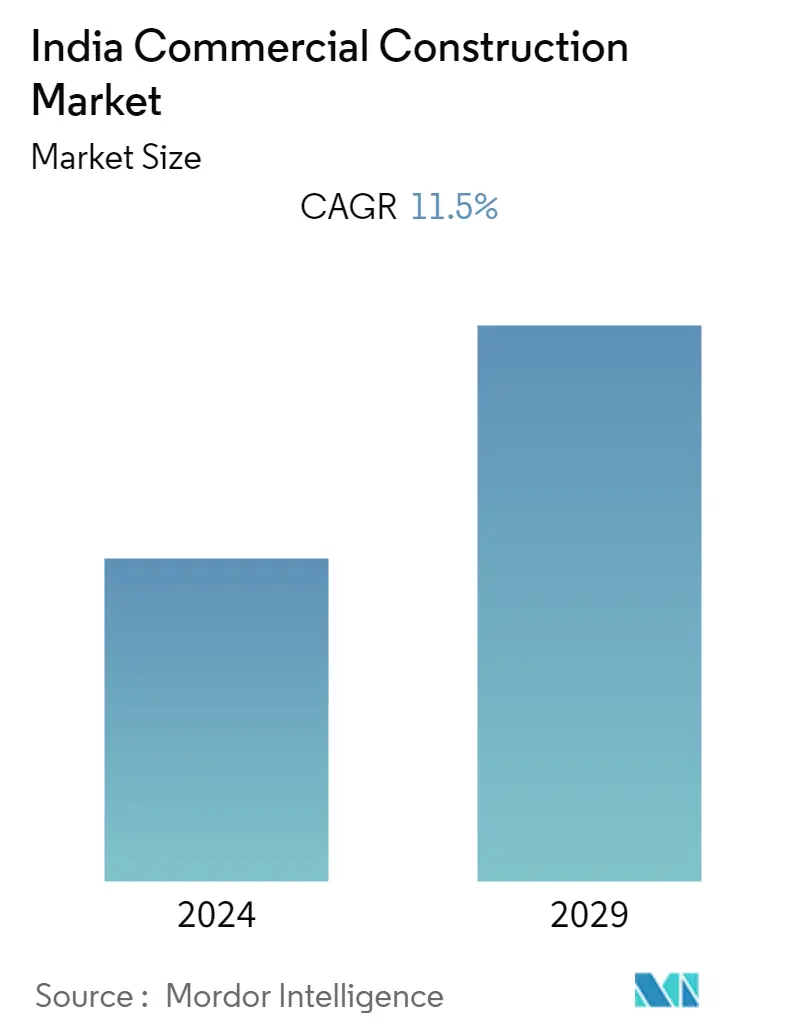

India Commercial Construction Market Size

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2020 - 2022 |

| CAGR | 11.50 % |

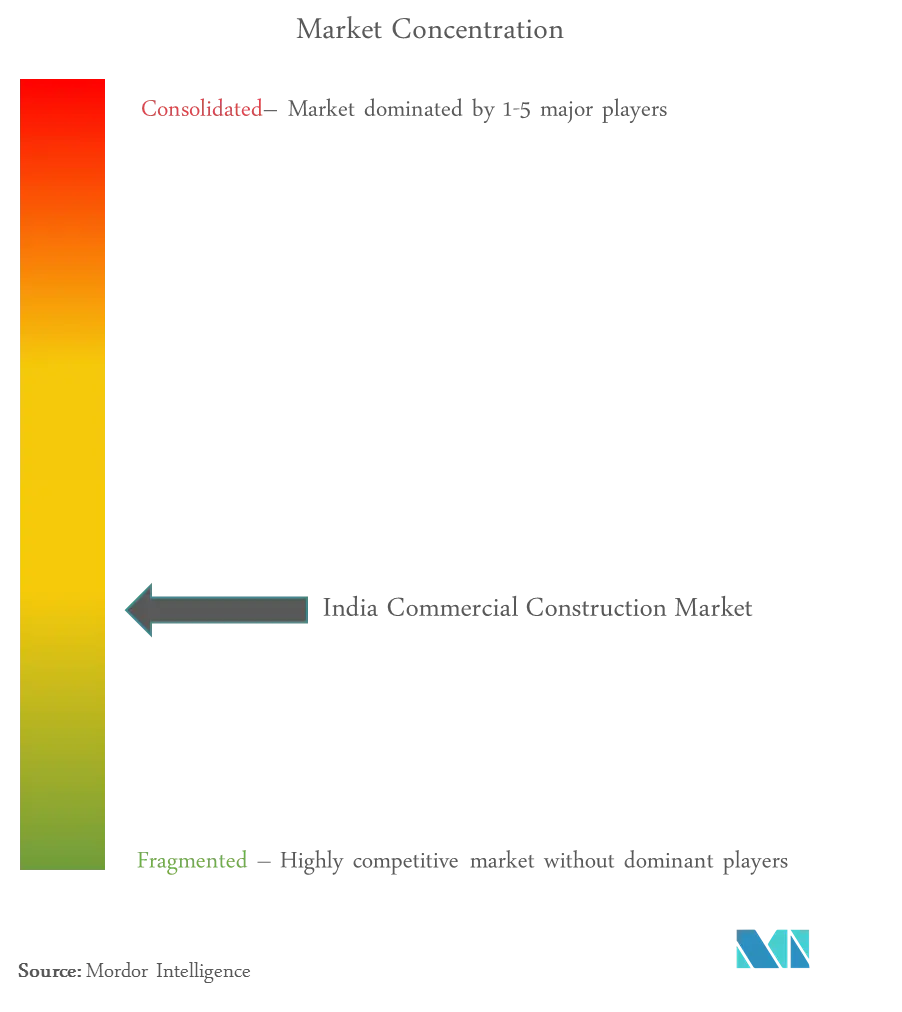

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

India Commercial Construction Market Analysis

The market for Commercial Construction in India is estimated to be valued at more than USD XX billion and is estimated to grow at a CAGR of more than 11.5% during the forecast period.

Efforts are expected to continue to ease the regulations, multiply the organizations, amend the Foreign Direct Investment policies and legislations to generate flow of funds for the upcoming infrastructure with commercial construction forming a major focus. This is also evident from the large scale propaganda of the Government of India to focus on a 5 Trillion USD economy, launching of various investment initiatives by the Finance Ministry viz. innovative financing vehicles such as Infrastructure Debt Funds (IDFs), Infrastructure Investment Trusts (InvITs), Real Estate Investment Trusts (REITs), mainstreaming of Public Private Partnerships (PPPs) across industry through viability gap funding, and establishment of the National Investment and Infrastructure Fund (NIIF), which would be key initiatives for stabilizing industry's output post COVID-19 outbreak.

A brilliant example is the DLF-GIC Joint venture, a private Real Estate Investment Trust (REIT), to invest around USD 650 Million for the development of a 6.8 million square feet information technology park in Chennai, and the country's largest mall in Gurugram, next to Cybercity, having 2.5 Million sq. feet built up area. Further, Global private funds, including Blackstone Group, Canada Pension Plan Investment Board (CPPIB), APG Asset Management, Xander Group and GIC, have started investing in the retail sector to diversify their investment portfolios in the country and more funds are eyeing such alliance opportunities. To add, in one of India's biggest transactions to help build a property investment platform, private equity major Warburg Pincus entered a USD 1 billion alliance with Mumbai-based developer Runwal Group to fund retail-led mixed-use projects across the country. Companies exiting China and entering Indian market, in search of retail and office space, post COVID-19 outbreak, would be a bonus in the economic slowdown.

