockets. Platforms differentiate through visualization, warranties, and project management that reduce execution risk for both homeowners and corporate tenants. Livspace reported 23% year-on-year growth in FY25 while shifting toward premium and mass-premium cohorts that accept higher take-rates for full-stack execution. HomeLane marked a profitability inflection in Q4 FY25, reflecting franchise scale and operating discipline focused on customer acquisition cost and throughput.

Vertical integration and supply-chain control are gaining favor as ways to stabilize margins and reduce imported component markups. Livspace’s strategic stake in a furniture hardware manufacturer supports local sourcing to compress costs and shorten lead times. Godrej Interio targets USD 1,169.4 million (INR 10,000 crore) in three years with a sharpened brand identity, expanded store footprint, and immersive online experiences that improve discovery and conversion. IKEA is calibrating store formats by adding smaller studios to capture local catchments that complement the footfall magnetism of large flagships.

Design firms embedded in GCCs and hybrid work models are using data-informed layouts, generative tools, and flexible systems to win enterprise projects. Rental and subscription platforms such as Furlenco provide an alternative value proposition for customers who prefer access and flexibility over ownership, shifting spend patterns for furniture and interiors. As regulations elevate the importance of documentation and certifications, organized players that can coordinate compliant suppliers gain an advantage in larger bids. These strategic adjustments are reshaping competitive playbooks and raising execution standards across the India interior design market.

India Interior Design Industry Leaders

Homelane

Pepperfry Studio

Urban Ladder

IKEA India – Planning Studio

Godrej Interio

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

ESG-linked retrofits and compliance-led renovation workflows create an opening where organized firms can productize audits, documentation, and faster-turn execution for Grade-A offices and institutional spaces. The launch of GRIHA for Interior Spaces (InS) V1.0 in January 2026 provides a recognized framework for interiors-specific sustainability scoring, supporting packaged offerings around low-impact materials, resource efficiency, and measurable performance criteria. With renovation and remodeling already a major service line, standardizing processes for waste segregation, material traceability, and post-handover maintenance can improve bid outcomes in projects that require documented results.

Platform-based, tech-enabled delivery is also a practical expansion lever as companies shift toward hybrid operating models that combine visualization and automation with distributed execution capacity. At the same time, the April 1, 2026 implementation of the Environment (Construction and Demolition) Waste Management Rules, 2025 raises requirements for renovation site management, increasing demand for organized execution, compliant disposal partners, and repeatable worksite governance. Public-sector procurement can be another access channel as discussions around expanding Government e-Marketplace (GeM) coverage to architectural and interior services (highlighted around Union Budget 2026) point toward more standardized tendering expectations, where firms with transparent BoQs, QA checklists, and multi-city delivery capability can compete more effectively.

Recent Industry Developments

- July 2026: IKEA India announced plans to double its investment in India to over INR 21,000 crore by 2030, alongside efforts to deepen local sourcing. The announcement supports long-horizon retail and supply availability for home furnishings and modular categories that feed into interior execution pipelines across major cities.

- December 2025: TCC Concept Limited completed the acquisition of a 98.75% stake in Pepperfry Limited. The ownership consolidation supports a broader reset of strategy and capital backing for omnichannel studios and B2B decor initiatives, affecting competitive intensity in organized home interiors and furnishings.

- September 2024: HomeLane acquired DesignCafe in a share-swap deal to expand its scale in modular kitchens and home interiors. The combination increases network density and procurement leverage, supporting faster multi-city rollouts and more standardized execution for mid-range residential customers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the India interior design market is counted as the value of interior design services delivered within India for residential and commercial spaces, including new build and renovation projects, across price points.

Scope exclusions: We exclude the stand-alone sale of furniture, home decor items, and building materials when they are not tied to an interior design service contract.

Segmentation Overview

- By End-User

- Residential

- Commercial

- By Service Type

- New Construction

- Renovation / Remodeling

- By Price Tier

- Economy

- Mid-Range

- Premium / Luxury

- By Region

- North India

- West India

- South India

- East & North-East India

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by framing the demand pool for interiors and the activity level in construction and remodeling. We refer to public statistics and industry releases such as Ministry of Housing and Urban Affairs updates, National Statistical Office publications, RBI data on housing and credit conditions, GST collections as a broad spending signal, and state RERA dashboards for project trends.

