India Aviation, Defense, And Space Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 19.81 Billion |

| Market Size (2030) | USD 26.32 Billion |

| Growth Rate (2025 - 2030) | 5.84% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Aviation, Defense, And Space Market Analysis by Mordor Intelligence

The India Aviation, Defense, And Space Market size is estimated at USD 19.81 billion in 2025, and is expected to reach USD 26.32 billion by 2030, at a CAGR of 5.84% during the forecast period (2025-2030).

The technology sectors are undergoing a significant transformation driven by ambitious modernization initiatives and policy reforms. The Ministry of Civil Aviation's Vision 2040 outlines plans for expanding airport infrastructure to 190-200 operational airports, with projected capital investments of EUR 34-42 billion. This expansion aligns with the growing fleet requirements, as Indian carriers are expected to procure 500-520 new aircraft between 2021 and 2026, bringing the total fleet size to over 1,200 aircraft. The government's focus on developing India as an aviation maintenance hub is evidenced by recent policy changes, including a GST reduction from 18% to 5%. It plans to lease airport land at discounted rates for MRO facilities.

The defense sector is witnessing a decisive shift toward indigenous defense manufacturing and self-reliance. The Indian Ministry of Defense has enforced an import embargo on 208 defense items, including artillery guns and assault rifles, with planned contracts worth EUR 48.31 billion by 2027. The military modernization program is substantial, with requirements for 180 combat jets, 400 helicopters, and approximately 100 UAVs to be inducted from 2025 to maintain strategic capabilities. This indigenization drive has created opportunities for domestic manufacturers and international companies seeking strategic partnerships in India.

The commercial space sector is experiencing unprecedented privatization and commercialization initiatives. ISRO is currently sourcing satellite and launch vehicle components from over 200 suppliers based in India, with plans to completely outsource launch vehicle manufacturing to private players. The establishment of New Space India Limited (NSIL) as the commercial arm of ISRO marks a significant step toward enabling Indian industries to scale up high-technology manufacturing. The government plans to share 70% of the current space program revenue with private firms and entities, estimated to be worth EUR 1.3 billion, spanning 50 launches and 27 satellites over five years.

The maintenance, repair, and overhaul (MRO) segment is poised for substantial growth through strategic international partnerships and domestic capability enhancement. Currently, about 85% of maintenance work for domestic scheduled carriers is conducted overseas, presenting a significant opportunity for domestic market development. The government's initiatives to establish India as an MRO hub have attracted foreign investments and partnerships between international players and local MRO providers. These developments are complemented by infrastructure improvements at major airports and the creation of dedicated MRO facilities, positioning India to capture a larger share of the regional aviation maintenance market.

India Aviation, Defense, And Space Market Trends and Insights

Reforms in Defense Policies

The Indian government has implemented significant policy reforms to boost domestic defense manufacturing and reduce import dependence. Through the Defence Production and Export Promotion Policy 2020, the Ministry of Defense has allocated a substantial capital procurement budget of EUR 6.25 billion specifically for domestic procurement in FY2020. This policy framework aims to achieve comprehensive self-reliance in defense manufacturing while promoting exports of defense equipment and services. The introduction of the Green Channel Status Policy has further encouraged private sector investments, with 14 firms already granted this status by the end of 2020, streamlining procurement processes and enhancing industry participation.

The government has enforced an import embargo on 208 defense items, including critical equipment like artillery guns and assault rifles, demonstrating its commitment to indigenous production. This strategic move is complemented by enhanced Foreign Direct Investment (FDI) policies that now permit up to 74% investment through the automatic route in defense manufacturing, with the possibility of higher FDI under government approval. For existing licensees, the policy allows the infusion of new FDI up to 49% through simple declarations within a 30-day timeframe, creating a more conducive environment for international partnerships while maintaining domestic control over strategic assets.

Growing Military Expenditure and Modernization

India's defense modernization initiatives have gained significant momentum, driven by evolving security challenges and the need for technological advancement. In September 2023, the Indian Army announced ambitious plans for next-generation guns to be exclusively developed and manufactured by domestic firms, with an estimated investment of USD 60 billion. This initiative specifically focuses on developing lighter and more adaptable towed gun systems incorporating cutting-edge defense technology, representing a major shift towards indigenous weapons development and manufacturing capabilities.

The country's strategic focus on becoming a global manufacturing hub for advanced military equipment is evidenced by recent developments in artillery ammunition production. In February 2023, the Ministry of Defense awarded contracts to five domestic manufacturers for producing approximately two thousand 155mm terminally guided munitions (TGMs), catering to various caliber requirements of the Army's artillery units. This development is particularly significant as 155mm ammunition is utilized by more than 75 armies worldwide, positioning India as a potential major supplier in the global defense market while strengthening its domestic manufacturing capabilities.

Infrastructure Development and Aviation Growth

The Indian aviation sector has witnessed substantial infrastructure development, marked by significant investments in new airport construction and modernization of existing facilities. The recent inauguration of the Maryada Purushottam Shri Ram International Airport in Ayodhya in December 2023 exemplifies the government's commitment to expanding aviation infrastructure across the country. This expansion is driven by the increasing congestion at existing airports and the need to accommodate growing air traffic, leading to the development of new aviation hubs in various regions of the country.

The modernization of India's aviation fleet is evidenced by major aircraft acquisition programs by leading carriers. Air India's strategic fleet expansion, demonstrated by its acquisition of A350-900 aircraft through a finance lease with HSBC in September 2023, marks a significant step in upgrading the country's aviation capabilities. The airline's commitment to inducting six A350-900s, with five units scheduled for delivery by March 2024, reflects the industry's focus on incorporating modern, fuel-efficient military aircraft to enhance operational capabilities and passenger experience. These developments are complemented by continuous improvements in airport infrastructure and support facilities, creating a comprehensive ecosystem for aviation growth. Furthermore, the integration of advanced aviation systems and aviation electronics is pivotal in enhancing the overall efficiency and safety of air travel.

Segment Analysis

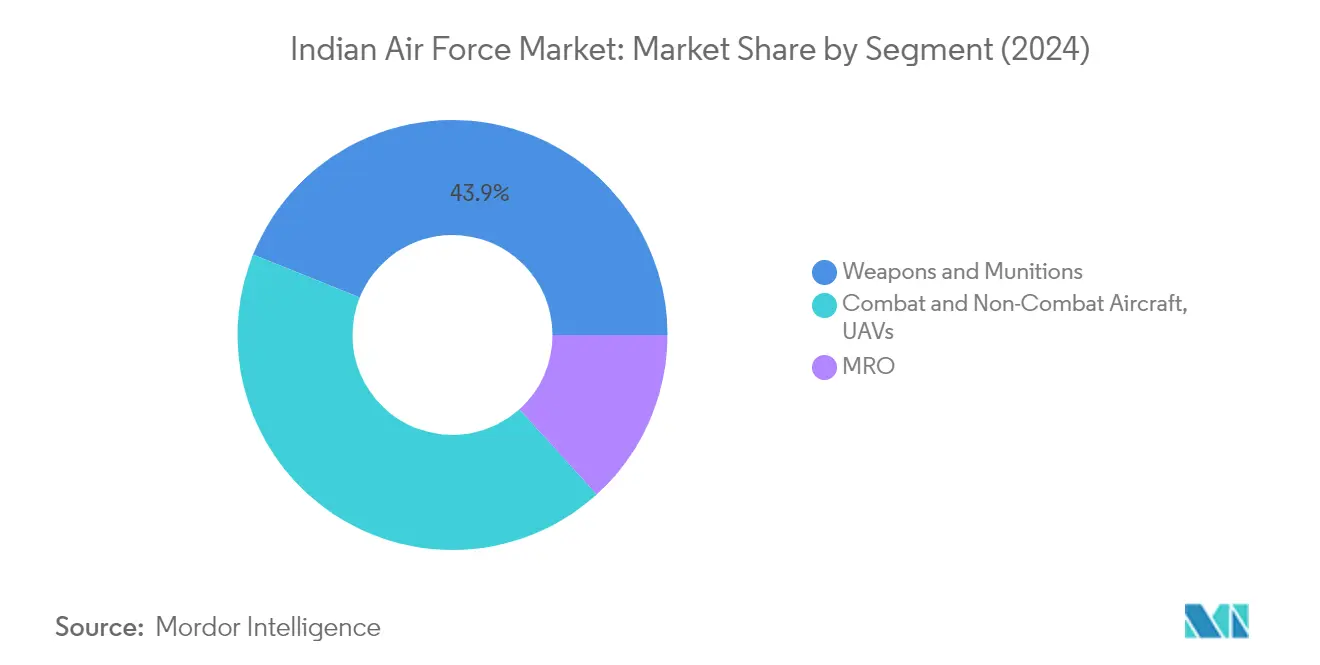

Weapons and Munitions Segment in Indian Air Force Market

The Weapons and Munitions segment currently holds the largest share in the Indian Air Force market, accounting for approximately 44% of the total market value in 2024. This dominance is primarily driven by the increasing focus on indigenous missile systems development programs and ammunition manufacturing capabilities. The segment's growth is further supported by ongoing modernization efforts of the Indian Air Force's weapons systems, including the development and procurement of advanced air-to-air missiles, precision-guided munitions, and smart weapons. The government's push for self-reliance in defense manufacturing through initiatives like 'Make in India' has led to increased participation from private sector companies in weapons and ammunition production, strengthening the segment's market position.

Combat and Non-Combat Aircraft, UAVs Segment in Indian Air Force Market

The Combat and Non-Combat Aircraft, UAVs segment is experiencing rapid growth in the Indian Air Force market, driven by significant investments in fleet modernization and indigenous aircraft development programs. This growth is supported by the increasing focus on unmanned aerial systems for surveillance and combat operations, as well as the development of next-generation fighter aircraft. The segment's expansion is further bolstered by ongoing programs like the Light Combat Aircraft (LCA) Tejas and various UAV development initiatives. The Indian government's emphasis on developing domestic aerospace manufacturing capabilities and the establishment of maintenance, repair, and overhaul (MRO) facilities are also contributing to the segment's robust growth trajectory.

Remaining Segments in Air Force Market

The MRO (Maintenance, Repair, and Overhaul) segment plays a crucial supporting role in the Indian Air Force market, ensuring the operational readiness and longevity of the existing fleet. This segment is particularly important given India's diverse aircraft inventory and the need for regular maintenance and upgrades of both indigenous and imported platforms. The segment is witnessing transformation through the incorporation of advanced technologies and the establishment of specialized maintenance facilities across the country. The government's focus on developing domestic MRO capabilities and reducing dependence on foreign service providers is reshaping this segment's landscape within the Indian Air Force market.

Segment Analysis: Army

Armored Vehicles, Helicopters, and UAVs Segment in Indian Army Market

The Armored Vehicles, Helicopters, and UAVs segment dominates the Indian Army market, accounting for approximately 60% of the total market share in 2024. This segment's prominence is driven by India's ongoing military modernization initiatives and the increasing focus on strengthening its armored capabilities. The segment encompasses a wide range of platforms including main battle tanks, infantry combat vehicles, light combat helicopters, and various categories of UAVs for surveillance and combat operations. The Indian Army's requirements for advanced armored vehicles like the Arjun MBT, T-90 Bhishma tanks, and the Future Infantry Combat Vehicle (FICV) program are contributing significantly to this segment's growth. Additionally, the procurement of helicopters, such as the HAL Light Combat Helicopter (LCH) and various UAV platforms, for surveillance and reconnaissance missions further strengthens this segment's market position. The government's emphasis on indigenous production through initiatives like 'Make in India' and the implementation of import embargoes on various military platforms has created substantial opportunities for domestic manufacturers in this segment.

Remaining Segments in Indian Army Market

The Weapons and Munitions segment, along with the Maintenance, Repair, and Overhaul (MRO) segment, form crucial components of the Indian Army market segment. The Weapons and Munitions segment focuses on the development and procurement of various artillery systems, small arms, ammunition, and missile systems to enhance the army's firepower capabilities. This includes indigenous projects, such as the Advanced Towed Artillery Gun System (ATAGS) and various missile development programs. The MRO segment plays a vital role in maintaining the operational readiness of the army's extensive fleet of vehicles and equipment, ensuring their longevity and combat effectiveness. The increasing complexity of modern military equipment and the growing focus on extending the service life of existing platforms have made the MRO segment particularly important for the Indian Army's operational capabilities.

Segment Analysis: Navy

Naval Vessel, Combat and Non-Combat Aircraft, UAV Segment in Indian Naval Market

The naval vessel, combat and non-combat aircraft, and UAV segment dominates the Indian naval market, accounting for approximately 65% of the total market revenue in 2024. This substantial market share is driven by India's ambitious naval modernization programs, including the indigenous aircraft carrier INS Vikrant, four Scorpene submarines, four destroyers, and two frigates that are currently under construction. The Indian Navy's vision to maintain a fleet of 200 warships by 2027 further strengthens this segment's position. Additionally, the development of home-grown UAVs and the increasing focus on surveillance capabilities have contributed significantly to this segment's dominance. The segment also benefits from the government's emphasis on indigenous manufacturing and the participation of major shipyards like Mazagon Dock Shipbuilders Ltd, Cochin Shipyard, and Garden Reach Shipbuilders & Engineers in various naval vessel construction projects.

Weapons and Munitions Segment in Indian Naval Market

The weapons and munitions segment is projected to experience the highest growth rate in the Indian naval market between 2024 and 2029. This growth is primarily driven by the increasing focus on enhancing naval combat capabilities through advanced weaponry systems. The segment's expansion is supported by significant developments in indigenous missile systems, including BrahMos cruise missiles and various anti-ship and anti-submarine warfare systems. The government's push for self-reliance in defense manufacturing, particularly through initiatives like the Defense Production and Export Promotion Policy, has created new opportunities for local manufacturers in this segment. The development of advanced torpedo systems, naval guns, and other maritime weapons systems by companies like Bharat Dynamics Limited and other defense public sector undertakings has further strengthened this segment's growth trajectory.

Remaining Segments in Indian Naval Market

The Maintenance, Repair, and Overhaul (MRO) segment plays a crucial role in maintaining the operational readiness of India's naval fleet. This segment encompasses a wide range of services, from routine maintenance of vessels and aircraft to major overhauls and modernization programs. The segment benefits from the increasing complexity of naval systems and the growing need for regular maintenance of the expanding fleet. The establishment of new maintenance facilities and partnerships with international MRO providers has enhanced the capability of this segment. The government's focus on developing India as a regional MRO hub, coupled with initiatives to improve infrastructure and reduce tax burden on MRO activities, has created a favorable environment for this segment's growth.

Segment Analysis: Space

Space Technology, Applications and Sciences Segment in Indian Space Market

Space Technology, Applications and Sciences represents the dominant segment in India's space market, accounting for approximately 89% of the total market revenue in 2024. This segment encompasses critical areas including satellite technology development, implementation of satellite systems for scientific missions, technological missions, and various space applications. The segment's strength is reinforced by ISRO's focus on developing indigenous capabilities across the entire space value chain, from satellite manufacturing to space launch services. The segment benefits from significant government support through the Department of Space and various research institutions. Major projects under this segment include the development of advanced satellite platforms, earth observation systems, and communication satellites. The segment's dominance is further strengthened by increasing private sector participation through initiatives like IN-SPACe and the transfer of technology to Indian industries.

INSAT Satellite System Segment in Indian Space Market

The INSAT Satellite System segment is projected to experience substantial growth between 2024-2029, driven by increasing demand for satellite systems-based communication services and broadcasting requirements. This growth is supported by the government's push for digital connectivity across remote areas and the rising need for satellite-based navigation systems. The segment is witnessing significant technological advancements, particularly in areas such as high-throughput satellites and improved communication capabilities. The growth is further accelerated by the increasing participation of private players in satellite manufacturing and operations. The segment's expansion is also supported by ISRO's plans to enhance the INSAT fleet with next-generation satellites featuring advanced capabilities. The implementation of the new Indian Space Policy and the establishment of NSIL as a commercial arm have created additional growth opportunities in this segment.

Remaining Segments in Indian Space Market

The remaining segments in India's space market primarily consist of specialized space services, ground infrastructure development, and support activities. These segments play a crucial role in supporting the overall space ecosystem through various specialized services and infrastructure development. The ground segment includes tracking stations, control centers, and data reception facilities that are essential for space operations. Support activities encompass areas such as space exploration, research and development, and technology demonstration projects. These segments are witnessing increased private sector participation following the government's initiatives to open up the space sector. The segments also benefit from international collaborations and technology transfer agreements with global space agencies and companies. The development of new space parks and specialized facilities across the country is further enhancing the capabilities of these supporting segments.

Segment Analysis: Civil Aviation

Commercial Aviation Segment in Civil Aviation Market

The commercial aviation segment dominates India's civil aviation market, driven by the robust growth in domestic air travel and fleet expansion plans of major carriers. Indian carriers are anticipated to procure 500-520 new aircraft between 2024-2026, bringing the total fleet size to over 1,200 aircraft by 2026. The segment's growth is further supported by recent government initiatives to develop India as an MRO hub, including GST reduction from 18% to 5%, discounted airport land lease rates, and reduction in royalty charges. These policy changes are expected to attract more foreign investments and foster partnerships between international players and local MRO providers. Currently, about 85% of the MRO work for domestic scheduled carriers is carried out overseas, presenting a significant opportunity for domestic market development.

Business Jet Segment in Civil Aviation Market

The business jet segment is experiencing rapid growth in the Indian civil aviation market, with significant expansion expected between 2024-2029. This growth is primarily driven by increasing demand from private operators and the trend toward aircraft management companies offering comprehensive services including charter, maintenance, and management under one roof. The segment's development is supported by established players upgrading their heavy-maintenance capabilities and OEMs like Bombardier, Embraer, Cessna, Falcon, and Gulfstream strengthening their presence in India through enhanced spare parts availability and service networks. The market is also benefiting from the consolidation trend where small fleet aircraft owners are increasingly shifting to aircraft management companies for more efficient operations and maintenance support.

Segment Analysis: Bearings Market Potential

Local Manufacturing Segment in Indian Aviation, Defense and Space Bearings Market

Local manufacturing dominates the Indian aviation, defense and space bearings market, accounting for approximately 62% of the total market value in 2024. The segment's strength comes primarily from manufacturing facilities in Bengaluru, Ludhiana and Chandigarh, which are crucial in supplying bearings for various military applications including the legacy Russian helicopter fleet. These locally manufactured bearings undergo rigorous material and quality checks at ISRO and DRDO facilities, followed by operational testing at Air Force bases in Barrackpore, Bengaluru, Hyderabad and other maintenance facilities. The segment's growth is being driven by increasing demand from engine applications across aviation, defense and space sectors, as well as emerging opportunities in naval vessels, armored vehicles and MRO services.

Import Segment in Indian Aviation, Defense and Space Bearings Market

The import segment of the Indian aviation, defense and space bearings market continues to play a vital role, particularly in specialized applications requiring high precision and advanced metallurgy. This segment faces unique challenges as many critical bearings are monopolized by international OEMs, with restrictions even on disassembly for inspection or maintenance. The growth in this segment is being driven by the increasing demand for bearings in jet engines for programs like Tejas Mk2, Advanced Medium Combat Jet, Naval Carrier Borne Advanced Combat Jet, and UAVs. The segment's development is also influenced by the government's push for local manufacturing partnerships with international OEMs to gain access to technical specifications and design expertise for high-precision bearings manufacturing.

Competitive Landscape

Top Companies in India Aviation, Defense, And Space Market

The market is dominated by established players like Hindustan Aeronautics Limited, Bharat Electronics, Tata Advanced Systems, Larsen & Toubro, and Mahindra Defense Systems, who have demonstrated strong capabilities across multiple domains. These companies are increasingly focusing on the indigenous development of advanced platforms and systems, with significant investments in research and development facilities. Strategic partnerships and technology transfer agreements with global OEMs have become a key trend, enabling domestic players to enhance their manufacturing capabilities and product portfolios. Companies are expanding their presence across the value chain through vertical integration while simultaneously developing specialized expertise in niche areas like avionics, unmanned systems, and space technologies. The industry has seen a marked shift towards digital transformation and Industry 4.0 adoption, with players incorporating advanced manufacturing processes, automation, and data analytics to improve operational efficiency.

Market Structure Evolving Through Strategic Consolidation

The market exhibits a hybrid structure with state-owned enterprises maintaining dominance in strategic sectors while private players are gaining ground through innovation and agility. Major conglomerates like Tata, L&T, and Mahindra have established dedicated defense subsidiaries, leveraging their industrial expertise and financial strength to compete effectively. The industry is witnessing increased consolidation through mergers and acquisitions, particularly among mid-sized players seeking to achieve scale and complement capabilities. International defense majors are establishing joint ventures and manufacturing facilities in India, responding to the government's push for localization and technology transfer.

The competitive dynamics are being reshaped by the emergence of specialized technology firms and startups focusing on niche capabilities in areas like artificial intelligence, cybersecurity, and unmanned systems. Traditional players are actively pursuing strategic partnerships and investing in these emerging companies to access new technologies and talent pools. The market is characterized by long-term relationships and complex procurement processes, with successful players demonstrating strong project execution capabilities and maintaining robust supplier networks. The industry structure is evolving with increased private sector participation in previously restricted domains like space and advanced weapons systems.

Innovation and Localization Drive Future Success

Success in this market increasingly depends on companies' ability to develop indigenous technological capabilities while maintaining cost competitiveness. Established players are focusing on expanding their intellectual property portfolios, investing in advanced manufacturing facilities, and developing strong systems integration capabilities. The ability to form effective partnerships, both domestic and international, has become crucial for accessing new technologies and markets. Companies are also emphasizing the development of comprehensive support ecosystems, including maintenance, repair, and upgrade services, to ensure long-term customer relationships.

Market contenders are finding opportunities by focusing on specialized niches and developing innovative solutions for specific military requirements. The increasing emphasis on self-reliance in defense production is creating opportunities for new entrants with strong technological capabilities. Success factors include the ability to navigate complex regulatory requirements, maintain strong relationships with defense research organizations, and demonstrate reliable project execution capabilities. Companies are also focusing on developing export capabilities to achieve scale and reduce dependence on domestic procurement cycles. The market rewards players who can maintain agility while building long-term capabilities and relationships. The aerospace and defense sector is particularly poised for growth as companies leverage advancements in defense technology to enhance their offerings.

India Aviation, Defense, And Space Industry Leaders

-

Hindustan Aeronautics Limited (HAL)

-

Bharat Electronics Limited (BEL)

-

Larsen & Toubro Limited

-

Adani Group

-

Indian Space Research Organisation (ISRO)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2023: The Indian government approved defense acquisition projects worth USD 2.67 million. The project includes the acquisition of 97 Tejas light combat aircraft and 156 Prachand combat helicopters. Moreover, 98% of the total procurement will be sourced from domestic industries, thereby significantly boosting the Indian defense industry.

- February 2023: Air India selected market-leading Boeing aircraft, including the B737 MAX, B787 Dreamliner, and B777X. Moreover, Air India plans to acquire 190 Boeing B737 MAXs, including B737-8s and B737-10s, with options for 50 more jets to serve the domestic and international networks.

India Aviation, Defense, And Space Market Report Scope

The India aviation, defense, and space market comprises the entire aviation, defense, and space industry in India.

The market is segmented by air force, army, navy, space, and civil aviation. By air force, the market is segmented into combat and non-combat aircraft (fixed wing and helicopter) and UAVs, weapons and munitions, and MRO. By army, the market is segmented into armored vehicles, helicopters, UAVs, weapons and munitions, and MRO. By navy, the market is segmented into naval vessels, combat and non-combat aircraft, UAVs, weapons and ammunition, and MROs. By space, the market is divided into satellite and launch vehicles & rovers. By civil aviation, the market is segmented into commercial aircraft, business jets, and MROs. For each segment, the market size is provided in terms of value (USD).

| Combat and Non-combat Aircraft (Fixed Wing and Helicopter) and UAVs |

| Weapons and Munitions |

| MRO |

| Armored Vehicles, Helicopters, and UAVs |

| Weapons and Munitions |

| MRO |

| Naval Vessels, Combat and Non-combat Aircraft, and UAVs |

| Weapons and Munitions |

| MRO |

| Satellite |

| Launch Vehicles and Rovers |

| Commercial Aircraft |

| Business Jet |

| MRO |

| By Air Force | Combat and Non-combat Aircraft (Fixed Wing and Helicopter) and UAVs |

| Weapons and Munitions | |

| MRO | |

| By Army | Armored Vehicles, Helicopters, and UAVs |

| Weapons and Munitions | |

| MRO | |

| By Navy | Naval Vessels, Combat and Non-combat Aircraft, and UAVs |

| Weapons and Munitions | |

| MRO | |

| By Space | Satellite |

| Launch Vehicles and Rovers | |

| By Civil Aviation | Commercial Aircraft |

| Business Jet | |

| MRO |

Key Questions Answered in the Report

How big is the India Aviation, Defense, And Space Market?

The India Aviation, Defense, And Space Market size is expected to reach USD 19.81 billion in 2025 and grow at a CAGR of 5.84% to reach USD 26.32 billion by 2030.

What is the current India Aviation, Defense, And Space Market size?

In 2025, the India Aviation, Defense, And Space Market size is expected to reach USD 19.81 billion.

Who are the key players in India Aviation, Defense, And Space Market?

Hindustan Aeronautics Limited (HAL), Bharat Electronics Limited (BEL), Larsen & Toubro Limited, Adani Group and Indian Space Research Organisation (ISRO) are the major companies operating in the India Aviation, Defense, And Space Market.

What years does this India Aviation, Defense, And Space Market cover, and what was the market size in 2024?

In 2024, the India Aviation, Defense, And Space Market size was estimated at USD 18.65 billion. The report covers the India Aviation, Defense, And Space Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the India Aviation, Defense, And Space Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: