Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 9.60 Billion |

| Market Size (2030) | USD 12.88 Billion |

| Growth Rate (2025 - 2030) | 6.05% CAGR |

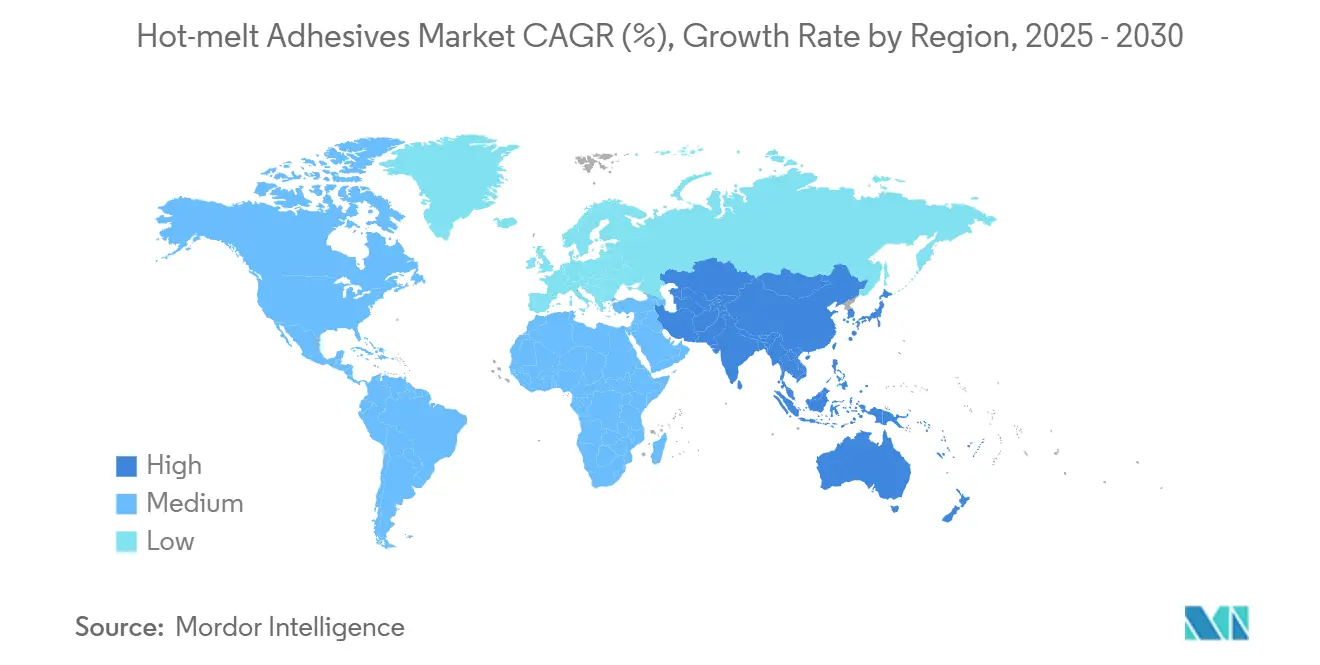

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

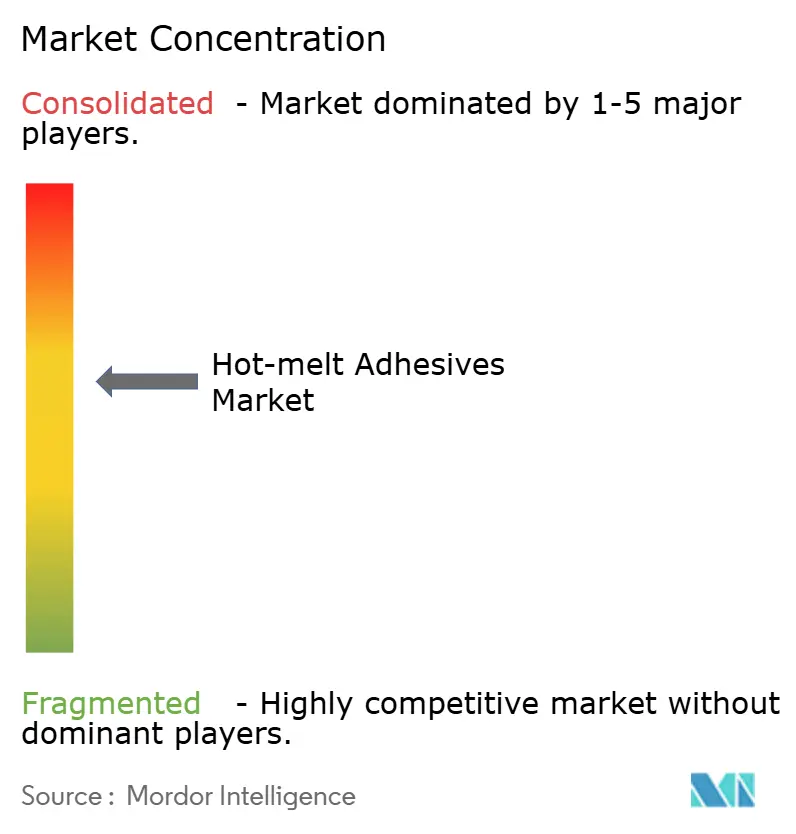

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hot-melt Adhesives Market Analysis by Mordor Intelligence

The Hot-melt Adhesives Market size is estimated at USD 9.60 billion in 2025, and is expected to reach USD 12.88 billion by 2030, at a CAGR of 6.05% during the forecast period (2025-2030). The expansion is propelled by the migration from solvent-borne chemistries to thermoplastic systems that eliminate volatile organic compounds, speed up packaging lines, and cut energy use. Fast-moving consumer goods companies rely on millisecond-precision dispensing equipment that supports case-sealing, label‐stock bonding, and flexible-film lamination without drying ovens. E-commerce in Asia continues to drive corrugated packaging volumes, while healthcare device makers adopt solvent-free bonding to satisfy sterilization and biocompatibility rules. Supply-side strategies emphasize vertical integration into polymer and tackifier production as insulation against crude-oil swings, and innovators are rolling out bio-based resins that command 15-20% price premiums in sustainability-focused niches.

Key Report Takeaways

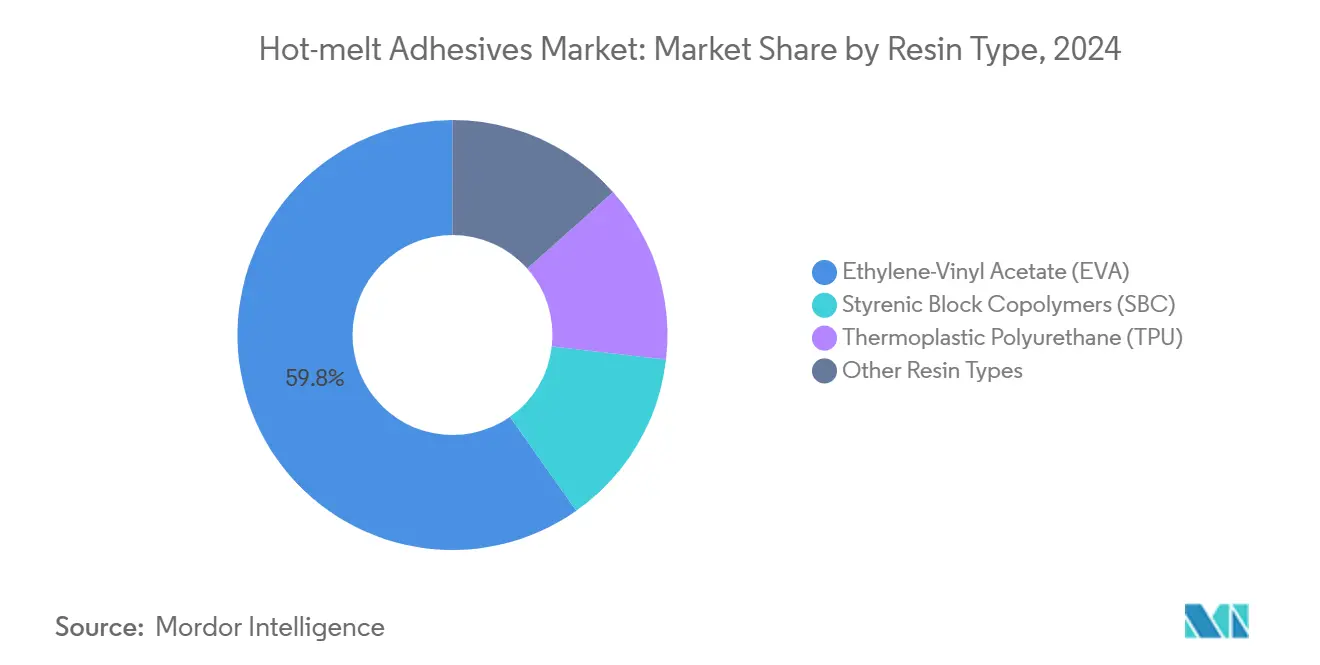

- By resin type, Ethylene-Vinyl Acetate maintained 59.76% of the market in 2024, and its 6.57% CAGR through 2030 is the fastest among major polymers.