Market experts are expecting around 15% decline in the office space absorption, complementing the fact that 30% decline in the same has been recorded in the first three months of this year, 2020, for Grade A segment of office built up space, across major metropolitans, though net office space absorption is still expected to be higher than previous year, backed by significant pre-booking or pre-leasing of space by occupiers. Labor shortages could be another issue post lockdown, as most of the labor have returned to their villages and it would be very dicey, if construction, the second largest employer, after Agriculture, faces tough time fetching minimum number of laborers at the construction sites, despite endless initiatives by the govt.

India Commercial Construction Market Trends

This section covers the major market trends shaping the India Commercial Construction Market according to our research experts:

Growth in Commercial Space Market unaffected

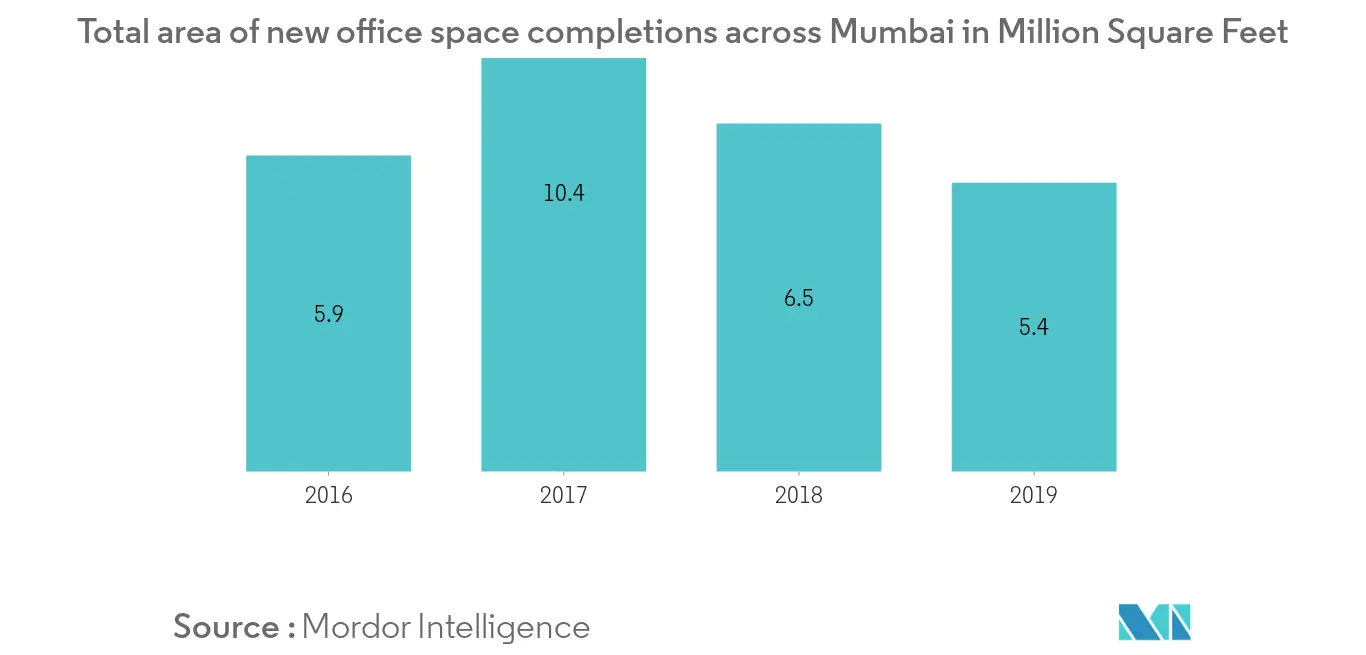

Across the major metropolitans, including Delhi-NCR, Hyderabad, Bangalore, Chennai, Mumbai, Ahmedabad and Pune, office space absorption has been showing a jump year on year, in the past 5 years. Despite last quarter of the Financial Year, 2020, resulting in an economic slowdown and decrease in the absorption of Grade A office spaces by 30% (as per reputed and trustable sources), the net absorption has been higher as compared to the previous F.Y. Though, market experts have been expecting a decrease in the office space absorption by around 15%, post Covid-19 breakout, complementary decrease in supply due to labor shortages and Government regulations, is bound to occur. As a result, the sync in demand-supply is being expected to prevail, and the incumbent revision in rentals or changes in rental contract terms is not expected. It is worth mentioning that the decreased demand is mainly because US-based companies, which typically lease between 40-50% of annual net offtake of office space, are the biggest occupiers in the country, followed by local companies that occupy nearly 30%, while Europe, one of the worst affected by Covid-19, contribute 10% of the overall leasing in the Indian office market. Despite an expected decline in demand and supply, net demand of office space in 2020, is still expected to be well over the past 5-year average, backed by significant pre-booking or pre-leasing of space by occupiers.

Further, commercial retail space in shopping malls, office space in IT Parks, are set to face a major improvement, due to the Real Estate Investment Trust (REIT) coming into picture, resulting in increased flow of investments. DLF-GIC Joint venture, a private REIT, is a good example, and is expected to increase investments worth several Hundreds of USD Million in the commercial space market of the country.

Government Initiatives backed by Foreign Investments driving the Industry:

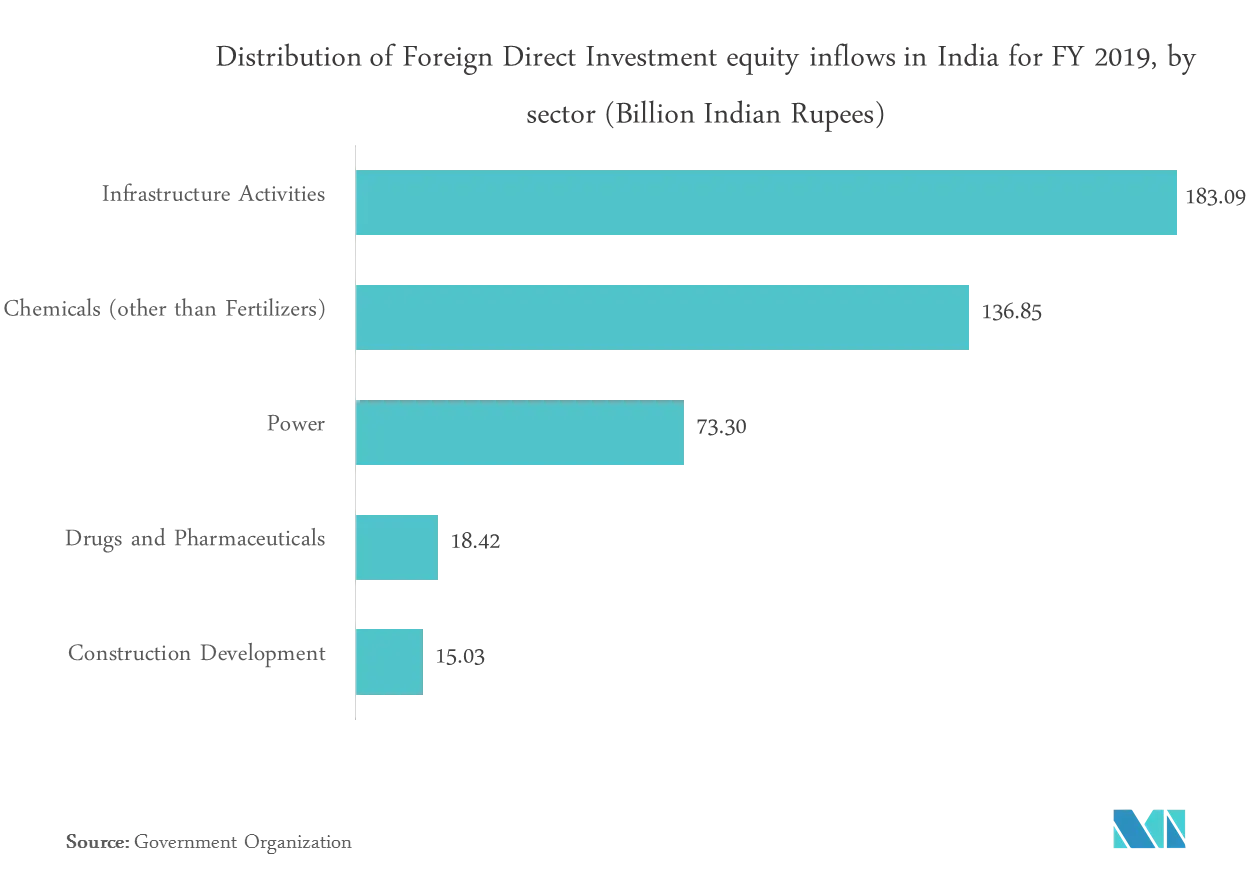

Five key regulatory reforms that are impacting Commercial Construction market growth are, Real Estate Regulation and Development Act (2016), resulting in increased transparency; Ind AS 115, an Indian Accounting Standard that directs the reality firms to shift from percentage completion to project completion, though its restraining effect is expected to be short term, till developers get adjusted; Insolvency and Bankruptcy Code, which urges stakeholders to settle bad loans, resulting in direct benefit to the industry; establishment of Real Estate Investment Trusts (REITs), which aim at raising avenues for generating finance and alternate investments; Goods And Services Act (GST), having mixed Impact on the suppliers and buyers. Besides, 100% FDI in construction sector under automatic route is permitted in completed projects for operations and management of townships, malls/shopping complexes, and business constructions which is a significant reason behind the fact that construction sector has proven to be a major FDI recipient sector for India.

Ample amount of construction opportunities have been floated in the market by the Government of India as a result of various development schemes like Make in India, Smart Cities Mission, Swachh Bharat Mission, Pradhan Mantri Awas Yojana, Atal Mission for Rejuvenation and Urban Transformation (AMRUT), National Heritage City Development and Augmentation Yojana (HRIDAY), Industrial Corridors Development, Modified Industrial Infrastructure Upgradation Scheme, Mega Ports Development, Railway Stations Development/ Re-development & Railway Line addition, and Infrastructure Debt Funds, resulting in growth across various construction segments, including commercial construction. Further, Government initiatives, diluting monetary commitments for the middle class and easing the liabilities have increased the mass investment for the public development schemes, including retail and contributions towards commercial complex spaces. In this regard, Real Estate Regulation and Development Act 2016 and GST Regime Implications, Model Guidelines for Development and Regulation of Retirement Homes are significant. All these initiatives could prove to be helpful in the post COVID-19 outbreak, where experts are predicting a slowdown due to lower revenues and labor shortages.

Moreover, besides the market trends, Sustainable Building, Green Building, Construction Equipment, Construction Vehicle Segments are the major Industry Trends leading to Commercial Construction Market growth.

India Commercial Construction Industry Overview

The India commercial construction market is highly competitive, with the major local and international players having created enough competitive environment in the sector. Still, the market opens opportunities for small and medium players due to increasing govt investments in the sector. The market presents opportunities for growth during the forecast period, which is expected to further drive market competition. With large players competing others for a significant share leaves the industry with no observable levels of consolidation.

A few key players in the market include DLF Ltd., Unitech Group, Sobha Ltd, Prestige Group, and Omaxe Ltd. - the market share of DLF and Unitech being primarily in Delhi-NCR (Gurugram) and distributed unevenly elsewhere. The Government regulations make it quite easy for any player, local, national or multi national to enter the market with ease and create its own share.

India Commercial Construction Market Leaders

-

DLF Limited

-

SOBHA Limited

-

Prestige Group

-

Unitech Group

-

Omaxe Limited

-

NBCC Limited

-

PCP International Limited

-

Bharti Realty Limited

-

B L Kashyap and Sons Limited

-

Oberoi Realty Limited

*Disclaimer: Major Players sorted in no particular order

India Commercial Construction Market Report - Table of Contents

-

1. INTRODUCTION

-

1.1 Study Assumptions

-

1.2 Scope of the Study

-

-

2. RESEARCH METHODOLOGY

-

2.1 Analysis Methodology

-

2.2 Research Phases

-

-

3. EXECUTIVE SUMMARY

-

4. MARKET INSIGHTS

-

4.1 Current Market Scenario

-

4.2 Technological Trends

-

4.3 Government Regulations

-

4.4 Value Chain / Supply Chain Analysis

-

4.5 Overview of Commercial Construction Market in India

-

4.6 Brief on Construction Costs (average cost, office and retail space, per sq feet)

-

4.7 Insights into the new office space completions (sq. feet)

-

4.8 Insights into the share of office space absorption (%, healthcare, telecom, construction and allied services)

-

4.9 Impact of COVID-19 on Indian Commercial Construction Market (Analyst View)

-

-

5. MARKET DYNAMICS

-

5.1 Drivers

-

5.2 Restraints

-

5.3 Opportunities

-

5.4 Industry Attractiveness - Porter's Five Forces Analysis

-

5.4.1 Bargaining Power of Suppliers

-

5.4.2 Bargaining Power of Consumers

-

5.4.3 Threat of New Entrants

-

5.4.4 Threat of Substitutes

-

5.4.5 Intensity of Competitive Rivalry

-

-

-

6. MARKET SEGMENTATION

-

6.1 By End Use

-

6.1.1 Office Building Construction

-

6.1.2 Retail Construction

-

6.1.3 Hospitality Construction

-

6.1.4 Institutional Construction

-

6.1.5 Others

-

-

-

7. COMPETITIVE LANDSCAPE

-

7.1 Market Concentration Overview

-

7.2 Company Profiles

-

7.2.1 Delhi Land And Finance Limited (DLF Ltd.)

-

7.2.2 Sobha Limited

-

7.2.3 Prestige Group

-

7.2.4 Unitech Group

-

7.2.5 Omaxe Ltd.

-

7.2.6 NBCC Limited

-

7.2.7 Punjab Chemi Plants Limited (PCP International Ltd)

-

7.2.8 Bharti Realty Ltd.

-

7.2.9 B. L. Kashyap and Sons Limited (BLK Ltd.)

-

7.2.10 Oberoi Reality Ltd.

-

-

-

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

-

9. APPENDIX

-

9.1 Macroeconomic Indicators (GDP Distribution by Activity, Contribution of Commercial Construction to economy)

-

9.2 Insights on Capital Flows (investments in Commercial Construction Sector)

-

India Commercial Construction Industry Segmentation

A complete background analysis of the India Commercial Construction market, which includes an assessment of the economy, market overview, market size estimation for key segments, and emerging trends in the market, market dynamics, and key company profiles are covered in the report.

India Commercial Construction Market Research FAQs

What is the current India Commercial Construction Market size?

The India Commercial Construction Market is projected to register a CAGR of 11.5% during the forecast period (2024-2029)

Who are the key players in India Commercial Construction Market?

DLF Limited, SOBHA Limited, Prestige Group, Unitech Group, Omaxe Limited, NBCC Limited, PCP International Limited, Bharti Realty Limited, B L Kashyap and Sons Limited and Oberoi Realty Limited are the major companies operating in the India Commercial Construction Market.

What years does this India Commercial Construction Market cover?

The report covers the India Commercial Construction Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the India Commercial Construction Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

India Commercial Construction Industry Report

Statistics for the 2024 India Commercial Construction market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. India Commercial Construction analysis includes a market forecast outlook 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.