Hybrid Electric Vehicle Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

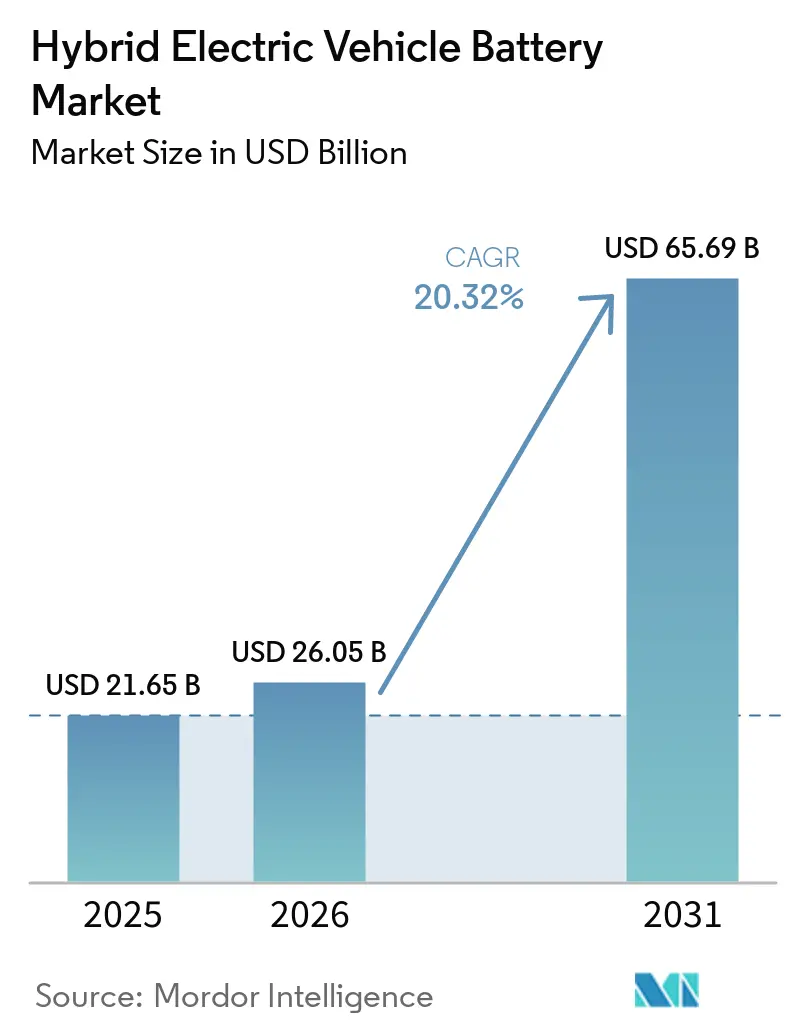

| Market Size (2026) | USD 26.05 Billion |

| Market Size (2031) | USD 65.69 Billion |

| Growth Rate (2026 - 2031) | 20.32% CAGR |

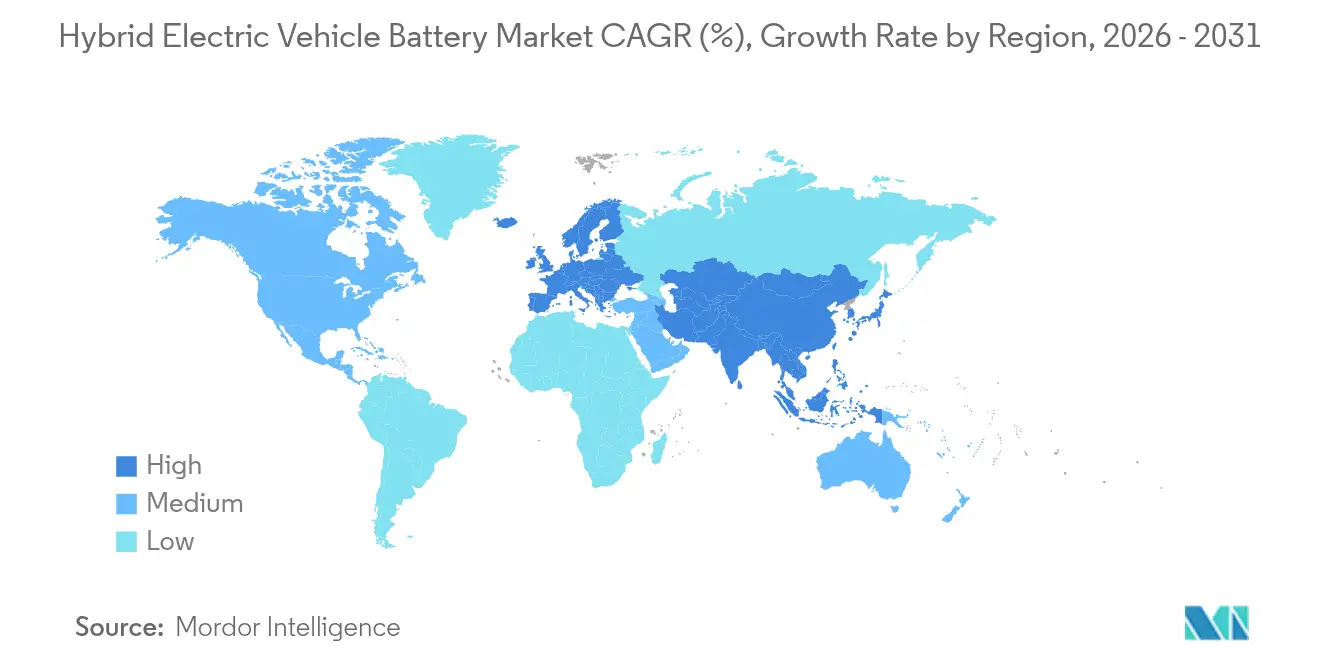

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Electric Vehicle Battery Market Analysis by Mordor Intelligence

Hybrid Electric Vehicle Battery Market size in 2026 is estimated at USD 26.05 billion, growing from 2025 value of USD 21.65 billion with 2031 projections showing USD 65.69 billion, growing at 20.32% CAGR over 2026-2031.

Automakers are scaling hybrids to meet tightening CO₂ caps, while the steep slide in lithium-ion pack prices to USD 115 per kWh in 2024 has narrowed the total-cost gap with combustion powertrains. Rapid energy-density gains, multi-chemistry flexibility, and AI-enabled battery management systems are intensifying supplier competition. Asia-Pacific’s production dominance, European regulatory mandates, and North American local-content rules are reshaping investment flows. Meanwhile, solid-state and sodium-ion prototypes are drawing capital as next-generation options that promise higher density and enhanced safety.

Key Report Takeaways

- By battery chemistry, lithium-ion retained 75.12% of the hybrid electric vehicle battery market share in 2025, whereas solid-state and sodium-ion batteries are forecast to expand at a 34.1% CAGR to 2031.

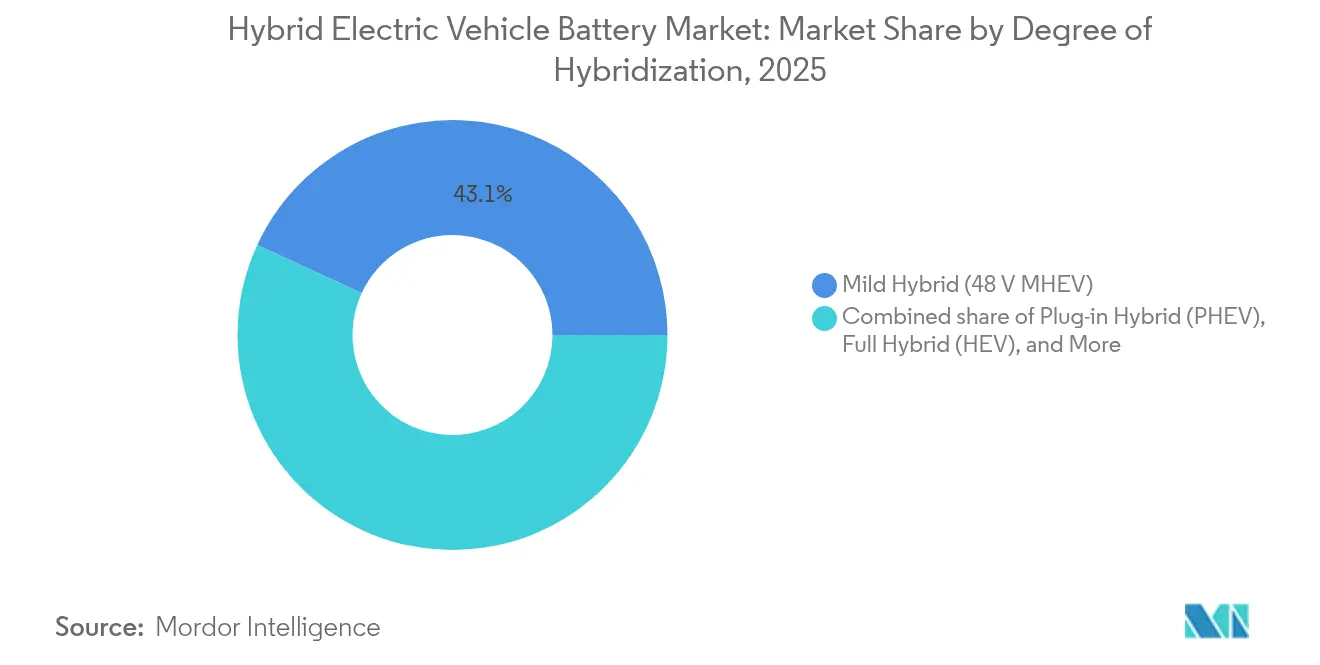

- By degree of hybridization, mild hybrids accounted for 43.12% of 2025 unit shipments, and this sub-segment is expected to grow at a 22.6% CAGR through 2031.

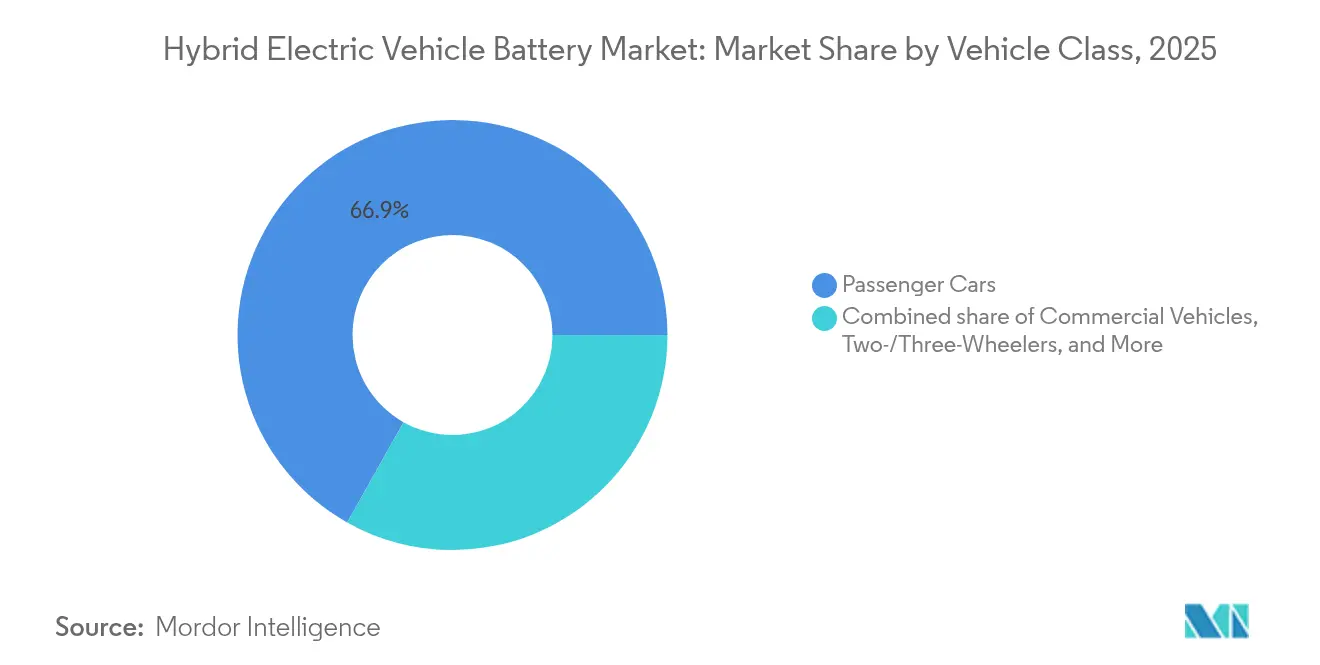

- By vehicle class, passenger cars led with 66.85% revenue share in 2025, while two- and three-wheelers are predicted to advance at a 23.5% CAGR to 2031 under subsidy programs in India and Southeast Asia.

- By voltage class, the 200 to 400 V segment accounted for 49.1% of unit shipments in 2025, while the Above 400 V segment is projected to grow at a CAGR of 25.4% through 2031.

- By geography, Asia-Pacific commanded 47.35% of 2025 sales and is projected to register a 22.3% CAGR through 2031 on the back of China’s 75% cell-production share.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hybrid Electric Vehicle Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating HEV production volumes under CO₂ mandates | +4.5% | EU, China, global spillover | Medium term (2-4 years) |

| Rapid fall in Li-ion $/kWh and higher energy density | +3.8% | Global, fastest in Asia-Pacific | Short term (≤ 2 years) |

| OEM migration from NiMH to Li-ion chemistries | +2.9% | Japan, North America | Medium term (2-4 years) |

| 48 V micro-hybrid boom creating low-cost Li-ion demand | +3.2% | Europe, North America, China | Short term (≤ 2 years) |

| Recycling-mandate-driven secondary metals supply | +1.8% | EU lead, North America emerging | Long term (≥ 4 years) |

| AI-enabled cloud BMS extending battery warranties | +1.5% | Premium segments worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating HEV Production Volumes Under CO₂ Mandates

CO₂ regulations in the European Union, China, and California are prompting automakers to scale hybrid output to bridge the gap to 100% zero-emission sales targets.[1]European Commission, “Regulation (EU) 2019/631 – CO₂ Standards for Cars and Vans,” EC.EUROPA.EU Non-compliance fines that hit EUR 95 per gram of CO₂ overshoot per vehicle create a clear economic case for hybrids. Toyota’s 40 GWh lithium-ion sourcing deal with Panasonic and Stellantis’s 1.2 million-unit hybrid capacity are emblematic responses. China’s dual-credit regime further rewards long-range plug-in hybrids, nudging OEMs to enlarge battery packs. These converging policies have raised hybrid launch velocity at most mainstream brands.

Rapid Fall in Li-ion $/kWh & Higher Energy Density

Lithium-ion pack prices fell 20% year over year to USD 115 per kWh in 2024, the sharpest decline since 2017, as new mining capacity in Australia and Chile relieved lithium carbonate shortages.[2]BloombergNEF, “Battery Pack Prices Fall to $115/kWh, Steepest Decline Since 2017,” BLOOMBERG.COM Cost learning curves show that each doubling of cumulative output trims prices by roughly 25%. CATL’s cell-to-pack Qilin design lifts energy density to 255 Wh/kg and demonstrates 100 km electric-only range in plug-in hybrids without oversizing the pack. LFP cells have slipped below USD 100 per kWh in China, opening mild-hybrid and two-wheeler opportunities previously reserved for lead-acid units.

OEM Migration From NiMH to Li-ion Chemistries

Honda’s USD 4.4 billion joint venture with LG Energy Solution in Ohio targets a 20% cost cut versus imported packs. Toyota, while sustaining NiMH output for price-sensitive markets, is shifting plug-in variants to Li-ion and accelerating solid-state pilots for a 2027 launch. NiMH’s 70-80 Wh/kg ceiling cannot meet emerging range expectations, yet its thermal stability keeps it relevant where cost and safety outshine density. Hyundai, Volkswagen, and Ford have already standardized Li-ion across upcoming hybrid portfolios.

48 V Micro-Hybrid Boom Creating Low-Cost Li-ion Demand

Mild-hybrid 48 V systems deliver 15-20% fuel savings at roughly half the incremental cost of full hybrids. Stellantis alone plans 1.2 million annual 48 V units, while Mercedes-Benz, BMW, and Audi have rolled the architecture across European models. Battery suppliers such as Clarios and Gotion are pivoting from lead-acid to lithium-based chemistries capable of 10,000-cycle durability. Lower per-pack energy content keeps absolute lithium demand modest, supporting rapid scale-up.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-metal supply risk amid BEV competition | -2.1% | Global; lithium, cobalt, nickel hot spots | Medium term (2-4 years) |

| Sparse PHEV fast-charge infrastructure | -1.4% | India, Southeast Asia, Latin America, Sub-Saharan Africa | Long term (≥ 4 years) |

| Thermal-runaway concerns in compact packs | -1.2% | EU and North America regulatory zones | Short term (≤ 2 years) |

| Geopolitical scrutiny of Chinese battery IP | -1.8% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Critical-Metal Supply Risk Amid BEV Competition

Lithium demand could hit 3.3 million t by 2030, six times 2022 usage, and BEVs consume three to five times more per vehicle than hybrids. Cobalt remains heavily concentrated in the DRC, while Indonesia dominates nickel processing. Price volatility complicates long-term supply deals; lithium carbonate plunged from USD 80,000/t in 2022 to USD 10,000/t in late 2024, deterring fresh mine investment. Smaller hybrid packs reduce absolute exposure but do not escape spot-price swings when BEV makers lock in multi-year contracts.

Sparse PHEV Fast-Charge Infrastructure in Emerging Markets

India had only 12,146 public chargers in 2024, 80% in tier-one cities, limiting the utility of 50 km electric-range plug-in hybrids for suburban commuters. Similar gaps exist across Indonesia and Vietnam. Policymakers often channel incentives to pure BEVs, leaving plug-in hybrids without parallel infrastructure support, which in turn weakens consumer adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Solid-State and Sodium-Ion Challenge Li-Ion Dominance

Lithium-ion technologies captured 75.12% of 2025 revenue for the hybrid electric vehicle battery market, yet solid-state and sodium-ion batteries are forecast to grow 34.1% annually to 2031. Lithium-ion vendors continue to refine NMC and LFP blends, cutting cobalt usage and improving volumetric efficiency. Toyota and Nissan plan solid-state commercial launches before 2028, targeting 500 Wh/kg cells that could double electric-only range without enlarging packs. Sodium-ion prototypes from CATL already deliver 160 Wh/kg and superior cold-weather retention, positioning the chemistry for entry-level hybrids in colder climates. Nickel-metal hydride endures where affordability and thermal stability trump energy density, chiefly in Southeast Asia. Lead-acid is relegated to auxiliary 12 V systems. The hybrid electric vehicle battery market size attributable to lithium-ion is expected to approach USD 46.8 billion by 2031, while emerging chemistries will jointly exceed USD 7.35 billion that year.

A tightening patent landscape is shaping competitive behavior. Toyota holds more than 1,300 solid-state-related patents, whereas CATL and BYD control key cell-to-pack designs. Licensing is becoming a realistic path for latecomers wishing to avoid litigation. Overall, the hybrid electric vehicle battery industry anticipates a multi-chemistry coexistence, with lithium-ion retaining volume leadership but ceding margin leadership to solid-state once scale materializes.

By Degree of Hybridization: Mild Hybrids Lead While PHEVs Face Headwinds

Mild hybrids achieved 43.12% unit volume in 2025, delivering the lowest-cost compliance option for fleets that must hit CO₂ targets quickly. The hybrid electric vehicle battery market size generated by mild hybrids is projected to surpass USD 22.24 billion in 2031, rising at a 22.6% CAGR. Full hybrids remain popular in Japan and North America thanks to two decades of reliability data. Plug-in hybrids enjoy corporate-fleet tax benefits in Europe but struggle in emerging markets that lack fast-charging networks. Range-extender architectures thrive mainly in China, led by Li Auto, though their global prospects hinge on emissions-credit treatment. Automakers are bundling identical cell formats across hybrid types to secure scale economies, yet software calibration differs markedly, increasing engineering complexity and favoring vertically integrated suppliers.

PHEV growth will depend on whether regulators continue to count their low CO₂ test-cycle ratings in the next phase of standards. Germany’s phase-out of purchase rebates in 2024 cut PHEV registrations by half, showing sensitivity to policy shifts. In emerging economies, conventional hybrids with no charging requirement and low-kWh packs remain the practical electrification entry point.

By Voltage Class: 800 V Platforms Gain Premium Momentum

Battery packs in the 200-400 V band held 48.62% revenue share in 2025, dominant in full hybrids and affordable plug-ins. Above-400 V packs, largely 800 V architectures, are set to grow 24.8% per year as Porsche, Hyundai, and General Motors push sub-20-minute fast-charging as a premium differentiator. Silicon-carbide inverters, although triple the cost of silicon, enable thinner cabling and lower heat loss. The hybrid electric vehicle battery market share for 800 V systems could reach 12.35% by 2031 as cost falls and infrastructure spreads.

Up-to-60 V platforms, centered on 48 V mild-hybrids, avoid high-voltage safety regulations, cutting harness and training costs. Between 60 V and 200 V, legacy NiMH hybrids persist, notably the Toyota Prius. Voltage migration depends on model price points and regional charging speeds; value-oriented markets in Southeast Asia will remain below 400 V through the forecast period.

By Vehicle Class: Two-Wheelers Surge While Passenger Cars Plateau

Passenger cars supplied 66.85% of the hybrid electric vehicle battery market revenue in 2025, but are trending toward single-digit growth as many OEMs divert R&D budgets to BEVs. By contrast, two- and three-wheelers in India, Vietnam, and Indonesia will drive a 23.5% CAGR, supported by USD 180 FAME II subsidies and proliferating battery-swapping ecosystems. Commercial vehicles, particularly city buses, use lithium-iron-phosphate packs with >3,000 cycles to capture regenerative braking benefits. Off-highway segments remain experimental; Caterpillar’s hybrid excavator tests highlight the engineering demands of harsh-duty cycles but could open another multi-billion-dollar niche by 2030.

The hybrid electric vehicle battery market size for two-wheelers is forecast to exceed USD 7.31 billion by 2031, while commercial vehicles could approach USD 10.42 billion, together diversifying demand beyond passenger cars.

Geography Analysis

Asia-Pacific accounted for 47.35% of 2025 revenue and is forecast to register a 22.3% CAGR through 2031, propelled by China’s 75% cell-production share and CATL’s 37.5% vendor position. Korean and Japanese suppliers are localizing output in the United States and Europe to evade geopolitical barriers, yet they continue to ship high-value electrodes and separators from domestic plants. India’s fast-growing two-wheeler segment relies on imported cells, and its USD 2.4 billion production-linked incentive scheme seeks to fill that supply gap.

Europe held 28.15% of 2025 revenue. Subsidy withdrawals hurt plug-in demand, but corporate fleets still favor PHEVs for tax advantages. The EU Battery Regulation now obliges carbon-footprint declarations and recycling thresholds, pushing gigafactory operators into closed-loop models. Northvolt’s insolvency underlines cost pressure from Asian imports, while LG Energy Solution and Samsung SDI advance large projects in Poland and Hungary to maintain regional supply.

North America generated 17.65% of 2025 sales. The Inflation Reduction Act’s component-origin rules are drawing USD 11.5 billion of announced battery investment from LG Energy Solution, Samsung SDI, and Panasonic. Mexico is positioning itself as a near-shoring alternative by promoting duty-free pack assembly in Nuevo León. South America and the Middle East-Africa combined held 6.85% share; Brazil’s ethanol-hybrid initiatives and the UAE’s electric-bus rollouts illustrate diverse regional strategies.

Mordor Intelligence provides coverage of the hybrid electric vehicle battery market across other key regional markets, including North America, South America, Europe, Asia, and Middle East and Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States, United Kingdom, China, India, and Germany incorporating local coverage and market participation, as required.

Competitive Landscape

The top five suppliers, CATL, LG Energy Solution, BYD, Panasonic, and Samsung SDI, held 68% of 2024 revenue, giving the hybrid electric vehicle battery market a moderate concentration profile. Vertically integrated BYD, with 16.4% market share, minimizes lead times by keeping cathode, anode, and module production in-house. CATL’s cloud-based battery management platform underpins decade-long warranties and improves renewal income streams. Automakers such as Ford, Stellantis, and General Motors are co-investing in U.S. and European gigafactories to lock in supply, while Tesla’s 4680 cylindrical-cell ramp aims to cut reliance on outsiders by 2026.

Mid-tier entrants like Microvast, Farasis, and Svolt target niches, fast-charging commercial vehicles, high-nickel premium hybrids, and cobalt-free LFP cells, respectively. Intellectual-property positions in solid-state electrolytes, silicon-dominant anodes, and cell-to-pack structures will be decisive as next-generation chemistries commercialize after 2027. Trade policy is another competitive lever; Korean and Japanese firms benefit from “trusted ally” status under U.S. rules, whereas Chinese giants must set up local joint ventures or risk exclusion.

Hybrid Electric Vehicle Battery Industry Leaders

Primearth EV Energy (Toyota-Panasonic)

Panasonic Energy Co.

LG Energy Solution

CATL

Samsung SDI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Volvo Cars announced the reintroduction of the XC70 as a long-range plug-in hybrid SUV in May 2025. The model includes lithium iron phosphate (LFP) battery options of 21.2 kWh and 39.6 kWh, providing electric-only ranges of up to 131 miles, depending on the configuration.

- September 2024: Samsung SDI and General Motors broke ground on a USD 2 billion Indiana pouch-cell plant targeted for 2026 start-up.

- August 2024: Panasonic increased Kansas 4680 output to 40 GWh and secured Subaru’s hybrid program as a new customer.

- April 2024: LG Energy Solution began production at its USD 5.5 billion Arizona plant, adding 40 GWh of annual capacity with automated cell-to-pack lines.

Global Hybrid Electric Vehicle Battery Market Report Scope

A Hybrid Electric Vehicle (HEV) battery is a rechargeable energy storage system that powers the electric motor of a hybrid vehicle. HEVs combine a conventional internal combustion engine (ICE) with an electric propulsion system. The battery in an HEV is crucial for capturing and storing energy, particularly during regenerative braking, and for providing additional power during acceleration.

The Global hybrid electric vehicle battery market is segmented by battery chemistry, degree of hybridization, voltage class, vehicle class, and Geography. By battery chemistry, the market is segmented into Lithium-ion (NMC, NCA, LFP, LTO), Nickel-Metal Hydride (NiMH), Lead-acid, and Emerging Solid-State/Sodium-ion. The market is segmented into Mild Hybrid (48 V MHEV), Full Hybrid (HEV), Plug-in Hybrid (PHEV), and Range-Extender Hybrid by degree of hybridization. The market is divided among Up to 60 V, 60 to 200 V, 200 to 400 V, and Above 400 V by voltage class. By vehicle class, the market is segmented into Passenger Cars, Commercial Vehicles, Two-/Three-Wheelers, and Off-Highway and Specialty. The report also covers the market size and forecasts for the global hybrid electric vehicle battery market across major regions. The Report Offers the Market Size and Forecasts in Revenue (USD) for all the Above.

| Lithium-ion (NMC, NCA, LFP, LTO) |

| Nickel-Metal Hydride (NiMH) |

| Lead-acid |

| Emerging Solid-State/Sodium-ion |

| Mild Hybrid (48 V MHEV) |

| Full Hybrid (HEV) |

| Plug-in Hybrid (PHEV) |

| Range-Extender Hybrid |

| Up to 60 V |

| 60 to 200 V |

| 200 to 400 V |

| Above 400 V |

| Passenger Cars |

| Commercial Vehicles |

| Two-/Three-Wheelers |

| Off-Highway and Specialty |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Norway | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Battery Chemistry | Lithium-ion (NMC, NCA, LFP, LTO) | |

| Nickel-Metal Hydride (NiMH) | ||

| Lead-acid | ||

| Emerging Solid-State/Sodium-ion | ||

| By Degree of Hybridization | Mild Hybrid (48 V MHEV) | |

| Full Hybrid (HEV) | ||

| Plug-in Hybrid (PHEV) | ||

| Range-Extender Hybrid | ||

| By Voltage Class | Up to 60 V | |

| 60 to 200 V | ||

| 200 to 400 V | ||

| Above 400 V | ||

| By Vehicle Class | Passenger Cars | |

| Commercial Vehicles | ||

| Two-/Three-Wheelers | ||

| Off-Highway and Specialty | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Norway | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will hybrid electric vehicle battery demand be by 2031?

The hybrid electric vehicle battery market size is forecast to reach USD 65.69 billion in 2031, up from USD 26.05 billion in 2026.

Which battery chemistry is growing fastest in hybrid applications?

Solid-state and sodium-ion chemistries are projected to grow at a 34.1% CAGR through 2031 as they offer higher energy density and improved safety.

Why are 48 V mild hybrids so popular with carmakers?

They cut CO₂ by up to 20% at roughly half the incremental hardware cost of full hybrids, making them an economical compliance bridge to upcoming emission caps.

What regions dominate battery production for hybrids?

Asia-Pacific leads with 47.35% revenue share and 75% of global cell output, driven mainly by Chinese suppliers.

How are regulations shaping hybrid battery recycling?

The EU Battery Regulation mandates 63% lithium recovery by 2030, prompting gigafactories to integrate closed-loop recycling to meet compliance and cost goals.

What impact will the U.S. Inflation Reduction Act have on supply chains?

It restricts tax credits for vehicles containing Chinese battery components after 2026, accelerating North American gigafactory investments by Korean and Japanese firms.

Page last updated on: