India Dairy Alternatives Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

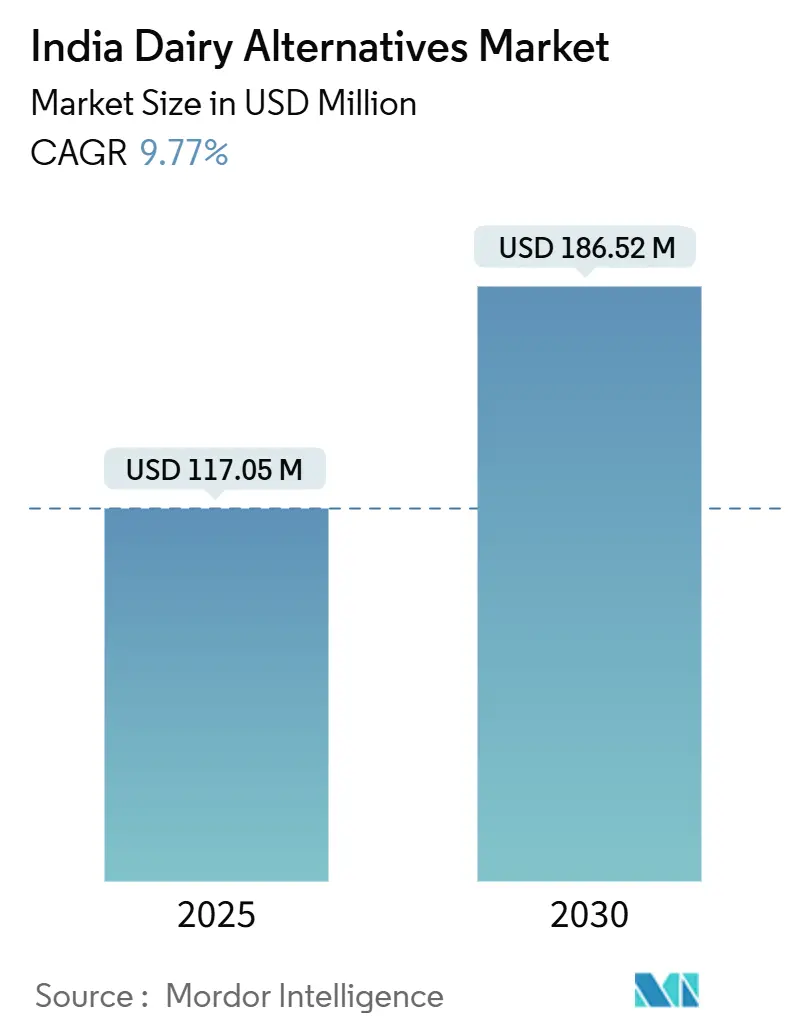

| Market Size (2025) | USD 117.05 Million |

| Market Size (2030) | USD 186.52 Million |

| Growth Rate (2025 - 2030) | 9.77% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Dairy Alternatives Market Analysis by Mordor Intelligence

The India Dairy Alternatives Market size is estimated at USD 117.05 million in 2025, and is expected to reach USD 186.52 million by 2030, at a CAGR of 9.77% during the forecast period (2025-2030). This growth trajectory reflects a fundamental shift in Indian consumer preferences, driven by rising health consciousness and the significant lactose intolerance prevalence affecting 66% of South Indians and 27% of North Indians [1]Source: National Institute of Nutrition, "lactose intolerance prevalence", nin.res.in. The market's expansion aligns with India's broader organized retail growth, which reached USD 70 billion in 2024 and continues expanding at 15-20% annually[2]Source: Retailers Association of India, "India's organized retail growth", rai.net.in. Growing café culture, digital influence, and shifting youth preferences toward vegan and flexitarian eating provide additional momentum, while established players sustain product development through scale advantages in distribution, formulation, and packaging. Investment priorities revolve around shelf-life extension and taste enhancement because cold chain gaps outside metros keep wastage rates above those of ultra-high temperature (UHT) dairy, which restrains penetration in tier-2 and tier-3 cities. Despite these frictions, the India non-dairy alternatives market continues to attract capital as disposable incomes rise and government regulators adopt progressive labeling rules that clarify consumer choice.

Key Report Takeaways

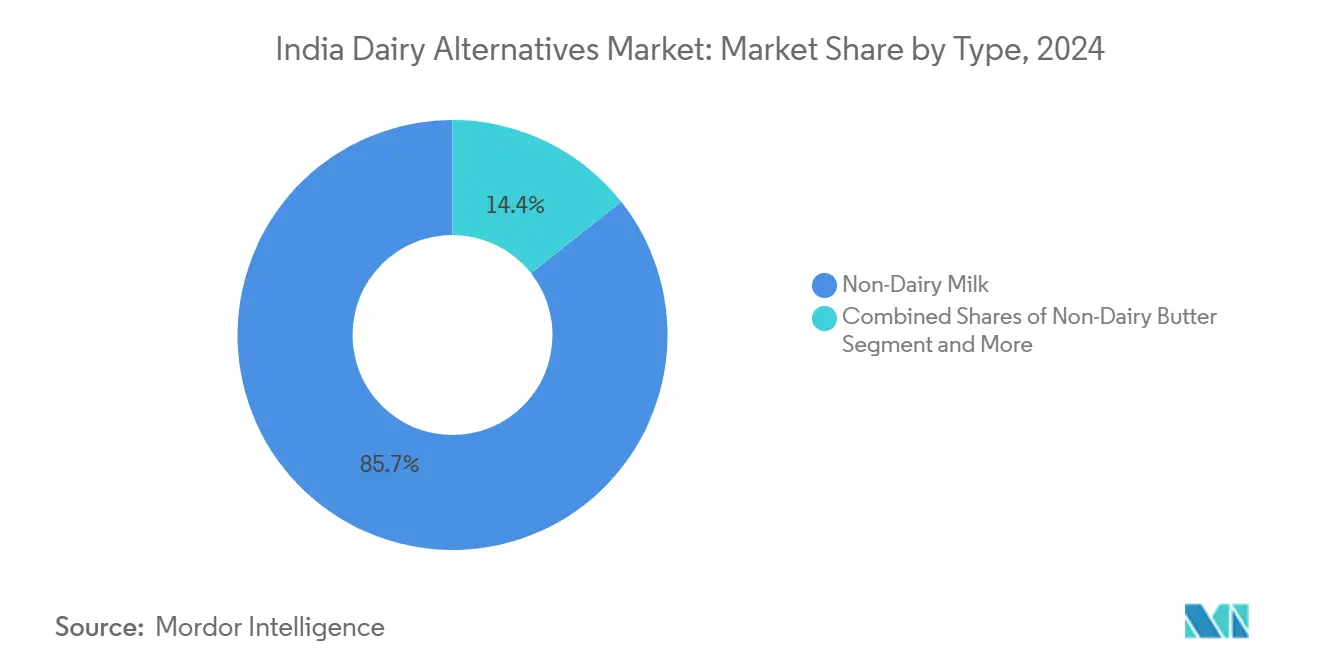

- By product type, non-dairy milk led with 85.65% revenue share in 2024; non-dairy butter is projected to expand at a 9.73% CAGR through 2030.

- By packaging type, cartons commanded 60.30% share of the India non-dairy alternatives market size in 2024, while PET bottles record the fastest CAGR at 10.33% to 2030.

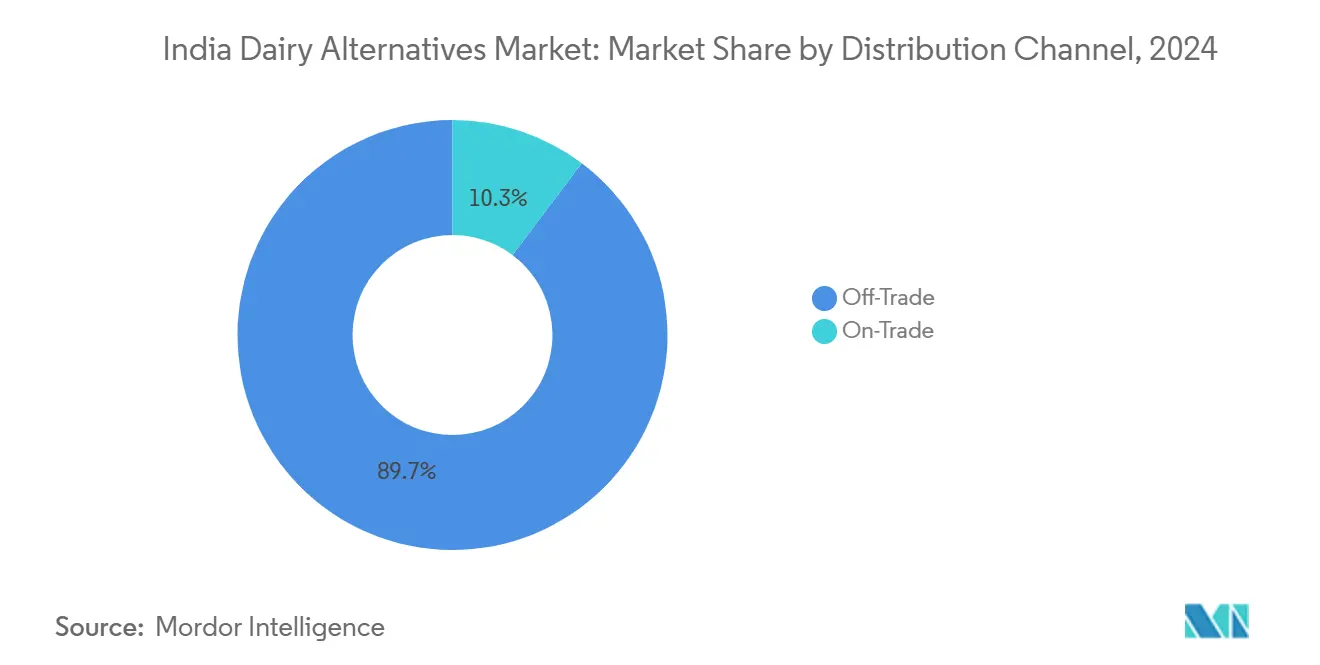

- By distribution channel, off-trade held 99.02% of the India non-dairy alternatives market share in 2024, whereas on-trade is advancing at an 11.32% CAGR through 2030.

India Dairy Alternatives Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of lactose intolerance population | +2.8% | National, with higher concentration in South India (66%) vs North India (27%) | Long term (≥ 4 years) |

| Youth shifting toward vegan, flexitarian diets | +2.1% | Urban centers, particularly Mumbai, Delhi, Bangalore, Chennai | Medium term (2-4 years) |

| Social media, influencers promote plant diets | +1.9% | Urban millennials and Gen-Z across tier-1 cities | Short term (≤ 2 years) |

| Growing concern over dairy animal welfare | +1.4% | Metropolitan areas with higher education levels | Medium term (2-4 years) |

| Modern retail, cafes expanding product range | +1.2% | Organized retail corridors in major cities | Short term (≤ 2 years) |

| Preference towards managing heart health, diabetes | +0.9% | National, with focus on urban populations aged 35+ | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Presence of Lactose Intolerance Population Drives Market Foundation

India's genetic predisposition toward lactose intolerance creates an inherent market foundation for non-dairy alternatives, with 66% of South Indians and 27% of North Indians experiencing lactose malabsorption according to the National Institute of Nutrition. This biological reality translates into approximately 400 million potential consumers who experience digestive discomfort from conventional dairy products, creating sustained demand for plant-based alternatives. The regional variation in lactose intolerance prevalence explains why southern states like Tamil Nadu and Karnataka demonstrate higher per-capita consumption of non-dairy products compared to northern regions. FSSAI's recognition of this health imperative has led to streamlined approval processes for lactose-free and plant-based dairy analogues, reducing regulatory barriers for manufacturers[3]Source: Food Safety and Standards Authority of India, "lactose intolerance prevalence ", fssai.gov.in. The demographic shift toward urbanization amplifies this trend, as urban consumers demonstrate greater willingness to experiment with alternative products and possess higher purchasing power to afford premium plant-based options.

Youth Shifting Toward Vegan, Flexitarian Diets Accelerates Adoption

India's millennial and Gen-Z demographics increasingly embrace flexitarian and plant-forward eating patterns, with 63% of urban consumers aged 18-35 incorporating plant-based alternatives into their diets at least twice weekly according to recent consumer surveys. This generational shift stems from environmental consciousness, health awareness, and exposure to global dietary trends through digital platforms and international travel. The trend gains momentum through educational institutions, where hostel mess services and campus cafeterias increasingly offer plant-based options to cater to diverse dietary preferences. Corporate wellness programs in IT hubs like Bangalore and Hyderabad actively promote plant-based nutrition, creating workplace demand that extends to retail purchasing decisions. The segment's purchasing power continues expanding as India's median age remains 28 years, ensuring sustained market growth as these consumers mature and establish household purchasing patterns according to the Ministry of Statistics and Programme Implementation.

Social Media, Influencers Promote Plant Diets Through Digital Engagement

Instagram and YouTube influencers specializing in health, fitness, and sustainable living have created substantial awareness around plant-based nutrition, with leading Indian wellness influencers accumulating over 50 million combined followers who regularly engage with plant-based content. This digital ecosystem generates authentic product trials through recipe demonstrations, taste comparisons, and lifestyle integration content that traditional advertising cannot replicate. The influencer marketing approach proves particularly effective for non-dairy alternatives because visual platforms showcase product versatility in cooking, beverages, and dessert applications. Quick commerce platforms like Zepto and Blinkit report most of their plant-based product sales originate from social media referrals, indicating direct conversion from digital engagement to purchase behavior. The trend accelerates as regional language content creators expand plant-based messaging beyond English-speaking urban audiences, broadening market reach into tier-2 cities where traditional marketing channels face cost and reach limitations.

Growing Concern Over Dairy Animal Welfare Influences Purchase Decisions

Ethical consumption patterns increasingly influence Indian consumer choices, with animal welfare concerns driving 23% of plant-based product trials among urban consumers according to industry surveys. This consciousness stems from increased media coverage of industrial dairy farming practices and growing awareness of animal rights issues through social media platforms and documentary content. The trend particularly resonates with educated urban consumers who demonstrate willingness to pay premium prices for products aligned with their ethical values. Religious and cultural factors amplify this trend, as traditional Indian philosophical concepts of ahimsa (non-violence) find contemporary expression through conscious consumption choices. The movement gains institutional support through animal welfare organizations and environmental groups that actively promote plant-based alternatives as ethical consumption options, creating sustained awareness campaigns that influence long-term purchasing behavior.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shorter shelf life compared to UHT dairy | -1.8% | National, particularly affecting tier-2 and tier-3 cities | Medium term (2-4 years) |

| Taste, texture often inferior to cow's milk | -1.5% | National, with higher impact in traditional dairy-consuming regions | Short term (≤ 2 years) |

| Labeling laws restrict use of "milk" terms | -0.9% | National regulatory compliance requirement | Long term (≥ 4 years) |

| Poor cold chain outside metro cities | -1.3% | Tier-2, tier-3 cities and rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shorter Shelf Life Compared to UHT Dairy Constrains Distribution Economics

Plant-based alternatives typically maintain 7-14 days refrigerated shelf life compared to UHT dairy's 6-month ambient storage capability, creating significant distribution and inventory management challenges for retailers and manufacturers. This limitation particularly impacts tier-2 and tier-3 cities where cold chain infrastructure coverage remains below 40% and inventory turnover rates lag metropolitan areas by 30-40%. The shorter shelf life increases wastage rates, with retailers reporting 8-12% product losses compared to 2-3% for UHT dairy products, directly impacting profit margins and pricing strategies. Manufacturers invest heavily in packaging innovations and preservative technologies to extend shelf life, but these solutions increase production costs by 15-25% compared to conventional dairy processing. The constraint forces companies to maintain smaller distribution networks and higher inventory turnover requirements, limiting market penetration speed and geographic expansion capabilities.

Taste, Texture Often Inferior to Cow's Milk Affects Consumer Retention

Sensory attributes remain the primary barrier to sustained consumption, with taste and mouthfeel differences causing 35% of first-time users to discontinue regular consumption of plant-based alternatives according to consumer research studies. The challenge proves particularly acute for traditional dairy-consuming regions where consumers possess deeply ingrained flavor preferences developed over generations of cow and buffalo milk consumption. Protein content variations create noticeable texture differences, especially in applications requiring frothing or heating, limiting adoption in tea and coffee preparations that constitute 80% of Indian milk consumption. Manufacturers invest substantially in flavor enhancement technologies and ingredient optimization, but achieving sensory parity with dairy milk remains technically challenging while maintaining cost competitiveness. The gap creates opportunities for premium positioning but limits mass market penetration, particularly among price-sensitive consumer segments that prioritize functional equivalence over ethical or health considerations.

Segment Analysis

By Type: Non-Dairy Milk Dominates Through Versatility

Non-dairy milk commands 85.65% market share in 2024, reflecting its fundamental role as a direct dairy substitute across multiple consumption occasions from beverages to cooking applications. The segment's dominance stems from its versatility in traditional Indian preparations like tea, coffee, and desserts, where functional performance closely matches conventional milk. Oat milk emerges as the fastest-growing variant within this category, driven by its superior frothing capabilities and creamy texture that appeals to cafe and foodservice applications. Almond milk maintains strong positioning in health-conscious segments, while coconut milk leverages traditional familiarity in South Indian cuisine. Soy milk, despite being the earliest entrant, faces declining share due to taste preferences and concerns about processing methods.

The fastest-growing segment, non-dairy butter at 9.73% CAGR through 2030, indicates expanding consumer experimentation beyond liquid alternatives into solid dairy replacements. This growth reflects increasing sophistication in plant-based product development and consumer willingness to trial premium alternatives for baking and cooking applications. Non-dairy cheese and yogurt segments remain nascent but demonstrate potential as manufacturers improve texture and flavor profiles through advanced fermentation technologies. The segment expansion creates opportunities for specialized players focusing on specific product categories rather than broad portfolios, enabling targeted innovation and marketing strategies.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Type: Cartons Lead While PET Bottles Gain Momentum

Cartons maintain 60.30% market share in 2024, benefiting from consumer perception of freshness, environmental friendliness, and superior product protection during transportation and storage. The format's dominance reflects established supply chain infrastructure and retailer preferences for shelf-stable packaging that minimizes handling complexity. However, PET bottles demonstrate the highest growth trajectory at 10.33% CAGR through 2030, driven by convenience factors and consumer preference for resealable packaging that enables portion control and extended consumption periods. The shift toward PET bottles aligns with increasing on-the-go consumption patterns and single-serve preferences among urban consumers.

Cans represent a smaller but stable segment, primarily serving institutional and foodservice channels where bulk packaging provides cost advantages and extended shelf life. The packaging evolution reflects broader consumer behavior changes, with convenience increasingly outweighing environmental considerations for certain use cases. Manufacturers face strategic decisions between sustainable packaging preferences and functional consumer requirements, leading to investments in recyclable PET technologies and lightweight carton innovations. The packaging dynamics influence distribution strategies, with PET bottles enabling broader geographic reach through ambient storage capabilities while cartons require consistent cold chain maintenance.

By Distribution Channel: Off-Trade Dominance with On-Trade Growth Potential

Off-trade channels command 99.02% market share in 2024, reflecting the nascent stage of foodservice adoption for plant-based alternatives in India's restaurant and cafe ecosystem. This dominance stems from consumer preference for home consumption and limited availability of non-dairy options in traditional foodservice establishments. Within off-trade, supermarkets and hypermarkets lead distribution, followed by convenience stores and online retail platforms. The organized retail expansion enables broader product availability and consumer trial opportunities through promotional activities and sampling programs.

On-trade channels, despite minimal current share, demonstrate the highest growth potential at 11.32% CAGR through 2030, indicating expanding foodservice adoption as cafes, restaurants, and quick-service establishments recognize consumer demand for plant-based options. This growth trajectory reflects the premiumization of Indian foodservice, where establishments differentiate through diverse menu options and health-conscious alternatives. Coffee chains and modern bakeries lead on-trade adoption, leveraging plant-based alternatives for specialty beverages and vegan dessert options. The channel expansion creates opportunities for manufacturers to develop foodservice-specific products with enhanced functionality and cost-effectiveness. Online retail continues growing within off-trade, benefiting from subscription models and direct-to-consumer strategies that enable brand building and customer education.

Competitive Landscape

The India non-dairy alternatives market demonstrates moderate consolidation with established players leveraging distribution networks, brand recognition, and innovation capabilities to maintain competitive advantages. Market concentration enables sustained investment in product development and supply chain optimization, while creating barriers for new entrants lacking scale economies.

Competitive strategies center on taste improvement, shelf-life extension, and cost optimization to achieve mass market penetration beyond niche health-conscious segments. Technology adoption proves crucial for market success, with leading players investing in fermentation technologies, protein extraction methods, and packaging innovations that enhance product quality and consumer acceptance. The competitive landscape reveals substantial white-space opportunities in tier-2 and tier-3 cities where distribution infrastructure development creates first-mover advantages for companies willing to invest in market development.

Strategic positioning varies significantly across player categories, with multinational corporations leveraging global expertise and local companies capitalizing on regional taste preferences and distribution relationships. Emerging disruptors focus on direct-to-consumer models and subscription services that bypass traditional retail limitations while building brand loyalty through customer education and engagement. Patent filings in plant-based processing technologies increased 45% in 2024, indicating intensifying innovation competition among market participants.

India Dairy Alternatives Industry Leaders

-

Tata Consumer Products Limited

-

Nestlé

-

Oatly Group AB

-

Danone

-

Rawpressery

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Country Delight, an Indian dairy and grocery brand, has made its debut in the plant-based drink sector with a novel milk alternative. The product, branded as Oat Beverage, is crafted from Australian oats and boasts a formulation devoid of chemical additives, preservatives, and added sugars. Additionally, the beverage is free from soy and nuts, and is produced in a facility with stringent allergen controls to mitigate cross-contamination risks.

- September 2024: Maiva Fresh has unveiled its flagship product - Unsweetened Almond Milk. The brand, "Maiva Fresh," promotes its new health drink range with the tagline "Pure Good" (emphasizing health) and "Pure Joy" (highlighting taste), effectively merging the concepts of health and flavor. The Maiva Fresh Almond Milk boasts zero cholesterol, a low glycemic index, and fortification with Vitamins B12 and D, making it ideal for daily consumption.

- September 2024: Recognizing a growing demand for dairy alternatives, 1.5 Degree, an innovative start-up, has rolled out a diverse lineup of plant-based dairy products. Their offerings span from oat and soy milk to cold coffee, flavored milkshakes, and gelato, boasting unique flavors like paan, Belgian chocolate, strawberry, Biscoff, and mocha almond fudge. The emphasis lies on delivering products that are not only taste-centric and healthy but also lactose-free.

India Dairy Alternatives Market Report Scope

Non-Dairy Butter, Non-Dairy Milk are covered as segments by Category. Off-Trade, On-Trade are covered as segments by Distribution Channel.| Non-Dairy Milk | Oat Milk |

| Hemp Milk | |

| Hazelnut Milk | |

| Soy Milk | |

| Almond Milk | |

| Coconut Milk | |

| Cashew Milk | |

| Non-Dairy Cheese | |

| Non-Dairy Desserts | |

| Non-Dairy Yogurt | |

| Others |

| PET Bottles |

| Cans |

| Cartons |

| Others |

| On-trade | |

| Off-trade | Convenience Stores |

| Supermarkets and Hypermarkets | |

| Online Retail Stores | |

| Other Distribution Channel |

| By Type | Non-Dairy Milk | Oat Milk |

| Hemp Milk | ||

| Hazelnut Milk | ||

| Soy Milk | ||

| Almond Milk | ||

| Coconut Milk | ||

| Cashew Milk | ||

| Non-Dairy Cheese | ||

| Non-Dairy Desserts | ||

| Non-Dairy Yogurt | ||

| Others | ||

| Packaging Type | PET Bottles | |

| Cans | ||

| Cartons | ||

| Others | ||

| Distribution Channel | On-trade | |

| Off-trade | Convenience Stores | |

| Supermarkets and Hypermarkets | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms