In-game Advertising Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 119.31 Billion |

| Market Size (2030) | USD 197.99 Billion |

| Growth Rate (2025 - 2030) | 10.66% CAGR |

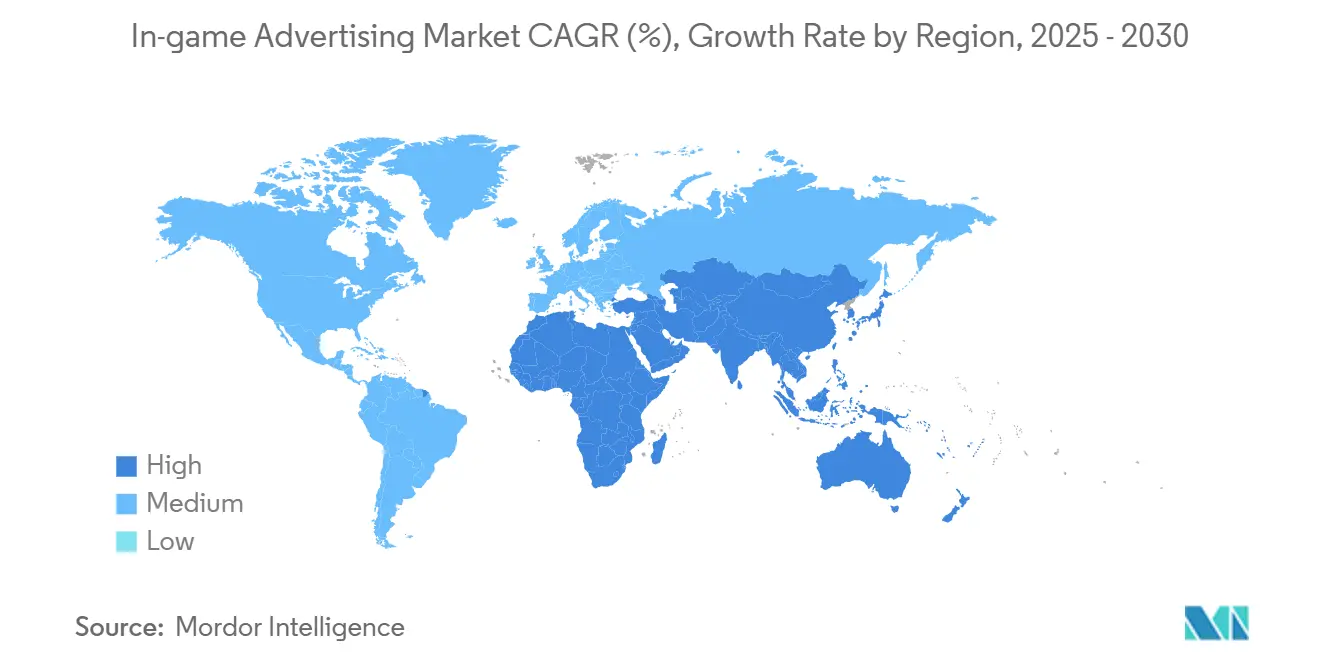

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

In-game Advertising Market Analysis by Mordor Intelligence

The in-game advertising market size is estimated at more than USD 119.31 billion in 2025 and is on track to almost double to just under USD 197.99 billion by 2030, reflecting a CAGR of nearly 10.66%. The expansion is propelled by mobile-first gaming audiences, 5G-enabled cloud gaming sessions that now sustain console-quality play on handheld devices, and the steady integration of programmatic pipes into premium inventory. Large consumer-packaged-goods and automotive advertisers are quickly moving budgets into gaming once third-party measurement verifies attention metrics, while programmatic exchange partnerships with AAA publishers are making previously closed environments broadly accessible. At the same time, tightening privacy rules force a pivot toward contextual signals and first-party data, creating both compliance costs and fresh opportunities for creative targeting models.

Key Report Takeaways

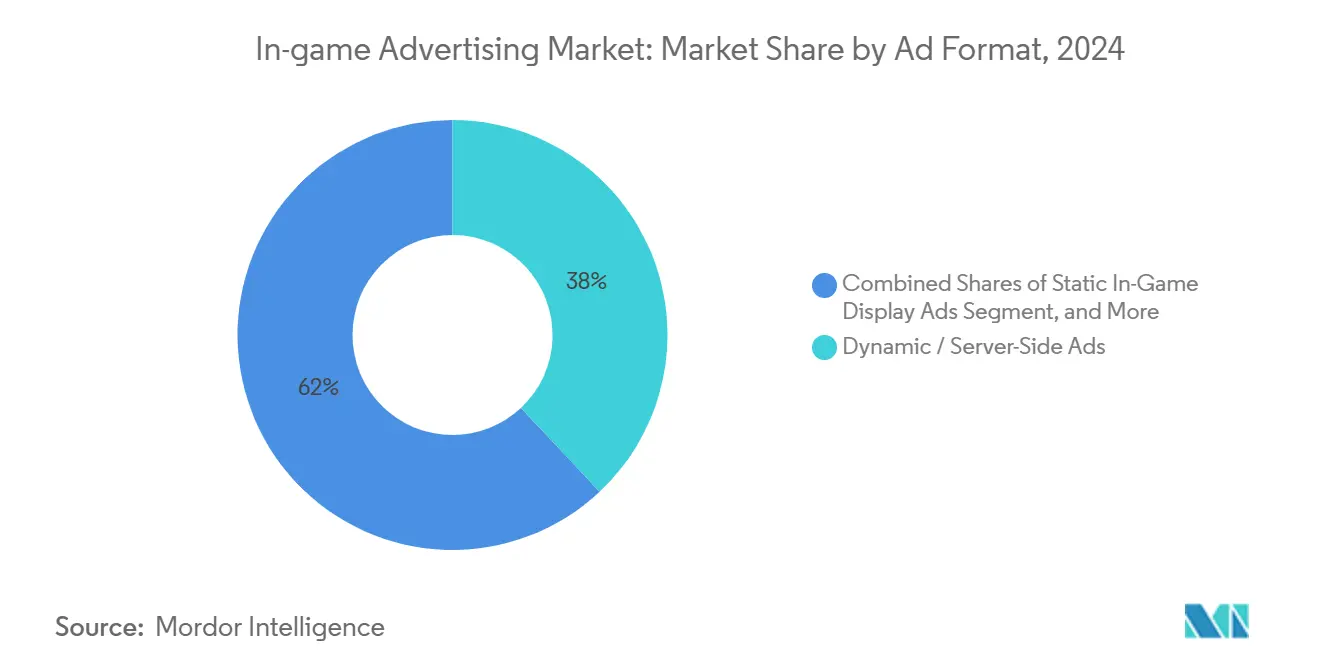

- By ad format, dynamic server-side placements led with 38% of the in-game advertising market share in 2024, while in-game video and audio spots are forecast to expand at a 16.8% CAGR through 2030.

- By device platform, mobile commanded a 56.5% share of the in-game advertising market size in 2024; the cloud/VR/AR/metaverse grouping is projected to rise at an 18.9% CAGR between 2025-2030.

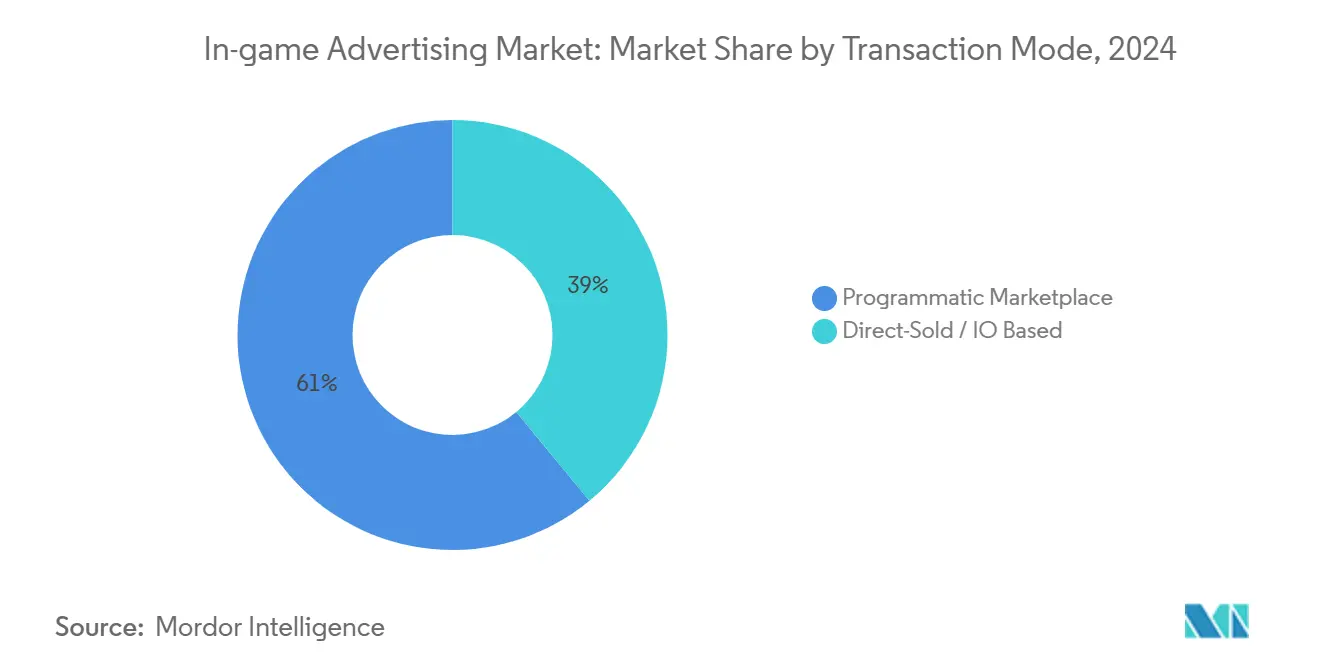

- By transaction mode, the programmatic marketplace accounted for 61% of the in-game advertising market size in 2024 and is advancing at a 12.4% CAGR through 2030.

- By geography, Asia-Pacific held 33.7% revenue in 2024, while the Middle East & Africa region is projected to grow at 14.6% CAGR to 2030.

Global In-game Advertising Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reward-Based Playable Ads in Mobile Esports | +2.1% | Global, with concentration in Asia-Pacific | Short term (≤2 yrs) |

| Real-Time Rendering for Cross-Platform Placements | +1.5% | North America, Europe, Asia-Pacific | Medium term (3-4 yrs) |

| Metaverse Product Placement | +1.3% | Asia-Pacific, with spillover to North America | Medium term (3-4 yrs) |

| 5G Roll-outs Accelerating Cloud-Gaming | +2.3% | Global, with early adoption in East Asia, North America | Medium term (3-4 yrs) |

| Programmatic AAA-Publisher Partnerships | +1.8% | Global | Short term (≤2 yrs) |

| CPG and Automotive Spend on Verified Ads | +1.2% | North America, Europe | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

Reward-based playable ads in mobile esports

Reward-centric placements are redefining monetization in competitive mobile titles by blending engagement with respect for match flow. In 2024 Huuuge Games reported an 81% jump in offer initialisations after introducing multi-reward cost-per-engagement units, and February 2025 tournament organisers in South Korea logged a 27% lift in viewer retention once rewarded spots replaced interstitials. Completion rates above 97% and seven-day retention gains of 15% demonstrate that tangible in-game benefits outweigh the perceived intrusion of advertising, turning esports participants into high-value cohorts. Brands recognise that these audiences skew affluent and spend longer per session, so message relevance and reward magnitude are fine-tuned through server-side tests before live roll-out. The result is steadily rising spend from categories where return-on-ad-spend transparency is mandatory, notably CPG and automotive.

Real-time rendering for cross-platform placements

Advances in real-time rendering engines now allow the same creative asset to adapt automatically to PC, console and mobile screen-space, eliminating costly parallel builds. Venatus cut processing latency tenfold after refactoring its stack in 2024, enabling campaigns to serve uniformly across 17 different games in a 2025 automotive promotion that lifted brand recall by 42%. Advertisers gain consistency without sacrificing fidelity, while publishers retain total control over on-screen geometry and performance budgets. These efficiencies open the door to dynamic product swaps based on local time or match status, an option previously confined to billboard-style sports titles. As cross-device gamers show 2.3 times higher engagement with ads than single-platform users, the commercial upside is clear.

5G roll-outs accelerating cloud gaming

Low-latency 5G connectivity solves the final obstacle that kept high-fidelity cloud streams from mass adoption. Median gaming latency drops from 50-100 ms on 4G to the 1-10 ms band on 5G networks [1]Verizon Communications, “Is 5G mobile gaming as exciting as playing on a console?,” verizon.com, letting platforms introduce interactive ad formats that react to player inputs in real time. Bandwidth increases to multi-gigabit speeds [3]GSMA, “5G MEC-Based Cloud Game Innovation Practice,” gsma.com enable 4K video insertions without buffering, and session length already stretches beyond 35 minutes versus 20 minutes on legacy networks [2] EY, “How gaming companies can utilize the full potential of cloud,” ey.com . These metrics encourage advertisers to treat cloud environments as mobile-addressable yet console-like in engagement depth. Telecom operators, keen to monetise vast capex, are bundling ad-supported tiers that frequently surpass subscription revenue in early pilots, pushing the in-game advertising market towards a hybrid service model.

Programmatic AAA-publisher partnerships

AAA studios historically shielded their environments from automated demand to preserve brand safety. The situation changed in 2025 when FIFA+ opened global ad inventory to Magnite’s exchange, proving that strict creative approval can sit inside a programmatic workflow while still doubling fill rates. Similar tie-ups across premium console franchises are lifting publisher yields by almost 50% without harming player sentiment. For buyers, automated access means deterministic audience data—ranging from in-match performance to team allegiance—can be used for attitudinal targeting. As more flagship titles adopt this model, the in-game advertising market gains the scale that mainstream brands need, narrowing the gulf between gaming and connected-TV budgets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ad-Format Standardisation Gaps | -1.7% | Global | Medium term (3-4 yrs) |

| Privacy Regulations Curtailing Targeting | -1.9% | Europe, North America, with global spillover | Short term (≤2 yrs) |

| Player Backlash Against Intrusive Ads | -1.2% | Global, with higher impact in mature markets | Short term (≤2 yrs) |

| Legacy Game-Engine Integration Complexity | -0.8% | Global | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

Ad-format standardisation gaps

A lack of cross-platform standards forces agencies to customise creative builds for every engine and perspective, bloating production time and depressing return on investment. While 2D viewability guidelines are mature, three-dimensional environments render those metrics useless, creating confusion over what constitutes a valid impression. Industry data shows a 20-point decline since 2021 in advertisers that planned to raise gaming budgets, directly linked to this ambiguity [4] MediaPost Communications, “Advertisers slow to invest in USD 184 B gaming media,” mediapost.com . Technical working groups launched in 2024 are drafting exposure definitions that account for camera angle, occlusion, and dwell time, but adoption remains voluntary. Until consensus is reached, major FMCG advertisers may cap spend at single-digit shares of digital budgets, keeping the in-game advertising market from achieving its full potential.

Privacy regulations curtailing targeting

GDPR, CCPA and prospective U.S. federal statutes restrict device-ID usage, undermining the high-precision segments that fuelled early mobile game campaigns. Publishers now shoulder compliance costs including the USD 4.2 million a top mobile studio invested in 2025 to overhaul data flows while performance teams rebuild around contextual cues. Early pilots show contextual models recover 82% of prior efficiency, but smaller studios lack resources to recreate such pipelines quickly, widening the competitive gap. As geofenced consent requirements spread, inventory liquidity tightens and CPMs rise, subtracting almost two percentage points from forecast growth in the in-game advertising market.

Segment Analysis

By Ad Format: Dynamic Leadership and Video Momentum

Dynamic server-side placements currently command the largest slice of the in-game advertising market, accounting for 38% of revenues in 2024. They refresh live without triggering game-client updates, letting publishers sell time-sensitive promotions that stay relevant across extended player lifecycles. The rewarded video and audio formats grow at a 16.8% CAGR, with audio alone expected to reach 182 million users by 2027. Completion rates above 97% and measurable lifts in seven-day retention illustrate the user-friendly perception of opt-in media. Static display remains foundational but its proportional contribution erodes as advertisers chase richer engagement metrics, and branded mini-games flourish when deep integration aligns with brand storytelling even if high development costs limit scalability.\

In-game video’s surge reflects advancements in compression and adaptive streaming that deliver high-definition playback with minimal resource overhead, making it suitable for mid-tier devices that still dominate emerging markets. Advertisers increasingly overlay performance interactivity such as “watch to unlock” bonuses turning a passive format into a revenue engine for both publisher and brand. The inclusion of server-side asset swaps pushes granular A/B testing at runtime, and April 2025 saw a global sportswear brand lift click-through rates by 37% using real-time creative rotation based on in-match player behaviour. As the number of brands willing to experiment grows, the in-game advertising market size attributed to interactive video is set to outpace legacy formats across most regions.

Note: Segment shares of all individual segments available upon report purchase

By Device Platform: Mobile Dominance Meets Metaverse Upswing

Mobile titles generated 56.5% of the in-game advertising market size in 2024, reflecting virtually universal smartphone access in Asia-Pacific, where 95% of users go online via handhelds. Casual genres lean on hybrid revenue models combining in-app purchases with ads, a mix that boosted overall takings 30% for studios adopting the approach. PC games, especially esports, still attract premium CPMs because long sessions and competitive intensity translate to higher brand recall. Console inventory, once inaccessible, is opening slowly as first-party platform holders trial programmatic direct deals, enticing blue-chip advertisers seeking pristine environments.

Beyond traditional categories, cloud streaming and VR/AR experiences are growing at an 18.9% CAGR, the fastest rate among device groups. The metaverse subset benefits from persistent worlds where product placements become functional parts of gameplay. A Japanese fashion label’s 2025 Fortnite show is a flagship case: players explored a virtual museum showcasing limited-edition designs, creating brand touchpoints that lasted long after the event. As headsets become lighter and telcos bundle cloud services with data plans, the in-game advertising market share arising from immersive platforms will climb, supported by average session lengths that already exceed 35 minutes on 5G connections.

By Transaction Mode: Programmatic Efficiency

Programmatic pipes routed 61% of all spend through the in-game advertising market in 2024 and are widening the gap by expanding at a 12.4% CAGR. Open auctions deliver scale in mobile casual titles, while programmatic guaranteed deals now cover premium console and PC placements once reserved for manual insertion orders.

Automation slashes campaign setup times and unlocks AI-driven optimisation: a March 2025 pilot by a leading mobile studio increased ad yield 27% and cut latency 42% after deploying real-time bidding on top of an ML framework. Direct-sold deals still dominate narrative integrations and bespoke mini-games, but even those use programmatic pipes for frequency capping and reporting, underscoring the infrastructure shift. As advertisers demand live attribution dashboards, the programmatic share of the in-game advertising market is expected to surpass two-thirds well before 2030.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific retained 33.7% of the in-game advertising market revenue in 2024, thanks to unmatched mobile penetration and a culture that accepts ad-supported models when rewarded mechanics are transparent. China’s state-backed investment in esports arenas and South Korea’s 21% games revenue jump in 2023 reinforce structural support for sustained growth. At the same time, user-sentiment surveys show fatigue when ad frequency exceeds tolerance thresholds; one Japanese studio fixed churn spikes in February 2025 by deploying an AI optimiser that cut duplicate exposures and lifted revenue 18%. Southeast Asian nations see local brands scale campaigns rapidly, often skipping desktop entirely and treating mobile gaming as the primary reach vehicle.

The Middle East and Africa show the steepest trajectory at 14.6% CAGR, fuelled by youthful populations and mobile-first infrastructure. Africa’s gaming revenue hit USD 1.8 billion in 2024 and grew six times faster than the global average. Saudi Arabia alone represented more than half of MENA-3 games turnover at USD 1.92 billion, and government incentives encourage local studios to integrate culturally relevant ad content. Latin America, where Android devices dominate, reported a rare dual rise in downloads and sessions through 2023; a March 2025 case in Brazil revealed that locally adapted creatives delivered 43% higher engagement. Collectively, these figures point to sustained diversification of the in-game advertising market base beyond its traditional East-Asian and North-American hubs.

Competitive Landscape

The in-game advertising market tilts toward a bifurcated structure. On one side, large technology conglomerates leverage device graphs, AI inference clouds and cross-channel attribution. AppLovin exemplifies the model, posting a 73% surge in advertising revenue to nearly USD 1 billion after doubling down on its AXON search engine . On the other side, specialist networks carve niches through bespoke integration with game engines. Venatus focuses on high-fidelity 3D placements and now handles 1.4 billion video impressions monthly across 900 publishers, a seven-fold network expansion since 2024.

Strategic manoeuvres revolve around capability acquisition. A North American media conglomerate bought a contextual-targeting startup for USD 340 million in January 2025 to shore up privacy-compliant offerings, while a specialised platform raised USD 75 million Series C funds to advance AI-driven creative optimisation. Partnerships also shape competition: Magnite’s alignment with Samsung TV Plus ensures that connected-TV gaming streams feed directly into its exchange, cross-pollinating audiences from linear programming. At the same time, white-space opportunities in Africa and MENA draw venture backing-Sandsoft Games netted over USD 50 million to build hybrid monetisation toolkits for Arabic-language titles.

Industry discussions increasingly place artificial intelligence at the centre of differentiation. Gamelight reported a 213% ROAS gain for JOYCITY’s Gunship Battle after applying AI-guided rewarded campaigns, echoing the sentiment that “marketing without AI is increasingly challenging . As the value chain automates, scale advantages accrue to players with proprietary datasets; yet regulatory pressure means transparency features must evolve in tandem. Mergers that blend creative automation, measurement and privacy infrastructure are therefore expected to accelerate over the forecast horizon.

In-game Advertising Industry Leaders

-

Google LLC

-

Meta Platforms Inc.

-

Unity Ads (Unity Software Inc.)

-

AppLovin / MoPub

-

ironSoure Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: AppLovin posted a 43% revenue jump to USD 1.37 billion, with its advertising segment contributing nearly USD 1 billion thanks to the AXON ad-search engine [cnbc.com]

- February 2025: Mondrian and GARDE staged a Fortnite fashion show inside the virtual museum COCOWARP, pioneering narrative-driven product placement

- December 2024: Magnite deepened its Samsung Ads partnership to power programmatic delivery on Samsung TV Plus across Southeast Asia converging connected-TV and gaming audiences

- October 2024: FIFA+ chose Magnite for global programmatic expansion, granting automated access to premium football content

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the in-game advertising (IGA) market as all gross revenue earned when brands, agencies, or exchanges serve static display, dynamic server-side placements, video and audio spots, or full advergaming integrations into mobile, PC, console, cloud, and XR game environments while play remains uninterrupted. Value is captured at the first paid impression or sponsorship insertion, expressed in USD.

Scope exclusion: revenue from banner ads surrounding game-related web pages, esports jersey logos, and loot box sales sits outside this definition.

Segmentation Overview

- By Ad Format

- Static In-Game Display Ads

- Dynamic / Server-Side Inserted Ads

- Advergaming / Branded Mini-Games

- In-Game Video and Audio Spots

- Sponsorships and Native Brand Integrations

- By Device Platform

- Mobile Games

- PC Games

- Console Games

- Others (Cloud / Streaming Games and VR / AR / Metaverse Games)

- By Transaction Mode

- Programmatic Marketplace

- Direct-Sold / IO Based

- By Geography

- North America

- United States

- Canada

- Latin America

- Brazil

- Argentina

- Mexico

- Rest of Latin America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with ad-tech integrators, AAA and indie studios, programmatic desks, and regional ad agencies across North America, Europe, Asia-Pacific, and the Middle East validate fill rates, average revenue per daily active user, and likely adoption curves of new formats. Follow-up surveys with gamers assess tolerance thresholds for ad frequency, closing critical perception gaps revealed by desk work.

Desk Research

We open every engagement with a sweep of tier-one public sources such as Interactive Advertising Bureau viewability standards, Entertainment Software Association player census tables, U.S. Bureau of Labor Statistics media spend indices, and Ofcom handset penetration surveys, complemented by trade portals like GamesIndustry.biz and StatCounter mobile OS dashboards. These datasets anchor gamer base, playtime, and CPM benchmarks by region.

To deepen company-level signals, Mordor analysts tap Dow Jones Factiva for deal pipelines, D&B Hoovers for publisher revenue splits, and Questel for patent filings that hint at ad-tech rollouts. Select shipment intel from Volza and weekly store charts from Bestsellingcarsblog help us align hardware install bases with ad serving capacity. The sources listed here illustrate our approach and are not exhaustive.

Market-Sizing & Forecasting

A top-down model starts by reconstructing the reachable ad pool: gamer population × average monthly playtime × median impressions per hour × net eCPM. Supplier roll-ups of leading ad SDKs and sampled publisher yields provide a bottom-up sense check, allowing us to adjust for under-monetized indie catalogs. Key inputs include smartphone gamer growth, 5G subscription penetration, console install base refresh cycles, average session length, and programmatic take-rate progression. Five-year forecasts rely on multivariate regression blended with scenario analysis; independent variables are stress tested through expert consensus before finalization.

Data Validation & Update Cycle

Outputs pass multi-layer variance checks, peer review, and consistency scans versus external ad spend series. Material data points that drift past preset tolerances trigger analyst re-contact. Reports refresh annually, with interim revisions for regulatory shifts or platform launches, ensuring clients receive the freshest baseline.

Why Mordor's In-Game Advertising Baseline Commands Reliability

Published figures often diverge because firms vary the ad formats counted, the devices tracked, and the cadence of currency conversion.

Our disciplined scoping, annual refresh, and dual-lens modeling minimize those gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 119.31 B (2025) | Mordor Intelligence | - |

| USD 60.6 B (2024) | Regional Consultancy A | Mobile-only scope; omits sponsorship and native integrations |

| USD 10.34 B (2025) | Global Consultancy B | Counts dynamic ads but excludes programmatic and console inventory; single-source bottom-up build |

The comparison shows that broad device coverage, calibrated eCPMs, and a blended model give Mordor Intelligence a balanced, transparent baseline that decision makers can trust.

Key Questions Answered in the Report

What is the current In-game Advertising Market size?

The In-game Advertising Market is projected to register a CAGR of 11.35% during the forecast period (2025-2030)

Who are the key players in In-game Advertising Market?

Google LLC, Anzu Virtual Reality Ltd., Blizzard Entertainment Inc., Electronic Arts Inc. and IronSource Ltd. are the major companies operating in the In-game Advertising Market.

Which is the fastest growing region in In-game Advertising Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in In-game Advertising Market?

In 2025, the North America accounts for the largest market share in In-game Advertising Market.

What years does this In-game Advertising Market cover?

The report covers the In-game Advertising Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the In-game Advertising Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: