Market Overview

| Study Period | 2020 - 2031 |

|---|---|

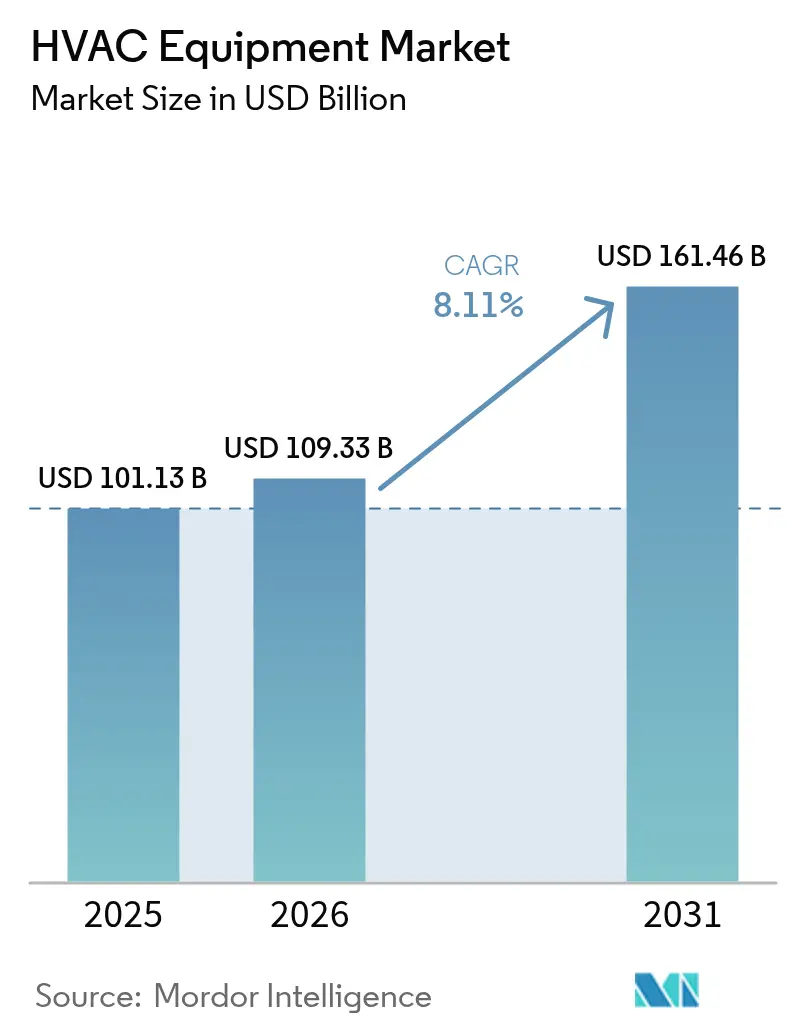

| Market Size (2026) | USD 109.33 Billion |

| Market Size (2031) | USD 161.46 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

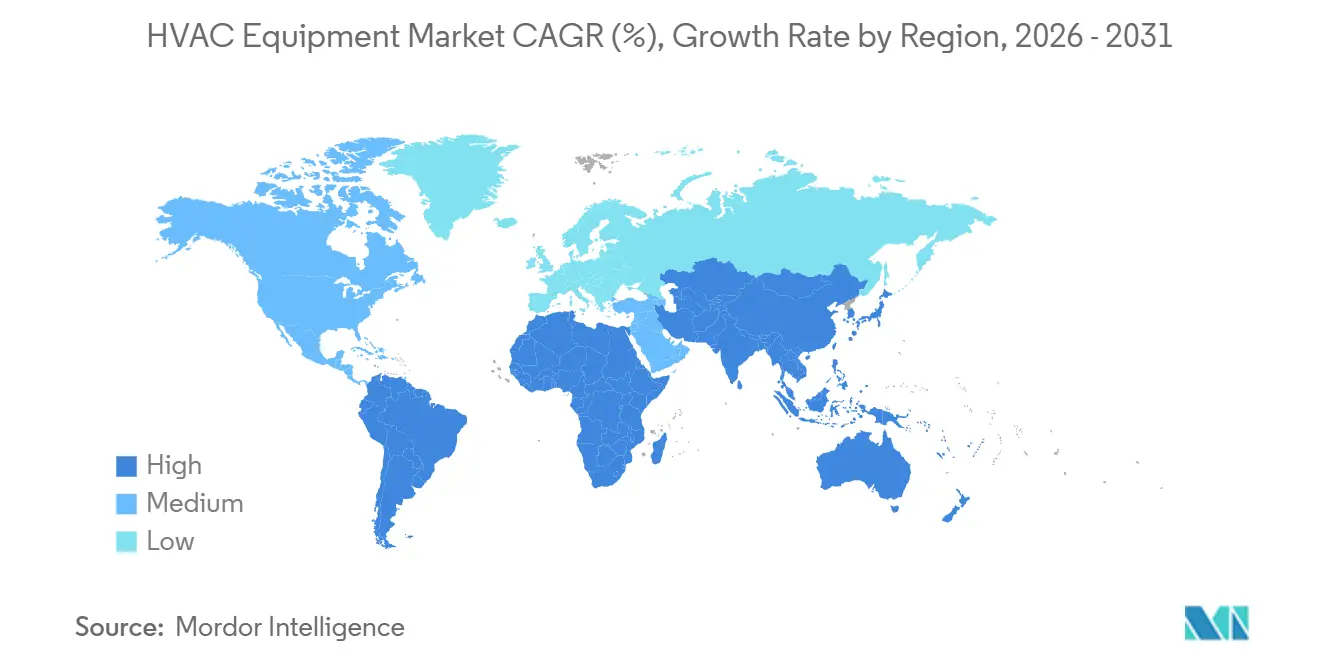

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HVAC Equipment Market Analysis by Mordor Intelligence

The HVAC equipment market size is projected to expand from USD 101.13 billion in 2025 and USD 109.33 billion in 2026 to USD 161.46 billion by 2031, registering an 8.11% CAGR between 2026 and 2031. Heightened policy pressure to eliminate fossil-fuel boilers in Europe, rapid data-center construction in cold-climate corridors, and widespread adoption of variable-refrigerant-flow (VRF) systems in Asian high-rises are accelerating equipment replacement cycles and pulling forward new-build demand. Europe’s Energy Performance of Buildings Directive eliminated standalone gas boilers in new projects from 2025, sending heat-pump retrofits sharply higher and compressing payback periods to seven years. Hyperscale cloud operators clustering campuses in the Nordics and the Frankfurt-London-Amsterdam-Paris-Dublin (FLAP-D) corridor now cover up to 70% of annual cooling hours with free cooling, slashing mechanical-chiller runtimes and lifting precision-cooling capital budgets. Meanwhile, VRF systems are replacing ducted splits in Chinese, Indian, and Southeast Asian towers because they fit tight floorplates, deliver zone-level control, and cut energy use by 20%-30%.

Key Report Takeaways

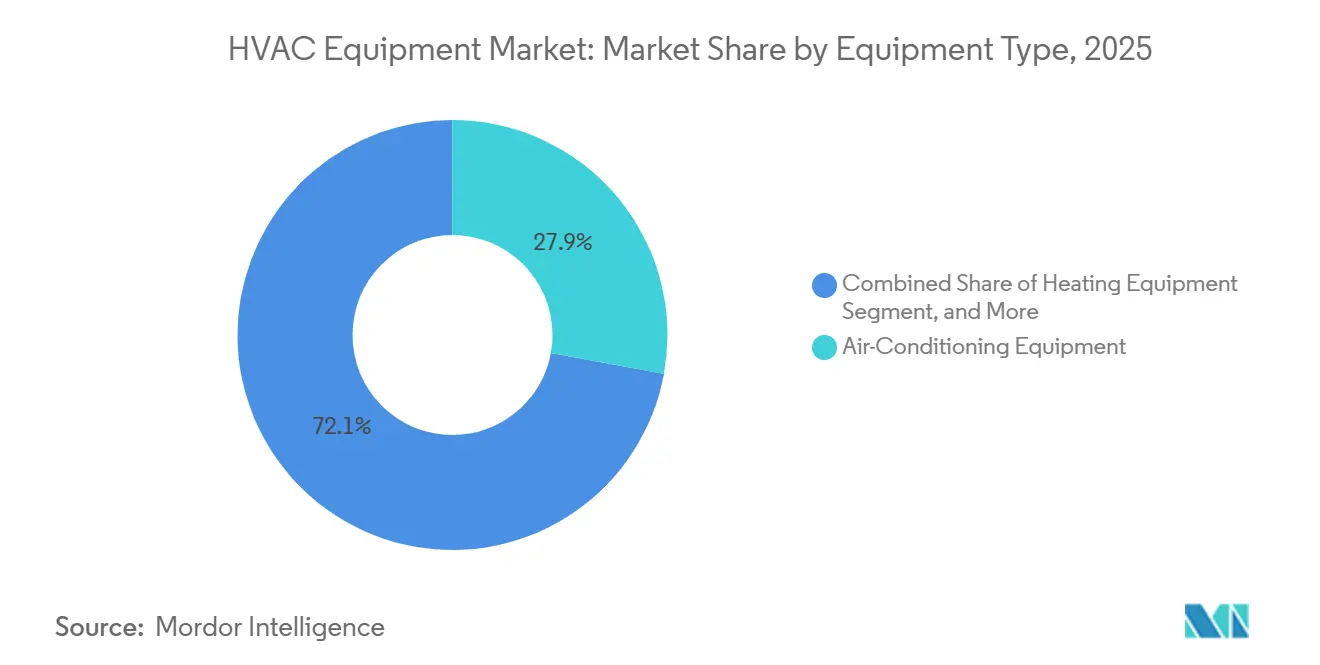

- By equipment type, air-conditioning systems retained the largest 27.89% share of the HVAC equipment market in 2025, while heating equipment delivered the fastest 8.78% CAGR through 2031.

- By installation type, retrofit and replacement projects accounted for 62.33% of 2025 revenue; however, new construction is advancing at an 8.58% CAGR on the back of data-center and Asian high-rise pipelines.

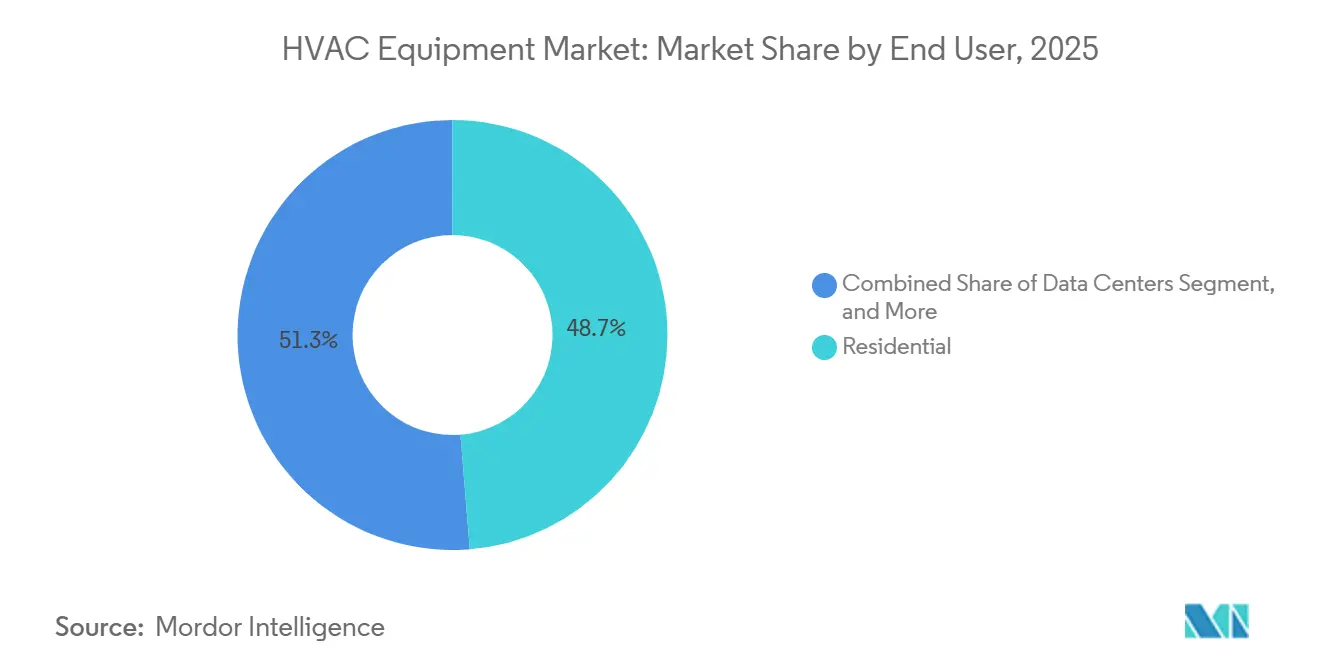

- By end user, residential applications represented 48.72% of 2025 spending, whereas data centers are expanding at an 8.74% CAGR as rack densities accelerate liquid-cooling adoption.

- By commercial building type, data centers led with 21.34% revenue share in 2025; healthcare facilities are forecast to post the quickest 9.33% CAGR to 2031.

- By geography, Asia Pacific captured 38.56% of 2025 sales; Africa, though smaller in absolute size, is projected to grow the fastest at 9.12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global HVAC Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent building energy codes in Europe accelerating heat-pump adoption | +1.8% | Europe, with spillover to UK and Scandinavia | Medium term (2-4 years) |

| Surge in data-center construction in Nordics and FLAP-D region elevating precision cooling demand | +1.5% | Europe (Nordics, FLAP-D), North America | Short term (≤ 2 years) |

| Rapid uptake of variable-refrigerant-flow systems in high-rise Asian residential complexes | +1.3% | Asia Pacific (China, India, ASEAN) | Medium term (2-4 years) |

| Inflation Reduction Act tax credits catalyzing early furnace replacement cycles | +1.2% | United States | Short term (≤ 2 years) |

| District-heating expansion in Eastern Europe spurring large-capacity boiler retrofits | +0.9% | Eastern Europe (Poland, Czech Republic, Hungary) | Long term (≥ 4 years) |

| Solar-hybrid HVAC packages gaining traction in off-grid African mining camps | +0.6% | Africa (Botswana, Zambia, DRC) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Building Energy Codes in Europe Accelerating Heat-Pump Adoption

Europe’s 2024 directive outlawed new fossil-fuel boilers from 2025 and requires the worst 16% of non-residential buildings to meet minimum energy-performance thresholds by 2030, forcing owners to install air- or ground-source heat pumps that exceed seasonal performance factors of 3.5.[1]European Parliament, “Directive (EU) 2024/1275 on the Energy Performance of Buildings,” europarl.europa.eu National statutes amplify the push: France’s RE2020 caps carbon intensity at 4 kg CO₂ e /m²-year for homes, Germany’s amended Gebäudeenergiegesetz demands 65% renewable heat, and both frameworks align economically when carbon taxes and avoided gas purchases reduce payback periods below a decade. OEMs have responded. Daikin tripled Belgian capacity to 1.5 million units per year by 2027, underscoring confidence that policy-led demand will persist. Heat-pump adoption, therefore, delivers the single-largest positive uplift to the HVAC equipment market growth outlook.

Surge in Data-Center Construction in Nordics and FLAP-D Region Elevating Precision Cooling Demand

Cloud hyperscalers continue clustering megawatt-scale facilities in the Nordics, where average annual temperatures of 5 °C-12 °C allow air-side economizers to serve up to 70% of cooling hours, cutting power-usage-effectiveness below 1.2. Meta’s 150 MW campus in Odense leveraged seawater cooling to eliminate winter mechanical refrigeration and save USD 12 million per year in energy expense. Microsoft’s Stockholm expansion relies on adiabatic towers operating within 2 °C of ambient.[2]Microsoft Azure, “Stockholm Region Expansion,” azure.microsoft.com Direct-to-chip liquid solutions now pull 80% of heat before it enters data halls, permitting 30 kW-per-rack densities that command price premiums over legacy air units. Precision cooling, therefore, becomes a high-margin subsegment, pushing the overall HVAC equipment market upwards.

Rapid Uptake of VRF Systems in High-Rise Asian Residential Complexes

VRF systems captured 35% of new high-rise installations in China, India, and Southeast Asia in 2025 because they eliminate bulky duct shafts, enable room-by-room temperature control, and modulate compressors to match part-load demand. Mumbai’s 78-story World One tower serves 400 apartments from rooftop condensers, avoiding facade clutter and streamlining maintenance. Vietnamese building codes adopted in 2024 introduced compulsory energy certificates, favoring VRF with a part-load efficiency ratio above 4.0. LG’s Multi V 5 provides simultaneous heating and cooling, recovering waste heat to cut annual HVAC energy by 18%. Subsidy schemes in China reimburse 15% of incremental VRF costs, triggering 22% sales growth at Gree in 2025.

Inflation Reduction Act Tax Credits Catalyzing Early Furnace Replacement Cycles

The United States 25C credit refunds 30% of the cost, up to USD 2,000, for qualifying heat pumps and USD 600 for efficient furnaces, pushing replacements forward by roughly 18 months. Carrier reported a 28% jump in residential heat-pump shipments in 1H 2025, with Rheem noting that 40% of units qualified for enhanced, income-based caps. Lennox opened a USD 70 million plant in Texas dedicated to heat-pump production in 2024, banking on sustained double-digit domestic growth. Although a technician shortage extended installation backlogs into mid-2026, OEM backorders confirm that incentives materially increase addressable demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of low-GWP refrigerant transition for OEMs | -1.2% | Global, with acute pressure in EU and North America | Medium term (2-4 years) |

| Talent shortage of certified HVAC technicians in mature markets | -0.9% | United States, Germany, United Kingdom, Canada | Short term (≤ 2 years) |

| Semiconductor supply-chain volatility constraining VRF inverter availability | -0.7% | Global, with bottlenecks in Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Stringent F-gas quotas in EU increasing compliance burden for importers | -0.6% | European Union, with spillover to UK and EFTA states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Low-GWP Refrigerant Transition for OEMs

EU F-gas quotas fall to 2.4% of 2015 baselines by 2030, forcing R410A retirement and driving capital spending of USD 50 million-USD 100 million per manufacturing site to retool for mildly flammable A2L refrigerants. Daikin cites USD 18 million to convert a single line; Johnson Controls expects USD 250 million group-wide through 2027, compressing margins by 120 bp during the transition. Larger heat-exchanger coils, additional leak sensors, and new safety certifications add USD 300-USD 500 per unit, costs difficult to pass through in price-sensitive segments. Until tooling amortizes, the drag on profitability acts as a modest brake on HVAC equipment market expansion.

Talent Shortage of Certified HVAC Technicians in Mature Markets

Retirements and lagging apprenticeship enrolment leave the United States short of an estimated 50,000 technicians by 2030.[3]U.S. Bureau of Labor Statistics, “HVAC Technician Outlook,” bls.gov ACCA members blamed workforce shortages for a 15% backlog of sold but not installed units in 2025. Germany faced a 60,000-installer deficit in 2025, delaying 18% of planned heat-pump projects. The United Kingdom enrolled only 3,200 HVAC apprentices in 2024, against targets of 15,000. A2L refrigerant protocols require extra certification, yet fewer than 30% of technicians had completed the 40-hour course by mid-2025. Labor scarcity, therefore, caps the pace at which the HVAC equipment market can physically deploy ordered systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Heat Pumps Extend Lead Over Legacy Heating

Heating equipment expanded at an 8.78% CAGR through 2031, outpacing the overall HVAC equipment market as heat pumps displaced furnaces and boilers in both new projects and retrofits. By 2025, heating revenue, heat pumps captured 58%, while boilers and furnaces retained 32%, because large-capacity commercial boilers remain economical for district-heating upgrades in Eastern Europe. The shift widened after EU rules banned standalone fossil-fuel boilers, and the United States, by combining federal and utility rebates, compressed payback periods from 10 to 6 years.

Air-conditioning equipment, although accounting for the largest 27.89% slice of 2025 revenue, grew more slowly because North American and Western European households operate at near-saturation and focus on efficiency-driven replacements. Nonetheless, VRF and liquid-cooling solutions posted double-digit gains inside the air-conditioning category, buoyed by mixed-use high-rises and data-center rack densities. Ventilation products accounted for 22% of 2025 sales, following upgrades in healthcare and education to MERV 13 filtration under ASHRAE 241. The blend of robust heating growth and steady cooling replacements confirms a balanced demand mix that supports the long-run expansion of the HVAC equipment market.

By Installation Type: Retrofit Dominates Value While New Construction Accelerates

Retrofit and replacement accounted for 62.33% of 2025 revenue, reflecting the aging global building stock and energy-savings math that favor swapping fixed-speed units for inverter-driven models. Replacing a 20-year-old 10 SEER unit with a 2025 model featuring a 16 SEER rating can result in significant energy savings. The older unit consumes 60% more electricity compared to the newer model, leading to annual savings of USD 400 to USD 600 for commercial owners. These savings not only reduce operational costs but also justify the early replacement of outdated equipment.

New construction, however, is advancing at an 8.58% CAGR thanks to data-center campuses in the Nordics and FLAP-D corridor, residential towers in India, Vietnam, and the Philippines that specify VRF at first fit-out, and Middle-Eastern industrial plants requiring precision cooling. Developers frequently allocate 8%-12% of project budgets to mechanical systems in high-performance buildings, driving significant upfront demand. The convergence of retrofit techniques, modular AHUs, ductless minis, and rooftop packaged units blurs boundaries, yet retrofit remains the value anchor of the HVAC equipment market size in the near term.

By End User: Data Centers Propel High-Value Growth

Residential buyers accounted for 48.72% of 2025 revenue, but growth lags at a 7.8% CAGR because penetration in developed economies exceeds 90% and the replacement interval stretches to 15 years. Data centers, conversely, contributed only 8% of 2025 revenue yet are expanding at an 8.74% CAGR as AI inference workloads triple rack heat densities and mandate liquid-cooling architectures commanding 40%-60% price premiums.

Commercial buildings posted 32% of 2025 revenue and an 8.5% CAGR as hospitals rushed to meet ASHRAE 170 ventilation rules, hotels installed guest-room mini-splits, and offices integrated HVAC with occupancy analytics through smart-building software. Industrial facilities accounted for 12% of turnover, rising 7.2% annually, driven by semiconductor, pharmaceutical, and food-processing lines that demand tight thermal tolerances. Collectively, these trends reinforce data centers as the premium growth wedge inside the broader HVAC equipment market.

By Commercial Building Type: Healthcare and Hospitality Lift Mixed-Use Spending

Data-center projects dominated the category, accounting for 21.34% of commercial building share in 2025, leveraging liquid-cooling and redundancy requirements that yield gross margins of 35%-40 % for OEMs. As infection-control standards mandated increased ventilation in patient rooms, healthcare facilities captured an 18% market share, witnessing an 9.33% CAGR. This growth highlights the rising emphasis on maintaining stringent air quality standards to ensure patient safety and reduce the risk of airborne infections.

Hospitality properties accounted for 16% of commercial spending, rising 8.2% annually as VRF retrofits enabled guest-level billing and reduced idle-room waste by 40%. Office buildings delivered a 22% share but only a 6.8% CAGR due to hybrid-work patterns, while retail lagged at 12% share and 5.5% growth because landlords shifted HVAC responsibility to tenants via ductless splits. Education facilities rounded out the mix at 11% share, advancing 7.8% annually through the replacement of 30-year-old rooftop units. This segmentation underscores how regulatory and comfort-driven upgrades steer the HVAC equipment market toward higher-margin niches.

Geography Analysis

Asia Pacific held 38.56% of 2025 revenue, anchored by China’s 85 million room-air-conditioner shipments and India’s surge in inverter-AC penetration from 30% in 2023 to 60% in 2025. Southeast Asian high-rises are increasingly adopting VRF systems, while Japanese households are swapping out their aging split systems for low-GWP models. As a result, the region is set to outpace the global average, with a projected growth rate of 8.3% CAGR.

North America delivered 26% of 2025 turnover and 7.9% CAGR, shaped by the Inflation Reduction Act’s tax credits and data-center builds in Virginia, Texas, and Oregon. Europe contributed 22% of revenue, advancing at an 8.6% CAGR, as the boiler ban drives heat-pump retrofits and Scandinavia leads ground-source adoption, with seasonal performance factors above 4.5. The Middle East posted 8% share and an 8.8% CAGR on megaprojects such as Saudi Arabia’s NEOM city and United Arab Emirates data hubs, where 45 °C summers require oversizing and redundancy.

South America added 6% of 2025 volume and 7.5% CAGR, buoyed by Brazil’s residential rebound yet tempered by Argentine volatility, while Africa, starting from a USD 4 billion 2025 base, is forecast to expand at a leading 9.12% CAGR as mining camps adopt solar-hybrid packaged units and urban centers retrofit inverters to curb electricity costs. Together, these dynamics position Asia Pacific as the revenue anchor and Africa as the percentage-growth frontier of the HVAC equipment market.

Competitive Landscape

The five largest vendors, Daikin Industries, Carrier Global, Trane Technologies, Johnson Controls, and Mitsubishi Electric, controlled roughly 42% of 2025 global revenue, yielding a moderately concentrated competitive field. Daikin led with an 11% share and filed 127 inverter- and R32-related patents between 2024 and 2025, aiming to lock in leadership in the refrigerant transition. Carrier vaulted to second place in European heat pumps by acquiring Viessmann Climate Solutions for EUR 12 billion (USD 13.6 billion) in 2025, adding 13,000 employees and 2.8 million-unit annual capacity.

Chinese manufacturers Gree, Midea, and Haier, commanding a dominant 68% share of the domestic residential split market, are now setting their sights on the Middle Eastern and African markets. Leveraging economies of scale, they're managing to price their products 20%-30% lower than their Western counterparts. A testament to this strategy is Midea's 2025 joint venture in Cairo, which has already ramped up shipments to a notable 1.2 million units annually, catering to both North Africa and the Gulf states.

Technology platforms differentiate incumbents: Johnson Controls’ OpenBlue suite integrates HVAC, lighting, and security data to cut whole-building energy by 28%, winning 18 million ft² of contracts in 2025. Gradient Comfort introduced window heat pumps for U.S. rentals, targeting markets where landlords ban wall penetrations, challenging traditional packaged terminal units. Early completion of low-GWP transitions also confers an advantage; Daikin and Mitsubishi Electric captured incremental European share in 2025 while rivals retooled lines. Overall, innovation pace, rather than price alone, now shapes competitive wins in the HVAC equipment market.

HVAC Equipment Industry Leaders

Daikin Industries Ltd.

Carrier Global Corp.

Mitsubishi Electric Corp.

Lennox International Inc.

Midea Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: LG Electronics opened an USD 80 million inverter-compressor R and D center in Seoul to accelerate AI-based diagnostics for VRF systems, with commercial product launches slated for 2027.

- November 2025: Daikin Industries committed JPY 150 billion (USD 1 billion) to a new Polish heat-pump plant capable of 500,000 units annually, targeting post-boiler-ban retrofits.

- October 2025: Carrier Global closed its EUR 12 billion (USD 13.6 billion) acquisition of Viessmann Climate Solutions, boosting European heat-pump capacity to 2.8 million units.

- September 2025: Trane Technologies inaugurated a USD 180 million Bangalore chiller facility producing 4,500 low-GWP units per year for South Asian and Middle Eastern clients.

Global HVAC Equipment Market Report Scope

The HVAC Equipment Market Report is Segmented by Equipment Type (Heating Equipment, Ventilation Equipment, Air-Conditioning Equipment), Installation Type (New Construction, and Retrofit/Replacement), End User (Residential, Commercial, Industrial), Commercial Building Type (Office Buildings, Healthcare Facilities, Hospitality and Leisure, Retail Stores and Malls, Educational Institutions, Data Centers), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

By Equipment Type

| Heating Equipment | Boilers and Furnaces | |

| Heat Pumps | ||

| Unitary Heaters | ||

| Ventilation Equipment | Air Handling Units | |

| Humidifiers and Dehumidifiers | ||

| Air Filters | ||

| Fan Coil Units | ||

| Air-Conditioning Equipment | Unitary Air Conditioners | Ducted Splits |

| Ductless Mini-Splits | ||

| Packaged Rooftops | ||

| Variable Refrigerant Flow (VRF) Systems | ||

| Room Air Conditioners | ||

| Packaged Terminal Air Conditioners | ||

| Chillers | ||

By Installation Type

| New Construction |

| Retrofit / Replacement |

By End User

| Residential |

| Commercial |

| Industrial |

By Commercial Building Type

| Office Buildings |

| Healthcare Facilities |

| Hospitality and Leisure |

| Retail Stores and Malls |

| Educational Institutions |

| Data Centers |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Equipment Type | Heating Equipment | Boilers and Furnaces | |

| Heat Pumps | |||

| Unitary Heaters | |||

| Ventilation Equipment | Air Handling Units | ||

| Humidifiers and Dehumidifiers | |||

| Air Filters | |||

| Fan Coil Units | |||

| Air-Conditioning Equipment | Unitary Air Conditioners | Ducted Splits | |

| Ductless Mini-Splits | |||

| Packaged Rooftops | |||

| Variable Refrigerant Flow (VRF) Systems | |||

| Room Air Conditioners | |||

| Packaged Terminal Air Conditioners | |||

| Chillers | |||

| By Installation Type | New Construction | ||

| Retrofit / Replacement | |||

| By End User | Residential | ||

| Commercial | |||

| Industrial | |||

| By Commercial Building Type | Office Buildings | ||

| Healthcare Facilities | |||

| Hospitality and Leisure | |||

| Retail Stores and Malls | |||

| Educational Institutions | |||

| Data Centers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the HVAC equipment market expected to grow between 2026 and 2031?

The HVAC equipment market is forecast to expand at an 8.11% CAGR from 2026 to 2031, rising from USD 109.33 billion in 2026 to USD 161.46 billion by 2031.

Which equipment type is gaining the most revenue share?

Heating equipment, driven by heat pumps, already commands 58% of heating revenue and outpaces the overall market with an 8.78% CAGR through 2031.

Why are data centers a strategic segment for HVAC suppliers?

Precision-cooling gear achieves 35%-40% gross margins and is advancing at an 8.74% CAGR because AI-driven rack densities require liquid-cooling architectures.

How do European policies affect HVAC demand?

The Energy Performance of Buildings Directive bans new fossil-fuel boilers from 2025 and mandates deep retrofits of the worst 16% of buildings by 2030, generating a sustained heat-pump replacement cycle.

What limits the pace of HVAC installations in the United States?

A technician shortage that could reach 50,000 workers by 2030 has already created a 15% backlog of sold-but-not-installed units, delaying full realization of policy-driven demand.

Which region is poised for the highest percentage growth?

Africa is forecast to lead percentage growth, expanding at a 9.12% CAGR as solar-hybrid packaged units and inverter retrofits gain traction in mining and urban markets.

Page last updated on: