Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

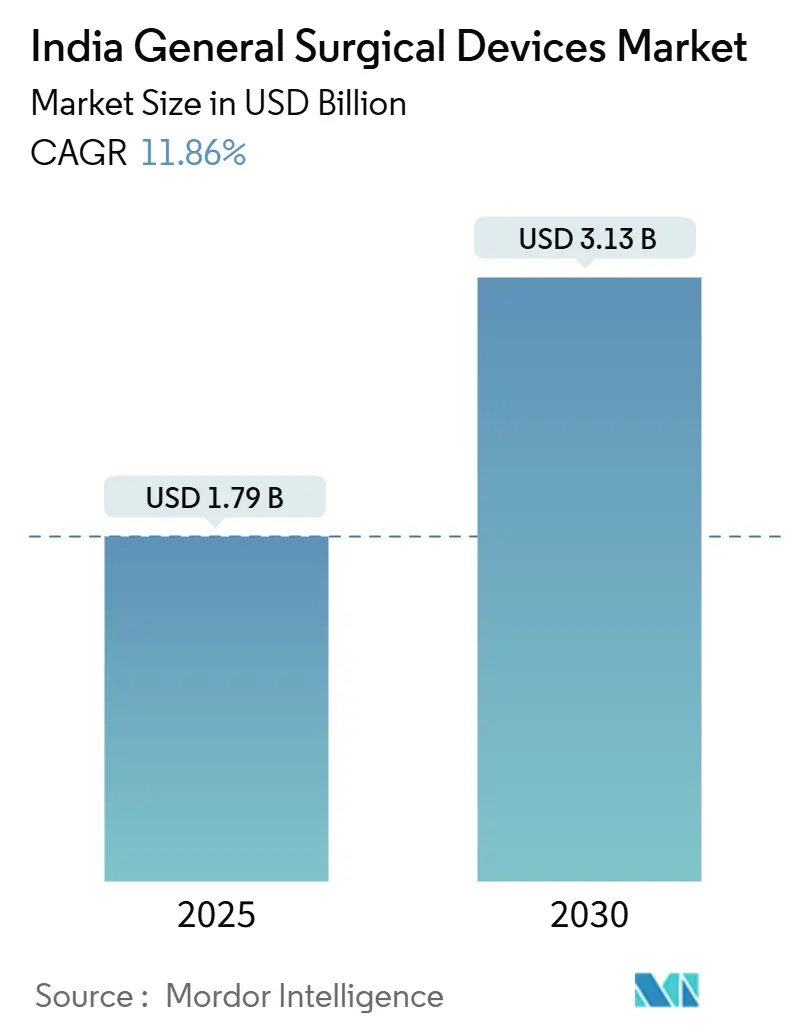

| Market Size (2025) | USD 1.79 Billion |

| Market Size (2030) | USD 3.13 Billion |

| Growth Rate (2025 - 2030) | 11.86% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India General Surgical Devices Market Analysis by Mordor Intelligence

India general surgical devices market size stands at USD 1.79 billion in 2025 and is forecast to reach USD 3.13 billion in 2030, reflecting an 11.86% CAGR during 2025-2030. This solid growth mirrors accelerating healthcare modernization, sustained government incentives, and rising procedure volumes across metropolitan and emerging secondary cities. Demand is amplified by demographic shifts that elevate chronic disease prevalence, the progressive roll-out of universal insurance through Ayushman Bharat, and persistent inflows of international medical travelers. The India general surgical devices market also benefits from steady infrastructure build-out under the Pradhan Mantri Swasthya Suraksha Yojana, while domestic innovation—epitomized by cost-efficient robotic platforms—adds competitive momentum. Simultaneously, import dependence for sophisticated equipment, delayed reimbursements, and foreign-exchange volatility place downward pressure that manufacturers must carefully navigate.

Key Report Takeaways

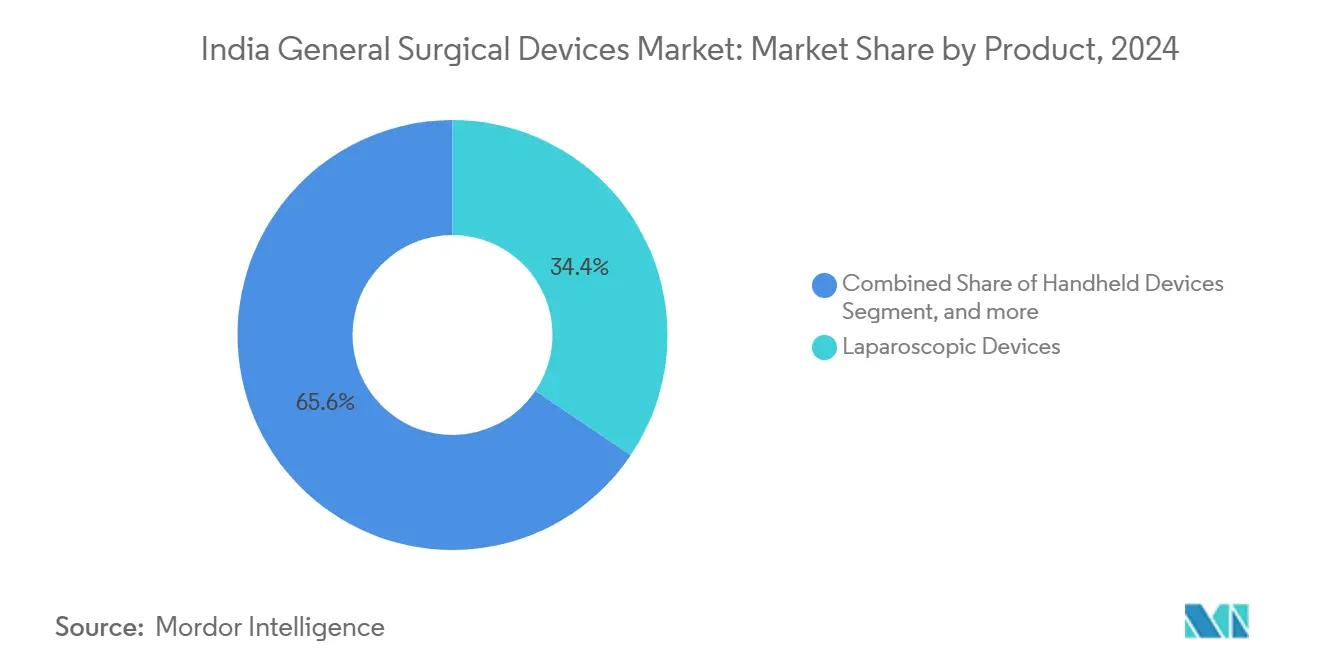

- By product, laparoscopic devices led with 34.54% of India general surgical devices market share in 2024, while electrosurgical devices posted the fastest CAGR at 12.44% through 2030.

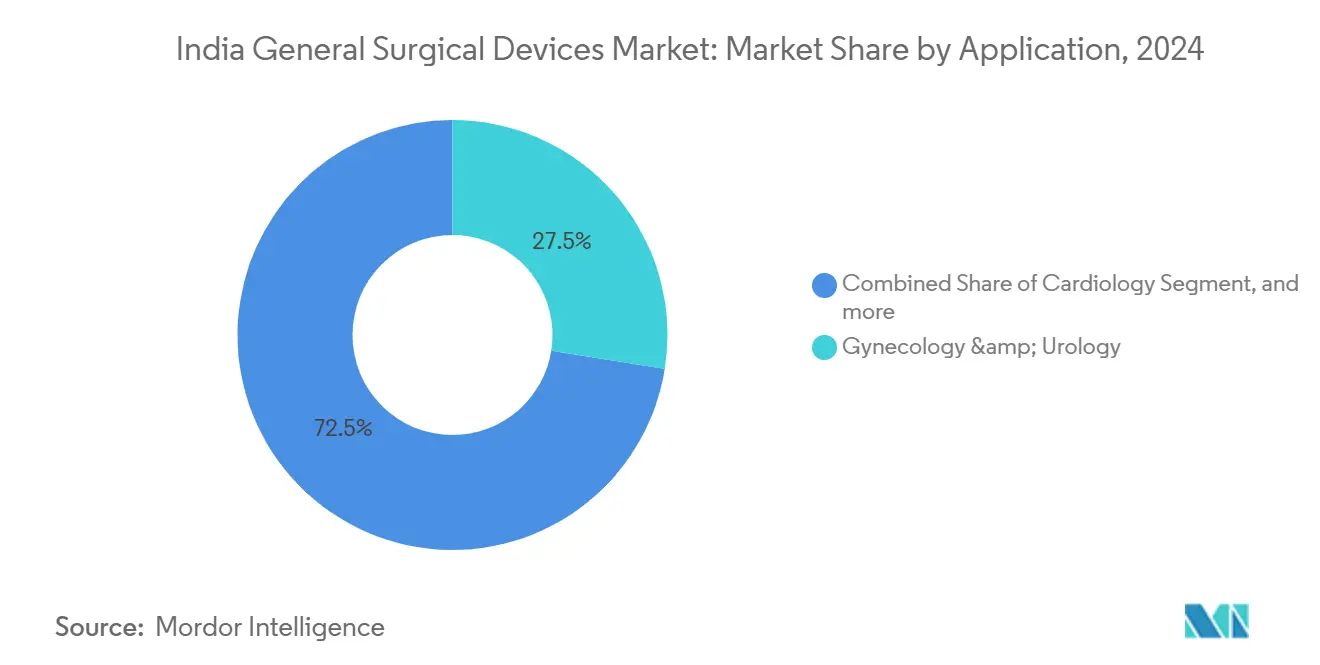

- By application, gynecology and urology held 27.54% of India general surgical devices market size in 2024, yet gastro-intestinal and hepato-biliary procedures are advancing at a 13.21% CAGR through 2030.

India General Surgical Devices Market Trends and Insights

Driver Impact Analysis

| Driver | % (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Minimally-Invasive & Robotic-Assisted Surgeries | +2.5% | National, with early gains in Mumbai, Delhi, Bangalore and Chennai | Medium term (2-4 years) |

| Increasing Incidence of Road-Traffic Injuries | +1.0% | National hotspots along major highway corridors | Short term (≤ 2 years) |

| Growing Burden of Chronic Non-Communicable Diseases | +1.8% | National, higher impact in urban centers and aging demographics | Long term (≥ 4 years) |

| Expansion of Private Tertiary/Day-Care Surgical Centers | +1.4% | Tier-1 cities expanding into Tier-2 clusters | Medium term (2-4 years) |

| Government Ayushman Bharat Insurance Boost | +2.1% | National, stronger impact in rural and semi-urban areas | Short term (≤ 2 years) |

| Surge in Inbound Medical Tourism | +1.2% | Regional, concentrated in Delhi NCR, Mumbai, Chennai and Bangalore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rising Adoption of Minimally Invasive and Robotic-Assisted Surgeries

Hospitals in major metros now routinely deploy robotic or laparoscopic techniques, and indigenous systems are narrowing past cost barriers. Meril’s MISSO robotic knee platform, cleared in June 2024, reports 98% success while cost. The September 2024 debut of the AI-enabled Mizzo Endo 4000 added multi-specialty capability and 5G telesurgery functions that shrink distance constraints. Academic centers such as AIIMS Delhi have installed several da Vinci units, and the Yashoda Group is placing Medtronic’s Hugo system across 25 hospitals, illustrating broad institutional endorsement. Still, a Northeast India audit found only 28% of surgeries that could be laparoscopic actually use the technique, underscoring untapped potential. Expanded training funds and vendor-backed financing are therefore expected to accelerate penetration, especially in secondary cities where demand is rising fastest.

Growing Burden of Chronic Non-Communicable Diseases

Diabetes affects more than 77 million Indian adults, and cardiovascular disorders contribute 28.1% of all deaths, both trends propelling demand for complex surgical interventions. Annual cancer incidence is projected to hit 1.39 million new cases by 2025, pressuring oncology service capacity and driving precision-instrument needs[1]Indian Council of Medical Research, “Projected Cancer Burden in India,” icmr.gov.in. Gastro-intestinal and hepato-biliary surgery volumes expand in tandem, boosted by endoscopic technology diffusion and nascent liver-transplant programs. Parallel demographic aging—19.5% of citizens will be over 60 by 2050—elevates orthopedic, cardiothoracic, and neurology volumes, while younger cohorts sustain elective and tourism-based procedures. PMSSY funding has created 157 new medical colleges since 2014, widening institutional footprints that require full suites of general surgical devices. Rising disposable income and broader insurance cover enable many patients to choose premium implants and energy platforms, stimulating domestic and multinational product launches.

Government Ayushman Bharat Insurance Boost

Ayushman Bharat now shields 550 million beneficiaries across 1,393 defined procedures, sharply lowering out-of-pocket expenses for surgery and raising utilization in district hospitals. The November 2024 inclusion of higher-end procedures instantly widened addressable demand for robotic, energy-based, and advanced closure devices. States such as Chhattisgarh and Himachal Pradesh have rapidly integrated package rates, but Bihar and Jharkhand lag behind, illustrating uneven uptake. Outcome-based reimbursements compel hospitals to modernize operating theaters, especially in tier-2 geographies where government facilities serve as main referral hubs. The standardized coding reduces price sensitivity, allowing surgeons to base purchasing on clinical evidence rather than list cost alone. However, administrative delays still create cash-flow strain for smaller manufacturers, a challenge that persistent policy refinement aims to address.

Surge in Inbound Medical Tourism

Medical travel receipts are projected to reach USD 13 billion in 2025, with cardiovascular, orthopedic, and transplant procedures leading case mix. Comparative cardiac-surgery prices are 60-80% below Western markets yet deliver similar outcomes, cementing India’s value proposition. JCI- and NABH-accredited hospitals maintain global-grade protocols, necessitating recurring investment in premium surgical devices. The multiplier effect covers diagnostics, rehabilitation, and post-operative wound care, widening revenue streams for consumables and capital equipment suppliers. Government initiatives such as the Medical Value Travel framework and streamlined e-medical visas remove bureaucratic friction, sustaining arrivals to Delhi, Mumbai, Chennai, and Bangalore clusters. Device vendors respond by stationing service engineers in high-traffic hubs to guarantee uptime, a measure that bolsters brand loyalty.

Restraints Impact Analysis

| Restraint | % (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Delayed & Inconsistent Reimbursement for Advanced Devices | -1.4% | National, with higher impact in government and semi-urban facilities | Short term (≤ 2 years) |

| NPPA Price-Capping Eroding Margins | -1.1% | National, especially high-value devices in public procurement | Short term (≤ 2 years) |

| Shortage of Trained Laparoscopic Surgeons in Tier-2/3 Cities | -0.8% | Tier-2/3 hospitals and medical colleges | Medium term (2-4 years) |

| High Import Dependence & Forex-Linked Supply Risk | -0.9% | National, affecting all segments with imported components | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Delayed and Inconsistent Reimbursement for Advanced Devices

Hospitals waiting six to twelve months for payment under programs such as CGHS often defer purchases of premium systems, constraining market diffusion[2]Indian Medical Association, “Hospital Reimbursement Challenges,” ima-india.org. Private insurers add to friction through stringent pre-authorizations that delay cases and dampen device usage. Ayushman Bharat sets conservative package rates that may not fully reflect robotic or energy platform costs, compelling hospitals to either subsidize or ration access. Uneven reimbursement rules across states create patchwork demand, with progressive Karnataka routinely funding advanced procedures, while other regions still exclude them. Lacking a unified health technology assessment process, CDSCO and NPPA rely on price ceilings that rarely capture the true value of innovation. Vendors must therefore combine cost-efficient design, financing solutions, and clinical-outcomes dossiers to offset persistent payment uncertainty.

High Import Dependence and Forex-Linked Supply Risk

Roughly 80% of advanced medical equipment remains imported, creating a USD 8.1 billion trade deficit in FY 2023-24[3]Central Drugs Standard Control Organisation, “Advisory on Refurbished Device Imports,” cdsco.gov.in. Any 10% rupee depreciation immediately inflates acquisition prices, straining hospital capital budgets. Pandemic-era logistics disruptions illustrated fragility when ports backlog left surgical staples and electrosurgical generators in short supply nationwide. The January 2025 ban on refurbished device imports, while safeguarding safety, removes a budget option for price-sensitive public hospitals. Domestic innovators such as Meril are narrowing the gap with home-grown robotic systems and cardiovascular implants, but sophisticated energy platforms still rely on overseas supply chains. Technology-transfer restrictions and intellectual property constraints further slow local manufacturing, prolonging exposure to currency swings.

Segment Analysis

By Product: Laparoscopic Leadership Drives Minimally Invasive Adoption

Laparoscopic devices captured 34.54% of India general surgical devices market share in 2024, anchoring demand as surgeons across gynecology, gastroenterology, and general surgery migrate toward minimally invasive practice. Electrosurgical tools are the fastest climber, recording a 12.44% CAGR that outpaces every other category through 2030, a trend tied to shorter operating times and enhanced hemostasis. India general surgical devices market size for these two segments is set to widen rapidly as public hospitals upgrade theaters under PMSSY funding. Disposable trocars, precision sutures, and advanced wound-closure kits add dependable volume, buoyed by infection-control mandates that favor single-use products. Domestic launches such as Meril’s New Edge Suture and high-performance heart valves illustrate how local engineering can substitute imports without sacrificing performance.

Steady demand for handheld basic instruments persists, given their indispensability in every open or minimally invasive procedure, while emerging robotic accessories introduce premium revenue lines. CDSCO’s updated quality classifications heighten compliance costs yet raise buyer confidence, particularly for energy-based platforms. Vendors competing in the India general surgical devices market increasingly bundle service contracts and surgeon training to lock in loyalty. Cross-category synergies are apparent as device makers add imaging integration, navigation aids, or AI analytics, thereby expanding total account value per hospital. Momentum is strongest in tier-2 cities where newly built colleges and private hospitals seek integrated solutions rather than piecemeal purchases, indicating a shift toward platform-oriented procurement.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Gynecology Dominance Meets GI Growth Potential

Gynecology and urology procedures maintained 27.54% of India general surgical devices market size in 2024, propelled by high birth rates, women’s-health awareness programs, and expanded cancer-screening coverage. Device volumes span laparoscopes, morcellators, staplers, and energy sources, making the segment a stable base for vendors. However, gastro-intestinal and hepato-biliary applications exhibit a 13.21% CAGR that positions them as the next growth frontier, supported by rising liver-disease incidence, endoscopy diffusion, and burgeoning transplant programs. India general surgical devices market share in GI specialties will therefore expand as metropolitan centers add dedicated hepatobiliary units and as medical tourists seek complex yet affordable care.

Cardiology surgeries remain a sizable but steady contributor, with valve replacements and off-pump coronary systems benefiting from domestic production strides. Orthopedic interventions gain traction among both senior citizens and younger athletic populations, increasing demand for arthroscopy towers and powered tools. Neurosurgical volumes grow in tertiary centers equipped with intra-operative imaging and precision microscopes, although overall share stays modest due to limited specialist pools. Plastic, ENT, and emerging subspecialties round out the long-tail of procedures that collectively ensure baseline demand for general-purpose devices and consumables. Application diversity thus buffers the India general surgical devices market against cyclical swings in any single clinical area.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

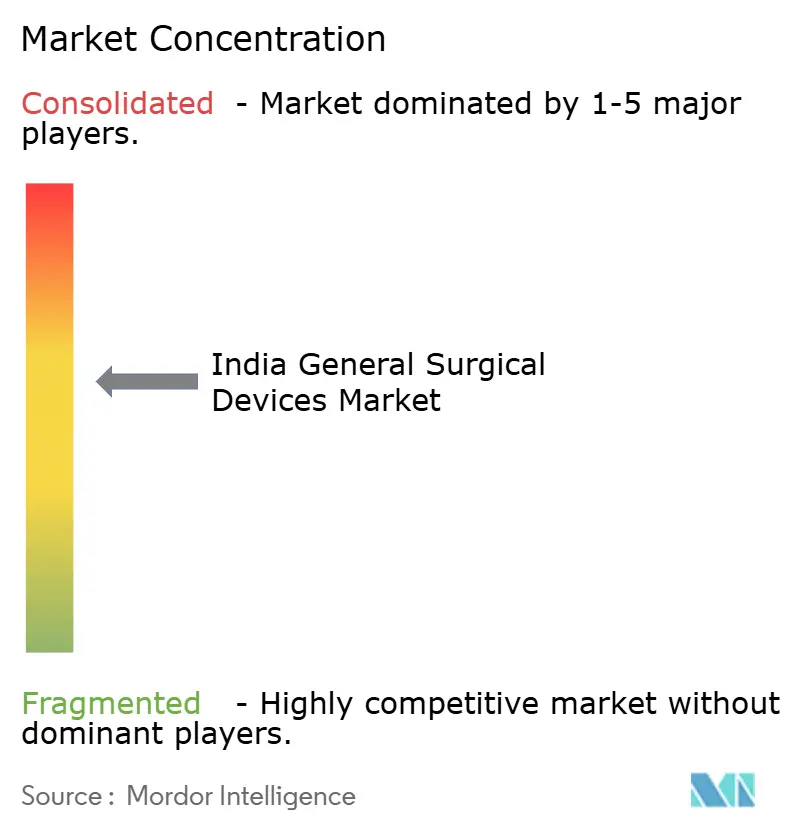

Competitive Landscape

Private-equity inflows crossed USD 1.2 billion by August 2024, epitomized by KKR’s USD 840 million acquisition of Healthium Medtech, the global leader in surgical needles. The transaction underscores confidence in the India general surgical devices market and signals likely follow-on consolidation. Multinationals such as Johnson & Johnson (Ethicon), Medtronic, and Boston Scientific still command sizable revenue through comprehensive catalogs and entrenched surgeon relationships. Domestic champions like Meril Life Sciences and Poly Medi¬cure steadily gain ground by coupling cost advantages with home-grown innovation, especially in cardiac and robotic niches.

Technology leadership is the new battleground. Medtronic’s INR 3,000 crore R&D expansion in Hyderabad courts engineers to localize next-gen platforms while compressing design-to-launch timelines. Meril’s MISSO and Mizzo robots validate indigenous capability and pressure imported price points. Distribution revamp is another theme; vendors extend service depots into tier-2 corridors, deploy digital inventory tracking, and roll out surgeon-education academies. Ethical compliance also differentiates competitors following the 2024 Uniform Code for Marketing Practices of Medical Devices, which rewards transparent promotions and evidence-based detailing.

Market fragmentation remains moderate. The top five vendors collectively hold roughly 48% revenue, creating sufficient headroom for mid-tier entrants specializing in consumables or niche subspecialties. Partnerships between multinationals and local fabricators accelerate time-to-market for implants and energy probes tailored to Indian clinical settings, as illustrated by the Alkem-Exactech joint venture. Companies that balance quality, affordability, and regulatory stewardship are therefore best positioned to capture incremental shares as procedure volumes climb.

India General Surgical Devices Industry Leaders

-

Conmed Corporation

-

Boston Scientific Corporation

-

Johnson & Johnson

-

B. Braun SE

-

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: CDSCO suspended imports of used and refurbished medical devices to enhance patient safety and encourage hospitals to procure new equipment.

- November 2024: Government unveiled a Rs 500 crore scheme to strengthen domestic medical-device manufacturing, R&D, and exports

- September 2024: Meril Life Sciences introduced the Mizzo Endo 4000 soft-tissue robotic system with AI guidance and 5G telesurgery

- September 2024: United States-based Stryker, a global leader in medical technologies, unveiled its pioneering 1788 Advanced Imaging Platform in India. The 1788 platform stands as Stryker's most advanced and all-encompassing surgical visualization system to date. Tailored for diverse specialties, it equips surgeons with superior imaging capabilities, ultimately aiming for better patient outcomes. Stryker's 1788 platform stands as its most advanced and comprehensive surgical visualization system to date.

- June 2024: the World Laparoscopy Hospital (WLH) in Gurgaon conducted the nation's inaugural remote robotic telesurgery, utilizing the advanced Mantra Robot. This milestone not only highlights India's leading role in medical innovation but also signifies a pivotal shift in the worldwide medical arena.

India General Surgical Devices Market Report Scope

According to the report's scope, general surgical devices are specifically designed instruments that are clinically and accurately produced to assist surgeons during surgeries.

The India general surgical devices market is segmented by product (handheld devices, laparoscopic devices, electrosurgical devices, wound-closure devices, trocars & access devices, other products), application (gynecology & urology, cardiology, orthopedic, neurology, gastro-intestinal & hepato-biliary, other applications). The report offers the value (in USD million) for the above segments.

By Product

| Handheld Devices |

| Laparoscopic Devices |

| Electrosurgical Devices |

| Wound-Closure Devices |

| Trocars & Access Devices |

| Other Products |

By Application

| Gynecology & Urology |

| Cardiology |

| Orthopedic |

| Neurology |

| Gastro-intestinal & Hepato-biliary |

| Other Applications |

| By Product | Handheld Devices |

| Laparoscopic Devices | |

| Electrosurgical Devices | |

| Wound-Closure Devices | |

| Trocars & Access Devices | |

| Other Products | |

| By Application | Gynecology & Urology |

| Cardiology | |

| Orthopedic | |

| Neurology | |

| Gastro-intestinal & Hepato-biliary | |

| Other Applications |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the India general surgical devices market?

The market is valued at USD 1.79 billion in 2025 and is projected to reach USD 3.13 billion by 2030 at an 11.86% CAGR.

Which product segment holds the largest share in IndiaÕs surgical devices space?

Laparoscopic equipment leads with 34.54% share, driven by widespread adoption of minimally invasive techniques.

Which application area is expanding the fastest in IndiaÕs surgical device landscape?

Gastro-intestinal and hepato-biliary surgery shows the highest growth, advancing at a 13.21% CAGR through 2030.

How is Ayushman Bharat influencing surgical device demand?

The scheme covers 550 million citizens and 1,393 procedures, lowering out-of-pocket costs and encouraging hospitals to acquire advanced devices.

What are the primary challenges for device manufacturers in India?

Key hurdles include reimbursement delays, high import dependence, and currency-linked cost volatility.

Which regions offer the most untapped potential for surgical device suppliers?

Tier-2 and tier-3 cities represent the fastest-growing opportunity, supported by new medical colleges and higher insurance penetration.

Page last updated on: