India Home Loan Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 379.72 Billion |

| Market Size (2030) | USD 765.73 Billion |

| Growth Rate (2025 - 2030) | 15.06% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Home Loan Market Analysis by Mordor Intelligence

The India home loan market size reached USD 379.72 billion in 2025 and is forecast to touch USD 765.73 billion by 2030, advancing at a 15.06% CAGR during 2025-2030. Demographic shifts, urban migration beyond Tier-1 metros, and sustained policy support are enlarging the lending opportunity pool for the India home loan market. Aggressive monetary easing, 100 basis points of repo-rate cuts in 2025, has lowered borrowing costs, while extension of Pradhan Mantri Awas Yojana (PMAY) subsidies through 2027 keeps affordable housing demand buoyant[1]Reserve Bank of India, “Monetary Policy Report April 2025,” rbi.org.in. Rapid deployment of Digital Public Infrastructure (Aadhaar, UPI, Account Aggregators) has trimmed customer-onboarding costs from USD 12 to USD 0.06, raising operating leverage for incumbent and new lenders[2]World Bank, “India’s Digital Public Infrastructure,” worldbank.org. Public-sector banks still originate the largest loan volumes, yet nimble NBFCs are gaining in the India home loan market through specialized underwriting aimed at underserved segments.

Key Report Takeaways

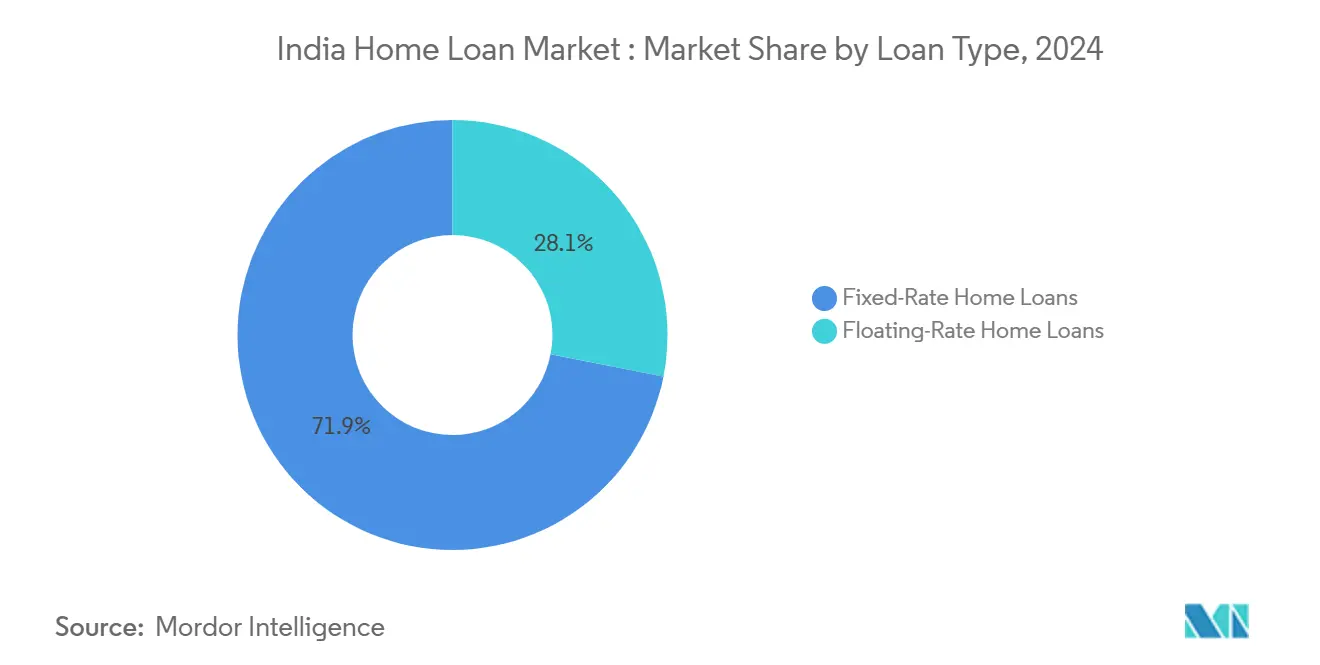

- By loan type, floating-rate products led with 71.9% of the India home loan market share in 2024; fixed-rate loans are projected to post a 15.94% CAGR to 2030.

- By provider type, public-sector banks held 46.7% revenue share in 2024, whereas NBFCs are anticipated to expand at a 15.54% CAGR through 2030.

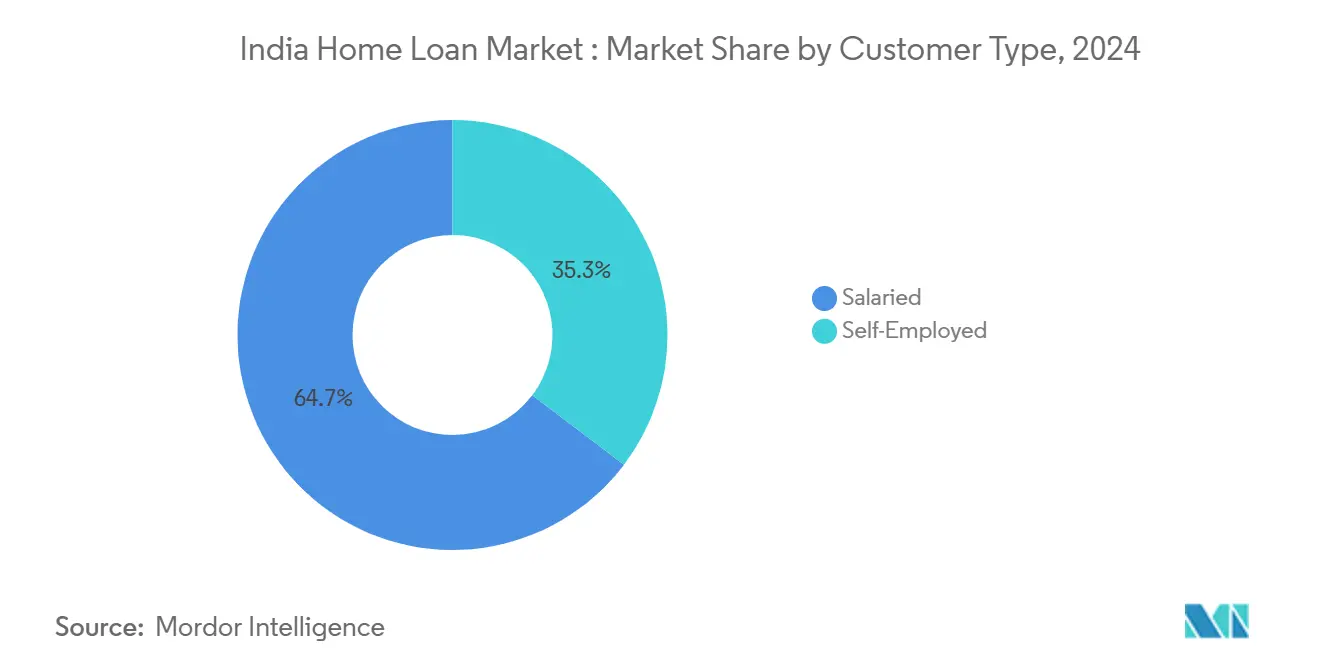

- By customer type, salaried borrowers accounted for a 64.6% slice of the India home loan market size in 2024, and self-employed borrowers are expected to register a 16.12% CAGR to 2030.

- By interest-subsidy participation, non-subsidized loans represented 69.5% of originations in 2024, while the PMAY-CLSS segment is set to climb at a 15.73% CAGR through 2027.

India Home Loan Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated urban migration into Tier-2 & Tier-3 cities | +2.8% | Tier-2/3 cities, peri-urban corridors | Medium term (2-4 years) |

| Surge in women-centric tax incentives & preferential rates | +1.9% | National, urban clusters | Short term (≤ 2 years) |

| Increasing formal-sector employment & payroll digitization | +2.1% | National, organized-sector hubs | Medium term (2-4 years) |

| PMAY subsidies extended through 2027 | +1.7% | National, EWS/LIG borrowers | Short term (≤ 2 years) |

| Embedded-finance distribution via PropTech platforms | +1.3% | Urban, tech-enabled markets | Short term (≤ 2 years) |

| Satellite-based property-valuation data | +0.8% | National, large cities first | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Urban Migration into Tier-2 & Tier-3 Cities

Industrial decentralization and improved infrastructure are drawing households toward smaller cities where real-estate prices stand 40-60% below Tier-1 benchmarks[3]Cushman & Wakefield, “India Urbanization Outlook 2030,” cushmanwakefield.com. Lower ticket sizes produce favorable loan-to-value ratios, enhancing credit acceptance in the India home loan market. Union-government capital spending climbed 38.8% between FY2020 and FY2024, funding roads, rail, and metro projects that boost liveability in these growth corridors. Lenders now open dedicated micro-branches and deploy digital KYC vans to deepen reach. As a result, first-time buyer demand is outpacing supply, supporting double-digit disbursement growth.

