Market Size of In Vitro Diagnostic Industry

| Study Period | 2021 - 2029 |

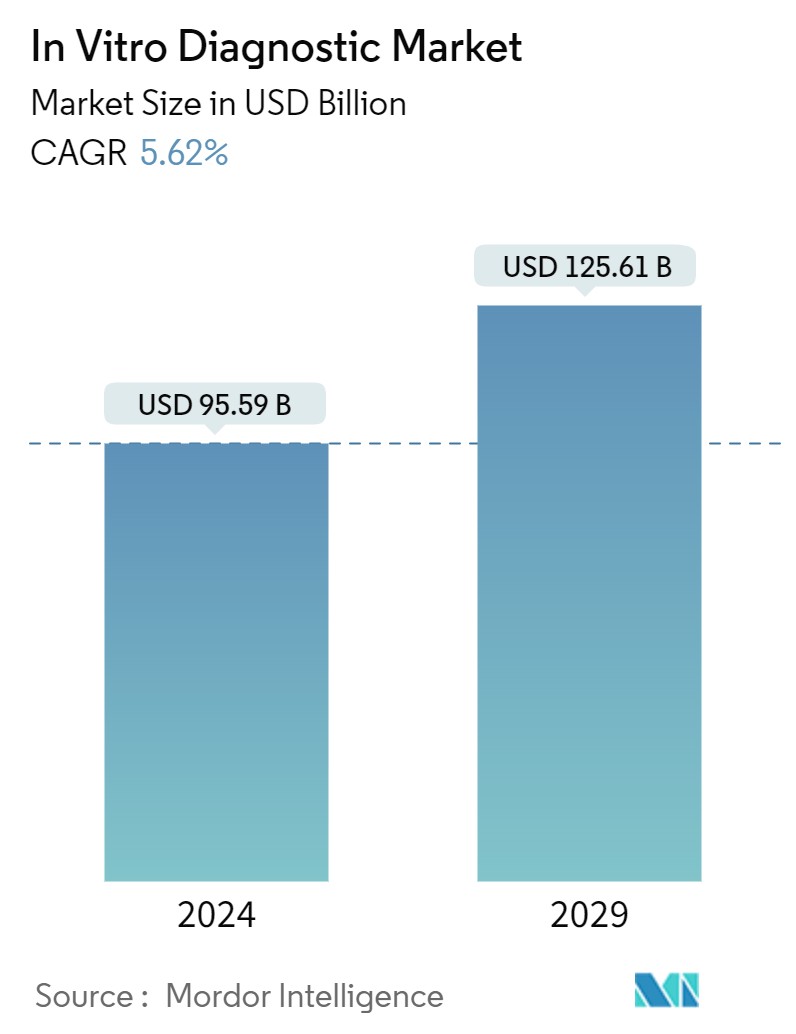

| Market Size (2024) | USD 95.59 Billion |

| Market Size (2029) | USD 125.61 Billion |

| CAGR (2024 - 2029) | 5.62 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

In Vitro Diagnostic Market Analysis

The In Vitro Diagnostic Market size is estimated at USD 95.59 billion in 2024, and is expected to reach USD 125.61 billion by 2029, growing at a CAGR of 5.62% during the forecast period (2024-2029).

The growth of the in vitro diagnostics (IVD) market is attributed to the high prevalence of chronic and infectious diseases, increasing use of point-of-care (POC) diagnostics, advanced technologies in in vitro diagnostic products, and the growing awareness and acceptance of personalized medicine and companion diagnostics.

The growing burden of chronic diseases fuels the need for in-vitro diagnostics solutions to improve early diagnosis of the condition, which is expected to contribute to market growth. For instance, in December 2023, the Australian Institute of Health and Welfare (AIHW) mentioned that the risk of coronary heart disease increases significantly with age and is prevalent in around 1 in 9 adults (11%) aged 75 years and above in Australia. In addition, in July 2023, the United Nations Office for the Coordination of Humanitarian Affairs (OCHA) reported that around 39 million individuals were infected with HIV in 2022 worldwide. The high incidence of chronic diseases is increasing the demand for substantial diagnostic procedures, which, in turn, is expected to drive the market over the forecast period.

The use of IVD products with advanced technologies increases their adoption rate and contributes to industry growth. There has been a paradigm shift from traditional diagnostics to a new generation of diagnostics that work at the gene level. This was made possible by including advanced technologies, such as genetic testing, molecular diagnostics, polymerase chain reaction (PCR), and next-generation sequencing (NGS) in the IVD platform. For instance, in June 2023, Deyser launched genetic testing solutions, such as LynchFAP and Devyser BRCA PALB2, to analyze genes like PMS2 and nine other associated genes with Lynch syndrome and breast and ovarian cancer. These kits are equipped with next-generation sequencing (NGS) technology that offers an analysis of genes and improves the diagnosis of hereditary cancer syndromes. This is expected to enhance its adoption and propel market growth over the forecast period.

Additionally, market players incorporate strategic initiatives such as product launches, which will lead to an increase in the accessibility of the products, and thus, drive market growth. For instance, in November 2023, Roche launched the Light Cycler PRO System, incorporating advanced qPCR technology to support clinical diagnostics and research. This advanced system improves performance and usability to address the needs and gaps between translational research and in vitro diagnostics. Similarly, in June 2022, Agilent Technologies launched IVD-compliant instruments, kits, and reagents to comply with the new European Union IVDR regulation.

Therefore, owing to the market trends such as the rising prevalence of chronic diseases and infectious disorders, coupled with advanced technologies in in vitro diagnostics products, the market anticipated to grow over the forecast period. However, the stringent regulations regarding product approvals and cumbersome reimbursement procedures are a few factors expected to restrain the market growth over the forecast period.

In Vitro Diagnostic Industry Segmentation

As per the scope of this industry research report, in vitro diagnostics involves medical devices and consumables that are utilized to perform in-vitro tests on various biological samples. They are used for the diagnosis of various medical conditions, such as diabetes and cancer. As detailed in industry pdf, the in vitro diagnostics market is segmented by test type, product, usability, application, end user, and geography. By test type, the market is segmented into clinical chemistry, molecular diagnostics, immunodiagnostics, hematology, and other test types. By product, the market is segmented into instruments, reagents, and other products. By usability, the market is segmented into disposable IVD devices and reusable IVD devices. By application, the market is segmented into infectious disease, diabetes, cancer/oncology, cardiology, autoimmune disease, nephrology, and other applications. By end user, the market is segmented into diagnostic laboratories, hospitals and clinics, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market size is provided in terms of value (USD).

| By Test Type | |

| Clinical Chemistry | |

| Molecular Diagnostics | |

| Immuno Diagnostics | |

| Hematology | |

| Other Test Types |

| By Product | |

| Instruments | |

| Reagents | |

| Other Products |

| By Usability | |

| Disposable IVD Devices | |

| Reusable IVD Devices |

| By Application | |

| Infectious Disease | |

| Diabetes | |

| Cancer/Oncology | |

| Cardiology | |

| Autoimmune Disease | |

| Nephrology | |

| Other Applications |

| By End User | |

| Diagnostic Laboratories | |

| Hospitals and Clinics | |

| Other End Users |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

In Vitro Diagnostic Market Size Summary

The in-vitro diagnostics (IVD) market is poised for significant growth over the forecast period, driven by the increasing prevalence of chronic and infectious diseases, the rising adoption of point-of-care diagnostics, and advancements in diagnostic technologies. The shift from traditional diagnostics to more sophisticated methods, such as genetic testing and next-generation sequencing, has enhanced the accuracy and speed of disease detection, thereby boosting market demand. The growing acceptance of personalized medicine and companion diagnostics further supports this trend, as these approaches offer tailored treatment options based on individual genetic profiles. Strategic initiatives by market players, including product launches and expansions, are expected to enhance the accessibility and availability of IVD products, contributing to market expansion.

North America is anticipated to maintain a strong presence in the IVD market, supported by a robust healthcare infrastructure and a high incidence of chronic diseases. The United States, in particular, is witnessing increased healthcare expenditure and a rapid adoption of advanced diagnostic technologies, which are driving market growth. The fragmented nature of the market, with numerous global and regional players, fosters a competitive environment where companies are actively engaging in mergers, acquisitions, and partnerships to expand their product offerings and market reach. Despite the promising growth prospects, challenges such as stringent regulatory requirements and complex reimbursement processes may pose obstacles to market advancement. Nonetheless, the ongoing developments in diagnostic technologies and the strategic efforts by key players are expected to propel the IVD market forward.

In Vitro Diagnostic Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 High Prevalence of Chronic Diseases

-

1.2.2 Increasing Use of Point-of-Care (POC) Diagnostics

-

1.2.3 Advanced Technologies in In-vitro Diagnostic Products

-

1.2.4 Increasing Awareness and Acceptance of Personalized Medicines and Companion Diagnostics

-

-

1.3 Market Restraints

-

1.3.1 Stringent Regulations Regarding Product Approvals

-

1.3.2 Cumbersome Reimbursement Procedures

-

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD)

-

2.1 By Test Type

-

2.1.1 Clinical Chemistry

-

2.1.2 Molecular Diagnostics

-

2.1.3 Immuno Diagnostics

-

2.1.4 Hematology

-

2.1.5 Other Test Types

-

-

2.2 By Product

-

2.2.1 Instruments

-

2.2.2 Reagents

-

2.2.3 Other Products

-

-

2.3 By Usability

-

2.3.1 Disposable IVD Devices

-

2.3.2 Reusable IVD Devices

-

-

2.4 By Application

-

2.4.1 Infectious Disease

-

2.4.2 Diabetes

-

2.4.3 Cancer/Oncology

-

2.4.4 Cardiology

-

2.4.5 Autoimmune Disease

-

2.4.6 Nephrology

-

2.4.7 Other Applications

-

-

2.5 By End User

-

2.5.1 Diagnostic Laboratories

-

2.5.2 Hospitals and Clinics

-

2.5.3 Other End Users

-

-

2.6 Geography

-

2.6.1 North America

-

2.6.1.1 United States

-

2.6.1.2 Canada

-

2.6.1.3 Mexico

-

-

2.6.2 Europe

-

2.6.2.1 Germany

-

2.6.2.2 United Kingdom

-

2.6.2.3 France

-

2.6.2.4 Italy

-

2.6.2.5 Spain

-

2.6.2.6 Rest of Europe

-

-

2.6.3 Asia-Pacific

-

2.6.3.1 China

-

2.6.3.2 Japan

-

2.6.3.3 India

-

2.6.3.4 Australia

-

2.6.3.5 South Korea

-

2.6.3.6 Rest of Asia-Pacific

-

-

2.6.4 Middle East and Africa

-

2.6.4.1 GCC

-

2.6.4.2 South Africa

-

2.6.4.3 Rest of Middle East and Africa

-

-

2.6.5 South America

-

2.6.5.1 Brazil

-

2.6.5.2 Argentina

-

2.6.5.3 Rest of South America

-

-

-

In Vitro Diagnostic Market Size FAQs

How big is the In Vitro Diagnostic Market?

The In Vitro Diagnostic Market size is expected to reach USD 95.59 billion in 2024 and grow at a CAGR of 5.62% to reach USD 125.61 billion by 2029.

What is the current In Vitro Diagnostic Market size?

In 2024, the In Vitro Diagnostic Market size is expected to reach USD 95.59 billion.