| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 7.31 % |

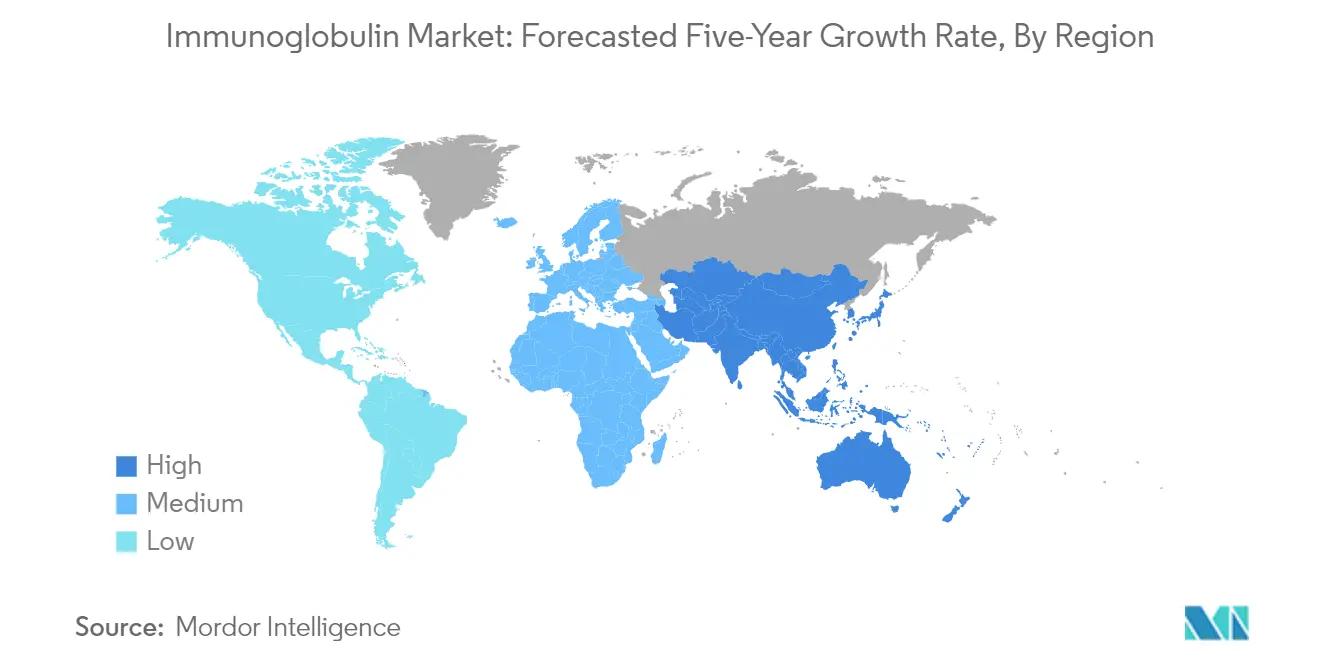

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

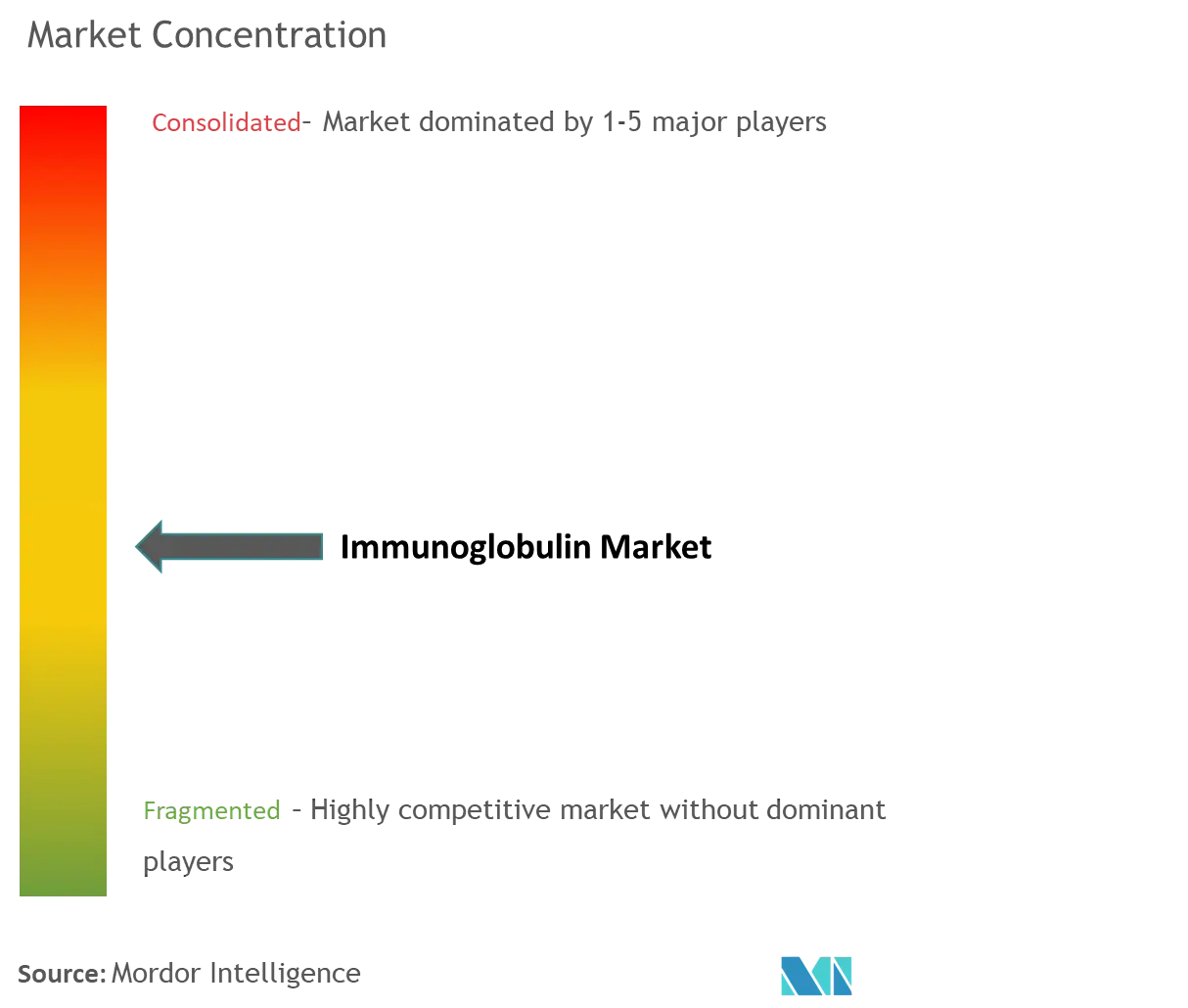

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Immunoglobulin Market Analysis

The Immunoglobulin Market is expected to register a CAGR of 7.31% during the forecast period.

The immunoglobulin industry is experiencing significant transformation driven by technological advancements in plasma collection and processing methods. Advanced fractionation techniques and improved purification processes have enhanced the quality and yield of immunoglobulin products, leading to better therapeutic outcomes. The integration of automation and artificial intelligence in manufacturing processes has streamlined production workflows, reducing processing times and improving product consistency. These technological improvements have also contributed to better plasma utilization rates and reduced wastage during production.

The regulatory landscape for immunoglobulin products continues to evolve, with authorities implementing more stringent quality control measures and safety standards. This shift is particularly evident in the European market, where myasthenia gravis (MG) affects approximately 56,000 to 123,000 people annually, prompting regulatory bodies to expedite approval processes for novel treatments. The industry has responded by investing in advanced quality management systems and implementing robust pharmacovigilance programs to ensure compliance with these enhanced requirements.

Strategic collaborations and licensing agreements have become increasingly prevalent in the immunoglobulin market, reflecting a trend toward consolidated research efforts and shared expertise. Companies are forming partnerships to leverage complementary capabilities, accelerate product development timelines, and expand market reach. These collaborations often focus on developing specialized immunoglobulin formulations for specific therapeutic applications, leading to more targeted and effective treatment options for patients with various immunological disorders.

