| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 18.41 Billion |

| Market Size (2030) | USD 24.39 Billion |

| CAGR (2025 - 2030) | 5.79 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Indian Defense Market Overview

The India Defense Market size is estimated at USD 18.41 billion in 2025, and is expected to reach USD 24.39 billion by 2030, at a CAGR of 5.79% during the forecast period (2025-2030).

India's defense industry has emerged as a cornerstone of national security and economic development, reflecting the country's growing strategic importance in the Indo-Pacific region. According to the Stockholm International Peace Research Institute (SIPRI) report 2022, India maintained its position as the world's fourth-largest defense spender with an expenditure of USD 81.4 billion, highlighting the nation's commitment to military modernization. The sector has witnessed a significant transformation through the implementation of various policy reforms aimed at promoting indigenous defense manufacturing and reducing import dependencies. The government's strategic focus on self-reliance has led to the establishment of robust domestic manufacturing capabilities, with defense exports reaching unprecedented levels as India now exports to more than 75 countries globally.

The landscape of India's defense industry has been fundamentally reshaped by the emphasis on indigenous production and technological innovation. For the fiscal year 2023-24, the government has allocated USD 19.64 billion specifically for the procurement of new weapons and platforms, demonstrating its commitment to defense modernization. This substantial investment is complemented by a planned investment of USD 2.79 billion in defense technology research and development to promote "Atmanirbhar Bharat" (self-reliant India) initiatives. These investments have catalyzed the development of a robust domestic defense industrial base, encouraging partnerships between public and private sector entities.

The market has witnessed a significant shift towards strategic partnerships and technology transfer agreements with global defense manufacturers. In 2023, several notable collaborations have emerged, including the partnership between Thales and Bharat Dynamics Limited for manufacturing precision-strike laser-guided rockets, representing a major step towards indigenous production capabilities. The industry has also seen increased participation from private sector players, with companies like Adani Defense and Aerospace, Kalyani Strategic Systems, and Tata Advanced Systems expanding their defense manufacturing portfolios through various joint ventures and technology transfer agreements.

The sector's transformation is further evidenced by the growing focus on advanced military technology integration and export potential. Indian defense manufacturers have made substantial progress in developing sophisticated systems across various domains, including aerospace & defense, land systems, and naval platforms. The government's emphasis on modernization has led to increased investments in emerging technologies such as artificial intelligence, unmanned systems, and cybersecurity. This technological advancement has been supported by policy initiatives that encourage foreign direct investment and promote ease of doing business in the defense sector, creating a more conducive environment for both domestic and international players to participate in India's defense market growth.

Indian Defense Market Trends

Increased Defense Budget

India's defense sector has witnessed substantial financial commitment from the government, demonstrated by the significant defense budget of USD 81.4 billion in 2022, marking a 7% increase from the previous year. The government's long-term commitment is further evidenced by its plan to spend USD 130 billion by 2030 on programs for Indian Armed Forces fleet modernization. This increased budgetary allocation has been strategically directed toward indigenous manufacturing, with the Ministry of Defense allocating 75% of the defense capital budget for the domestic industry in 2023-2024, representing a 12% increase from 2021-2022.

The enhanced defense budget has catalyzed several indigenous development initiatives, fostering a robust domestic defense manufacturing ecosystem. The government has set aside USD 19.64 billion specifically for purchasing new military equipment and platforms for 2023-2024, while simultaneously investing USD 2.79 billion in defense technology research and development to promote "Atmanirbhar Bharat" indigenous manufacturing. This financial commitment has already shown tangible results, with capital imported acquisition from foreign countries increasing by 7.2% between 2011-12 and 2020-21, while acquisition from indigenous sources demonstrated stronger growth at 9.7% for the same period, reflecting the success of domestic procurement initiatives.

Understand The Key Trends Shaping This Market

Download PDF

Technological Advancements and Modernization

India's defense sector is undergoing rapid technological transformation, marked by significant advancements in indigenous capabilities and modernization initiatives across all military branches. The development of the Advanced Medium Combat Aircraft (AMCA) project, with its first flight expected between 2025-2026 and full production targeted by 2030, exemplifies India's push toward advanced military technology. This technological evolution is further demonstrated by Hindustan Aeronautics Limited's announcement in February 2023 regarding the development of a new 13-ton-class helicopter for the Indian Armed Forces, potentially marking the most extensive helicopter design program attempted by India.

The modernization drive extends across various defense platforms, with notable developments in naval capabilities and aircraft systems. The Indian Navy's announcement in November 2023 regarding the construction of approximately 67 ships under the Make in India initiative highlights the scale of modernization efforts. The commissioning of INS Sandhayak in February 2024, equipped with advanced hydrographic survey capabilities, demonstrates India's commitment to incorporating cutting-edge defense technology in its naval fleet. Additionally, the development of the Tejas Mk 2 initiated in 2023, with series production planned for 2026, along with the pursuit of the Medium Multi-role Combat Aircraft (MMRCA) 2.0 deal worth an estimated USD 18-20 billion, underscores the comprehensive nature of India's military modernization program. This includes significant investments in military aviation and military weapons to enhance the country's defense capabilities.

Segment Analysis: By Ammunition

Large Ammunition Segment in India Defense Market

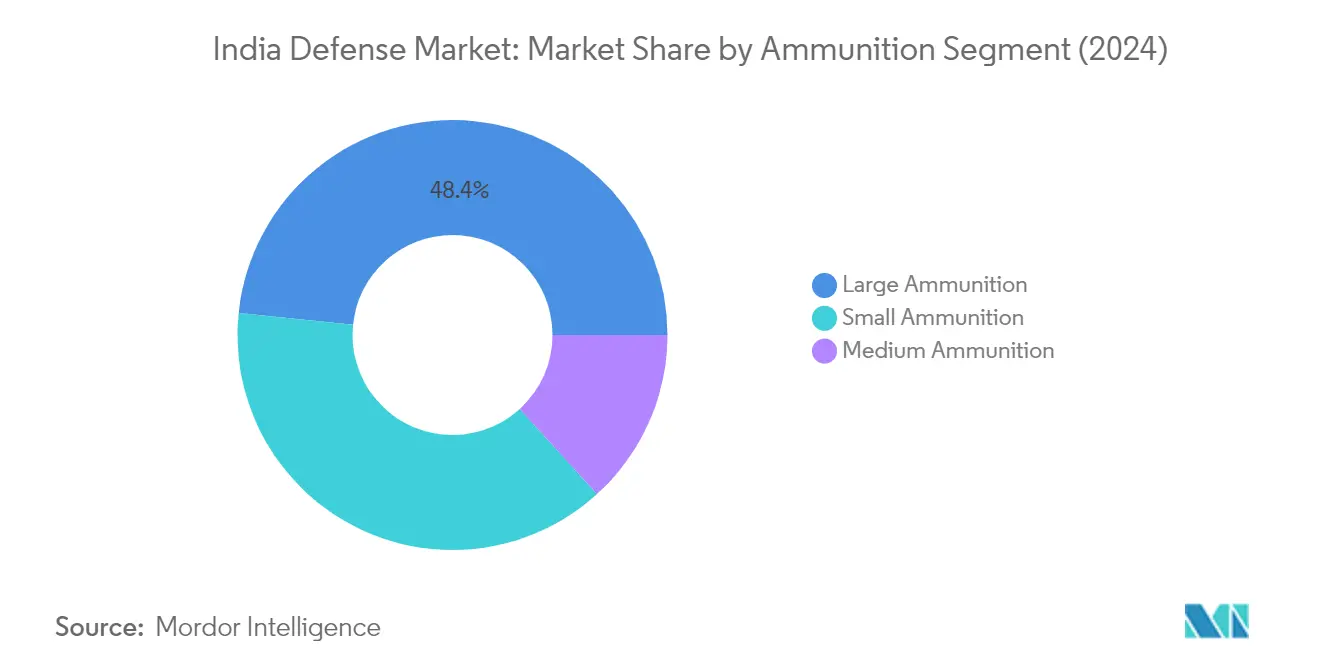

The large ammunition segment continues to dominate the Indian defense market, commanding approximately 48% of the market share in 2024. This segment's prominence is primarily driven by its crucial role in artillery and military weapons applications, particularly in addressing India's strategic defense needs along its borders. The segment encompasses both mortar and artillery ammunition, with artillery shells constituting the vast majority of large-caliber ammunition production. The Indian military's focus on modernizing its artillery capabilities, coupled with the continuous need for replenishment of large-caliber ammunition stockpiles, has maintained this segment's market leadership. The domestic manufacturing capabilities for large ammunition have significantly improved, with several Indian companies now producing world-class artillery ammunition systems.

Small Ammunition Segment in India Defense Market

The small ammunition segment is projected to exhibit the highest growth rate of approximately 5% during the forecast period 2024-2029. This accelerated growth is attributed to increasing demand for small arms ammunition across various military equipment applications, ongoing modernization efforts of the Indian armed forces, and the segment's adaptability to varied military scenarios. The growth is further supported by technological advancements in ammunition manufacturing, including improved precision, reliability, and performance characteristics. The Indian government's push for indigenous production under the 'Make in India' initiative has led to increased investments in small arms ammunition manufacturing facilities, contributing to the segment's robust growth trajectory.

