Market Trends of Hydrogen Compressor Industry

Oil-based Segment Expected to Dominate the Market

- Oil-based lubricated compressors cost less and provide a longer service life than oil-free compressors. They are considered ideal for commercial and industrial applications until and unless they are used in industries where the consequences of oil contamination are considered very high and having an oil-free compressor is a must.

- Oil-based compressors are considered more efficient than oil-free compressors, as oil acts as a cooling medium, taking out approximately 80% of the compressor's heat during the compression process. They are also considered more suitable for industrial usage with requirements of a high compression ratio.

- In terms of capital outlay, lubricated oil-based compressors are often considered less expensive than oil-free compressors, with price differences often varying in the range of 30-40%. It may even reach 50%, depending upon factors such as capacity and industry-specific requirements, resulting in increased demand for oil-based hydrogen compressors.

- Although oil-based compressors are more affordable than oil-free compressors, they require continuous maintenance and greater attention to replacing filters and other components used to eliminate the risk of oil leakage. Ongoing oil contamination may result in severe consequences, such as spoiled or unsafe products, production downtime, and legal issues.

- Oil-based hydrogen compressors are mostly preferred in the manufacturing industry for glass purification, iron and steel industry, semiconductor manufacturing, welding, annealing, and heat-treating metals in power plants (coolant for generators), aerospace applications, pharmaceuticals, etc.

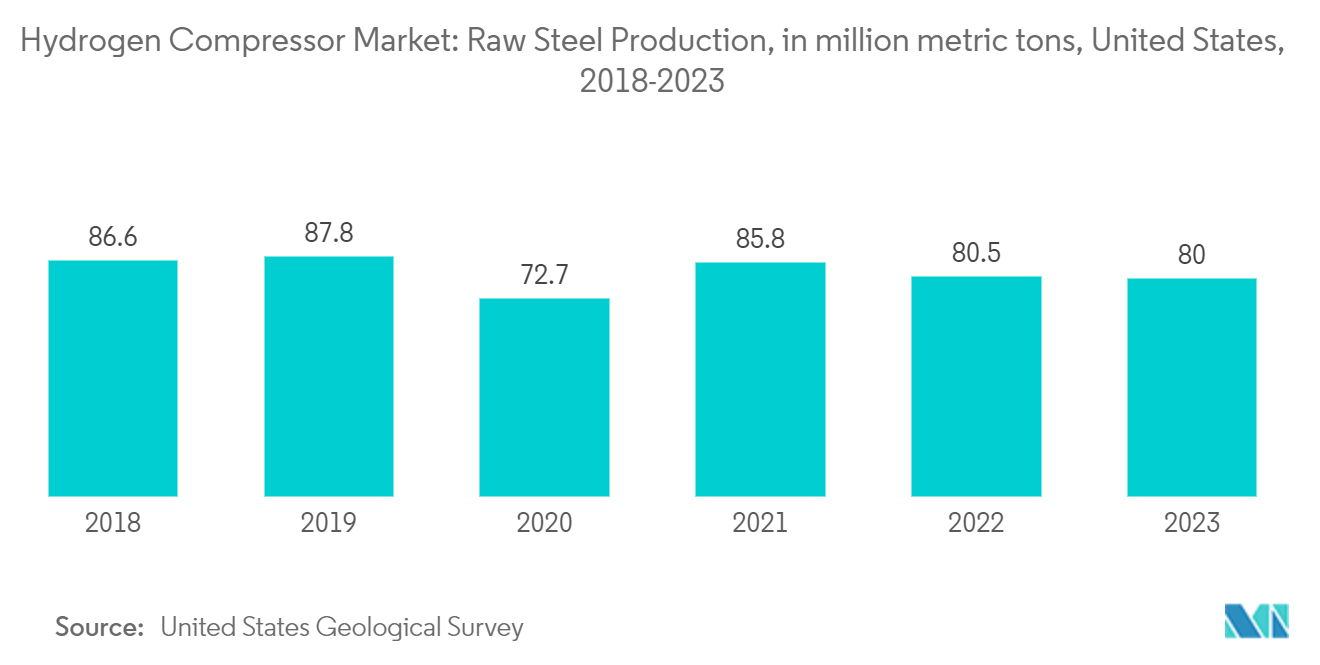

- According to the United States Geological Survey, in 2023, raw steel production in the United States was estimated to be 80 million metric tons. The US iron and steel industry produced raw steel in 2023 with an estimated value of about USD 110 billion, a 15% decrease from USD 128 billion in 2022. With the increasing industrialization, steel production may continue to increase, which, in turn, may create demand for oil-based hydrogen compressors.

- Furthermore, according to the World Steel Association, steel demand is expected to increase by 1.7% in 2024 and grow by 1.2% in 2025 to reach 1,815 million tonnes. Thus, the increase in demand for steel will drive the market's growth in the future.

- Insufficient lubrication persistently threatens premature wear of hydrogen compressor components, which may increase the maintenance cost of oil-based hydrogen compressors and limit their demand.

- Therefore, based on such factors, the oil-based type segment is expected to dominate the hydrogen compressor market during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

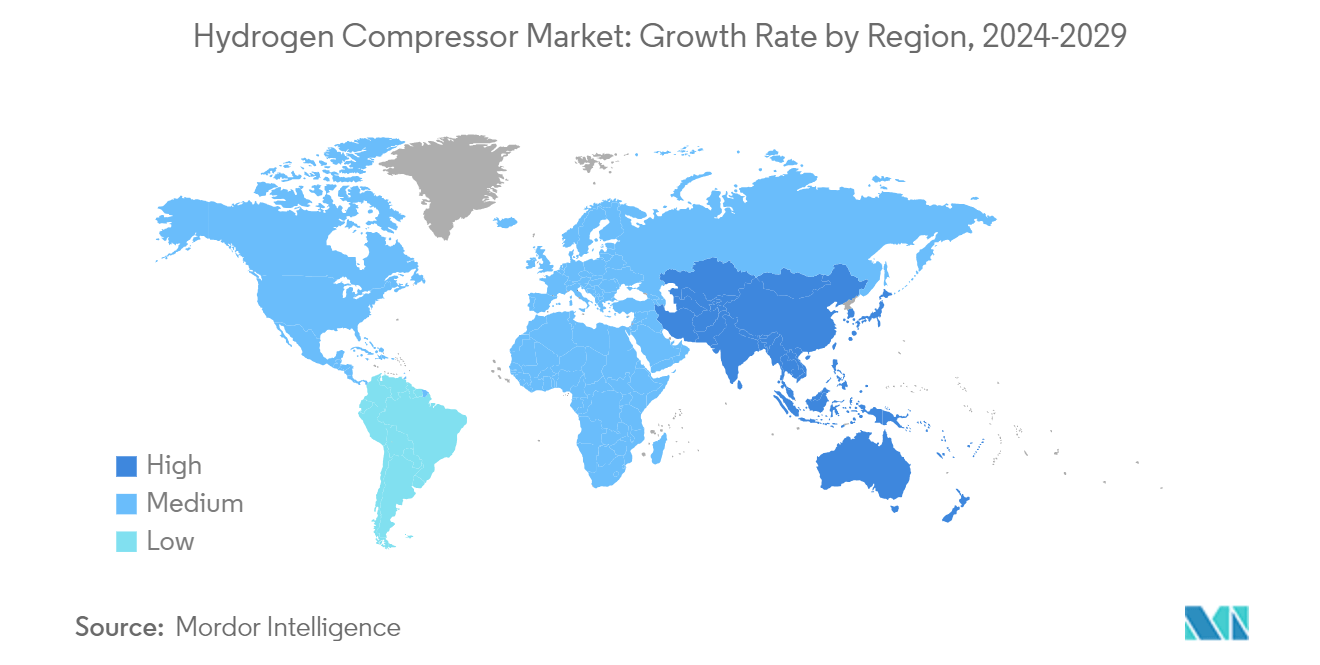

Asia-Pacific Expected to Dominate the Market

- Asia-Pacific is expected to be a promising market for fuel cells in the coming years because of the favorable government policies in countries such as China, Japan, and India.

- China is one of the world's largest and fastest-growing hydrogen compressor markets. The country has witnessed significant growth in its chemical, oil, gas, and manufacturing sectors in recent years.

- Hydrogen centrifugal compressors are used in refining and petrochemical industries, such as ethylene plants, for cracked-gas compression and refrigeration services. Due to ethylene and benzene production shortages, China has been investing in increasing its ethylene and benzene production capacities.

- Furthermore, several compressor companies are investing in Asian countries to expand the compressor market. For instance, in April 2024, PDC Machines and Kirloskar Pneumatic Company Limited agreed to provide hydrogen compression solutions throughout India. As per the agreement, PDC will support the local Indian hydrogen market, amplifying its reach in Asia by leveraging KPCL’s existing customer base. This will boost the significance of the hydrogen compressor market in the region.

- The development of hydrogen fuel cell vehicles and Japan's aim to build hydrogen fuel stations for recharging the vehicles are expected to drive the hydrogen compressor market.

- For instance, according to AIRIA (Japan), as of March 2023, 7.47 thousand fuel-cell electric vehicles were in use in Japan, increasing from less than 200 in 2015. The majority of these vehicles were primarily hydrogen-fueled passenger cars. This, in turn, is expected to drive the demand for hydrogen compressors for hydrogen fuel stations during the forecast period.

- Therefore, based on such factors, Asia-Pacific is expected to dominate the hydrogen compressor market during the forecast period.

Get Analysis on Important Geographic Markets

Download PDF