To stress test the service-led scope, we also use company annual reports, investor presentations, and reputed business press for order commentary and pricing direction. Patent databases can help confirm which design and visualization tools are being adopted, and shipment-level import-export databases are used selectively to sanity check movement in finish and fixture categories that often trigger redesign cycles. This desk source list is illustrative, and many other sources were also consulted for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focuses on clarifying what share of interior spend is captured as paid design service fees and how pricing shifts by project type and city tier. We speak with design studios, contractors and fit-out partners, and commercial project buyers so assumptions on typical project values, fee structures, conversion rates, and renovation frequency are not left to desk estimates alone.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 18% | |

| Mid tier: 40% | Functional/Unit leaders: 29% | |

| Smaller Players: 22% | Managers: 53% |

Market-Sizing & Forecasting

The core model is built using a top-down approach where construction and renovation activity is translated into a serviceable interior design demand pool, and then converted into value using typical design fee rates and project mix. Once that picture is formed, we corroborate it with selective bottom-up checks like sampled studio revenue ranges, channel discussions on project ticket sizes, and ASP-by-square-foot benchmarks to adjust for under-reporting in fragmented parts of the market.

Inputs used in the model include new housing additions and completions, commercial space additions in offices and retail, renovation and remodeling frequency in metro versus non-metro cities, the share of projects using organized design services, and the average design fee progression by economy, mid-range, and premium work. Where direct visibility is limited for very small studios, gap handling is done through calibrated penetration rates and validated price bands rather than assuming a full roll-up.

For forecasting, scenario analysis is used because demand moves with real estate cycles and discretionary spending. We apply agreed forward drivers from interviews, and then test high and low cases around housing momentum, commercial fit-out cycles, and expected fee inflation.

Data Validation & Update Cycle

Outputs are checked against independent signals like construction momentum, renovation triggers, and observed pricing movement, and then variance flags are reviewed before sign-off. If a city or end-use trend looks out of line, we re-check inputs, revisit assumptions, and re-contact relevant respondents until the delta is explainable.

Reports are refreshed annually, and interim updates are made when material events change demand or pricing. Before delivery, an analyst does a fresh review pass so clients receive the latest updated view.

Mordor Intelligence's India Interior Design Market Sizing Compared With Other Published Estimates

Published market sizes for India interior design can look far apart because authors do not always count the same thing, even when the title sounds identical. Differences usually come from what is treated as a service fee versus a broader interiors basket, and from how pricing is converted and carried forward.

In practice, the gap tends to be driven by whether a study includes furniture and decor sales, whether it mixes home interiors with full commercial fit-outs, and whether fee rates are assumed to rise smoothly without checks. By time-aligning currency conversion, rechecking fee bands with fresh interviews, and updating ASP logic when a project mix shift is observed, Mordor Intelligence keeps the estimate closer to the value of interior design services actually billed in India.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 31.43 B (2025) | |

| Trade Journal A | USD 36.90 B (2025) | Often presented as a broader interiors value that can fold in furnishings and decor-linked spending, which lifts the total beyond service fees. |

| Industry Platform B | USD 31.50 B (2023) | Uses an earlier base year and a simplified growth path to later years, with limited visibility on how fee rates and renovation cycles were validated across city tiers. |

Across the three figures, the spread is mainly explained by scope boundaries and how pricing is carried forward year to year. When the counted basket is kept service-led and assumptions are refreshed in line with current fee levels and demand signals, the resulting market value is easier to trace and repeat.

Key Questions Answered in the Report

What is the current size and growth outlook for the India interior design market?

The India interior design market size is USD 35.48 billion in 2026 and is forecast to reach USD 65.01 billion by 2031 at a 12.87% CAGR.

Which end-user is the fastest growing in the India interior design market?

Residential is the fastest growing, expected to expand at a 16.47% CAGR through 2031 as incomes rise and housing programs mandate finished interiors.

Which service line is expanding the quickest within the India interior design market?

Renovation and remodeling are growing at a 13.35% CAGR as office retrofits, wellness criteria, and ESG compliance drive upgrades to existing stock.

How are platforms changing customer experience in the India interior design market?

AI-enabled visualization, AR, and VR reduce decision cycles and improve cost transparency, while omnichannel showrooms and franchise formats expand access in rising cities.

Which regions lead demand in the India interior design market?

North India leads by share due to Delhi-NCR’s commercial base, while East and North-East India grow fastest as connectivity and organized retail expand.

What regulations are influencing specifications in the India interior design market?

BIS quality controls and green certification frameworks such as IGBC and LEED are increasingly embedded in project criteria, raising documentation and performance requirements.

Page last updated on: