| Study Period | 2017 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 47.96 Million |

| Market Size (2030) | USD 68.6 Million |

| CAGR (2025 - 2030) | 7.42 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

India Controlled Release Fertilizer Market Analysis

The India Controlled Release Fertilizer Market size is estimated at 47.96 million USD in 2025, and is expected to reach 68.6 million USD by 2030, growing at a CAGR of 7.42% during the forecast period (2025-2030).

India's agricultural sector is experiencing a significant transformation in fertilizer application technologies, driven by the pressing need to optimize nutrient efficiency. With field crops occupying 90% of the cultivated area in 2022, the sector faces substantial challenges in maintaining soil fertility and ensuring sustainable crop yields. The overall primary nutrient application rate reached 125.1 kg/ha in 2022, highlighting the intensive nature of agricultural practices. Traditional fertilizer applications have shown considerable inefficiencies, with studies indicating 30-40% nutrient loss through various processes, including leaching and volatilization, necessitating the adoption of more advanced fertilizer technologies.

The controlled release fertilizer industry has emerged as a crucial solution to address the challenges of nutrient management in Indian agriculture. The technology's ability to extend nutrient release time by 3 to 15 months has revolutionized fertilizer application practices, particularly benefiting major crops such as wheat, rice, and maize. The sector has witnessed remarkable innovation in coating technologies, with polymer-coated and polymer-sulfur-coated variants gaining prominence. These advanced formulations have demonstrated the potential to reduce cultivation costs by 20-30% while significantly improving nutrient use efficiency. The adoption of slow release fertilizer is also contributing to this transformation, offering a more environmentally friendly fertilizer option.

The horticultural sector has become a key growth driver for controlled release fertilizer adoption, with total horticulture production reaching 341.63 million tons in 2021-22, marking a 2.10% increase from the previous year. The precision agriculture movement has gained momentum, with farmers increasingly recognizing the value of smart fertilizer and controlled nutrient release in maintaining optimal growth conditions for high-value crops. The industry has responded by developing specialized formulations that cater to the specific nutritional requirements of different horticultural crops, ensuring sustained nutrient availability throughout the growing season.

The regulatory landscape has played a pivotal role in shaping market dynamics, particularly through the government's mandate for domestic producers to manufacture 100% neem-coated urea and distribute it at subsidized rates to farmers. This policy intervention has accelerated the transition toward enhanced efficiency fertilizer while ensuring accessibility for farmers. The industry has also witnessed significant developments in distribution networks and supply chain optimization, with manufacturers focusing on establishing direct farmer connect programs and technical support services to promote proper application practices and maximize the benefits of controlled release fertilizer technology.

India Controlled Release Fertilizer Market Trends

The intense cereal cultivation in the country is anticipated to drive the Indian fertilizer market

- The area under field crop cultivation in the country increased by 3.5% during the study period. The increased cultivation of cereals, pulses, and oilseeds in the country due to the rising consumer demand domestically and internationally is the major driving factor for the rising acreage. By crop type, rice, wheat, and soybean occupied the largest area under cultivation in the country, accounting for 47 million ha, 31.1 million ha, and 12.3 million ha in 2022. Rice is the most important food crop of India, covering about one-fourth of the total cropped area and providing food to about half of the Indian population. It is cultivated in almost all the states of the country, mainly in West Bengal, Uttar Pradesh, Andhra Pradesh, Punjab, and Tamil Nadu.

- Accordingly, rice consumption in the country increased from 95.8 million tons in 2016 to 107 million tons in 2022, which shows the rising demand for the crop in the country. This trend is further anticipated to drive the demand for fertilizers during 2023-2030. Similarly, wheat cultivation in the country increased from 98.5 million tons in 2017 to 107.6 million tons in 2020. It is cultivated majorly in Punjab, West Bengal, Haryana, and Rajasthan. Wheat is the second most important cereal crop in India and plays a vital role in the country's food and nutritional security. Therefore, the intense cereal cultivation in the country, coupled with rising domestic and international demand, is anticipated to drive the Indian fertilizer market during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

Among the primary nutrients, nitrogen is the most-applied nutrient in field crops, with an average application rate of 223.5 kg per hectare

- The overall primary nutrient average application rate in 2022 was 125.1 kg/ha, with nutrients such as nitrogen with the highest average application rate of 223.5 kg/ha. Accordingly, nitrogen is the major source of nutrients for crops such as rice, which is intensively cultivated in the country, and such nutrient deficiency in soil is limiting rice productivity across the nation.

- The State of Biofertilizers and Organic Fertilizers in India marked the poor status of soil health, with increasing consumption of chemical fertilizers in India. Accordingly, 97.0%, 83.0%, and 71.0% of the soil tested were found to be deficient in nitrogen, phosphorous, and potassium, respectively.

- By crop, wheat, rice, and corn/maize are estimated to be the crop types with the highest average nutrient application rate of 231, 156, and 149 kg/ha in 2022. Wheat and rice are important staple food domestically and globally. Multiple nutrient deficiencies are the key factors that reduce yield and profit. Wheat and rice crops require nitrogen, phosphorous, and potassium, along with other micronutrients such as sulfur, boron, iron, and zinc, for their proper growth and development. The proper management of nutrients is necessary for successful crop production, which is driving market growth.

- Field crops consume the maximum amount of primary nutrients, such as nitrogen fertilizer. As grains and cereals are intensively grown in the country, the soil is depleted of its nutrition, and hence, they require more fertilizers to supplement them, which, in turn, is anticipated to drive the market during 2023-2030.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- The area under horticulture is steadily increasing over the years due to the increasing demand for fruits and vegetables

- Among the primary nutrients, nitrogen is used in larger amounts to aid in rapid vegetative growth and the production of fruits

Segment Analysis: Coating Type

Polymer Coated Segment in India Controlled Release Fertilizer Market

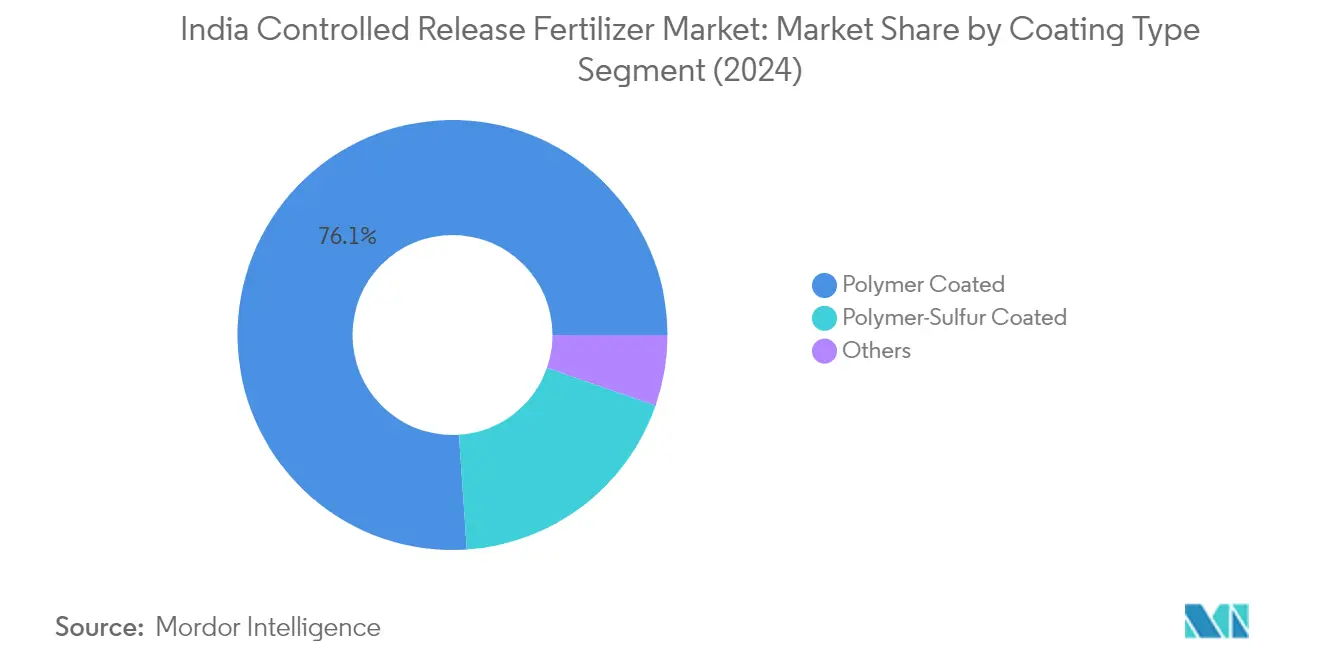

The polymer coated fertilizer segment dominates the Indian controlled release fertilizer market, commanding approximately 76% market share in 2024, primarily due to its superior efficiency in increasing fertilizer use capacity and reducing nutrient losses. This segment's prominence is particularly evident in field crops, which account for nearly 89% of polymer coated fertilizer applications, followed by horticultural crops. The segment's strong market position is attributed to the increased awareness among farmers about the negative impacts of nutrient leaching and environmental pollution, with polymer coated fertilizer CRFs offering a viable solution through controlled nutrient release timing. Furthermore, the segment is experiencing robust growth at around 7% CAGR from 2024 to 2029, driven by the rising popularity of polyolefin resin coating in agriculture and active research on developing biodegradable and cost-effective polymer coating materials. The maximum benefit from polymer coated fertilizer CRF is achieved when farmers synchronize the nutrient release duration with crop nutrient uptake periods, making it particularly effective for various agricultural applications.

Remaining Segments in Coating Type

The sulfur coated fertilizer and other coating segments complete the market landscape, each serving specific agricultural needs. Sulfur coated fertilizer effectively addresses sulfur deficiency in various crops like cereals, fruits, and vegetables, making them particularly valuable for acidic and sandy soils with low organic matter content. The other coating segment includes innovative solutions such as biodegradable material coatings and zinc-coated urea, which are gaining traction due to their effectiveness in preventing nitrate leakage and addressing specific nutrient deficiencies. These segments continue to evolve with technological advancements and increasing focus on sustainable agricultural practices, offering farmers diverse options for optimizing nutrient delivery based on their specific crop and soil requirements.

Segment Analysis: Crop Type

Field Crops Segment in India Controlled Release Fertilizer Market

Field crops dominate the Indian controlled release fertilizer market, commanding approximately 89% of the total market value in 2024. This substantial market share can be attributed to the segment's extensive cultivation area, which covers over 90% of India's agricultural land. The segment's prominence is particularly evident in major crops like rice, wheat, and maize, where timed release fertilizer has proven highly effective in addressing nutrient deficiency challenges. These crops require significant nitrogen content throughout their growth stages, making encapsulated fertilizer particularly valuable. The efficiency of controlled release fertilizer in field crops is demonstrated by their ability to reduce nutrient losses by 30-40% compared to conventional fertilizers, while simultaneously decreasing cultivation costs by 20-30%. The segment's dominance is further strengthened by the increasing adoption of advanced fertilizer technologies among field crop farmers, who recognize the benefits of controlled nutrient release in improving crop yields and reducing environmental impact.

Horticultural Crops Segment in India Controlled Release Fertilizer Market

The horticultural crops segment is emerging as the fastest-growing segment in India's controlled release fertilizer market, with an expected growth rate of approximately 8% from 2024 to 2029. This accelerated growth is driven by the increasing adoption of precision farming techniques and greenhouse cultivation methods in fruit and vegetable production. The segment's growth is further supported by the rising awareness among horticultural farmers about the benefits of coated fertilizer in reducing nutrient leaching and improving nutrient use efficiency. The expansion of high-value horticultural crops, coupled with the growing export market for fruits and vegetables, is creating a strong demand for advanced fertilizer solutions. Additionally, the segment's growth is bolstered by the increasing focus on quality production and the need for optimal nutrient management in intensive horticultural systems, particularly in crops like tomatoes, cabbage, and cauliflower, which require precise nutrient delivery throughout their growing cycle.

Remaining Segments in Crop Type

The turf and ornamental segment, while smaller in market share, plays a significant role in the Indian controlled release fertilizer market, particularly in specialized applications such as golf courses, public gardens, and ornamental plant cultivation. This segment is characterized by its unique requirements for sustained nutrient release and the need for premium fertilizer products that can maintain aesthetic appeal while minimizing maintenance requirements. The segment's growth is supported by the expanding landscaping industry and increasing urbanization, which has led to greater demand for well-maintained green spaces. The adoption of coated fertilizer in this segment is driven by their ability to provide consistent nutrient supply over extended periods, reducing the frequency of applications and labor costs while maintaining optimal plant health and appearance.

India Controlled Release Fertilizer Industry Overview

Top Companies in India Controlled Release Fertilizer Market

The controlled release fertilizer market in India is characterized by the strong presence of both global and domestic players, with ICL Group Ltd, Grupa Azoty S.A. (Compo Expert), New Mountain Capital (Florikan), and Hebei Sanyuanjiuqi Fertilizer leading the competitive landscape. Companies in this sector are increasingly focusing on product innovation, particularly in developing advanced fertilizer coating technologies that enable precise nutrient release timing and improved efficiency. Strategic partnerships have become a crucial growth lever, with firms collaborating with local distributors and agricultural institutions to expand their market reach and technical expertise. Operational agility is demonstrated through investments in research and development facilities, while companies are also expanding their manufacturing capabilities to meet the growing demand. The industry has witnessed a significant trend towards developing environmentally friendly fertilizer solutions, with companies investing in biodegradable coating materials and eco-friendly production processes.

Market Dominated by Global Technology Leaders

The Indian controlled release fertilizer market exhibits a moderate level of consolidation, with global technology leaders holding significant market share due to their advanced coating technologies and established distribution networks. These multinational companies leverage their extensive research capabilities and global experience to maintain their competitive edge, while domestic players focus on building regional distribution strengths and customizing products for local agricultural conditions. The market structure favors companies with strong technological capabilities and established relationships with agricultural institutions, as success in this sector requires significant investment in research and development.

The competitive dynamics are shaped by the presence of diversified agricultural input conglomerates alongside specialized fertilizer manufacturers. While mergers and acquisitions activity has been limited, strategic partnerships and joint ventures have emerged as preferred modes of market expansion. Companies are increasingly focusing on vertical integration to secure raw material supplies and strengthen their position in the value chain. The market also sees active collaboration between international technology providers and local manufacturers, enabling knowledge transfer and market access.

Innovation and Distribution Key to Growth

Success in the Indian controlled release fertilizer market increasingly depends on companies' ability to develop cost-effective solutions while maintaining product efficacy. Incumbent players must focus on expanding their product portfolio with specialized formulations for different crops and soil conditions, while also strengthening their distribution networks in emerging agricultural regions. Building strong relationships with agricultural extension services and farmer communities has become crucial for market penetration, as the adoption of smart fertilizer requires significant farmer education and technical support.

For new entrants and challenger brands, the path to market share growth lies in developing innovative coating technologies that offer better cost-efficiency ratios and focusing on underserved market segments. Companies must also navigate the complex regulatory environment surrounding fertilizer manufacturing and distribution in India, while addressing the growing emphasis on environmental sustainability. The future competitive landscape will be shaped by companies' ability to develop products that balance performance, cost, and environmental impact, while building robust distribution networks that can effectively reach and serve the diverse Indian agricultural market.

India Controlled Release Fertilizer Market Leaders

-

Grupa Azoty S.A. (Compo Expert)

-

Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

-

ICL Group Ltd

-

New Mountain Capital (Florikan)

-

Zhongchuang xingyuan chemical technology co.ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

India Controlled Release Fertilizer Market News

- July 2018: Haifa Group introduces a novel a range of coated micronutrients, enabling an all-season complete nutrition. Based on Multicote™ technology, the coated micronutrients provide your crops with all the benefits of controlled release nutrition.

Free With This Report

Along with the report, We also offer a comprehensive and exhaustive data pack with 25+ graphs on area under cultivation and average application rate per hectare. The data pack includes Globe, North America, Europe, Asia-Pacific, South America, and Africa.

India Controlled Release Fertilizer Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

-

4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

-

4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

-

5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

-

5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles

- 6.4.1 Grupa Azoty S.A. (Compo Expert)

- 6.4.2 Haifa Group

- 6.4.3 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.4 ICL Group Ltd

- 6.4.5 New Mountain Capital (Florikan)

- 6.4.6 Zhongchuang xingyuan chemical technology co.ltd

- *List Not Exhaustive

7. KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- CULTIVATION OF FIELD CROPS IN HECTARE, INDIA, 2017 - 2022

- Figure 2:

- CULTIVATION OF HORTICULTURAL CROPS IN HECTARE, INDIA, 2017 - 2022

- Figure 3:

- CONSUMPTION OF PRIMARY NUTRIENTS BY FIELD CROPS IN KG/HECTARE, INDIA, 2022

- Figure 4:

- CONSUMPTION OF PRIMARY NUTRIENTS BY HORTICULTURAL CROPS IN KG/HECTARE, INDIA, 2022

- Figure 5:

- SPECIALITY FERTILIZER CONSUMPTION IN METRIC TON, INDIA, 2017 - 2030

- Figure 6:

- SPECIALITY FERTILIZER CONSUMPTION IN USD, INDIA, 2017 - 2030

- Figure 7:

- CRF CRF FERTILIZER CONSUMPTION BY COATING TYPE IN METRIC TON, INDIA, 2017 - 2030

- Figure 8:

- CRF CRF FERTILIZER CONSUMPTION BY COATING TYPE IN USD, INDIA, 2017 - 2030

- Figure 9:

- CRF CRF FERTILIZER CONSUMPTION VOLUME BY COATING TYPE IN %, INDIA, 2017 VS 2023 VS 2030

- Figure 10:

- CRF CRF FERTILIZER CONSUMPTION VALUE BY COATING TYPE IN %, INDIA, 2017 VS 2023 VS 2030

- Figure 11:

- POLYMER COATED CRF FERTILIZER CONSUMPTION IN METRIC TON, INDIA, 2017 - 2030

- Figure 12:

- POLYMER COATED CRF FERTILIZER CONSUMPTION IN USD, INDIA, 2017 - 2030

- Figure 13:

- POLYMER COATED CRF FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, INDIA, 2023 VS 2030

- Figure 14:

- POLYMER-SULFUR COATED CRF FERTILIZER CONSUMPTION IN METRIC TON, INDIA, 2017 - 2030

- Figure 15:

- POLYMER-SULFUR COATED CRF FERTILIZER CONSUMPTION IN USD, INDIA, 2017 - 2030

- Figure 16:

- POLYMER-SULFUR COATED CRF FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, INDIA, 2023 VS 2030

- Figure 17:

- OTHERS CRF FERTILIZER CONSUMPTION IN METRIC TON, INDIA, 2017 - 2030

- Figure 18:

- OTHERS CRF FERTILIZER CONSUMPTION IN USD, INDIA, 2017 - 2030

- Figure 19:

- OTHERS CRF FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, INDIA, 2023 VS 2030

- Figure 20:

- CRF CRF FERTILIZER CONSUMPTION BY CROP TYPE IN METRIC TON, INDIA, 2017 - 2030

- Figure 21:

- CRF CRF FERTILIZER CONSUMPTION BY CROP TYPE IN USD, INDIA, 2017 - 2030

- Figure 22:

- CRF CRF FERTILIZER CONSUMPTION VOLUME BY CROP TYPE IN %, INDIA, 2017 VS 2023 VS 2030

- Figure 23:

- CRF CRF FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, INDIA, 2017 VS 2023 VS 2030

- Figure 24:

- CRF FERTILIZER CONSUMPTION BY FIELD CROPS IN METRIC TON, INDIA, 2017 - 2030

- Figure 25:

- CRF FERTILIZER CONSUMPTION BY FIELD CROPS IN USD, INDIA, 2017 - 2030

- Figure 26:

- FERTILIZER CONSUMPTION VALUE BY COATING TYPE IN %, INDIA, 2023 VS 2030

- Figure 27:

- CRF FERTILIZER CONSUMPTION BY HORTICULTURAL CROPS IN METRIC TON, INDIA, 2017 - 2030

- Figure 28:

- CRF FERTILIZER CONSUMPTION BY HORTICULTURAL CROPS IN USD, INDIA, 2017 - 2030

- Figure 29:

- FERTILIZER CONSUMPTION VALUE BY COATING TYPE IN %, INDIA, 2023 VS 2030

- Figure 30:

- CRF FERTILIZER CONSUMPTION BY TURF & ORNAMENTAL IN METRIC TON, INDIA, 2017 - 2030

- Figure 31:

- CRF FERTILIZER CONSUMPTION BY TURF & ORNAMENTAL IN USD, INDIA, 2017 - 2030

- Figure 32:

- FERTILIZER CONSUMPTION VALUE BY COATING TYPE IN %, INDIA, 2023 VS 2030

- Figure 33:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, INDIA, 2017 - 2030

- Figure 34:

- INDIA CONTROLLED RELEASE FERTILIZER MARKET, MOST ADOPTED STRATEGIES, 2018 - 2021

- Figure 35:

- MARKET SHARE OF MAJOR PLAYERS IN %, INDIA

India Controlled Release Fertilizer Industry Segmentation

Polymer Coated, Polymer-Sulfur Coated, Others are covered as segments by Coating Type. Field Crops, Horticultural Crops, Turf & Ornamental are covered as segments by Crop Type.| Coating Type | Polymer Coated |

| Polymer-Sulfur Coated | |

| Others | |

| Crop Type | Field Crops |

| Horticultural Crops | |

| Turf & Ornamental |

Need A Different Region or Segment?

Customize Now

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Urea & Complex

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF