| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 3.86 Billion |

| Market Size (2030) | USD 5.84 Billion |

| CAGR (2025 - 2030) | 8.65 % |

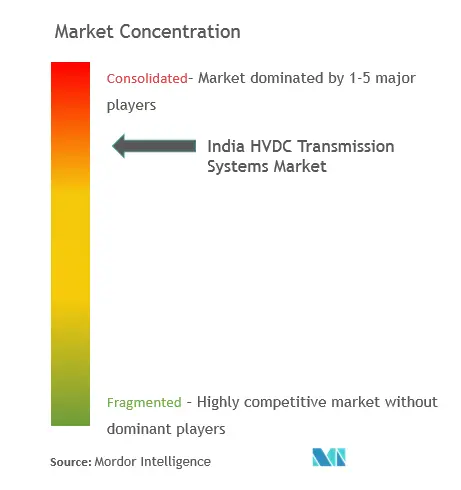

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

India HVDC Transmission System Market Analysis

The India HVDC Transmission Systems Market size is estimated at USD 3.86 billion in 2025, and is expected to reach USD 5.84 billion by 2030, at a CAGR of 8.65% during the forecast period (2025-2030).

India's power transmission infrastructure is undergoing a significant transformation driven by technological advancements and increasing power demand. The electricity transmission sector has witnessed substantial private sector participation, reflecting growing investor confidence and market maturity. The transmission landscape is evolving with the integration of advanced technologies like voltage source converter (VSC) technology, which was first introduced in the country through Power Grid Corporation's Pugalur-Thrissur HVDC transmission systems project in February 2021, representing a milestone in India's power transmission capabilities.

The market is experiencing a shift toward underground HVDC transmission systems, particularly in urban areas where overhead lines pose challenges. This trend is exemplified by the Maharashtra government's ambitious plan announced in December 2020 to invest INR 8000 crore in an 80-kilometer underground HVDC line from Aarey to Kudus in Palghar district, designed to provide an additional 1000 megawatts of electricity to the state. Such projects demonstrate the growing preference for underground transmission solutions in densely populated regions while addressing environmental and aesthetic concerns.

The integration of renewable energy transmission sources is reshaping the HVDC transmission landscape, with particular emphasis on offshore wind power development. India's ambitious target to deploy 30 GW of offshore wind energy installations by 2030 is creating substantial opportunities for HVDC technology, which is particularly efficient for offshore environments. This strategic focus on renewable energy transmission is driving innovations in transmission technology and infrastructure development across the country.

Cross-border power transmission projects are emerging as a significant trend in India's HVDC market. Notable developments include the ongoing exploration of an overhead electricity link with Sri Lanka, featuring a planned 2x500 MW HVDC line between Madurai and New Habarana. Additionally, India's existing power supply arrangements with Bangladesh, including the 1,000 MW through Baharampur to Bheramara AC link and various other interconnections, demonstrate the growing importance of international power exchange infrastructure in the region's energy landscape.

India HVDC Transmission System Market Trends

Growing Power Transmission Requirements and Grid Expansion

India's position as the second-most populous country globally has created an unprecedented demand for robust electrical transmission systems. The increasing size and complexity of transmission networks have introduced significant challenges related to load flow management, power oscillation control, and voltage quality maintenance, making HVDC transmission systems an essential solution for modern power distribution needs. This is evidenced by the fact that over 58% of the country's transmission lines operate at voltage ratings exceeding 400 kV, demonstrating the clear shift toward high-capacity power transmission systems.

The implementation of the One Nation-One Grid initiative has further accelerated the need for efficient power grid systems, enabling seamless interregional electricity exchange between surplus and deficit regions. This is particularly crucial given that power transmission and distribution companies faced substantial losses of INR 27,000 crore, primarily attributed to transmission and distribution inefficiencies. Major infrastructure projects, such as Maharashtra's billion-dollar underground HVDC project from Aarey to Kudus in Palghar District, exemplify the continued investment in expanding and modernizing the country's transmission capabilities to address critical power supply challenges in metropolitan regions.

Understand The Key Trends Shaping This Market

Download PDF

Cost Advantages and Technical Benefits of HVDC Systems

HVDC transmission systems offer compelling economic advantages over traditional HVAC systems, particularly in terms of construction and operational costs. The simplified tower construction requirements and lower per-unit costs, including both per kilometer of line and per MW of transmitted power, make HVDC solutions increasingly attractive for long-distance power transmission projects. This cost efficiency is further enhanced by the reduced number of conductors required in HVDC systems compared to HVAC networks, resulting in lower mechanical loads and decreased transmission line costs over distances exceeding 100 kilometers.

The technical superiority of HVDC technology is demonstrated through its inverse relationship between voltage ratings and transmission losses, enabling more efficient power transmission at higher voltages. This advantage is particularly valuable in land-constrained areas, where HVDC lines' higher power transmission capacity allows for more efficient land utilization. The successful implementation of major projects, such as the Raigarh-Pugalur-Thrissur 6000 MW HVDC system, showcases the practical benefits of these systems in achieving efficient power transfer across vast distances while maintaining system stability and reliability.

Increasing Focus on Renewable Energy Integration

The ambitious renewable energy targets set by the Indian government have created a strong impetus for HVDC technology adoption. The integration of large-scale renewable energy projects, particularly from remote generation sites, requires sophisticated transmission solutions that can efficiently handle variable power flows and maintain grid stability. HVDC systems' superior control capabilities and lower losses make them ideal for connecting renewable energy sources to the main grid, as demonstrated by numerous successful projects across the country.

The expansion of existing HVDC networks through capacity additions and new project developments reflects this growing focus on renewable energy integration. Significant infrastructure developments, such as the Jharsuguda (Sundargarh) substation with its 3000 MVA capacity addition, demonstrate the scale of investment in HVDC infrastructure to support renewable energy transmission. The ongoing expansion projects, including the upgrade of the Champa Pool-Kurukshetra HVDC Bipole from 1500 MW to 2000 MW, further illustrate the commitment to enhancing the country's renewable energy transmission capabilities through smart grid transmission.

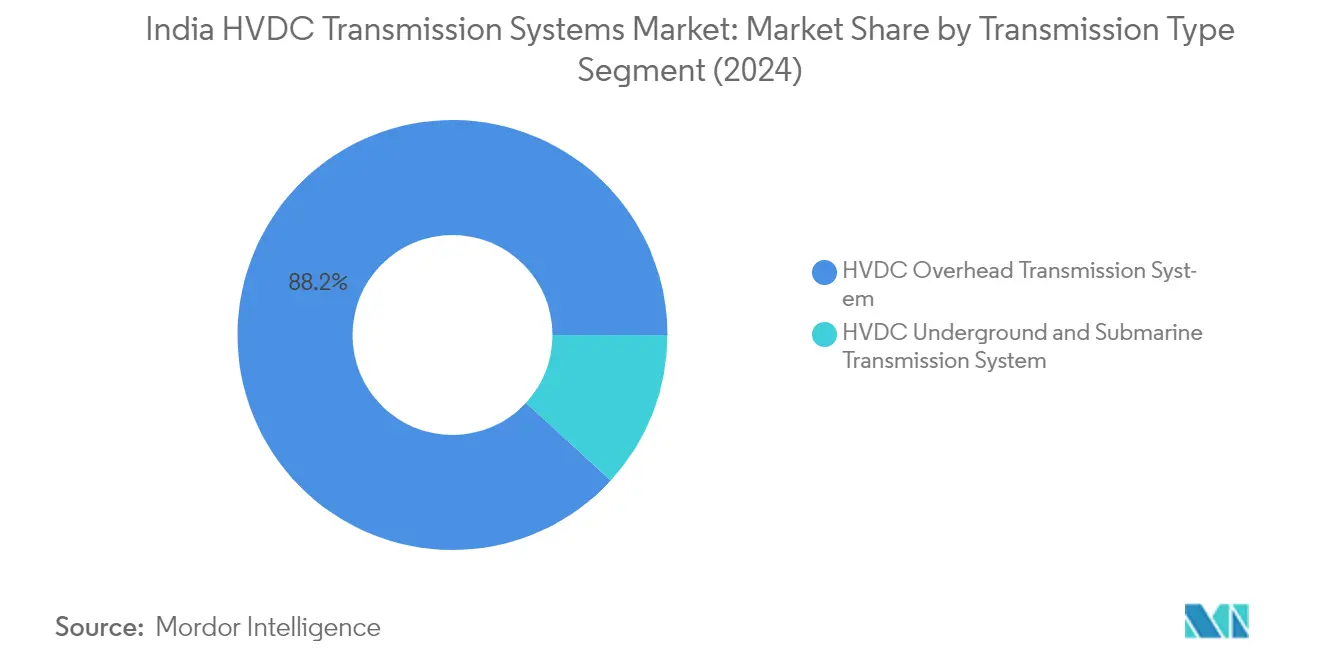

Segment Analysis: Transmission Type

HVDC Overhead Transmission Segment in India HVDC Transmission Systems Market

The HVDC overhead transmission system segment continues to dominate the India HVDC transmission systems market, holding approximately 88% market share in 2024. This segment's dominance can be attributed to several key advantages, including simpler line tower construction requirements compared to HVAC transmission lines, and lower per-unit costs, including cost per km of line and per MV of transmitted power. The technology's ability to transport more power with fewer transmission losses compared to HVAC systems has made it particularly attractive for long-distance power transmission projects. Additionally, the segment's growth is being driven by increasing cross-border power transmission projects and capacity additions in pre-existing HVDC networks. The deployment of advanced technologies like Voltage Source Converter (VSC) HVDC overhead transmission and ultra-high-voltage direct current (UHVDC) overhead line technology has further strengthened this segment's market position.

HVDC Underground and Submarine Transmission Segment in India HVDC Transmission Systems Market

The HVDC underground and submarine transmission segment, while smaller in market share, plays a crucial role in specific applications where overhead transmission is not feasible. This segment is particularly important in densely populated urban areas and for subsea power transmission applications. The segment utilizes two main cable technologies: Single-core Mass Impregnated Cables and Polymeric Cables, each serving specific voltage and power capacity requirements. The increasing focus on offshore wind power projects, following the Indian Ministry of New and Renewable Energy's targets, and the growing need for power transmission in urban areas are creating new opportunities for this segment. The segment is also benefiting from technological advancements in cable design and installation techniques, making underground and submarine transmission more reliable and efficient for specific applications. The use of HVDC cable technologies is integral to meeting these demands, ensuring efficient DC transmission over long distances.

Segment Analysis: Component

Converter Stations Segment in India HVDC Transmission Systems Market

The converter stations segment dominates the India HVDC transmission systems market, holding approximately 92% market share in 2024. This significant market share is driven by the critical role converter stations play as specialized substations that form the terminal equipment for HVDC transmission lines. The segment's dominance is supported by technological advancements in both Line-commutated Converters (LCC) and Voltage Source Converters (VSC), with modern converter stations incorporating features like thyristor valves, cooling systems, HVDC control and protection systems, direct current measuring devices, and surge arrestors. The increasing deployment of large-scale HVDC projects across India, such as the Raigarh-Pugalur 800 kV ultra-high-voltage direct current system spanning over 1800 km, continues to drive substantial demand for HVDC converter stations.

Transmission Medium (Cables) Segment in India HVDC Transmission Systems Market

The transmission medium (cables) segment is experiencing rapid growth in the India HVDC transmission systems market from 2024-2029, driven by increasing investments in underground and submarine cable projects. The growth is supported by the technical advantages of HVDC cable transmissions, including lower losses, improved system stability, and enhanced reliability. The segment's expansion is particularly notable in projects requiring longer transmission lines and hybrid configurations, where HVDC cable systems provide controllable bulk power transmission capacity without increasing short circuit current levels. The development of new cable technologies and materials, combined with India's push towards modernizing its power transmission infrastructure, is expected to further accelerate the growth of this segment during the forecast period. The integration of advanced HVDC components and power electronics is crucial in enhancing the efficiency and reliability of these systems.

India HVDC Transmission System Industry Overview

Top Companies in India HVDC Transmission Systems Market

The market features established players like Hitachi ABB Power Grids, Siemens AG, General Electric, Power Grid Corporation of India Limited, and Bharat Heavy Electricals Limited leading the competitive landscape. These companies are focusing on technological advancement through the development of next-generation digital control systems and enhanced HVDC power electronics for HVDC applications. Strategic collaborations between equipment manufacturers and EPC contractors have become increasingly common to strengthen project execution capabilities. Companies are expanding their domestic manufacturing footprint in response to the government's Make in India initiative, with many establishing dedicated facilities for HVDC components. The industry is witnessing increased investment in research and development, particularly in areas like voltage source converter technology and smart grid integration. Market leaders are also emphasizing service capabilities through comprehensive operation and maintenance solutions while developing specialized expertise in areas like submarine cable systems and ultra-high voltage transmission.

Market Dominated by Integrated Solution Providers

The HVDC transmission systems market in India exhibits a relatively consolidated structure dominated by large multinational corporations with integrated capabilities across the value chain. These companies combine manufacturing expertise with project execution capabilities, offering turnkey HVDC solutions from component manufacturing to system commissioning. The competitive landscape is characterized by high entry barriers due to the technical complexity of HVDC systems and substantial capital requirements for establishing manufacturing facilities. Recent years have seen increased participation from domestic players, particularly in components and EPC services, though global technology leaders maintain their dominance in core HVDC equipment.

The market has witnessed significant merger and acquisition activity, particularly aimed at strengthening technological capabilities and expanding geographic presence. Notable transactions include Hitachi's acquisition of ABB's power grids business and Adani's strategic acquisitions in the transmission sector. Companies are increasingly forming joint ventures and technical collaborations to combine complementary strengths in technology and project execution. The industry structure is evolving with the emergence of specialized players in specific components or services, though they typically operate in partnership with major system integrators.

Innovation and Localization Drive Market Success

For established players, maintaining market leadership increasingly depends on developing advanced technological solutions while simultaneously expanding local manufacturing capabilities to meet domestic content requirements. Companies need to focus on building comprehensive service networks, establishing strong relationships with state utilities, and developing innovative financing solutions for large-scale projects. Success also requires maintaining a balanced portfolio between equipment supply and EPC services, while investing in digital capabilities for smart grid transmission and remote asset management. Incumbent players must additionally focus on cost optimization through local sourcing and manufacturing to remain competitive in price-sensitive market segments.

New entrants and challenger companies can gain market share by focusing on specific components or services where entry barriers are relatively lower, such as cable systems or maintenance services. Building strategic partnerships with established players for technology access while developing specialized expertise in emerging areas like renewable energy integration presents a viable entry strategy. Companies must also navigate the regulatory landscape, particularly regarding domestic manufacturing requirements and grid connectivity standards. The increasing focus on renewable energy integration and grid modernization creates opportunities for companies with innovative solutions in these areas, while the government's emphasis on self-reliance in manufacturing presents opportunities for local players to expand their presence in the supply chain.

India HVDC Transmission System Market Leaders

-

General Electric Company

-

Bharat Heavy Electricals Limited

-

TAG Corporation

-

Power Grid Corporation of India Limited

-

Hitachi Energy Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

India HVDC Transmission System Market News

- In February 2021, Power Grid Corporation of India Limited (POWERGRID) inaugurated its 320 kV 2000 MW Pugalur (Tamil Nadu) - Thrissur (Kerala) HVDC project. The project was the first time a Voltage Source Converter (VSC) technology has been used introduced in the country for transmission. Out of the 165 kilometers (km) of the transmission, 27 Km were underground cables. The overall project cost was approximately INR 5070 crores.

- In December 2020, Maharashtra Government revised its plan to invest INR 8000 crore on 80 kilometers (Km) underground high voltage direct current (HVDC) line from Aarey to Kudus in Palghar district.

India HVDC Transmission System Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

5. MARKET SEGMENTATION

-

5.1 Transmission Type

- 5.1.1 HVDC Overhead Transmission System

- 5.1.2 HVDC Underground & Submarine Transmission System

-

5.2 Component

- 5.2.1 Converter Stations

- 5.2.2 Transmission Medium (Cables)

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Hitachi Energy Ltd

- 6.3.2 Siemens AG

- 6.3.3 General Electric Company

- 6.3.4 Adani Transmission Ltd

- 6.3.5 TAG Corporation

- 6.3.6 Power Grid Corporation of India Limited

- 6.3.7 Bharat Heavy Electricals Limited

- 6.3.8 Tata Projects Limited

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

India HVDC Transmission System Industry Segmentation

The India HVDC transmission systems market report includes:

| Transmission Type | HVDC Overhead Transmission System |

| HVDC Underground & Submarine Transmission System | |

| Component | Converter Stations |

| Transmission Medium (Cables) |

Need A Different Region or Segment?

Customize Now

India HVDC Transmission System Market Research FAQs

How big is the India HVDC Transmission Systems Market?

The India HVDC Transmission Systems Market size is expected to reach USD 3.86 billion in 2025 and grow at a CAGR of 8.65% to reach USD 5.84 billion by 2030.

What is the current India HVDC Transmission Systems Market size?

In 2025, the India HVDC Transmission Systems Market size is expected to reach USD 3.86 billion.

Who are the key players in India HVDC Transmission Systems Market?

General Electric Company, Bharat Heavy Electricals Limited, TAG Corporation, Power Grid Corporation of India Limited and Hitachi Energy Ltd are the major companies operating in the India HVDC Transmission Systems Market.

What years does this India HVDC Transmission Systems Market cover, and what was the market size in 2024?

In 2024, the India HVDC Transmission Systems Market size was estimated at USD 3.53 billion. The report covers the India HVDC Transmission Systems Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the India HVDC Transmission Systems Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

India HVDC Transmission Systems Market Research

Mordor Intelligence delivers a comprehensive analysis of the HVDC transmission systems industry. We leverage deep expertise in electrical transmission systems and power transmission systems. Our extensive research covers crucial components, including voltage source converter technology, HVDC cable installations, and HVDC transformer implementations. The report provides detailed insights into HVDC technology developments and HVDC converter innovations. It also explores emerging DC transmission trends, available in an easy-to-download report PDF format.

Stakeholders gain valuable insights into the evolution of power grid systems, including HVDC grid infrastructure and HVDC interconnector projects across India. The analysis encompasses HVDC components, HVDC equipment, and advanced HVDC solutions driving industry growth. Our research extensively covers renewable energy transmission capabilities, smart grid transmission technologies, and power electronics in HVDC applications. This offers stakeholders a comprehensive understanding of market dynamics and growth opportunities in the high voltage direct current transmission systems sector.