The market is witnessing a shift toward personalized medicine approaches, with manufacturers developing tailored immunoglobulin therapies based on patient-specific factors. This trend is particularly relevant in treating Common Variable Immunodeficiency (CVID), which shows varying prevalence rates across regions, with Australia reporting a notably high prevalence of 34.2%. The industry's focus on precision medicine has led to the development of more sophisticated diagnostic tools and monitoring systems, enabling healthcare providers to optimize dosing regimens and improve treatment outcomes for individual patients.

Immunoglobulin Market Trends

Rise in Prevalence of Immunodeficiency Diseases

The global burden of immunodeficiency diseases continues to be a significant driver for the immunoglobulin market. According to the World Health Organization's 2021 report, approximately 37.7 million people were living with HIV globally, with about 0.7% of adults between the ages of 15-49 years affected worldwide. This widespread prevalence creates a substantial need for immunoglobulin therapies, as these patients often require immune system support. The increasing identification and diagnosis of various primary and secondary immunodeficiency disorders have further amplified the demand for immunoglobulin treatments across healthcare systems globally.

Recent statistics from developed nations highlight the growing challenge of immunodeficiency diseases. For instance, according to the United States Department of Health and Human Services (HHS) data released in October 2022, approximately 1.2 million people currently have HIV in the United States alone. Similarly, as reported by the Government of Canada in June 2023, the country documented 1,472 newly diagnosed cases of HIV in 2021. These numbers underscore the persistent challenge of immunodeficiency diseases and the critical need for effective treatments, driving the demand for immunoglobulin products across healthcare systems.

Increase in Adoption of Immunoglobulin

The adoption of immunoglobulin treatments has seen significant growth, driven by expanding therapeutic applications and regulatory approvals for new indications. A notable example is the January 2022 approval by Japan's Ministry of Health, Labour and Welfare (MHLW) for VYVGART (efgartigimod alfa) intravenous infusion for treating adult patients with generalized myasthenia gravis who haven't responded adequately to conventional therapies. Similarly, Pfizer's 2022 approval for PANZYGA, offering multiple FDA-approved maintenance dosing options for Chronic Inflammatory Demyelinating Polyneuropathy (CIDP), demonstrates the expanding therapeutic applications of immunoglobulin treatments.

The increasing adoption is further evidenced by recent regulatory approvals and expanded indications. In January 2023, the FDA's approval of nirsevimab, an antibody developed by Sanofi and AstraZeneca for preventing respiratory syncytial virus (RSV) lower respiratory tract disease in newborns and infants, represents a significant advancement in therapeutic applications. These developments, coupled with healthcare providers' growing confidence in immunoglobulin therapies for treating various immune-related conditions, continue to drive increased adoption across different medical specialties and patient populations.

Growing Research and Development Activities

The immunoglobulin industry is experiencing unprecedented growth in research and development activities, as evidenced by the substantial number of ongoing clinical trials. According to the National Clinical Trial (NCT) Registry data from June 2023, North America alone had approximately 12,327 immunoglobulin-based clinical trials across various development phases. This extensive research pipeline demonstrates the industry's commitment to developing novel immunoglobulin therapies and expanding their therapeutic applications. The increasing investment in R&D by pharmaceutical companies and research institutions continues to drive innovation in immunoglobulin development and delivery methods.

The research landscape is further enriched by strategic collaborations and partnerships between pharmaceutical companies, enhancing the scope and pace of immunoglobulin research. Major pharmaceutical companies are actively pursuing research in specialized areas such as rare diseases and autoimmune conditions. For instance, companies like Sanofi and AstraZeneca have successfully developed specialized immunoglobulin treatments through collaborative research efforts, as demonstrated by their joint development of nirsevimab. These ongoing research initiatives are crucial in identifying new therapeutic applications and improving existing treatments, thereby driving immunoglobulin market growth through scientific innovation and expanded treatment options.

Segment Analysis: By Product

IgG Segment in Global Immunoglobulin Market

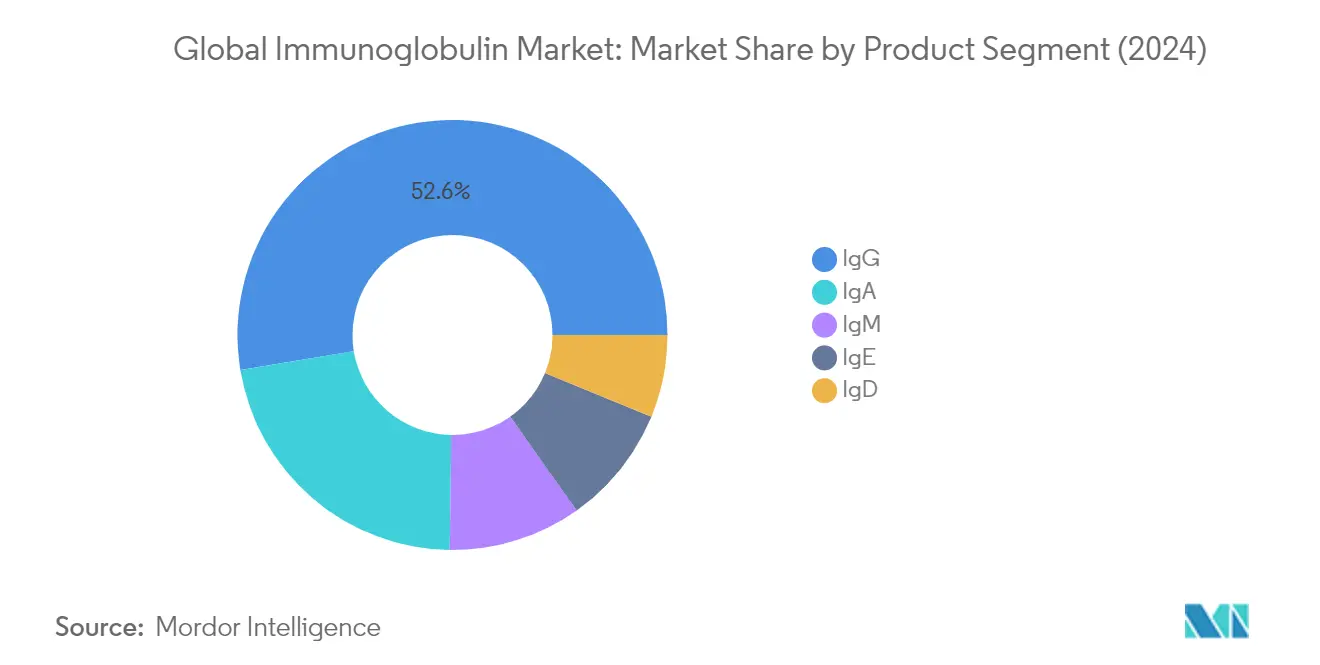

The IgG segment continues to dominate the global immunoglobulin market, holding approximately 53% of the market share in 2024. This significant market position is attributed to IgG being the most abundant antibody type in blood and tissue fluids, playing a crucial role in primary protection against local and systemic infections of the lower respiratory tract. The segment's dominance is further strengthened by its widespread application in treating various immunodeficiency conditions and its effectiveness in remembering which germs individuals have been exposed to before. Healthcare providers increasingly rely on IgG testing to determine if patients are infected by bacteria or viruses, making it an essential diagnostic tool in modern medicine.

IgA Segment in Global Immunoglobulin Market

The IgA segment is projected to experience the fastest growth rate of approximately 8% during the forecast period 2024-2029. This accelerated growth is driven by increasing research activities and expanding applications in treating various immunological disorders. The segment's growth is further supported by technological advancements in IgA-based therapies and rising awareness about its effectiveness in treating specific immune conditions. Healthcare providers are increasingly recognizing the importance of IgA in diagnostic procedures and treatment protocols, particularly in cases involving mucosal immunity and respiratory tract infections, contributing to its rapid market expansion.

Remaining Segments in Immunoglobulin Market by Product

The remaining segments in the immunoglobulin market include IgM, IgE, and IgD, each serving unique therapeutic purposes. IgM, being the largest antibody and the first to respond to infections, plays a crucial role in early immune responses. IgE, though present in smaller quantities, is vital in allergic responses and immunity against parasitic infections. IgD, while less abundant, contributes to the regulation of B-cell function and immune system development. These segments collectively complement the market's product portfolio, offering healthcare providers a comprehensive range of options for treating various immunological conditions and disorders.

Segment Analysis: By Mode of Delivery

Intravenous Mode of Delivery Segment in Immunoglobulin Market

The intravenous mode of delivery continues to dominate the global immunoglobulin market, accounting for approximately 87% of the total market share in 2024. This significant market position is attributed to its widespread adoption in healthcare settings due to its faster method of drug administration and immediate bioavailability. The segment's dominance is further strengthened by its extensive application in treating various conditions including primary immunodeficiency disorders, chronic inflammatory demyelinating polyneuropathy (CIDP), and other autoimmune disorders. Healthcare providers prefer intravenous immunoglobulin (IVIG) for acute conditions and situations requiring rapid therapeutic effects. The segment's growth is also supported by increasing investments in healthcare infrastructure, particularly in emerging economies, and the rising prevalence of immunodeficiency disorders globally.

Subcutaneous Mode of Delivery Segment in Immunoglobulin Market

The subcutaneous mode of delivery segment is emerging as the fastest-growing segment in the immunoglobulin market, projected to grow at approximately 8% CAGR during 2024-2029. This growth is primarily driven by increasing patient preference for home-based treatment options and the convenience of self-administration. The subcutaneous delivery method offers several advantages, including reduced systemic side effects, better tolerability, and improved quality of life for patients requiring long-term immunoglobulin therapy. Healthcare providers are increasingly recommending subcutaneous immunoglobulin (SCIG) for patients with stable conditions, particularly those with chronic disorders requiring regular treatment. The segment's growth is further supported by technological advancements in delivery devices and increasing awareness about self-administration options among patients and healthcare providers.

Segment Analysis: By Application

Immunodeficiency Disease Segment in Immunoglobulin Market

The Immunodeficiency Disease segment has established itself as a dominant force in the global immunoglobulin market, holding approximately 21% of the total market share in 2024. This substantial market position is driven by the increasing prevalence of primary and secondary immunodeficiency disorders worldwide, which has led to a growing demand for immunoglobulin treatments. The segment's prominence is further strengthened by ongoing advancements in diagnostic capabilities and increased awareness among healthcare providers about the importance of early detection and treatment of immunodeficiency disorders. Additionally, the expansion of healthcare infrastructure and improved access to immunoglobulin therapies in both developed and developing regions has contributed to the segment's market leadership. The segment's growth is also supported by continuous research and development efforts focused on developing more effective and targeted immunoglobulin treatments for various immunodeficiency conditions.

Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) Segment in Immunoglobulin Market

The CIDP segment is demonstrating remarkable growth potential in the immunoglobulin market, with an expected growth rate of approximately 8% during the forecast period 2024-2029. This accelerated growth is primarily attributed to increasing diagnosis rates and growing awareness about CIDP among healthcare professionals and patients. The segment's expansion is further fueled by technological advancements in treatment delivery methods and the development of more efficient immunoglobulin formulations specifically designed for CIDP patients. Healthcare providers are increasingly recognizing the effectiveness of immunoglobulin therapy in managing CIDP symptoms, leading to higher adoption rates. The segment is also benefiting from enhanced insurance coverage and reimbursement policies for CIDP treatments in major markets, making these therapies more accessible to patients. Additionally, ongoing clinical trials and research initiatives focused on improving CIDP treatment protocols are expected to drive further growth in this segment.

Remaining Segments in Immunoglobulin Market by Application

The immunoglobulin market's other significant segments include Hypogammaglobulinemia, Myasthenia Gravis, and various other applications such as Kawasaki Disease, immune thrombocytopenic purpura, and Guillain-Barre syndrome. The Hypogammaglobulinemia segment continues to be a crucial component of the market, driven by increasing diagnosis rates and improved treatment protocols. The Myasthenia Gravis segment demonstrates steady growth, supported by advancing therapeutic approaches and increasing disease awareness. The Other Applications segment encompasses a diverse range of conditions requiring immunoglobulin therapy, contributing significantly to the overall market dynamics. Each of these segments plays a vital role in shaping the market landscape, with their growth influenced by factors such as technological advancements, healthcare infrastructure development, and evolving treatment guidelines.

Immunoglobulin Market Geography Segment Analysis

Immunoglobulin Market in North America

The North American immunoglobulin market demonstrates robust growth driven by advanced healthcare infrastructure, an increasing prevalence of immunodeficiency disorders, and a strong presence of key market players. The United States, Canada, and Mexico form the key markets in this region, with each country showing distinct market characteristics and growth patterns. The region benefits from high healthcare expenditure, favorable reimbursement policies, and increasing awareness about immunoglobulin therapies among healthcare providers and patients.

Immunoglobulin Market in the United States

The United States dominates the North American immunoglobulin market, holding approximately 86% of the regional market share. The country's market leadership is attributed to its sophisticated healthcare system, extensive research and development activities, and the presence of major pharmaceutical companies. The market is further strengthened by the rising prevalence of primary immunodeficiency diseases and the increasing adoption of immunoglobulin therapies. The country's robust regulatory framework and continuous technological advancements in plasma collection and processing contribute to market growth.

Immunoglobulin Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected CAGR of approximately 7% during 2024-2029. The country's market growth is driven by increasing government initiatives supporting immunoglobulin research and development, rising awareness about plasma-derived therapies, and the growing prevalence of autoimmune disorders. The Canadian healthcare system's focus on improving access to innovative therapies and expanding plasma collection facilities further supports market expansion. The country's strategic partnerships between healthcare providers and pharmaceutical companies contribute to market development.

Immunoglobulin Market in Europe

The European immunoglobulin market showcases significant growth potential, supported by well-established healthcare systems across Germany, the United Kingdom, France, Italy, and Spain. The region benefits from strong research and development activities, an increasing prevalence of immune disorders, and growing adoption of advanced therapeutic solutions. The market is characterized by stringent regulatory frameworks and an increasing focus on plasma self-sufficiency programs.

Immunoglobulin Market in Germany

Germany leads the European immunoglobulin market, commanding approximately 24% of the regional market share. The country's market dominance is supported by its advanced healthcare infrastructure, substantial research and development investments, and the presence of major pharmaceutical manufacturers. The German market benefits from high healthcare spending, an increasing prevalence of primary immunodeficiency diseases, and growing adoption of immunoglobulin therapies in various therapeutic applications.

Immunoglobulin Market in France

France demonstrates the highest growth potential in the European region, with a projected CAGR of approximately 8% during 2024-2029. The country's market growth is driven by increasing research and development initiatives, rising awareness about immunoglobulin therapies, and the growing prevalence of autoimmune disorders. The French healthcare system's commitment to innovative therapies and expanding access to treatment options supports market expansion.

Immunoglobulin Market in Asia-Pacific

The Asia-Pacific immunoglobulin market exhibits dynamic growth potential, encompassing diverse markets including China, Japan, India, Australia, and South Korea. The region's market expansion is driven by improving healthcare infrastructure, rising healthcare expenditure, and increasing awareness about immunoglobulin therapies. The market benefits from growing investment in healthcare facilities and the rising prevalence of immune disorders.

Immunoglobulin Market in China

China dominates the Asia-Pacific immunoglobulin market, supported by its large patient population, expanding healthcare infrastructure, and increasing government initiatives in healthcare development. The country's market leadership is reinforced by growing research and development activities, rising healthcare expenditure, and improving access to advanced therapeutic options.

Immunoglobulin Market in Australia

Australia emerges as the fastest-growing market in the Asia-Pacific region, driven by advanced healthcare infrastructure, a strong regulatory framework, and increasing adoption of innovative therapies. The country's market growth is supported by rising awareness about immunoglobulin treatments, growing research activities, and strategic initiatives by key market players.

Immunoglobulin Market in Middle East & Africa

The Middle East & Africa immunoglobulin market demonstrates steady growth potential, with key markets including GCC countries and South Africa. The region's market development is supported by improving healthcare infrastructure, increasing healthcare awareness, and rising investment in medical facilities. The GCC countries lead the regional market in terms of size, while South Africa shows promising growth potential, driven by expanding healthcare access and increasing adoption of immunoglobulin therapies.

Immunoglobulin Market in South America

The South American immunoglobulin market shows promising growth prospects, with Brazil and Argentina as key contributing markets. The region's market expansion is driven by improving healthcare infrastructure, increasing awareness about immunological disorders, and rising healthcare expenditure. Brazil emerges as the largest market in the region, while Argentina demonstrates significant growth potential, supported by increasing healthcare investments and expanding access to advanced therapies.

Immunoglobulin Industry Overview

Top Companies in Immunoglobulin Market

The immunoglobulin market is characterized by intense innovation and strategic developments among key players, including Baxter International, CSL Limited, Grifols SA, Octapharma AG, and Johnson & Johnson. Companies are heavily investing in research and development to expand their product portfolios, with a particular focus on developing novel therapies for rare diseases and immunodeficiencies. Operational excellence is being achieved through the modernization of manufacturing facilities and optimization of plasma collection networks. Strategic partnerships and collaborations with biotechnology firms and research institutions are becoming increasingly common to accelerate product development and market access. Geographic expansion, particularly in emerging markets, is being pursued through the establishment of new plasma collection centers, manufacturing facilities, and distribution networks. Companies are also emphasizing technological advancement in production processes to improve yield and product quality while maintaining cost-effectiveness. The antibody companies are at the forefront of these advancements, driving the immunoglobulin industry forward.

Market Structure Shows Strong Consolidation Trends

The immunoglobulin market demonstrates a highly consolidated structure dominated by large multinational pharmaceutical companies with established plasma collection and processing capabilities. These major players possess significant advantages through their vertically integrated operations, spanning from plasma collection to end-product manufacturing and distribution. The market is characterized by high entry barriers due to stringent regulatory requirements, substantial capital investments needed for plasma collection centers and manufacturing facilities, and the complexity of production processes. Merger and acquisition activities are primarily focused on expanding plasma collection capabilities and gaining access to new geographic markets, with larger companies frequently acquiring smaller plasma collection centers and regional manufacturers.

The competitive dynamics are shaped by a mix of global pharmaceutical conglomerates and specialized plasma product manufacturers, each bringing unique strengths to the market. Global conglomerates leverage their extensive research capabilities and broad distribution networks, while specialized players focus on niche therapeutic areas and regional markets. Market consolidation continues through strategic partnerships and joint ventures, particularly in emerging markets where local manufacturing capabilities are being developed through technology transfer agreements and collaborative ventures with established players. The antibody market is a key area where these dynamics are particularly evident.

Innovation and Scale Drive Future Success

Success in the immunoglobulin market increasingly depends on companies' ability to balance innovation with operational efficiency while navigating complex regulatory requirements. Market leaders are strengthening their positions through investments in next-generation manufacturing technologies, expansion of plasma collection networks, and development of novel therapeutic applications. Companies must also address the growing importance of personalized medicine and the need for specialized formulations while maintaining cost competitiveness. The concentration of healthcare providers and increasing influence of payer organizations necessitate strong relationship management capabilities and innovative pricing strategies.

Future market success will require companies to effectively manage supply chain complexities while meeting stringent quality standards and regulatory requirements. New entrants and smaller players can gain ground by focusing on specific geographic markets or therapeutic niches where they can build specialized expertise and strong customer relationships. The threat of substitute treatments, particularly emerging cell and gene therapies, necessitates continued investment in product innovation and clinical evidence generation. Regulatory requirements are expected to become more stringent, particularly regarding plasma collection practices and product safety, making regulatory expertise and compliance capabilities critical success factors. The antibody industry must also focus on these areas to remain competitive within the immunoglobulin market.

Immunoglobulin Market Leaders

-

Baxter international Inc.

-

CSL Ltd.

-

Octapharma AG

-

Kedrion Biopharma Inc.

-

Grifols S.A

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Immunoglobulin Market News

- In April 2023, Everest Medicines received the approval of Nefecon, a primary immunoglobulin A nephropathy (IgAN) drug, from the Hainan Medical Products Administration for clinical use in China.

- In March 2022, Grifols received approval from several European Union member state health authorities as well as from the United Kingdom for XEMBIFY. It is an innovative 20% subcutaneous immunoglobulin (SCIG) that has been approved to treat primary and selected secondary immunodeficiencies.

Immunoglobulin Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Immunodeficiency Disorders

- 4.2.2 Rising Advancements in Antibody-based Therapies

- 4.2.3 Growing Research and Development Activities

-

4.3 Market Restraints

- 4.3.1 Stringent Government Regulations

- 4.3.2 High Cost of Therapy

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Value by Size - USD million)

-

5.1 By Product

- 5.1.1 IgG

- 5.1.2 IgA

- 5.1.3 IgM

- 5.1.4 IgE

- 5.1.5 IgD

-

5.2 By Mode of Delivery

- 5.2.1 Intravenous

- 5.2.2 Subcutaneous

-

5.3 By Application

- 5.3.1 Hypogammaglobulinemia

- 5.3.2 Chronic Inflammatory Demyelinating Polyneuropathy (CIDP)

- 5.3.3 Immunodeficiency Disease

- 5.3.4 Myasthenia Gravis

- 5.3.5 Other Applications

-

5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Baxter international Inc.

- 6.1.2 CSL Ltd

- 6.1.3 Grifols SA (Biotest AG)

- 6.1.4 Octapharma AG

- 6.1.5 Kedrion Biopharma Inc.

- 6.1.6 LFB group

- 6.1.7 China Biologics Products Inc.

- 6.1.8 Sichuan Yuanda Shuyang Pharmaceutical Co. Ltd

- 6.1.9 Eli Lilly

- 6.1.10 Takeda Pharmaceutical Company Limited

- 6.1.11 Bio Products Laboratory Ltd.

- 6.1.12 Pfizer Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Immunoglobulin Industry Segmentation

As per the scope of the report, immunoglobulin, also referred to as an antibody, is a protein produced by plasma cells and other lymphocytes. It is a complex entity that exerts its immunomodulatory effect on different immune system components. It is obtained from the blood through the process of fractionation and is purified for therapeutic and non-therapeutic applications. The Immunoglobulin Market is Segmented by Product (IgG, IgA, IgM, IgE, and IgD), Mode of Delivery (Intravenous and Subcutaneous), Application (Hypogammaglobulinemia, Chronic Inflammatory Demyelinating Polyneuropathy (CIDP), Immunodeficiency Disease, Myasthenia Gravis, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the abovementioned segments.

| By Product | IgG | ||

| IgA | |||

| IgM | |||

| IgE | |||

| IgD | |||

| By Mode of Delivery | Intravenous | ||

| Subcutaneous | |||

| By Application | Hypogammaglobulinemia | ||

| Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) | |||

| Immunodeficiency Disease | |||

| Myasthenia Gravis | |||

| Other Applications | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Immunoglobulin Market Research FAQs

What is the current Global Immunoglobulin Market size?

The Global Immunoglobulin Market is projected to register a CAGR of 7.31% during the forecast period (2025-2030)

Who are the key players in Global Immunoglobulin Market?

Baxter international Inc., CSL Ltd., Octapharma AG, Kedrion Biopharma Inc. and Grifols S.A are the major companies operating in the Global Immunoglobulin Market.

Which is the fastest growing region in Global Immunoglobulin Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Global Immunoglobulin Market?

In 2025, the North America accounts for the largest market share in Global Immunoglobulin Market.

What years does this Global Immunoglobulin Market cover?

The report covers the Global Immunoglobulin Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Immunoglobulin Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Immunoglobulin Market Research

Mordor Intelligence delivers comprehensive insights into the immunoglobulin market. We leverage our extensive expertise in the antibody industry research and consulting. Our analysis covers the complete spectrum of immunoglobulin products. This includes segments such as intravenous immunoglobulin and gamma globulin. Through collaboration with leading antibodies companies and antibody research organizations, we provide detailed market data for IG. Our thorough market analysis helps stakeholders understand industry dynamics.

Our detailed report, available as an easy-to-read report PDF, offers stakeholders access to IG historical data and current market review insights. The analysis includes extensive coverage of immunoglobulin high demand segments and emerging applications. This is supported by immunoglobulin chart visualizations and trend analysis. The report particularly benefits antibody research companies. It provides actionable intelligence on intravenous immunoglobulin IVIG market developments and major immunoglobulin product innovations. This enables informed strategic decision-making in this rapidly evolving sector.