| Study Period | 2021 - 2030 |

| Base Year For Estimation | 2024 |

| Market Size (2025) | USD 4.92 Billion |

| Market Size (2030) | USD 6.88 Billion |

| CAGR (2025 - 2030) | 6.95 % |

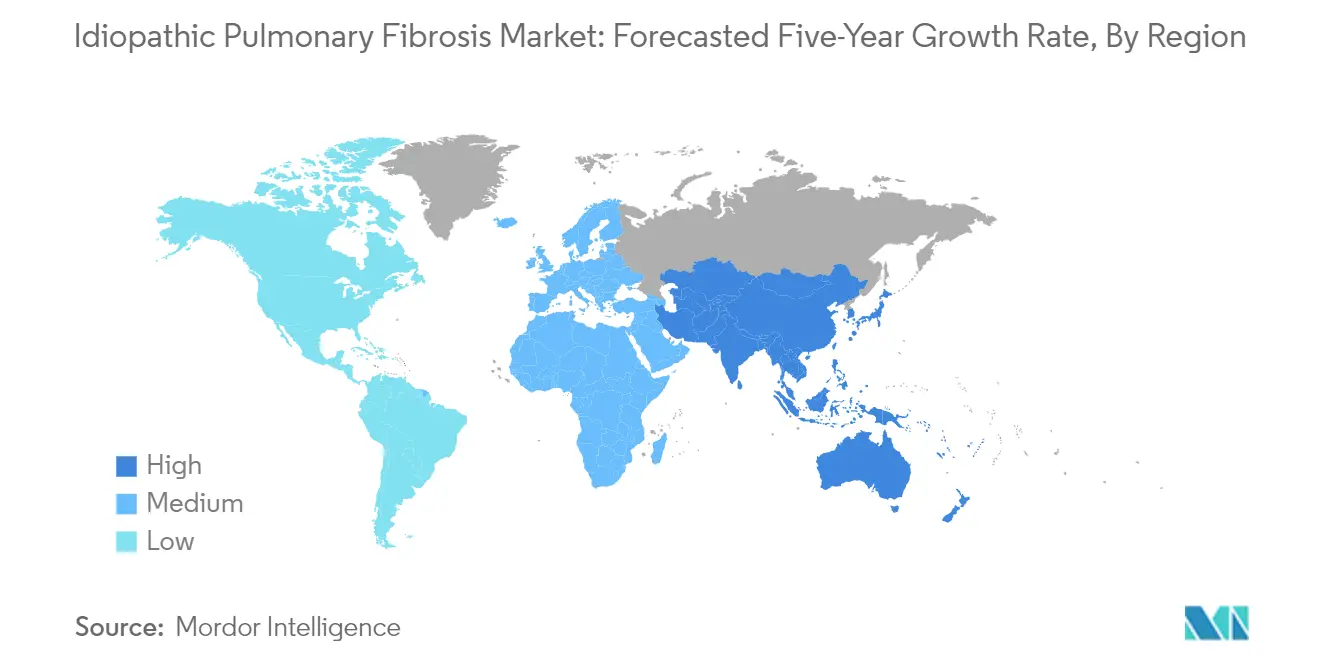

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order |

Idiopathic Pulmonary Fibrosis Market Analysis

The Idiopathic Pulmonary Fibrosis Market size is estimated at USD 4.92 billion in 2025, and is expected to reach USD 6.88 billion by 2030, at a CAGR of 6.95% during the forecast period (2025-2030).

The IPF market is experiencing significant transformation driven by demographic shifts and healthcare advancements. According to the World Health Organization's October 2022 update, one in every six individuals globally will be above 60 years by 2030, with the population aged 60 and above expected to increase by 1.4 billion. This demographic transition is reshaping healthcare priorities and treatment approaches, as aging is closely associated with cellular and molecular lung changes that contribute to IPF development. Healthcare systems worldwide are adapting their infrastructure and treatment protocols to address the unique needs of this growing patient population.

The therapeutic landscape for IPF continues to evolve with breakthrough innovations and regulatory approvals. Recent epidemiological data from Prescriber in July 2022 indicates that the annual incidence of idiopathic pulmonary fibrosis in Europe ranges from 0.22 to 7.4 per 100,000 people, with approximately 32,500 people affected in the United Kingdom alone. This significant patient population has spurred pharmaceutical companies to invest in novel treatment modalities and expand their product portfolios. The IPF industry has witnessed several strategic collaborations and licensing agreements aimed at accelerating drug development and commercialization.

The market is characterized by intense research activities focusing on novel therapeutic approaches and drug delivery systems. Pharmaceutical companies are increasingly exploring innovative treatment modalities, including combination therapies and targeted molecular approaches. The emphasis on personalized medicine has led to the development of more effective treatment strategies, considering individual patient characteristics and disease manifestations. This trend is supported by advances in biomarker research and diagnostic technologies, enabling more precise patient stratification and treatment selection.

The competitive landscape is evolving through strategic initiatives and industry consolidation. Major pharmaceutical companies are strengthening their market presence through mergers, acquisitions, and partnerships. These strategic moves are aimed at expanding product portfolios, enhancing research capabilities, and improving market access. The industry has also witnessed increased investment in manufacturing capabilities and distribution networks to ensure reliable product supply and broader market reach. Companies are focusing on developing comprehensive treatment solutions that address both the medical and quality-of-life aspects of IPF management. Additionally, the integration of respiratory therapeutics is becoming a focal point in addressing the complex needs of patients within the ILD market.

Idiopathic Pulmonary Fibrosis Market Trends

Increasing Prevalence of Idiopathic Pulmonary Fibrosis

The rising prevalence of idiopathic pulmonary fibrosis (IPF) globally has become a significant driver for market growth, with the condition primarily affecting people between the ages of 50 and 70 years. Recent epidemiological studies have shown concerning trends in disease burden, particularly among specific populations. For instance, according to data published in February 2022, the incidence of IPF nearly tripled among US veterans over a decade, with prevalence increasing dramatically from 276 cases per 100,000 in 2010 to 725 cases per 100,000 in 2019. The disease demonstrates a particular impact on elderly populations, with studies indicating that each year increase in average age is associated with a 6.2% increase in the IPF prevalence rate. Additionally, research from Japan published in 2022 revealed an estimated nationwide patient count of 34,040, with a mean age of 73 years and a male predominance of 73%.

The global burden of IPF continues to grow, creating an urgent need for enhanced therapeutic interventions and disease management strategies. According to recent estimates, idiopathic pulmonary fibrosis affects approximately 13 to 20 per 100,000 people worldwide, with the United States alone reporting around 100,000 affected individuals and 30,000 to 40,000 new cases diagnosed annually. The increasing geriatric population worldwide further compounds this challenge, as older adults are more susceptible to developing IPF. According to the World Population Ageing Report 2020, the global population aged 65 years or over is projected to more than double from 727 million in 2020 to over 1.5 billion by 2050, suggesting a potential surge in IPF cases in the coming decades. This demographic shift, combined with improved disease awareness and diagnostic capabilities, is expected to drive increased demand for IPF treatments and therapeutics, including advanced pulmonary function testing and antifibrotic therapy.

Understand The Key Trends Shaping This Market

Download PDF

Rising Research and Development Activities in Fibrotic Diseases

The pharmaceutical industry has demonstrated increased commitment to research and development in fibrotic diseases, particularly focusing on innovative treatments for idiopathic pulmonary fibrosis. Recent research initiatives have yielded promising results in various therapeutic approaches. For instance, in March 2023, a significant clinical trial was registered at the UMIN Clinical Trials Registry investigating perioperative pirfenidone therapy in patients with non-small cell lung cancer combined with idiopathic pulmonary fibrosis. Additionally, groundbreaking research published in early 2022 demonstrated that Coenzyme Q10 (CoQ10) could enhance the efficacy of airway basal stem cell transplantation for IPF treatment, showing potential in counteracting oxidative stress in the alveolar microenvironment. These developments represent significant advances in understanding and treating IPF, driving market innovation and growth.

The industry has also witnessed substantial investment and strategic initiatives from key market players, fostering continued innovation in IPF treatment. Major pharmaceutical companies are actively pursuing novel therapeutic approaches through clinical trials and research collaborations. For example, in February 2022, Boehringer Ingelheim's investigational therapy BI 1015550 received Breakthrough Therapy Designation from the FDA for IPF treatment, demonstrating the industry's commitment to developing innovative solutions. Furthermore, research published in the Springer Nature journal in February 2022 revealed that eperisone may offer safer and more therapeutically beneficial outcomes for IPF patients compared to existing treatments like pirfenidone and nintedanib. These ongoing research efforts, combined with increasing investment in clinical trials and drug development, are creating a robust pipeline of potential treatments that could significantly improve patient outcomes in the future. This includes advancements in lung scarring treatment and the development of antifibrotic drugs.

Segment Analysis: By Drug Type

Nintedanib Segment in Idiopathic Pulmonary Fibrosis Market

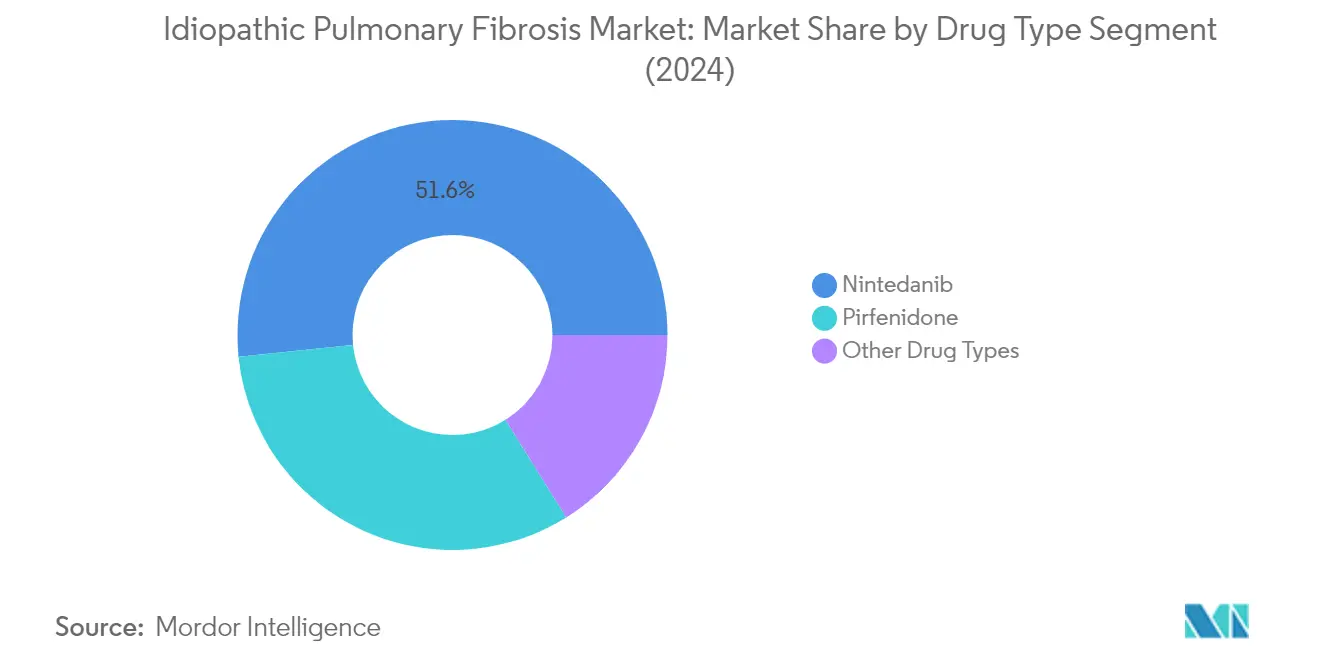

Nintedanib has emerged as the dominant segment in the idiopathic pulmonary fibrosis (IPF) market, commanding approximately 52% of the total market share in 2024. This segment's leadership position can be attributed to its proven efficacy as a tyrosine kinase inhibitor that significantly reduces the progression of IPF. The drug's widespread adoption across major healthcare markets globally has been supported by its inclusion in various national healthcare reimbursement programs and its availability through multiple distribution channels. The segment is also demonstrating robust growth potential, expected to grow at nearly 9% from 2024 to 2029, driven by increasing awareness among healthcare providers, expanding patient access programs, and the drug's established safety profile in long-term usage. The continued dominance of Nintedanib is further reinforced by ongoing research activities exploring its potential in treating other forms of progressive fibrosing interstitial lung diseases (interstitial lung diseases).

Remaining Segments in Drug Type Market

The remaining segments in the IPF drug market include Pirfenidone and other drug types, each playing crucial roles in providing treatment options for patients. Pirfenidone, as an established antifibrotic drug, continues to maintain a significant presence in the market with its proven ability to slow disease progression and improve patient outcomes. The other drug types segment, which includes N-acetylcysteine and various emerging therapeutic options, represents an area of active research and development. These segments collectively provide healthcare providers with a diverse range of treatment options, allowing for more personalized therapeutic approaches based on individual patient needs, tolerance levels, and response patterns. The availability of multiple drug types has also fostered healthy market competition, potentially leading to improved accessibility and affordability of IPF treatments.

Segment Analysis: By Mode of Action

Tyrosine Kinase Inhibitors Segment in Idiopathic Pulmonary Fibrosis Market

The Tyrosine Kinase Inhibitors segment continues to dominate the global idiopathic pulmonary fibrosis market, holding approximately 52% of the market share in 2024. This significant market position is primarily attributed to the segment's proven efficacy in suppressing fibrosis in patients with idiopathic pulmonary fibrosis, while demonstrating a growth rate of nearly 9% through 2029. The segment's strong performance is supported by increasing reimbursement coverage for tyrosine kinase inhibitors across major markets and the expanding adoption of nintedanib, a key tyrosine kinase inhibitor. Recent clinical studies have consistently demonstrated the effectiveness of tyrosine kinase inhibitors in managing disease progression, particularly in patients with progressive fibrosing interstitial lung diseases (interstitial lung diseases), further solidifying their position as the preferred treatment option among healthcare providers.

Antifibrotic Agents Segment in Idiopathic Pulmonary Fibrosis Market

The antifibrotic agents segment represents a crucial component of the idiopathic pulmonary fibrosis treatment landscape, with drugs like pirfenidone leading the therapeutic approach. These agents have shown remarkable efficacy in slowing the decline in lung function and reducing the risk of acute respiratory deteriorations, which are associated with high morbidity and mortality rates. The segment's growth is being driven by increasing awareness about early diagnosis and treatment initiation, coupled with expanding access to antifibrotic therapy in emerging markets. Recent clinical evidence supporting the use of antifibrotic agents in both IPF and non-IPF progressive fibrosis has opened new avenues for market expansion, while ongoing research continues to uncover additional therapeutic benefits of these agents in managing fibrotic lung diseases.

Remaining Segments in Mode of Action

Other modes of action in the idiopathic pulmonary fibrosis market include autotaxin inhibitors, antioxidants, and corticosteroids, which collectively provide alternative treatment approaches for patients who may not respond optimally to primary therapies. These emerging therapeutic options are gaining attention due to their potential in addressing specific pathways involved in the disease progression. The development of novel treatment mechanisms, particularly in the area of autotaxin inhibition, represents a promising direction for future therapeutic interventions. These alternative modes of action are particularly important in providing personalized treatment options for patients with varying disease presentations and comorbidities, contributing to a more comprehensive treatment landscape in the management of idiopathic pulmonary fibrosis.

Segment Analysis: By End User

Hospitals and Clinics Segment in Idiopathic Pulmonary Fibrosis Market

The hospitals and clinics segment continues to dominate the global idiopathic pulmonary fibrosis market, holding approximately 74% of the market share in 2024. This significant market share can be attributed to the sophisticated infrastructure and advanced technological capabilities available in hospital settings for managing IPF cases. The segment's dominance is further strengthened by the increasing number of specialized pulmonary care units in hospitals worldwide, coupled with the rising preference for hospital-based treatment due to the complexity of IPF management. Additionally, the availability of skilled healthcare professionals, advanced diagnostic equipment, and the ability to handle emergency complications related to IPF make hospitals and clinics the primary choice for treatment. The presence of established reimbursement policies in many countries for hospital-based IPF treatments has also contributed to this segment's substantial market share. Moreover, the growing trend of establishing specialized IPF treatment centers within hospitals has further consolidated their position as the leading end-user segment in the market.

Other End Users Segment in Idiopathic Pulmonary Fibrosis Market

The other end users segment, which includes ambulatory surgical centers, nursing homes, and long-term care facilities, is projected to grow at approximately 8% from 2024 to 2029. This accelerated growth is primarily driven by the increasing preference for outpatient care settings and the rising demand for specialized long-term care facilities for IPF patients. The segment's growth is further supported by the emergence of state-of-the-art ambulatory surgical centers equipped with advanced respiratory care facilities. These centers are increasingly becoming preferred alternatives for patients seeking immediate intervention services following diagnosis, particularly under private insurance coverage. The trend towards reducing hospital stays and the growing focus on providing personalized care in more comfortable settings has also contributed to the segment's rapid growth. Additionally, the expansion of healthcare services in ambulatory care settings and the increasing investment in modernizing long-term care facilities are expected to sustain this growth trajectory over the forecast period.

Idiopathic Pulmonary Fibrosis Market Geography Segment Analysis

Idiopathic Pulmonary Fibrosis Market in North America

North America represents the dominant region in the global IPF market, encompassing the United States, Canada, and Mexico. The region's leadership position is attributed to its robust healthcare infrastructure, high prevalence of idiopathic pulmonary fibrosis, and significant research and development activities. The presence of major pharmaceutical companies, advanced diagnostic capabilities, and favorable reimbursement policies further strengthen the IPF market in this region. Additionally, the increasing aging population and growing awareness about rare diseases contribute to the market's expansion across these countries.

Idiopathic Pulmonary Fibrosis Market in the United States

The United States dominates the North American IPF market with approximately 84% share of the regional market. The country's market leadership is driven by its advanced healthcare system, high healthcare expenditure, and presence of key market players. The strong focus on research and development, coupled with favorable regulatory policies for rare disease treatments, creates a conducive environment for market growth. The country's well-established healthcare infrastructure and increasing prevalence of idiopathic pulmonary fibrosis among the aging population further solidify its position. The presence of specialized treatment centers and ongoing clinical trials also contributes to market expansion.

Idiopathic Pulmonary Fibrosis Market in Canada

Canada emerges as the fastest-growing market in North America with a projected growth rate of approximately 7% during 2024-2029. The country's market growth is fueled by increasing healthcare investments and growing awareness about rare diseases. The Canadian healthcare system's universal coverage model ensures better accessibility to treatments for idiopathic pulmonary fibrosis patients. The country's focus on improving diagnostic capabilities and treatment options, combined with rising research activities, drives market expansion. Additionally, the presence of well-established healthcare facilities and increasing government initiatives support market growth.

Idiopathic Pulmonary Fibrosis Market in Europe

Europe represents a significant market for idiopathic pulmonary fibrosis treatments, encompassing key countries including Germany, the United Kingdom, France, Italy, and Spain. The region's market is characterized by its strong healthcare infrastructure, significant research initiatives, and growing patient population. The presence of major pharmaceutical companies and research institutions, coupled with favorable healthcare policies, drives market growth. The region's focus on rare disease treatments and increasing healthcare expenditure further supports market expansion.

Idiopathic Pulmonary Fibrosis Market in Germany

Germany leads the European market with approximately 21% share of the regional market. The country's dominant position is attributed to its advanced healthcare system and substantial investment in medical research. Germany's robust healthcare infrastructure, combined with high healthcare spending and strong presence of pharmaceutical companies, supports market growth. The country's emphasis on innovative treatments and early disease diagnosis contributes to its market leadership. Additionally, the well-established reimbursement system ensures better access to treatments for patients.

Idiopathic Pulmonary Fibrosis Market in France

France demonstrates the highest growth potential in Europe with a projected growth rate of approximately 8% during 2024-2029. The country's market expansion is driven by increasing research activities and growing awareness about rare diseases. France's strong healthcare system and focus on innovative treatments contribute to market growth. The country's emphasis on patient care and increasing investments in healthcare infrastructure support market development. Additionally, the presence of key market players and ongoing clinical trials enhances market expansion.

Idiopathic Pulmonary Fibrosis Market in Asia-Pacific

The Asia-Pacific region represents an emerging market for idiopathic pulmonary fibrosis treatments, comprising key countries including China, Japan, India, Australia, and South Korea. The region demonstrates significant growth potential due to its large patient population and improving healthcare infrastructure. The increasing healthcare expenditure, growing awareness about rare diseases, and rising research activities contribute to market expansion. The region's economic growth and focus on healthcare development create opportunities for market advancement, particularly in the IPF market size.

Idiopathic Pulmonary Fibrosis Market in Japan

Japan emerges as the largest market in the Asia-Pacific region, driven by its advanced healthcare system and aging population. The country's strong focus on healthcare innovation and substantial research investments supports market growth. Japan's well-established pharmaceutical industry and emphasis on rare disease treatments contribute to its market leadership. The country's robust healthcare infrastructure and favorable reimbursement policies ensure better access to treatments, enhancing the IPF market size.

Idiopathic Pulmonary Fibrosis Market in India

India represents the fastest-growing market in the Asia-Pacific region, supported by its improving healthcare infrastructure and increasing healthcare investments. The country's large patient population and growing awareness about rare diseases drive market expansion. India's developing pharmaceutical sector and increasing focus on research activities contribute to market growth. The country's economic growth and rising healthcare expenditure create opportunities for market development, particularly in the interstitial lung disease (ILD) market.

Idiopathic Pulmonary Fibrosis Market in Middle East & Africa

The Middle East & Africa region, including GCC countries and South Africa, demonstrates growing potential in the idiopathic pulmonary fibrosis market. The region's market development is supported by improving healthcare infrastructure and increasing healthcare investments. GCC countries lead the regional market, while South Africa shows the fastest growth potential. The region's focus on healthcare development, coupled with rising awareness about rare diseases, contributes to market expansion. The presence of international healthcare providers and growing medical tourism further supports market growth, particularly in respiratory therapeutics.

Idiopathic Pulmonary Fibrosis Market in South America

The South American market, primarily comprising Brazil and Argentina, shows steady growth in the idiopathic pulmonary fibrosis treatment sector. Brazil emerges as the largest market in the region, while also demonstrating the fastest growth potential. The region's market development is driven by improving healthcare infrastructure and increasing awareness about rare diseases. The presence of international pharmaceutical companies and growing research activities supports market expansion. The region's focus on healthcare development and increasing healthcare expenditure contributes to market growth, particularly in the interstitial lung disease (ILD) market.

Get Analysis on Important Geographic Markets

Download PDF

Idiopathic Pulmonary Fibrosis Industry Overview

Top Companies in Idiopathic Pulmonary Fibrosis Market

The IPF market is characterized by intense research and development activities focused on novel therapeutic solutions. Companies are actively pursuing innovation through clinical trials of new drug candidates, particularly in areas like tyrosine kinase inhibitors, antifibrotic drug agents, and autotaxin inhibitors. Strategic collaborations and licensing agreements between pharmaceutical companies have become increasingly common to leverage complementary capabilities and accelerate drug development. Market leaders are expanding their geographical presence while simultaneously investing in manufacturing capabilities to ensure reliable supply chains. The competitive landscape is further shaped by companies' efforts to develop generic versions of existing treatments, making therapies more accessible and affordable across different regions.

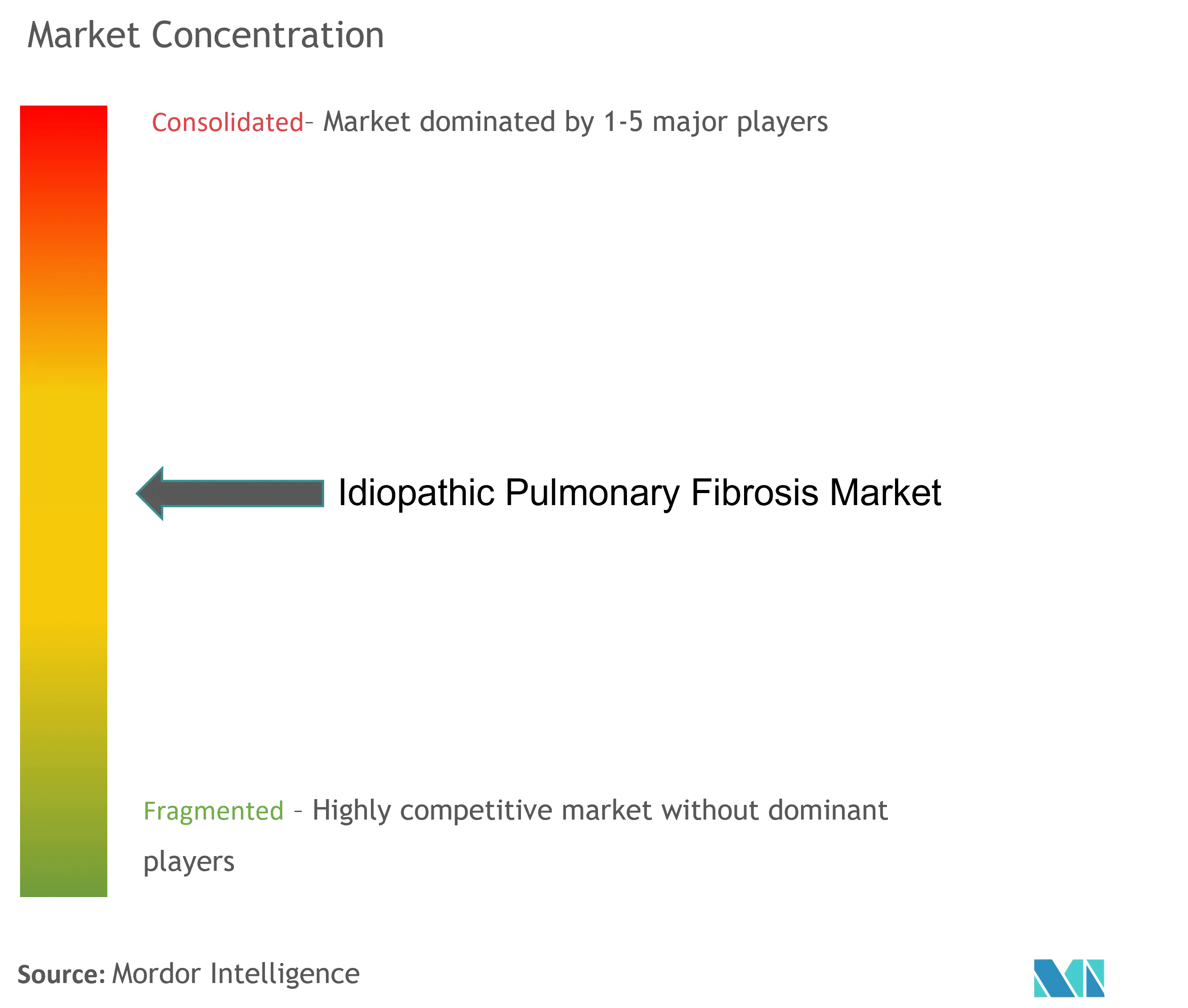

Consolidated Market Led By Global Players

The idiopathic pulmonary fibrosis market demonstrates a relatively consolidated structure dominated by large pharmaceutical conglomerates with an established global presence. Companies like Boehringer Ingelheim, Roche, Bristol-Myers Squibb, and Merck & Co. leverage their extensive research capabilities, robust distribution networks, and significant financial resources to maintain their market positions. These major players are complemented by specialized biotechnology firms like FibroGen and MediciNova, which focus exclusively on developing novel therapies for fibrotic diseases. The market has witnessed significant merger and acquisition activity, particularly involving larger pharmaceutical companies acquiring smaller biotech firms to expand their product pipelines and therapeutic capabilities.

The competitive dynamics are characterized by a mix of established pharmaceutical giants and emerging biotechnology companies, creating a diverse ecosystem of market participants. Market consolidation continues through strategic acquisitions, as demonstrated by Roche's acquisition of Promedior and Bristol Myers' acquisition of Forbius, both aimed at strengthening their positions in fibrotic disease treatment. Companies are increasingly focusing on expanding their presence in emerging markets while maintaining their stronghold in developed regions. The entry barriers remain high due to the complex nature of drug development, stringent regulatory requirements, and the need for substantial investment in research and clinical trials.

Innovation and Market Access Drive Success

Success in the idiopathic pulmonary fibrosis market increasingly depends on companies' ability to develop innovative therapeutic solutions while ensuring broad market access. Incumbent players must focus on expanding their product portfolios through internal research and development while simultaneously pursuing strategic partnerships to access new technologies and markets. Companies need to invest in real-world evidence generation to demonstrate the clinical and economic value of their treatments, while also developing patient support programs to enhance treatment adherence and outcomes. The ability to navigate complex regulatory environments across different regions while maintaining cost-effective manufacturing and distribution operations has become crucial for sustainable growth.

Market contenders can gain ground by focusing on developing differentiated therapeutic approaches and addressing unmet medical needs in specific patient populations. Companies must build strong relationships with healthcare providers and patient advocacy groups while investing in educational initiatives to raise disease awareness. The competitive landscape is influenced by increasing pressure from healthcare systems to demonstrate value for money, making pricing strategies and market access capabilities critical success factors. Future success will depend on companies' ability to balance innovation with affordability while adapting to evolving regulatory requirements and healthcare delivery models. The development of companion diagnostics and personalized treatment approaches represents an emerging opportunity for differentiation in this competitive market. The IPF industry is also seeing a rise in respiratory therapeutics as companies aim to address broader respiratory health challenges.

Idiopathic Pulmonary Fibrosis Market Leaders

-

Cipla Inc.

-

Boehringer Ingelheim International GmbH

-

F. Hoffmann-La Roche Ltd

-

FibroGen, Inc.

-

Horizon Therapeutics plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Idiopathic Pulmonary Fibrosis Market News

- In January 2023, Daewoong Pharmaceutical signed an agreement with CS Pharmaceuticals for a first-in-class PRS inhibitor Bersiporocin in Greater China, including mainland China, Hong Kong, Taiwan, and Macau. Under this agreement, CSP will in-license bersiporocin for idiopathic pulmonary fibrosis (IPF) and potentially other fibrotic indications for a total consideration of up to USD 336 million, including up to USD 76 million in upfront and development milestone payments and double-digit royalties on net sales.

- In May 2022, Sandoz launched generic pirfenidone, an AB-rated (fully substitutable) equivalent to Genentech's Esbriet, to treat patients with idiopathic pulmonary fibrosis (IPF) in the United States.

Idiopathic Pulmonary Fibrosis Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Idiopathic Pulmonary Fibrosis and Growing Geriatric Population

- 4.2.2 Rising Research and Development Activities in Fibrotic Diseases

-

4.3 Market Restraints

- 4.3.1 Unavailability of Proper Treatment and Lack of Awareness in Developing Countries

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

-

5.1 By Drug Type

- 5.1.1 Nintedanib

- 5.1.2 Pirfenidone

- 5.1.3 Other Drug Types

-

5.2 By Mode of Action

- 5.2.1 Antifibrotic Agents

- 5.2.2 Tyrosine Kinase Inhibitors

- 5.2.3 Other Modes of Action

-

5.3 By End User

- 5.3.1 Hospitals and Clinics

- 5.3.2 Pharmacies

- 5.3.3 Other End Users

-

5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 United Therapeutics Corporation

- 6.1.2 Boehringer Ingelheim International GmbH

- 6.1.3 Bristol-Myers Squibb Company

- 6.1.4 Cipla Inc.

- 6.1.5 F. Hoffmann-La Roche Ltd

- 6.1.6 FibroGen Inc.

- 6.1.7 MediciNova Inc.

- 6.1.8 Jubliant Pharma Limited (Jubliant Cadista Limited)

- 6.1.9 Merck & Co. Inc.

- 6.1.10 Horizon Therapeutics Inc.

- 6.1.11 Avalyn Pharma Inc.

- 6.1.12 CS Pharmaceuticals

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Idiopathic Pulmonary Fibrosis Industry Segmentation

As per the scope of the report, idiopathic pulmonary fibrosis (IPF) refers to a type of lung disease that causes scarring (fibrosis) of the lungs for an unknown reason. As time passes, this scarring gets worse, and it becomes hard to take deep breaths, and the lungs cannot take in enough oxygen. IPF involves the interstitium (the tissue and space around the air sacs of the lungs) and not directly involve the airways or blood vessels.

The idiopathic pulmonary fibrosis market is segmented by drug type, mode of action, end user, and geography. Based on drug type the market is segmented as nintedanib, pirfenidone, and other drug types. Based on mode of action the market is segmented as antifibrotic agents, tyrosine kinase inhibitors, and other modes of action. Based on end users the market is segmented as hospitals and clinics, pharmacies, and other end users. Based on geography the market is segmented by North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in USD for the above segments.

| By Drug Type | Nintedanib | ||

| Pirfenidone | |||

| Other Drug Types | |||

| By Mode of Action | Antifibrotic Agents | ||

| Tyrosine Kinase Inhibitors | |||

| Other Modes of Action | |||

| By End User | Hospitals and Clinics | ||

| Pharmacies | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Idiopathic Pulmonary Fibrosis Market Research FAQs

How big is the Idiopathic Pulmonary Fibrosis Market?

The Idiopathic Pulmonary Fibrosis Market size is expected to reach USD 4.92 billion in 2025 and grow at a CAGR of 6.95% to reach USD 6.88 billion by 2030.

What is the current Idiopathic Pulmonary Fibrosis Market size?

In 2025, the Idiopathic Pulmonary Fibrosis Market size is expected to reach USD 4.92 billion.

Who are the key players in Idiopathic Pulmonary Fibrosis Market?

Cipla Inc., Boehringer Ingelheim International GmbH, F. Hoffmann-La Roche Ltd, FibroGen, Inc. and Horizon Therapeutics plc are the major companies operating in the Idiopathic Pulmonary Fibrosis Market.

Which is the fastest growing region in Idiopathic Pulmonary Fibrosis Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Idiopathic Pulmonary Fibrosis Market?

In 2025, the North America accounts for the largest market share in Idiopathic Pulmonary Fibrosis Market.

What years does this Idiopathic Pulmonary Fibrosis Market cover, and what was the market size in 2024?

In 2024, the Idiopathic Pulmonary Fibrosis Market size was estimated at USD 4.58 billion. The report covers the Idiopathic Pulmonary Fibrosis Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Idiopathic Pulmonary Fibrosis Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Idiopathic Pulmonary Fibrosis Market Research

Mordor Intelligence provides a comprehensive analysis of the Idiopathic Pulmonary Fibrosis (IPF) market, drawing on our extensive experience in healthcare industry research. Our latest IPF annual report offers detailed insights into this critical respiratory health sector. It covers everything from pulmonary function testing methodologies to advanced antifibrotic therapy developments. The analysis also explores the growing field of Interstitial Lung Disease (ILD) and its relationship to IPF. Additionally, it examines innovative lung scarring treatment approaches and emerging respiratory therapeutics.

Our thorough examination of the IPF market size gives stakeholders crucial data-driven insights. These insights are available in an easy-to-read report PDF format for download. The report extensively covers the IPF industry landscape, including a detailed analysis of antifibrotic drug developments and the evolving market for pulmonary function testing. Healthcare providers, pharmaceutical companies, and investors in the ILD market benefit from our comprehensive evaluation of treatment protocols, technological advancements, and market dynamics. This ensures informed decision-making in this rapidly evolving therapeutic space.