Remaining Segments in Ammunition Market

The medium ammunition segment, including grenades and related ammunition types, plays a vital role in bridging the gap between small arms and large artillery requirements. This segment serves crucial tactical requirements for the Indian military, particularly in close combat situations and specialized operations. The segment has witnessed significant technological advancements in terms of precision, effectiveness, and versatility, making it an essential component of India's defense capabilities. The development of advanced medium-caliber ammunition systems has enhanced the Indian military's operational flexibility and combat effectiveness across various tactical scenarios.

Segment Analysis: By Ammunition Application

Lethal Ammunition Segment in India Defense Market

The lethal ammunition segment dominates the Indian defense ammunition market, commanding approximately 80% market share in 2024, while also exhibiting the strongest growth trajectory. This segment's prominence is driven by its vital role in safeguarding India's borders, particularly in conflict-prone regions like Jammu and Kashmir. The segment's growth is further bolstered by India's increasing expertise in lethal ammunition production, which has created significant export opportunities for the domestic industry. The development of advanced ammunition types, including specialized rounds for counter-terrorism operations and precision strikes, continues to drive market expansion. Modern lethal ammunition systems incorporate sophisticated technologies for enhanced accuracy and effectiveness, meeting the evolving requirements of India's armed forces. The segment has witnessed substantial technological advancements, particularly in areas such as smart ammunition and guided projectiles, which provide superior targeting capabilities and reduced collateral damage.

Non-lethal Ammunition Segment in India Defense Market

The non-lethal ammunition segment plays a crucial complementary role in India's defense arsenal, focusing on crowd control, training scenarios, and specialized military applications. This segment encompasses various products including rubber bullets, tear gas, and other riot control munitions that are essential for maintaining public order while minimizing casualties. The Indian military and law enforcement agencies increasingly rely on non-lethal ammunition for training purposes, helping personnel prepare for real-world scenarios in a controlled environment. The segment has seen notable innovations in terms of effectiveness and safety features, with manufacturers developing new compounds and delivery systems that maximize deterrence while minimizing potential harm. Border security operations, particularly along the Indo-Bangladesh border, have incorporated non-lethal ammunition as a crucial component of their security protocol, demonstrating the segment's strategic importance in modern military operations.

Segment Analysis: By Other Armaments

Rockets Segment in India Defense Market

The rockets segment dominates the other armaments category in India's defense market, commanding approximately 97% market share in 2024. This substantial market presence is primarily driven by the increasing deployment of rocket systems for military operations and strategic defense capabilities. The Indian military's focus on modernizing its rocket artillery systems, including multi-barrel rocket launchers and precision-guided systems, has significantly contributed to this segment's dominance. The development and procurement of advanced rocket systems like Pinaka and other indigenous platforms have further strengthened this segment's position. Additionally, the emphasis on domestic manufacturing capabilities and the integration of modern technologies in rocket systems have enhanced India's self-reliance in this crucial defense segment. The segment's growth is also supported by ongoing military modernization programs and the increasing focus on precision strike capabilities.

Explosives Segment in India Defense Market

The explosives segment is projected to exhibit the strongest growth among other armaments during the forecast period 2024-2029, with an expected growth rate of approximately 2%. This growth trajectory is driven by increasing investments in indigenous explosive manufacturing capabilities and the rising demand for advanced explosive materials in military applications. The segment's expansion is further supported by technological advancements in explosive manufacturing processes and the development of new-generation explosive compounds with enhanced safety features and performance characteristics. The focus on research and development in this sector, particularly in developing specialized explosives for various military applications, continues to drive innovation and market growth. The segment also benefits from increasing defense collaboration agreements and technology transfer partnerships with international players, enabling access to advanced explosive manufacturing technologies and expertise.

Remaining Segments in Other Armaments

The bombs and mines segments complete the other armaments category in India's defense market, each playing crucial roles in the country's defense capabilities. The bombs segment encompasses various types of aerial munitions and precision-guided weapons, contributing to India's air strike capabilities and strategic deterrence. The development of indigenous bomb manufacturing capabilities and integration of smart technologies has enhanced this segment's significance. The mines segment, while smaller in market share, remains important for territorial defense and area denial strategies. Both segments continue to evolve with technological advancements, focusing on improved precision, reliability, and safety features while adhering to international protocols and regulations governing these weapons systems.

Segment Analysis: By Uniform

Military Uniform Segment in India Defense Market

Military uniforms represent the largest segment in India's defense uniform market, commanding approximately 48% market share in 2024. This dominant position stems from the segment's comprehensive coverage of various uniform types including duty wear, off-duty attire, sports uniforms, and formal occasion wear for the Indian armed forces. The segment's strength is reinforced by the continuous need to equip India's large military force with standardized, high-quality uniforms that meet specific requirements for different operational environments and ceremonial purposes. The military uniform segment encompasses both traditional service dress and modern combat attire, with recent developments focusing on incorporating advanced materials for enhanced durability and comfort. The segment's leadership is further supported by ongoing modernization initiatives in the Indian defense sector, with manufacturers emphasizing the development of uniforms that can withstand diverse climatic conditions while maintaining professional appearance and functionality.

Combat Uniforms Segment in India Defense Market

The combat uniforms segment is projected to exhibit the highest growth rate of approximately 3% during the forecast period 2024-2029, driven by increasing emphasis on specialized combat gear and technological advancements in fabric development. This growth trajectory is supported by the Indian military's focus on modernizing combat wear with enhanced features for different operational environments. The segment's expansion is further fueled by innovations in material science, leading to the development of combat uniforms with improved durability, comfort, and protective capabilities. Manufacturers are incorporating advanced features such as better camouflage patterns, enhanced moisture-wicking properties, and improved thermal regulation systems. The segment's growth is also bolstered by increasing investments in research and development for creating combat uniforms that can better withstand extreme weather conditions while providing optimal mobility and protection to military personnel.

Remaining Segments in By Uniform

The remaining segments in the uniform market include special suits, coveralls, and pressure suits, each serving specific operational requirements of the Indian defense forces. Special suits are designed for specialized operations and hazardous environments, incorporating features like HAZMAT protection and reflective capabilities. Coveralls serve as essential protective gear for maintenance and technical personnel, offering comprehensive body coverage during various military operations. Pressure suits, while representing a smaller portion of the market, play a crucial role in aviation and high-altitude operations, providing necessary protection for pilots and aircrew. These segments collectively contribute to the comprehensive range of uniform solutions required by modern military forces, with each category addressing specific operational needs and safety requirements.

Segment Analysis: By Uniform Accessories

Shoes and Boots Segment in India Defense Uniform Accessories Market

The shoes and boots segment maintains its dominant position in India's defense uniform accessories market, commanding approximately 50% market share in 2024. This significant market presence is attributed to the segment's crucial role in ensuring operational effectiveness and personnel safety across diverse terrains and combat conditions. The Indian military's focus on modernizing footwear specifications to enhance durability, comfort, and protection has further strengthened this segment's market position. Military boots and shoes are being designed with advanced materials and technologies to provide superior ankle support, water resistance, and protection against extreme weather conditions. The segment's growth is also driven by the increasing emphasis on specialized footwear for different operational environments, including desert warfare, mountain warfare, and jungle operations.

Paddings Segment in India Defense Uniform Accessories Market

The paddings segment is projected to exhibit the strongest growth trajectory with an anticipated CAGR of approximately 2% during 2024-2029. This growth is primarily driven by the increasing focus on soldier protection and comfort in various operational environments. The segment is witnessing significant technological advancements in materials and design, incorporating innovative shock-absorption technologies and lightweight yet durable materials. The development of advanced padding solutions for tactical vests, helmets, and other protective gear is enhancing soldier mobility while maintaining optimal protection levels. The segment's growth is further supported by the increasing adoption of ergonomically designed padding systems that distribute weight more effectively and reduce soldier fatigue during extended operations.

Remaining Segments in Uniform Accessories Market

The other significant segments in the uniform accessories market include helmets, belts, gloves, and various supplementary accessories. The helmets segment plays a crucial role in providing essential head protection and has seen considerable technological advancement in terms of materials and design. The belts segment continues to evolve with the integration of modular designs that support various equipment carrying configurations. The gloves segment has gained importance due to the increasing focus on tactical operations requiring both protection and dexterity. These segments collectively contribute to the comprehensive modernization of military uniform accessories, with each component designed to enhance soldier effectiveness and safety in various operational scenarios.

Segment Analysis: By Body Armor

Soft and Hard Armors Segment in India Defense Market

The soft and hard armors segment dominates the Indian defense body armor market, commanding approximately 70% of the market share in 2024. This segment's prominence is attributed to its comprehensive coverage of body armor needs and ability to balance protection with flexibility for military and law enforcement personnel. The segment incorporates advanced materials offering superior protection while maintaining mobility, making it essential for modern combat scenarios. The integration of cutting-edge technologies and materials like ultra-high molecular weight polyethylene and advanced ceramic composites has enhanced the segment's capabilities. The segment is experiencing the highest growth rate of around 3% for the forecast period 2024-2029, driven by continuous advancements in armor technology, increasing adoption of advanced body armor systems, and evolving security challenges. The growth is further supported by India's focus on modernizing its armed forces and enhancing soldier survivability through improved protection systems.

Remaining Segments in Body Armor

The other segments in the body armor market include clothing, helmets, and accessories, each serving crucial roles in providing comprehensive protection solutions. The helmets segment represents a significant portion of the market, offering essential head protection with advanced materials and integrated systems for enhanced situational awareness. The clothing segment focuses on specialized protective garments designed for various operational environments and threat levels, incorporating advanced fabrics and protective materials. The accessories segment, while smaller in market share, plays a vital role in completing the protective ensemble with components like tactical vests, plate carriers, and modular attachment systems. These segments collectively contribute to a comprehensive body armor ecosystem, with manufacturers continuously innovating to improve protection levels, comfort, and operational effectiveness while meeting the specific requirements of different military and law enforcement units.

Segment Analysis: By Body Armor Protection

Above NIJ 3 Segment in India Defense Body Armor Protection Market

The Above NIJ 3 segment dominates the Indian defense body armor protection market, commanding approximately 96% of the market share in 2024. This overwhelming market dominance can be attributed to the increasing emphasis on enhanced protection capabilities for military personnel operating in high-threat environments. The segment's growth is driven by continuous technological advancements in materials and manufacturing processes, enabling the development of lighter yet more effective armor solutions. The Indian military's focus on modernizing its protective equipment, particularly for special forces and frontline troops, has further strengthened this segment's position. The segment is also witnessing significant developments in terms of integration with other protective systems and enhanced mobility features. Additionally, the increasing adoption of multi-hit protection capabilities and the development of armor systems that can withstand high-velocity ammunition have contributed to its market leadership. The segment is expected to maintain its strong growth trajectory with a compound annual growth rate of approximately 3% from 2024 to 2029, driven by ongoing military modernization programs and increasing focus on soldier survivability.

Below NIJ 3 Segment in India Defense Body Armor Protection Market

The Below NIJ 3 segment, while smaller in market share, plays a crucial role in meeting specific tactical requirements where lighter protection is needed. This segment caters to scenarios requiring enhanced mobility and flexibility, particularly in urban operations and low-intensity conflict situations. The segment has seen notable developments in terms of improved comfort features, better heat dissipation capabilities, and enhanced ergonomic designs. Manufacturers in this segment are focusing on developing innovative solutions that balance protection levels with user comfort and mobility. The integration of advanced materials and manufacturing techniques has enabled the production of armor solutions that offer adequate protection while maintaining optimal weight characteristics. The segment also serves specialized units requiring discrete protection capabilities, such as VIP protection teams and reconnaissance units. The development of hybrid protection solutions combining different materials and protection levels has further enhanced the segment's relevance in specific operational scenarios. Additionally, the segment has benefited from advancements in flexible armor technologies and the increasing demand for concealed protection solutions.

Segment Analysis: By Military Parachute

Round Parachute Segment in India Defense Market

Round parachutes continue to dominate the Indian military parachute market, commanding approximately 61% market share in 2024, primarily due to their proven reliability and versatile applications. These parachutes are extensively utilized by the Indian defense forces for various missions including personnel drops, cargo delivery, and training exercises. The round canopy design makes them more dependable than other shapes, creating symmetrical airflow that enhances stability and prevents unwanted spinning during descent. Their straightforward design also contributes to easier maintenance and repair procedures, making them a cost-effective choice for military applications. The Indian defense forces prefer round parachutes for their robust construction and ability to operate effectively across diverse geographical conditions, from high-altitude regions to coastal areas. Additionally, domestic manufacturers have developed advanced materials and technologies to enhance the performance characteristics of round parachutes, including improved descent control and landing accuracy.

Other Parachute Segments in India Defense Market

The "Others" category, which includes aircraft brake parachutes and backup parachutes, is projected to experience the highest growth rate of approximately 7% during the forecast period 2024-2029. This growth is primarily driven by increasing emphasis on aircraft safety systems and the modernization of India's air force fleet. The segment's expansion is further supported by technological advancements in materials and design, particularly in developing sophisticated brake parachute systems for advanced fighter aircraft. The Indian defense forces are increasingly investing in backup parachute systems as part of their safety protocols, recognizing their critical role in emergency scenarios. Manufacturers are focusing on developing lightweight yet durable materials for these specialized parachutes, incorporating advanced features such as automated deployment systems and enhanced reliability mechanisms. The segment is also benefiting from increased research and development activities in aerodynamic designs and smart materials, leading to more efficient and reliable parachute systems.

Remaining Segments in Military Parachute Market

The cruciform and ram air parachutes represent significant segments in India's military parachute market, each serving distinct operational requirements. Cruciform parachutes are valued for their enhanced stability and reduced oscillation characteristics, making them particularly effective for precision cargo drops and specialized military operations. These parachutes feature a unique cross-shaped design that provides better control and predictability during descent. Meanwhile, ram air parachutes have gained prominence in special forces operations due to their superior maneuverability and glide capabilities. Their advanced aerodynamic design allows for greater control over direction and speed, making them ideal for tactical insertions and covert operations. Both segments continue to evolve with technological advancements, incorporating modern materials and design improvements to enhance their performance capabilities and meet the evolving requirements of India's armed forces.

Segment Analysis: By Military Parachute Application

Troops Segment in India Defense Market

The troops segment maintains its dominant position in India's military parachute application market, commanding approximately 52% market share in 2024. This substantial market presence is driven by the critical role of parachute systems in tactical military operations, particularly in strategic and surprise deployments. The segment's strength is underpinned by the Indian Air Force's extensive utilization of Parachute Tactical Assault-Main (PTA-M) systems, which are advanced personnel parachute systems designed for deployment from various aircraft platforms including AN-32 and C-130. These systems incorporate sophisticated features such as anti-inversion nets, air scoops, and mesh-covered stability slots, ensuring reliable flight performance and smooth opening characteristics. The segment's robustness is further reinforced by the manufacturing focus on using advanced materials like "Ripstop" nylon, specifically engineered with double or extra-thick threading at regular intervals to prevent tearing during flight operations.

Cargo Segment in India Defense Market

The cargo segment is projected to exhibit the strongest growth trajectory with an anticipated CAGR of approximately 6% during the forecast period 2024-2029. This accelerated growth is primarily attributed to the increasing need for efficient aerial delivery systems capable of transporting military supplies, ammunition, and vehicles to various drop zones, particularly in challenging terrains lacking ground transport infrastructure. The segment's expansion is further supported by significant technological advancements in heavy drop systems and the development of more durable cargo parachutes. The growth momentum is reinforced by the successful implementation of indigenous manufacturing capabilities, exemplified by the Type V Heavy Drop System, which enables the transportation of payloads up to 20 tons. Additionally, the development of the P-7 Heavy Drop Parachute System, capable of para-dropping military stores up to 7-ton weight class, demonstrates the segment's technological evolution and increasing sophistication in meeting complex military logistics requirements.

Remaining Segments in Military Parachute Application

The emergency parachute segment plays a vital complementary role in India's defense market, focusing on providing critical safety systems for military aircraft and personnel during emergency situations. This segment encompasses various specialized applications, including emergency evacuation systems for fighter aircraft and backup parachute systems for airborne operations. The segment's importance is highlighted by its integration into modern fighter aircraft systems and its crucial role in ensuring pilot safety during aircraft malfunctions. The development of advanced ejection seat parachute systems and backup parachute technologies continues to enhance the segment's significance in military operations, particularly in high-risk combat scenarios and training missions. The segment's evolution is characterized by continuous improvements in reliability, deployment speed, and overall safety features, making it an indispensable component of India's military parachute applications.

Segment Analysis: By EO/IR Systems

Air-based Segment in Indian Defense EO/IR Systems Market

The air-based segment continues to dominate the Indian defense EO/IR systems market, commanding approximately 53% market share in 2024. This significant market position is primarily driven by the extensive deployment of EO/IR systems in military aircraft, unmanned aerial vehicles (UAVs), and helicopters for intelligence, surveillance, reconnaissance (ISR), and combat missions. The segment's prominence is further reinforced by India's increasing focus on modernizing its air force capabilities through the integration of advanced EO/IR sensors in various airborne platforms. The growing emphasis on enhancing aerial surveillance capabilities, particularly along border regions, has led to substantial investments in sophisticated airborne EO/IR systems. These systems provide critical capabilities such as long-range imaging, target identification, and tracking in various weather conditions, making them indispensable for modern military operations.

Land-based Segment in Indian Defense EO/IR Systems Market

The land-based segment is projected to exhibit the highest growth rate of approximately 4% during the forecast period 2024-2029, driven by increasing investments in ground-based surveillance and security systems. This growth trajectory is supported by India's focus on strengthening its border security infrastructure and modernizing its ground forces with advanced EO/IR capabilities. The segment's expansion is further fueled by the integration of sophisticated EO/IR systems in armored vehicles, mobile surveillance units, and stationary observation posts. The development of advanced man-portable EO/IR devices and their increasing adoption by infantry units has created additional growth opportunities. The segment is also benefiting from technological advancements in thermal imaging, night vision capabilities, and target acquisition systems, which are essential for modern ground warfare operations.

Remaining Segments in EO/IR Systems Market

The sea-based segment represents a crucial component of the Indian defense EO/IR systems market, focusing on maritime surveillance and naval operations. This segment plays a vital role in enhancing the surveillance capabilities of naval vessels, coastal security installations, and maritime patrol units. The integration of EO/IR systems in naval platforms has significantly improved their ability to detect, track, and identify potential threats in maritime environments. These systems are particularly valuable for coastal surveillance, anti-piracy operations, and maritime border security. The segment continues to evolve with the introduction of advanced stabilization technologies, enhanced imaging capabilities, and improved performance in adverse weather conditions, making it an integral part of India's maritime defense infrastructure.

Segment Analysis: By EO/IR Systems Type

Equipment/Weapons System Segment in India Defense EO/IR Systems Market

The Equipment/Weapons System segment maintains its dominant position in India's defense EO/IR systems market, commanding approximately 43% market share in 2024. This significant market presence is driven by the segment's crucial role in military applications and combat effectiveness. The segment's strength lies in its comprehensive range of solutions including weapon-mounted sights, stabilized payloads, and advanced targeting systems that are essential for modern military operations. The Indian defense forces' increasing focus on precision strike capabilities and enhanced battlefield awareness has further cemented this segment's leadership position. Equipment/Weapons Systems continue to be at the forefront of military modernization efforts, with particular emphasis on integration with various platforms including land vehicles, aircraft, and naval vessels. The segment's robust performance is also supported by ongoing indigenous development programs and strategic partnerships with global technology providers.

Personnel Systems Segment in India Defense EO/IR Systems Market

The Personnel Systems segment is emerging as the most dynamic sector in India's defense EO/IR systems market, projected to grow at approximately 4% CAGR during 2024-2029. This accelerated growth is primarily driven by increasing investments in soldier modernization programs and the growing emphasis on enhancing individual soldier capabilities. The segment is witnessing significant technological advancements in areas such as personal thermal imaging devices, night vision equipment, and portable surveillance systems. The Indian military's focus on improving situational awareness at the individual soldier level has created substantial opportunities for innovations in this segment. The growth is further supported by the increasing adoption of advanced personal EO/IR devices across various military operations, from border surveillance to counter-insurgency operations. The segment's expansion is also bolstered by the development of lighter, more efficient, and more sophisticated personal EO/IR systems that enhance soldier effectiveness in various operational scenarios.

Remaining Segments in EO/IR Systems Type Market

The Night Vision segment represents another crucial component of India's defense EO/IR systems market, playing a vital role in enhancing military operational capabilities during low-light conditions. This segment encompasses a wide range of night vision technologies, including image intensification systems, thermal imaging devices, and fusion systems that combine multiple sensing technologies. The segment's significance is particularly evident in its applications across various military platforms and operations, from vehicle-mounted systems to handheld devices. Night vision capabilities have become increasingly important in modern military operations, especially in border surveillance and counter-terrorism operations. The segment continues to evolve with technological advancements in areas such as digital night vision technology, enhanced resolution capabilities, and improved target detection ranges, making it an integral part of India's military modernization efforts.

India Defense Industry Overview

Top Companies in India Defense Market

The Indian defense industry is characterized by a mix of established public sector undertakings and emerging private sector players driving innovation and technological advancement. Companies are increasingly focusing on the indigenous development of defense systems and equipment through the 'Make in India' initiative, with significant investments in research and development of advanced technologies like electro-optical systems, ammunition, and military gear. Strategic collaborations with international OEMs have become a key trend, enabling technology transfer and capability enhancement. Operational agility is demonstrated through the establishment of specialized manufacturing units across the country, while companies are expanding their product portfolios to cover multiple defense segments, from ammunition to electronic warfare systems. The market witnesses continuous product innovation in areas such as night vision devices, thermal imaging, and advanced body armor, with companies investing in state-of-the-art manufacturing facilities and testing capabilities.

Market Structure Shows Strategic Growth Potential

The Indian defense manufacturing market exhibits a unique structure with dominant public sector enterprises like Bharat Electronics Limited and emerging private sector players like Adani Defense and Aerospace reshaping the competitive landscape. The market is moderately consolidated, with established players holding significant market share, particularly in specialized segments like EO/IR systems and ammunition. Global defense giants maintain their presence through joint ventures and technology partnerships with Indian companies, while domestic players are strengthening their capabilities through strategic acquisitions and collaborations. The government's push for defense indigenization has created opportunities for new entrants, particularly in niche technological segments.

The market demonstrates increasing consolidation through strategic partnerships and joint ventures, with companies focusing on vertical integration to enhance their value proposition. Major players are expanding their manufacturing capabilities and establishing dedicated facilities for different product lines, while smaller players are carving out specialized niches in areas like military textiles and parachutes. The industry is witnessing a transformation from import-dependence to indigenous manufacturing capability, with companies investing in advanced manufacturing technologies and research facilities to develop next-generation defense technology products.

Innovation and Integration Drive Future Success

For established players to maintain and increase their market share, a focus on technological innovation and system integration capabilities is crucial. Companies need to invest in developing proprietary technologies while maintaining strong relationships with defense security procurement agencies. The ability to offer complete solutions rather than standalone products is becoming increasingly important, as is the capability to adapt to changing military requirements and threat scenarios. Successful incumbents are those who can balance cost-effectiveness with advanced technological capabilities while maintaining strong quality standards and delivery timelines.

New entrants and contenders can gain ground by focusing on specialized niches and developing unique technological capabilities. The market presents opportunities for companies that can offer innovative solutions in emerging areas like drone technology, advanced materials, and electronic warfare systems. Success factors include the ability to navigate complex regulatory requirements, establish strong supply chain networks, and demonstrate reliable performance through rigorous testing and certification processes. Companies must also consider the concentrated nature of military industrial procurement and develop strategies to manage long sales cycles while maintaining financial sustainability.

Indian Defense Market Leaders

-

Hindustan Aeronautics Limited (HAL)

-

Airbus SE

-

Defense Research and Development Organisation (DRDO)

-

Bharat Electronics Limited (BEL)

-

Rostec

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

India Defense Market News

November 2023: The United States and India signed a partnership agreement to co-produce Stryker armored vehicles to boost India’s military capabilities.

March 2023: The Indian Defence Ministry approved procuring 70 locally made HTT-40 primary trainer aircraft for USD 388.5 million. The new aircraft will complement the Swiss-made PC-12 Mark II essential training fleet with the Indian Air Force.

Indian Defense Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Armed Forces

- 5.1.1 Army

- 5.1.2 Navy

- 5.1.3 Air Force

-

5.2 Type

- 5.2.1 Fixed-wing Aircraft

- 5.2.2 Rotorcraft

- 5.2.3 Ground Vehicles

- 5.2.4 Naval Vessels

- 5.2.5 C4ISR

- 5.2.6 Weapons and Ammunition

- 5.2.7 Protection and Training Equipment

- 5.2.8 Unmanned Systems

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 Hindustan Aeronautics Limited (HAL)

- 6.2.2 Defense Research and Development Organisation (DRDO)

- 6.2.3 Ordance Factory Board (OFB)

- 6.2.4 Bharat Electronics Limited (BEL)

- 6.2.5 Goa Shipyard Limited (GSL)

- 6.2.6 Larsen & Toubro Limited

- 6.2.7 Hinduja Group

- 6.2.8 Kalyani Group

- 6.2.9 Tata Sons Private Limited

- 6.2.10 Reliance Group

- 6.2.11 Mahindra & Mahindra Ltd

- 6.2.12 Rafael Advanced Defense Systems Ltd

- 6.2.13 IAI Group

- 6.2.14 Rostec

- 6.2.15 Airbus SE

- 6.2.16 The Boeing Company

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Indian Defense Industry Segmentation

The Indian defense market covers all aspects of the military vehicle, armament, other equipment procurements, and upgrade and modernization plans. The report also provides insights into the budget allocation and spending of the country in the past, present, and forecast periods.

The Indian defense market is segmented by armed forces and type. Armed forces segment the market into the army, navy, and air force. By type, the market is classified into fixed-wing aircraft, rotorcraft, ground vehicles, naval vessels, C4ISR, weapons and ammunition, protection and training equipment, and unmanned systems. The report also covers the market sizes and forecasts for the Indian defense market. The market size is provided for each segment in terms of value (USD).

| Armed Forces | Army |

| Navy | |

| Air Force | |

| Type | Fixed-wing Aircraft |

| Rotorcraft | |

| Ground Vehicles | |

| Naval Vessels | |

| C4ISR | |

| Weapons and Ammunition | |

| Protection and Training Equipment | |

| Unmanned Systems |

Need A Different Region or Segment?

Customize Now

Indian Defense Market Research FAQs

How big is the India Defense Market?

The India Defense Market size is expected to reach USD 18.41 billion in 2025 and grow at a CAGR of 5.79% to reach USD 24.39 billion by 2030.

What is the current India Defense Market size?

In 2025, the India Defense Market size is expected to reach USD 18.41 billion.

Who are the key players in India Defense Market?

Hindustan Aeronautics Limited (HAL), Airbus SE, Defense Research and Development Organisation (DRDO), Bharat Electronics Limited (BEL) and Rostec are the major companies operating in the India Defense Market.

What years does this India Defense Market cover, and what was the market size in 2024?

In 2024, the India Defense Market size was estimated at USD 17.34 billion. The report covers the India Defense Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the India Defense Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

India Defense Market Research

Mordor Intelligence delivers a comprehensive analysis of the defense industry landscape. We leverage extensive expertise in the aerospace and defense sector to provide detailed research. Our examination covers the entire defense industrial base, including military defense capabilities, air defense systems, and naval defense infrastructure. The report offers in-depth coverage of emerging trends in defense technology and military technology. It focuses particularly on cyber defense innovations and defense modernization initiatives. Our analysis also extends to defense manufacturing processes, military equipment procurement, and defense systems integration.

Stakeholders can gain strategic insights into defense logistics, military aviation developments, and defense infrastructure planning through our meticulously researched report, available as an easy-to-download PDF. The analysis addresses critical aspects of defense security and military industrial capabilities, including missile defense advancements and ground defense solutions. Our report examines defense electronics, military hardware, and defense ammunition developments. It also addresses defense communication strategies and defense simulation technologies. This comprehensive coverage enables decision-makers to understand military weapons systems development and defense software applications in the evolving Indian defense landscape.