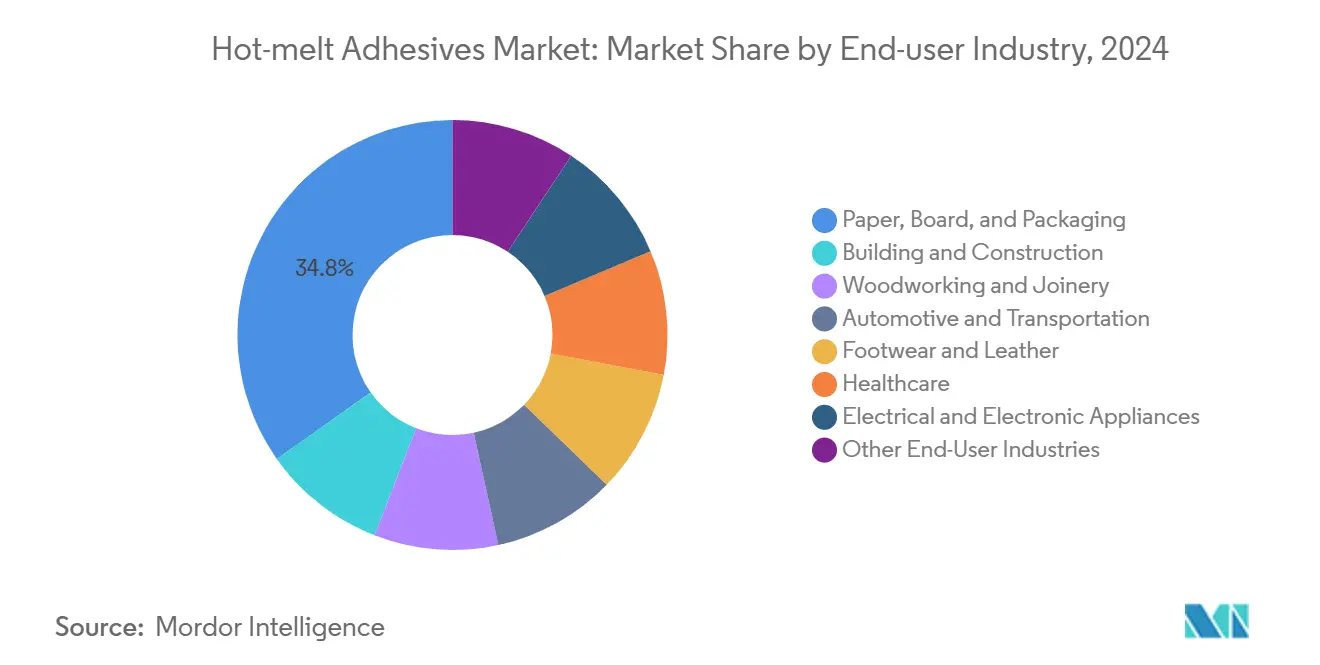

- By end-user industry, paper, board, and packaging led with 34.78% revenue share in 2024; healthcare is projected to record the highest CAGR at 6.23% through 2030.

- By geography, Asia-Pacific held 48.57% of the hot melt adhesives market share in 2024, while it is also forecast to expand at a 6.85% CAGR to 2030.

Global Hot-melt Adhesives Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift From Solvent-Borne to Hot-Melt Systems in Fast-Moving Packaging Lines | +1.8% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Explosive Growth of Asian E-Commerce Fulfilment Hubs Demanding Eco-Friendly Case-Sealing Adhesives | +1.5% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Surge in Bio-Based Resin Capacity (Soy, Tall-Oil, Starch) Unlocking New Premium Niches | +1.2% | North America and EU leading, APAC following | Long term (≥ 4 years) |

| Automation of Furniture and Mattress Production Driving PUR And MPO Hot-Melts | +0.9% | Global, concentrated in manufacturing hubs | Medium term (2-4 years) |

| EV Lightweighting and Battery Module Bonding Requirements | +1.0% | Global, with China and EU leading EV adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift from Solvent-Borne to Hot-Melt Systems in Fast-Moving Packaging Lines

Production lines have cut cycle times by 40-60% by eliminating solvent flash-off and adopting melt-on-demand units that keep viscosity stable for entire shifts. Robatech’s Volta platform trims energy draw by 30% while meeting REACH and FDA food-contact rules, making it a template for upgrades across beverage multipack and snack pouch plants.

Explosive Growth of Asian E-Commerce Fulfilment Hubs Demanding Eco-Friendly Case-Sealing Adhesives

China processed more than 130 billion parcels in 2024, and fulfilment centers specify starch-based hot melts that compost within 180 days, curbing landfill loads. India and ASEAN follow, pushing corrugators to install high-speed gluers compatible with low-temperature bio-formulations that prevent board warping in humid climates.

Surge in Bio-Based Resin Capacity (Soy, Tall-Oil, Starch) Unlocking New Premium Niches

H.B. Fuller’s investments in renewable raw materials cut cradle-to-gate CO₂ by up to 40%. Soy-based polyols widen service temperature windows, and tall-oil tackifiers leverage pulp-mill by-products to lower fossil exposure, positioning suppliers for price‐premium contracts in personal-care wipes and infant-nutrition closures[1]H.B. Fuller, “Sustainability Report 2024,” hbfuller.com .

Automation of Furniture and Mattress Production Driving PUR and MPO Hot-Melts

SCM Group’s edgebanders deliver 20 m min⁻¹ feed rates with precise PUR bead control, enabling seamless joins on radius panels. Mattress lines adopt flame-retardant MPOs that retain elasticity after repeated compression tests, reducing polyurethane foam scrap rates in lean factories.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-Oil-Linked Price Volatility of Tackifier Resins | -1.1% | Global, with emerging markets most affected | Short term (≤ 2 years) |

| Limited Heat-Resistance Window Versus Structural Epoxies | -0.8% | Global, concentrated in automotive and aerospace | Medium term (2-4 years) |

| Growing VOC Scrutiny on Traditional SBC Tackifiers In EU | -0.6% | EU primary, with regulatory spillover to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil-Linked Price Volatility of Tackifier Resins

C5 and C9 hydrocarbon tackifiers make up 15-25% of conventional formulations and saw 30-40% price swings during 2024 energy shocks. Large buyers secure multi-year supply contracts; smaller converters absorb margin squeeze or reduce adhesive load rates, risking bond failure in humid transit environments.

Limited Heat-Resistance Window Versus Structural Epoxies

Under-hood parts must survive up to 150 °C, yet EVA softens near 85 °C, restricting adoption for engine components. High-temperature polyamides exist but cost three to five times more, so they remain confined to aerospace cabin interiors and premium electronics that can absorb the price delta.

Segment Analysis

By Resin Type: EVA Dominance Drives Market Stability

EVA accounted for 59.76% of the hot melt adhesives market size in 2024 and is forecast to compound at 6.57% annually to 2030. Its balance of flexibility, adhesion, and cost keeps converters loyal, and decades of installed slot-die and spray equipment dampen switching incentives. The segment also benefits from a deep feedstock base in Asia and North America that cushions against isolated supply shocks.

Heightened sustainability goals push buyers toward metallocene polyolefins with 65% renewable content, such as Dow’s AFFINITY RE, which cuts carbon footprint by 40-50% while matching bond strength. Thermoplastic polyurethane captures share in footwear, offering abrasion resistance that withstands 100,000 flex cycles. Specialty polyamides and polyimides cater to electronics potting, leveraging high-temperature stability that EVA and SBC cannot match, but volumes remain niche due to price premiums.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Packaging Leadership Amid Healthcare Acceleration

Paper, board, and packaging consumed 34.78% of 2024 volume thanks to surge orders from e-commerce and beverage multipacks. Automation favors bead and swirl patterns that create tear-fibrous failure modes in corrugated case-sealing, boosting tamper evidence. Multi-substrate compatibility reduces SKUs for contract packers handling coated board, foil-lined pouches, and filmic overwraps in the same plant.

Healthcare is the fastest expander at 6.23% CAGR to 2030. Device makers require USP Class VI and ethylene-oxide sterilization resistance, which reactive hot melts fulfill without plasticizers. Pharmaceutical blister packs adopt low-application-temperature grades that avoid heat deformation of thin-gauge aluminum. Elsewhere, automotive harness wrapping, footwear toe-puff bonding, and electronics wire management all choose hot melts for weight savings and recyclability, underpinning a diverse demand base.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific’s 48.57% dominance in 2024 stems from integrated supply corridors linking polymer crackers, tackifier reactors, and high-volume corrugators. Chinese converters sit adjacent to cell phone and appliance plants, ensuring just-in-time adhesive deliveries that minimize heated-tank idle time. India’s consumer-goods boom lifts demand for all-temperature carton sealing, and Southeast Asia benefits from printed-circuit board migration that needs precision jetting.

North American buyers prioritize premium performance and sustainability. U.S. automakers specify reactive polyolefins that permit end-of-life dismantling, while Canadian forestry residuals feed tall-oil tackifier streams that lower fossil intensity. Mexico’s maquiladoras amplify regional volumes with appliance assembly lines that require thermal-shock-resistant bonds.

Europe’s stringent VOC caps accelerate substitution of solvented laminating adhesives with melt-based grades. German vehicle makers co-develop lightweight cockpit modules using PUR that passes crash pulse tests[2]German Federal Motor Transport Authority, “Vehicle Safety Standards,” kba.de . The United Kingdom focuses on compostable bag seals to meet municipal waste targets, and Nordic players leverage bio-refineries to supply renewable waxes that trim CO₂ footprints. South America and MEA trail but invest in infrastructure insulation and consumer goods packaging, though currency volatility periodically tempers import demand.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Henkel, 3M, and H.B. Fuller together held around 38% of revenue in 2024, indicating moderate concentration. Leaders integrate backward into ethylene and rosin feedstocks to buffer crude swings and command margin. Product pipelines highlight bio-content credentials and digital services: Henkel’s IoT dispensers alert operators before char forms; 3M promotes low-fogging interior trim adhesives for EV cabins; H.B. Fuller markets renewable-label adhesives that enable PET bottle recycling streams.

Mid-tier firms such as Bostik and Jowat focus on furniture, hygiene, and tapes, differentiating through application equipment partnerships that bundle consumables with maintenance plans. Start-ups target reversible bonding chemistries triggered by heat or microwave fields, aiming to unlock circular-economy dismantling. Barriers to entry include FDA 21 CFR compliance, REACH dossier costs, and the need for global technical-service footprints. Buyers favor suppliers that can validate line trials, deliver rapid color-match, and guarantee batch-to-batch rheology.

Hot-melt Adhesives Industry Leaders

-

3M

-

Arkema

-

Henkel AG & Co. KGaA

-

H.B. Fuller Company

-

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Henkel introduced Technomelt EM 335 RE, a hot melt adhesive enabling clean separation of labels from PET bottles. The adhesive bonds 40,000 bottle labels hourly at 110-140°C, protecting equipment and enhancing operational reliability while reducing energy consumption.

- February 2025: Power Adhesives Ltd. introduced Tecbond 110B-PR, a biodegradable bulk adhesive for high-speed case sealing and carton closing in EOL operations. The low-viscosity adhesive operates through narrow nozzles at reduced temperatures, creating strong bonds on carton materials while minimizing energy usage.

Global Hot-melt Adhesives Market Report Scope

Hot-melt adhesives are generally composed of 100% solid components. The hot melts are sold in a solid state at room temperature and are activated by heating beyond their softening point, which is usually between 50 and 160 degrees. After melting, an adhesive may be applied to the substrate in a liquid state. The hot melt coats the substrate, penetrating the surface, and then solidifies to ensure uniformness. It takes very little time for this setting and cooling process.

The hot-melt adhesives market is segmented by resin type, end-user industry, and geography. By resin type, the market is segmented into ethylene vinyl acetate, styrene-butadiene copolymers, thermoplastic polyurethane, and other resin types (polyolefin, polyamide). Based on the end-user industry, the market is segmented into building and construction, paper, board, and packaging, woodworking and joinery, transportation, footwear and leather, healthcare, electrical and electronic appliances, and other end-user industries. The report also covers the market sizes and forecasts for the hot-melt adhesives market in 27 countries across major regions. The market sizing and forecasts were made for each segment based on value (USD).

By Resin Type

| Ethylene-Vinyl Acetate (EVA) |

| Styrenic Block Copolymers (SBC) |

| Thermoplastic Polyurethane (TPU) |

| Other Resin Types |

By End-user Industry

| Paper, Board, and Packaging |

| Building and Construction |

| Woodworking and Joinery |

| Automotive and Transportation |

| Footwear and Leather |

| Healthcare |

| Electrical and Electronic Appliances |

| Other End-User Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Resin Type | Ethylene-Vinyl Acetate (EVA) | |

| Styrenic Block Copolymers (SBC) | ||

| Thermoplastic Polyurethane (TPU) | ||

| Other Resin Types | ||

| By End-user Industry | Paper, Board, and Packaging | |

| Building and Construction | ||

| Woodworking and Joinery | ||

| Automotive and Transportation | ||

| Footwear and Leather | ||

| Healthcare | ||

| Electrical and Electronic Appliances | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is current size of hot melt adhesives market?

It is estimated at USD 9.60 billion in 2025 and projected to reach USD 12.88 billion, reflecting a 6.05% CAGR from 2025.

Which resin dominates current demand?

EVA accounts for 59.76% of global volume, sustaining its lead with a 6.57% forecast CAGR.

Why is Asia-Pacific the largest regional consumer?

The region hosts integrated polymer supply chains and high parcel volumes that require automated case-sealing.

What end-use industry is growing the fastest?

Healthcare industry is expanding at a 6.23% CAGR due to device assembly and pharmaceutical packaging needs.

Page last updated on: