Market Trends of India Home Loan Industry

Lower Interest Rates is Expected to Drive the Market

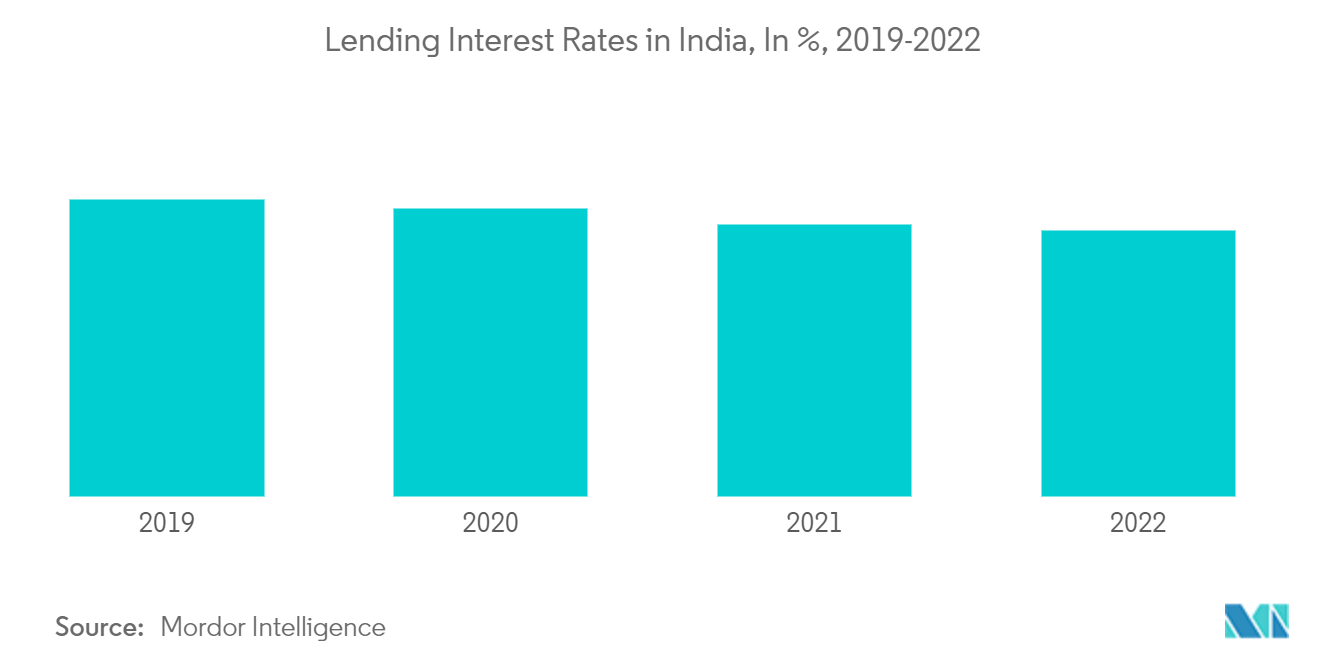

Lower interest rates have been a significant trend in the home loan market in India. The Reserve Bank of India (RBI) plays a crucial role in determining the interest rates in the economy. Through its monetary policy, the RBI adjusts key policy rates, such as the repo rate, which influences lending rates in the market. Lowering the repo rate makes borrowing cheaper for banks, enabling them to offer home loans at reduced interest rates. In recent years, the RBI has implemented a series of repo rate cuts as part of its efforts to boost economic growth and encourage borrowing. These rate cuts have a cascading effect on the interest rates charged by lenders, including banks and housing finance companies, leading to lower home loan interest rates.

The home loan market in India is highly competitive, with several lenders vying for borrowers. To attract customers, lenders often reduce their interest rates to offer more attractive loan products compared to their competitors. This competition among lenders has contributed to the overall decline in home loan interest rates. The Indian government has launched various initiatives to promote affordable housing and increase homeownership. These initiatives, such as the Pradhan Mantri Awas Yojana (PMAY) and Credit-Linked Subsidy Scheme (CLSS), provide interest rate subsidies and incentives for eligible home loan borrowers. The government's focus on affordable housing has put additional downward pressure on interest rates.

Rise in Affordable Housing

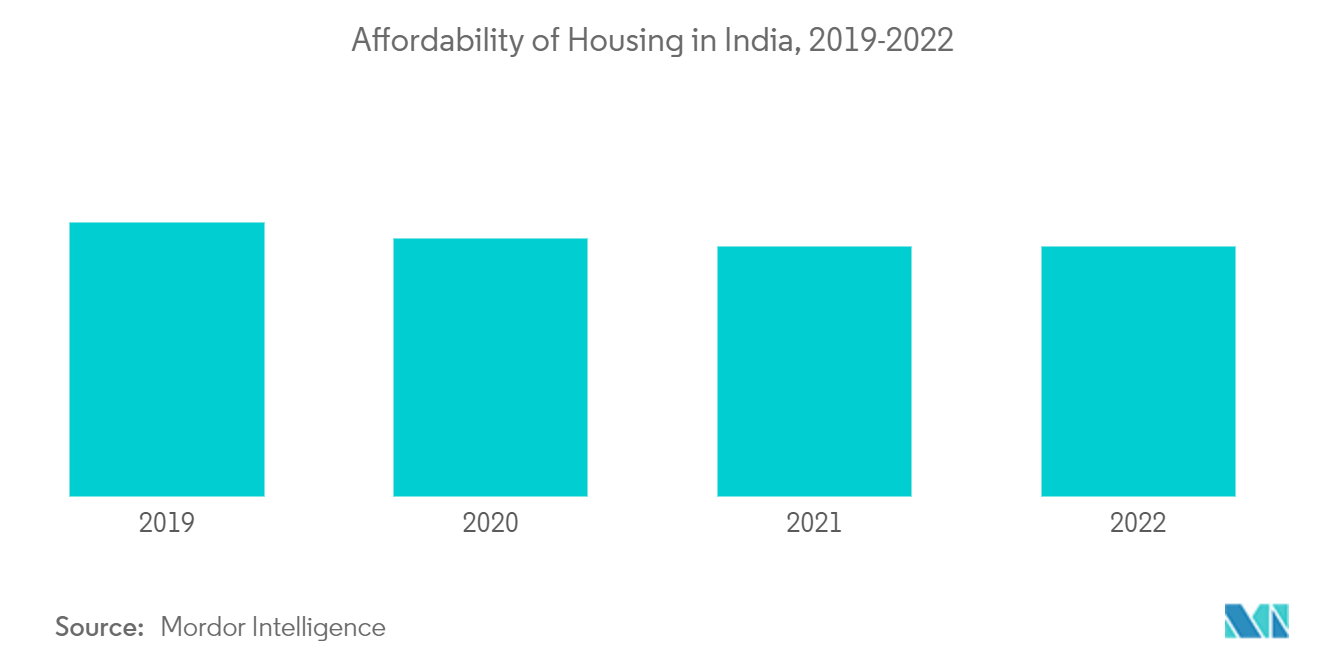

The rise in affordable housing has been a significant trend in the Indian home loan market. In the financial year 2022, the balance of property prices by annual income resulted in affordability of 3.2 for housing in India, the same as the previous year. Thereby, the affordability reached the lowest value since 2011, which makes housing more affordable. The Indian government has launched several initiatives to promote affordable housing and increase homeownership. One of the notable schemes is the Pradhan Mantri Awas Yojana (PMAY), which aims to provide affordable housing for all by 2022. Under PMAY, eligible borrowers can avail of interest rate subsidies and financial assistance, making homeownership more affordable. As part of the PMAY, the Credit-Linked Subsidy Scheme provides interest rate subsidies to home loan borrowers from the economically weaker sections (EWS), lower-income groups (LIG), and middle-income groups (MIG). The CLSS has played a crucial role in making home loans more affordable and accessible to a broader segment of the population.

The Indian government provides tax benefits on home loans, primarily through deductions on the principal repayment and interest payment components. These tax incentives reduce the overall cost of homeownership, making it more affordable for borrowers. Developers and real estate companies have recognized the demand for affordable housing and have focused on increasing the supply of such properties. The rise in affordable housing projects across the country has provided homebuyers with more options in terms of price, location, and amenities. Lenders have introduced specific home loan products tailored for affordable housing. These loans often come with competitive interest rates, relaxed eligibility criteria, and higher loan-to-value ratios, making it easier for borrowers to finance their affordable homes.

Technology has played a role in streamlining the construction and financing processes, leading to cost efficiencies in affordable housing projects. Innovative construction methods, such as prefabricated and modular construction, have helped reduce construction costs and improve affordability. The growth of affordable housing is not limited to major cities but has also extended to tier 2 and tier 3 cities. Developers and lenders are increasingly targeting these smaller cities and towns, where land and construction costs are relatively lower, contributing to the affordability factor.