Surge in Women-Centric Tax Incentives & Preferential Rates

Banks shave 5–25 bps off standard mortgage rates for women, citing stronger repayment behavior and policy encouragement toward gender-balanced asset ownership. Women’s formal-sector payroll additions doubled over six years, expanding the qualified borrower base. The India home loan market taps this demographic through joint-name documentation that secures lower stamp duty in several states. Lenders also bundle credit-life products tailored for women’s safety nets. These targeted benefits reinforce inclusive growth in mortgage origination volumes.

Increasing Formal-Sector Employment & Payroll Digitization

Formal hiring grew alongside a drop in unemployment to 3.2% in 2024, raising predictable cash flows for credit assessment. Account Aggregator rails give lenders real-time access to salary credits, GST returns, and UPI inflows after borrower consent. Verification costs fell from INR 100 to under INR 10, boosting operating margins across the India home loan market. Dynamic payroll analytics let lenders underwrite gig-workers on daily income data instead of static tax returns. Consequently, borrowers with irregular income histories gain formal-credit inclusion.

PMAY Subsidies Extended Through 2027

More than 8.9 million houses have been completed under PMAY, affirming sustained demand for CLSS-linked mortgages. Eligible borrowers receive up to 6.5% interest subvention, shrinking effective monthly payments. Digital subsidy disbursal cuts approval lags that once hampered affordability. Lenders face lower credit risk because the government offsets a portion of the interest. The program’s extension secures a multi-year runway for affordable-housing loan growth in the India home loan market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continued policy-rate volatility | −1.4% | National | Short term (≤ 2 years) |

| Rising developer insolvencies delaying possession | −0.9% | NCR, MMR hotspots | Medium term (2-4 years) |

| Unaddressed land-title ambiguities | −0.7% | Peri-urban Tier-2/3 | Long term (≥ 4 years) |

| Climate-risk exclusions for flood districts | −0.5% | Coastal belts, river basins | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Continued Policy-Rate Volatility

Although the repo rate dipped in 2025, global inflation remains unstable, generating repricing risk for 71.93% floating-rate loans. Borrowers face higher EMI shocks during upward cycles, stretching household budgets. Lenders absorb margin compression or pass costs, risking demand pullback. Fixed-rate products partly shield customers, yet they demand sophisticated asset-liability alignment. Persistent rate swings, therefore, temper growth momentum in the India home loan market.

Rising Developer Insolvencies Delaying Possession

More than 138,000 real-estate complaints were resolved under RERA by January 2025, spotlighting chronic project delays[4]Press Information Bureau, “RERA Progress Dashboard January 2025,” pib.gov.in. Buyers paying pre-delivery EMIs often juggle both rent and mortgage, heightening default probability. Lenders consequently tighten credit to projects without escrow safeguards. Insolvency events also strand construction-finance exposure on bank books, locking capital that could serve end-user mortgages. Such cascading stress softens origination appetite in certain corridors of the India home loan market.

Segment Analysis

By Loan Type: Fixed-Rate Products Gain Momentum

Floating loans dominated disbursals, yet fixed-rate balances are growing quickly as households hunt for payment stability. By loan type, floating-rate products led with 71.9% of the India home loan market share in 2024. Major banks launched fixed tenures below 9% after derivative hedges reduced funding risk. RBI’s model-risk norms push algorithms toward transparent pricing that favors clearly stipulated rates. Enhanced borrower awareness of interest-cycle effects drives the shift. This dynamic enlarges the India home loan market as cautious consumers re-enter borrowing plans.

Borrowers accept a moderately higher start rate in exchange for EMI certainty, lifting average ticket sizes. Digital calculators now illustrate lifetime savings scenario-wise, nudging conversions. Some lenders explore step-up fixed plans matching career earnings growth. Fintech originators bundle fixed-rate mortgages with top-up options tied to credit-score improvement. The evolving product mix broadens portfolio diversification benefits for the India home loan market.

By Provider Type: NBFCs Challenge Traditional Banking Dominance

Public banks maintain coverage across 60,000 branches, anchoring outreach in rural India. By provider type, public-sector banks held 46.7% revenue share in 2024, whereas NBFCs are anticipated to expand at a 15.54% CAGR through 2030. Yet tech-savvy NBFCs leverage alternate data and cloud underwriting to onboard borrowers within 24 hours. Regulatory harmonization permits banks to extend up to 20% of Tier-I capital to a single well-rated NBFC, improving wholesale liquidity. The partnership model accelerates co-lending, blending low-cost funds with agile risk tools. Consequently, competitive intensity is rising in the India home loan market.

Private banks aim at salaried professionals via premium service propositions, while Housing Finance Companies doubled down on self-employed borrowers. Equity deals, such as EQT’s 2025 purchase of Niwas Housing Finance, inject fresh capital and analytics prowess. Cross-selling of insurance and credit cards boosts fee income, subsidizing lower mortgage spreads. These strategic pivots collectively enlarge credit access and keep margins resilient across the India home loan market.

By Customer Type: Self-Employed Segment Accelerates

Entrepreneurial borrowers historically faced documentation hurdles, yet Account Aggregator rails transform cash-flow visibility. By customer type, salaried borrowers accounted for a 64.7% slice of the India home loan market size in 2024. GST and UPI feed lenders with granular turnover data, letting them gauge income volatility scientifically. Credit policies now grade risk on monthly variance bands rather than static profit statements. Flexible repayment schedules coincide with business seasonality, improving retention metrics. Such innovation fuels double-digit growth from self-employed clients in the India home loan market.

Salaried borrowers remain the revenue anchor because payroll deductions support automated EMI debits. Corporate tie-ups deliver preferential spreads and insurance bundles to retain this base. However, lenders fear saturation in metro salaried cohorts, pushing them outward to micro-enterprise owners. Tech-driven scorecards accelerate approvals where conventional ratio checks once failed. The balanced customer mix diminishes portfolio concentration risk for the India home loan market.

By Interest-Subsidy Scheme Participation: Policy-Driven Growth Momentum

Non-subsidized balances dominate due to rising middle-class incomes and maturing financial literacy. Still, the extended PMAY-CLSS window attracts many first-time buyers by shaving up to 6.5% off loan costs. Digital tracking portals show subsidy credit within four weeks, lifting trust. Banks deploy kiosk staff at municipal offices to educate eligible applicants. Policy certainty, therefore, sustains incremental volumes for the India home loan market.

Middle-income group inclusion expanded scheme limits to Rs 18 lakh slabs, bringing more borrowers under the subsidy. Women account for more than half the beneficiary roll, reinforcing gender-targeted growth. Guarantee cover on government-linked loans lowers risk weightings, freeing capital for fresh disbursals. Some lenders bundle micro-home-improvement loans under the same subsidy umbrella, diversifying revenue streams. The policy architecture thus remains a pivotal growth engine for the India home loan market.

Geography Analysis

The National Capital Region and Mumbai Metropolitan Region captured nearly 40% of new disbursals in 2024, backed by higher per-capita incomes and mature financial ecosystems. Yet escalating land prices in these Tier-1 markets cut affordability, slowing incremental originations. Banks now cap loan-to-value at 75% for high-value properties, managing risk prudently. Developers counter with compact units to keep ticket sizes stable. These pricing dynamics redirect some demand toward adjoining suburbs, sustaining overall momentum in the India home loan market.

Southern hubs such as Bengaluru, Hyderabad, and Chennai exhibit the fastest loan growth; technology employment and metro expansions spur sustained housing demand. Complaint-resolution under RERA, particularly effective in these states, restores buyer confidence and cushions default rates. Eastern cities like Kolkata and Bhubaneswar benefit from industrial corridors and port upgrades that lift household incomes gradually. However, lower formal-sector penetration moderates loan uptake relative to the national average. Strategic branch additions and digital kiosks are bridging this gap for the India home loan market.

Peri-urban belts ringing Tier-2 cities offer significant untapped volume, supported by government capital spending on roads and industrial parks. Mortgage penetration stands at 12% of GDP nationwide, implying ample headroom for formal credit deepening. Unified Lending Interface pilots integrate digitized land records, reducing title-check bottlenecks that plague these corridors. Flood-prone districts along river basins face selective underwriting because climate-risk exclusions tighten insurance availability. Despite such headwinds, sustained infrastructure rollouts are poised to invigorate rural funnels feeding the India home loan market.

Competitive Landscape

Industry structure is moderately concentrated; the top five lenders hold major market share in 2024, yielding intense but manageable rivalry. Public banks exploit sovereign trust and broad distribution to secure government-salary accounts. Private banks focus on digital experiences and bullet repayment features targeting high-income millennials. NBFCs employ alternative credit models to serve thin-file borrowers and Tier-3 geographies, while Housing Finance Companies carve niche specializations in self-constructed dwelling finance. Such diverse strategies collectively broaden borrower choice within the India home loan market.

Analytics adoption differentiates players: HDFC Bank integrated FICO’s cloud platform for real-time credit scoring, cutting approval times by 30% [RBI.ORG.IN]. Several banks pilot satellite-based valuation through partnerships with data-intelligence firms, enabling automated collateral grading. Fintech APIs are tied into Account Aggregator networks to deliver instant documentation fetch, shrinking drop-outs. Co-lending frameworks permit balance-sheet-light origination for small NBFCs, scaling reach without stressing capital ratios. This technological arms race uplift service standards across the India home loan market.

Investor appetite remains robust, as evidenced by a series of strategic deals. In September 2024, Bajaj Housing Finance made waves with a landmark IPO, raising USD 16 billion. The funds are earmarked for technology upgrades and expanding branch networks. Meanwhile, in July 2025, EQT's acquisition of Niwas Housing Finance underscores a growing confidence in niche affordable-housing models. The RBI greenlit Aquilo House's acquisition of Aavas Financiers, signaling a regulatory nod towards consolidations that enhance capital strength. In 2025, TVS Holdings bolstered its mortgage arm by acquiring Home Credit India, introducing new opportunities in consumer durables and potential cross-selling avenues. These moves heighten competition and amplify capital inflows into India's home loan sector.

India Home Loan Industry Leaders

-

State Bank of India

-

HDFC Ltd / HDFC Bank

-

LIC Housing Finance

-

ICICI Bank

-

Axis Bank

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: EQT acquired Niwas Housing Finance to deepen its India footprint and inject data analytics expertise.

- February 2025: RBI cleared Aquilo House’s buyout of Aavas Financiers, advancing consolidation in affordable housing finance.

- February 2025: TVS Holdings finalized the purchase of Home Credit India, broadening its consumer-finance portfolio.

- September 2024: Bajaj Housing Finance raised USD 16 billion in India’s largest housing-finance IPO to date.

India Home Loan Market Report Scope

The home loan market is the financial sector where lenders provide loans to purchase or construct residential properties. It involves borrowing and lending funds to individuals or households seeking financial assistance to buy a house, apartment, or land for residential purposes. India's Home Loan Market is segmented By Customer Type (Salaried, Self-Employed), By Source (Bank and Housing Finance Companies), By Interest Rate (Fixed Rate and Floating Rate), and By Tenure (up to 5 Years, 6 - 10 Years, 11 - 24 Years, and 25 - 30 Years). The report offers market size and forecasts in value (USD) for all the above segments.

| Fixed-Rate Home Loans |

| Floating-Rate Home Loans |

| Public Sector Banks |

| Private Sector Banks |

| Housing Finance Companies (HFCs) |

| Non-Banking Financial Companies (NBFCs) |

| Salaried |

| Self-Employed |

| PMAY-CLSS Beneficiaries |

| Non-Subsidized Loans |

| By Loan Type (Value) | Fixed-Rate Home Loans |

| Floating-Rate Home Loans | |

| By Provider Type (Value) | Public Sector Banks |

| Private Sector Banks | |

| Housing Finance Companies (HFCs) | |

| Non-Banking Financial Companies (NBFCs) | |

| By Customer Type | Salaried |

| Self-Employed | |

| By Interest-Subsidy Scheme Participation (Value) | PMAY-CLSS Beneficiaries |

| Non-Subsidized Loans |

Key Questions Answered in the Report

What is the projected value of the India home loan market by 2030?

The India home loan market size is expected to reach USD 765.73 billion by 2030, reflecting a 15.06% CAGR.

How much did public-sector banks contribute to mortgage originations in 2024?

Public-sector banks held 46.7% of originations, maintaining lead status within the India home loan market.

Why are NBFCs growing faster than traditional banks in housing finance?

NBFCs deploy agile digital underwriting and alternative data to serve underbanked borrowers, driving a 15.54% CAGR through 2030.

Which customer segment is expanding quickest in mortgage borrowing?

Self-employed borrowers are growing at a 16.12% CAGR due to improved cash-flow analytics via Account Aggregators.

What policy continues to boost affordable housing demand?

The Pradhan Mantri Awas Yojana subsidy program, extended through 2027, offers interest subventions up to 6.5%, enhancing affordability.

How do satellite-based valuations benefit lenders?

They automate collateral assessment, cut processing time, and lower field-inspection costs, tightening risk management.

Page last updated on: