Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

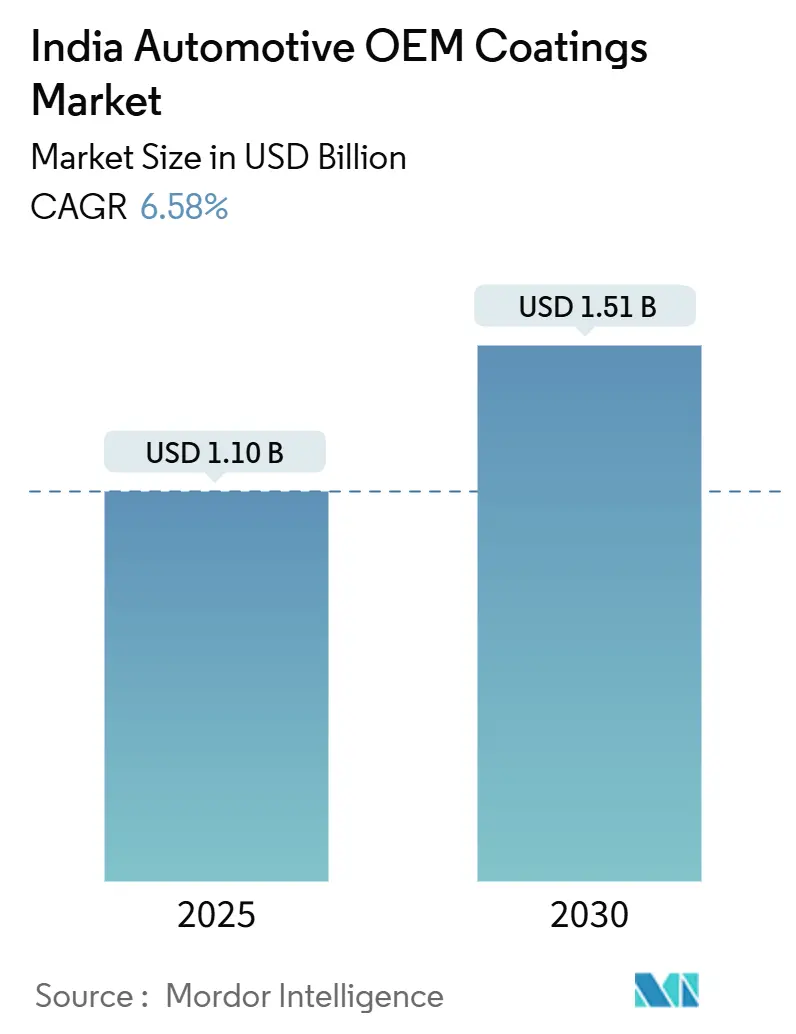

| Market Size (2025) | USD 1.10 Billion |

| Market Size (2030) | USD 1.51 Billion |

| Growth Rate (2025 - 2030) | 6.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automotive OEM Coatings Market Analysis by Mordor Intelligence

The India Automotive OEM Coatings Market size is estimated at USD 1.10 billion in 2025, and is expected to reach USD 1.51 billion by 2030, at a CAGR of 6.58% during the forecast period (2025-2030). The growth arises from a steady preference for premium finishes, regulatory pushes toward low-VOC technologies, and localization incentives that reduce raw-material risk. Passenger cars remain the volume anchor, but multi-layer systems for SUVs and electric vehicles lift value per unit. Resin manufacturers benefit from a USD 3.5 billion Production-Linked Incentive fund that shrinks import dependence and stabilizes pricing. Rising electric-vehicle adoption creates niche demand for corrosion-resistant coatings on battery enclosures, while semiconductor cost inflation encourages automation in paint shops to offset operating expenses. Together, these trends allow the India automotive OEM coatings market to outpace the broader vehicle production cycle despite short-term supply shocks.

Key Report Takeaways

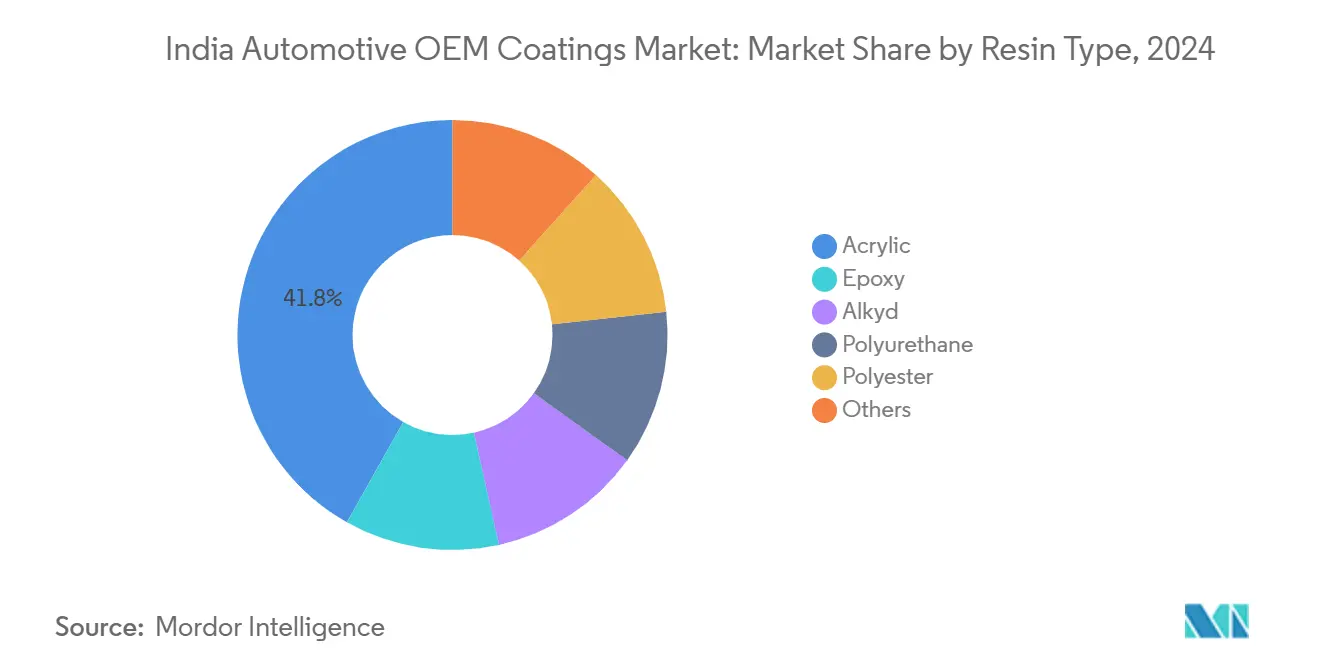

- By resin type, acrylics held 41.81% of the India automotive OEM coatings market share in 2024, whereas polyurethanes are poised for the fastest 6.72% CAGR through 2030.

- By technology, solvent-borne systems commanded 45.44% share of the India automotive OEM coatings market size in 2024, yet water-borne alternatives are expanding at 6.84% CAGR to 2030.

- By coat type, clearcoats contributed 33.96% revenue share in 2024, while e-coats advance at a 6.76% CAGR through 2030.

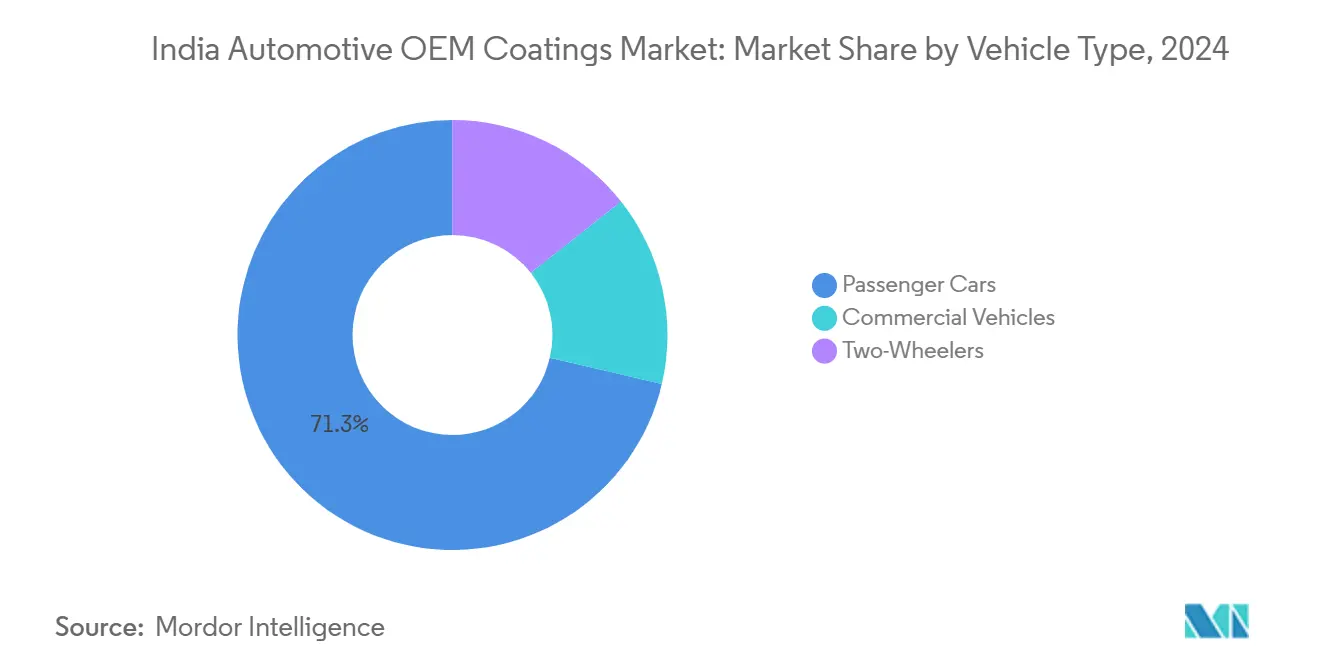

- By vehicle type, passenger cars accounted for 71.34% of the India automotive OEM coatings market size in 2024 and continue to grow at a 6.69% CAGR.

India Automotive OEM Coatings Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in SUV and premium-segment launches | +1.2% | National; early demand in Tamil Nadu, Karnataka, Maharashtra | Medium term (2-4 years) |

| OEM shift to water-borne lines | +0.8% | National; automotive manufacturing hubs | Short term (≤ 2 years) |

| PLI-linked localization of raw materials | +1.5% | Gujarat, Tamil Nadu, Maharashtra | Long term (≥ 4 years) |

| Lightweighting push for high-solid PU systems | +0.9% | Premium vehicle programs by global OEMs | Medium term (2-4 years) |

| EV battery-pack corrosion needs | +0.6% | Emerging EV hubs in Tamil Nadu, Karnataka, Maharashtra | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in SUV and Premium-Segment Launches Post-2024

Premium SUVs require multi-layer, high-gloss coatings with scratch resistance, driving higher value per vehicle. Luxury registrations in South India climbed 19.3% in 2024, prompting OEM investments in advanced spray robots that support two-tone roof designs. Domestic brands now deploy digital paint cells that enable fine color accents once limited to luxury imports. Larger body panels on SUVs expand the coated surface area and raise the consumption of clearcoat and basecoat layers. Certification under the Automotive Research Association of India standards anchors product specifications and keeps the barrier-to-entry high for new suppliers.

PLI-Linked Localization of Resin and Pigment Supply Chains

The Production-Linked Incentive program unlocks domestic investment in acrylic, polyurethane, and pigment plants, trimming currency exposure and shipping delays. Government data show USD 3.5 billion allocated to auto incentives, sparking multi-state resin projects[1]Press Information Bureau, “Revolutionizing Mobility – The Make in India Auto Story,” pib.gov.in. Early localization narrows the historic titanium-dioxide supply gap, giving large integrated suppliers a margin buffer. Smaller import-dependent applicants, however, face working-capital strain during the transition.

Automotive Lightweighting Drives High-Solid PU Demand

Polyurethane systems deliver chip resistance and elasticity ideal for aluminum and composite panels used in lighter vehicles. Their 6.72% CAGR reflects OEM targets to offset semiconductor and battery costs with weight savings. High-solid chemistry lowers VOC output while maintaining film build, aligning with environmental mandates. Material innovators advance PU resin chain-extensions to bond securely to new substrates, widening application beyond body panels to structural battery casings.

EV Battery-Pack Corrosion Requirements Create Niche Epoxy Demand

Uniform e-coat layers shield battery housings from electrolyte leaks and thermal cycling. Epoxy formulations with dielectric properties prevent short circuits and enhance fire safety. A dedicated application center opened by a global coatings major accelerates local prototype work, mirroring earlier facilities abroad. Powder e-coats gain favor for low-temperature cure profiles that protect sensitive battery components, reinforcing a specialized growth pocket inside the India automotive OEM coatings market.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor shortages delaying upgrades | -0.7% | Global; acute for Indian expansion plans | Short term (≤ 2 years) |

| Volatile titanium-dioxide prices | -0.9% | National; heavier on smaller applicators | Medium term (2-4 years) |

| Slow approval of powder clearcoats | -0.4% | National; affects exterior applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Shortages Delay New Paint-Shop Investments

Vehicle makers channel scarce chips to production, postponing capital for automation in coating lines. Advanced robots and inline quality sensors require the same microcontrollers that power infotainment systems. Project deferrals compress short-term demand for new spray booths, giving incumbent applicators extra volume but limiting overall capacity growth. OEMs favor equipment that operates on existing control platforms, restraining rollout of digital overspray-free technologies.

Volatile Titanium-Dioxide Prices Squeeze Tier-2 Applicators

Rutile feedstock tightness swings pigment costs, eroding margins for small‐scale coaters who lack hedging ability. Domestic output meets only one-fifth of demand, forcing reliance on imports denominated in strong currencies. Integrated players with captive mining or long contracts pass cost swings more easily to OEMs, accelerating consolidation. Industry hopes stem from PLI-backed mineral projects that could lift local production but will not materially ease pressure before 2027.

Segment Analysis

By Resin Type: Acrylics Anchor Volume, Polyurethanes Propel Value

Acrylic resins commanded 41.81% of 2024 revenue in the India automotive OEM coatings market. Their versatility across basecoat and clearcoat roles and cost advantage keep them the default choice for passenger cars. Polyurethanes, however, post the highest 6.72% CAGR, reflecting lightweighting and flexibility imperatives. Epoxy grades re-emerge for electric-vehicle enclosures that face chemical and thermal stress. Halloysite nanotube-reinforced epoxy-acrylate emulsions doubled salt-spray endurance in lab work, hinting at next-generation corrosion solutions[2]Frontiers in Chemistry, “Halloysite Nanotubes-Enhanced Epoxy Acrylate Latex Emulsion as a Novel Anticorrosive Protective Coating,” frontiersin.org . Niche bio-based chemistries occupy the “Others” bucket, gaining OEM attention for future zero-isocyanate programs.

Competitive positioning shifts as integrated resin makers leverage in-house pigment synthesis secured under PLI benefits. The India automotive OEM coatings market size tied to acrylics should still rise in absolute terms, though the share migrates incrementally to high-solid PU. Suppliers with balanced resin portfolios cushion against cyclical swings in any single chemistry. Certification processes under ISO 12944 balance experimentation with reliability, keeping barriers to rapid resin substitution high and ensuring gradual, not abrupt, share shifts.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Water-Borne Momentum Builds on Regulatory Tailwinds

Solvent-borne systems retained a 45.44% share in 2024, thanks to performance familiarity, especially for clearcoats. Yet water-borne volumes climb steadily with a CAGR of 6.84%, propelled by India-VI rules and carbon-reduction targets. Sustainability-led products already account for nearly half of a leading global supplier’s sales. Development focus centers on resins that trap hydrophobic segments within polymer shells, delivering high gloss at lower bake temperatures.

Investment announcements for dedicated water-based paint lines in central India shorten delivery cycles for OEMs shifting platforms. The India automotive OEM coatings market size allocated to water-borne solutions is projected to surpass solvent-borne by 2029 if current trajectories hold. Powder and UV-cure technologies reside in the “Others” category. Although powder clearcoats await final exterior certification, their zero-VOC profile ensures long-term relevance. UV systems find niche use on plastic exterior parts where fast tack-free cure enhances throughput.

By Coat Type: Clearcoats Capture the Largest Wallet Share

Clearcoats represented 33.96% value in 2024, validating their role as the final aesthetic and protective layer. Innovations such as pixelated robotic applications allow contrasting roofs and stripes with no masking film, cutting material waste up to 40%. E-coats register 6.76% CAGR as body-in-white surfaces and battery boxes seek uniform corrosion shields. Basecoats gain from metallic and pearl grades popular in SUVs, while primers increasingly adopt water-borne formats under VOC caps.

Adoption patterns tell a value-hierarchy story: OEMs cannot compromise on clearcoat quality, so premium formulations deliver pricing power. Conversely, volumes rest with primers and e-coats that cover the full body. The India automotive OEM coatings market share captured by high-function layers, therefore, skews value distribution. Powder clearcoats, once approved, could upset this balance by mixing top-tier durability with environmental compliance, but timelines remain uncertain.

By Vehicle Type: Passenger Cars Drive Scale, EVs Seed New Niches

Passenger cars held 71.34% of the 2024 volume and are growing at a CAGR of 6.69% owing to stringent cosmetic expectations. Compact SUVs lead color-variant rollout cycles, raising basecoat complexity. Commercial vehicles demand thick, chip-resistant coatings, often high-solid polyurethane blends, to survive rough logistics routes. Two-wheeler makers stress cost-per-part yet increasingly add metallic flake and matte finishes to differentiate models.

Electric three-wheelers reached 50% penetration and two-wheelers 5% in 2024, creating an immediate need for dielectric and thermal-management coatings on battery casings. Though unit economics differ, their fast growth pulls epoxy and powder specialists into new supply opportunities. The India automotive OEM coatings market size attached to passenger cars still dwarfs others, yet incremental growth from EV variants alters the chemistry mix, ensuring robust demand for innovation in corrosion and heat-dissipation layers.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Manufacturing hubs in Tamil Nadu, Gujarat, and Maharashtra anchor more than two-thirds of India’s automotive output, shaping regional coating consumption. Tamil Nadu leads luxury-vehicle demand, prompting suppliers to expand water-borne and clearcoat capacity near Chennai for logistical efficiency.

Gujarat benefits from proximity to petrochemical complexes that feed resin and solvent value chains. A leading domestic paint maker broke ground on a USD 350 million facility near Bharuch, underlining the pull of integrated feedstocks. The India automotive OEM coatings market grows in the West as global OEMs deploy export-oriented platforms from Sanand.

Maharashtra’s Chakan corridor showcases advanced paint automation, including AI-guided robots that adjust atomization parameters in real time. The corridor’s EV programs draw niche suppliers for battery-pack coatings. While the south and west dominate volumes, northern states add incremental capacity tied to commercial-vehicle assemblers who prefer epoxy-rich, high-build systems to suit long-haul duty cycles. Nationally, water-borne lines proliferate fastest where state industrial policies rebate capital on pollution control infrastructure, reinforcing the regional mosaic of technology uptake.

Competitive Landscape

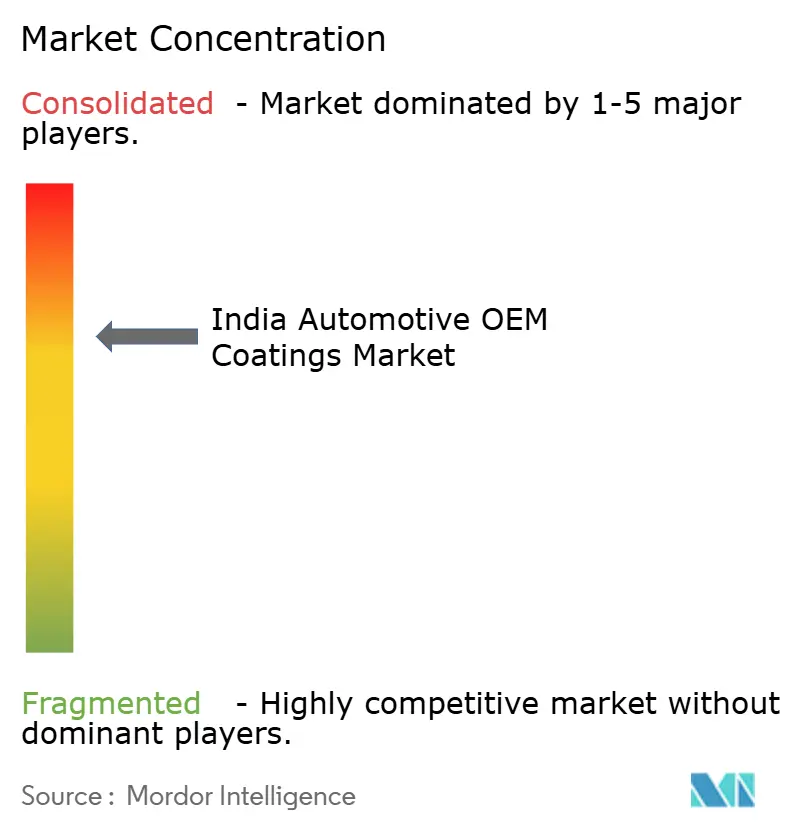

The India automotive OEM coatings market is moderately fragmented and tilting further toward scale players. Asian Paints, Kansai Nerolac, Berger Paints, and the newly formed JSW-Akzo entity run multi-site networks with aligned resin, pigment, and application technology. Potential disruptors surface in powder clearcoats and UV-cure solutions. Early-stage providers partner with equipment OEMs to co-validate processes for regulatory approval. Meanwhile, volatile titanium-dioxide pricing widens the gap between integrated and standalone players, creating acquisition prospects as smaller applicators seek balance-sheet relief. Overall, supplier alliances with equipment makers and raw-material localization continue to shape bargaining power in contract renewals with automotive OEMs.

India Automotive OEM Coatings Industry Leaders

Axalta Coating Systems LLC

BASF

JSW Paints

Kansai Nerolac Paints Limited

PPG Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: AkzoNobel divested its Indian subsidiary to JSW Group, marking a significant shift in the competitive landscape and signaling further consolidation in the coatings sector.

- February 2025: Nippon Paint Holdings acquired full ownership of its India automotive coatings joint ventures, streamlining decision pathways.

India Automotive OEM Coatings Market Report Scope

Automotive OEM coatings are used to manufacture automotive vehicles' body parts. The market is segmented by Resin Type, Technology, and End-User Industry. By Resin, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resins. Technology segments the market into water-borne, solvent-borne, and other coating technologies. End-User Industry segments the market into Passenger Cars, Commercial Vehicles, and ACE. For each segment, the market sizing and forecasts have been done based on revenue (USD million)

By Resin Type

| Epoxy |

| Acrylic |

| Alkyd |

| Polyurethane |

| Polyester |

| Others |

By Technology

| Water-borne |

| Solvent-borne |

| Others |

By Coat Type

| E-coat |

| Primer |

| Basecoat |

| Clearcoat |

By Vehicle Type

| Passenger Cars |

| Commercial Vehicles |

| Two-Wheelers |

| By Resin Type | Epoxy |

| Acrylic | |

| Alkyd | |

| Polyurethane | |

| Polyester | |

| Others | |

| By Technology | Water-borne |

| Solvent-borne | |

| Others | |

| By Coat Type | E-coat |

| Primer | |

| Basecoat | |

| Clearcoat | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| Two-Wheelers |

Key Questions Answered in the Report

What is the current value of the India automotive OEM coatings market?

The market is worth USD 1.10 billion in 2025 and is forecast to reach USD 1.51 billion by 2030.

Which resin type leads demand in India for OEM coatings?

Acrylic resins lead with 41.81% share thanks to versatility and cost efficiency.

How fast are water-borne automotive coatings growing in India?

Water-borne systems are expanding at a 6.84% CAGR through 2030 under VOC regulations.

What vehicle segment drives the highest coating consumption?

Passenger cars account for 71.34% of coating demand and remain the innovation anchor.

Which Indian states host the largest automotive paint facilities?

Tamil Nadu, Gujarat, and Maharashtra house the most significant coating manufacturing clusters.

Page last updated on: