Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 51.23 Billion |

| Market Size (2030) | USD 61.21 Billion |

| Growth Rate (2025 - 2030) | 3.62% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Hospitality Real Estate Market Analysis by Mordor Intelligence

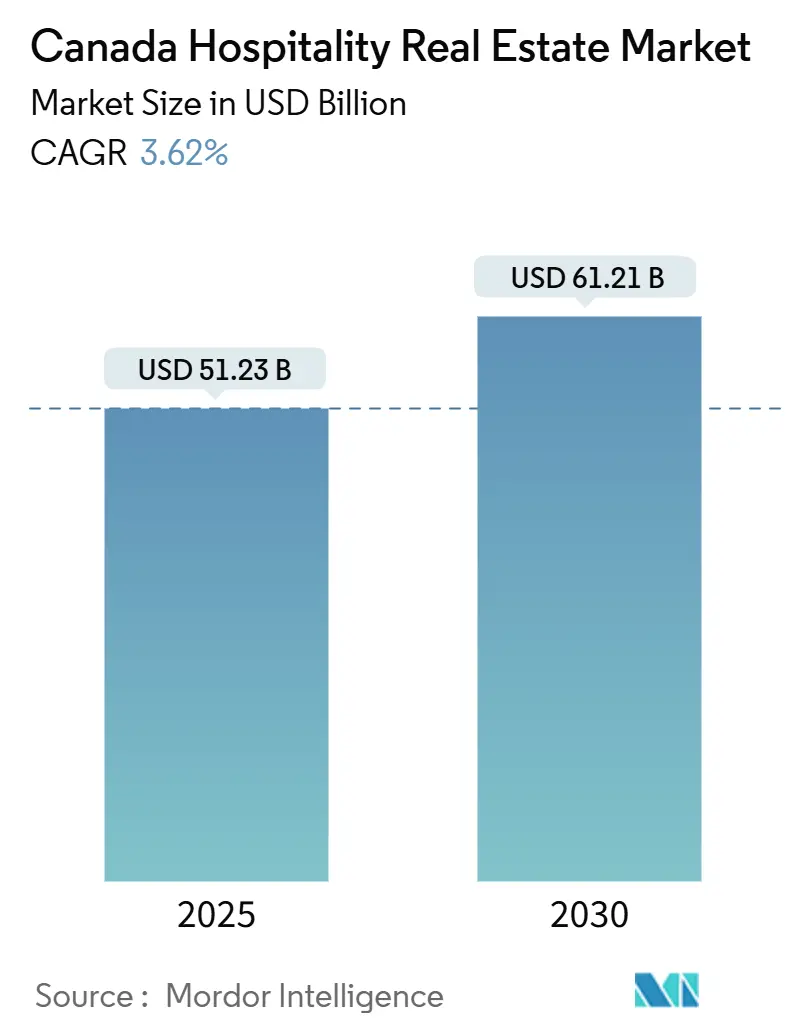

The Canada Hospitality Real Estate Market size is estimated at USD 51.23 billion in 2025, and is expected to reach USD 61.21 billion by 2030, at a CAGR of 3.62% during the forecast period (2025-2030). Leisure-driven domestic demand, the rebound of inbound tourism, and price-resilient average daily rates (ADR) in supply-constrained metros are sustaining revenue momentum. Gateway cities—Toronto, Vancouver, and Montreal—benefit from restored air capacity and a weaker Canadian dollar that boosts cross-border spending, while secondary markets capture extended-stay and corporate-relocation demand. Tight credit and elevated construction costs temper ground-up development, but adaptive-reuse projects and ESG retrofits provide alternative growth corridors. Global chains double down on focused-service and extended-stay roll-outs, whereas well-capitalized independents use soft-brand affiliations to scale distribution.

Key Report Takeaways

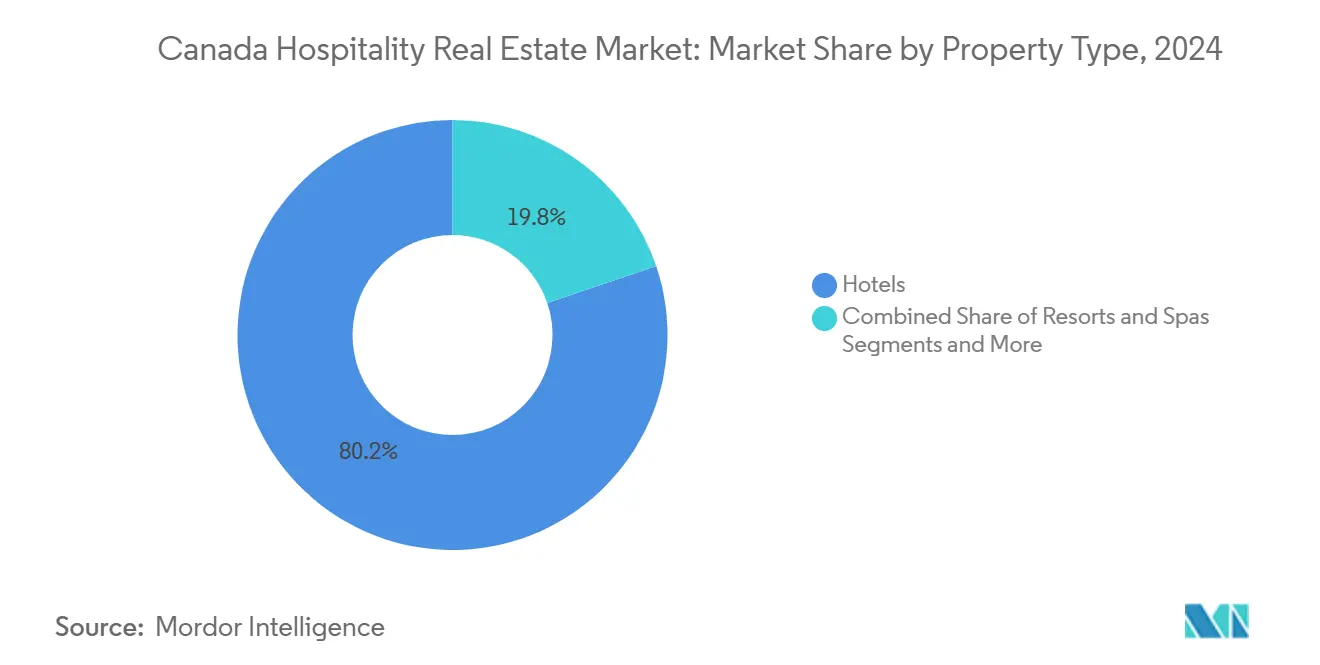

- By property type, hotels held 80.2% of 2024 revenue, while resorts & spas are growing at a 4.12% CAGR through 2030.

- By type, chain hotels accounted for 62.8% of the 2024 Canada hospitality real estate market share; independent hotels post the fastest forecast CAGR at 4.51%.

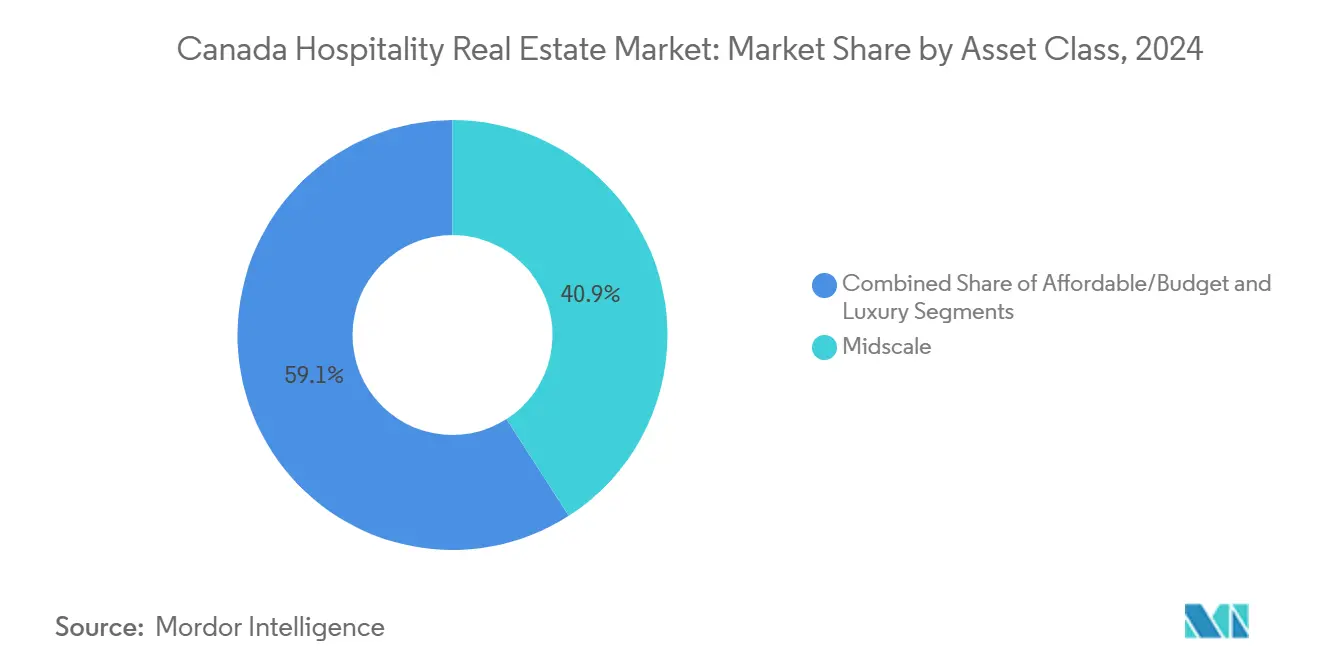

- By asset class, midscale captured 40.9% of 2024 revenue; luxury is projected to expand at a 4.81% CAGR to 2030.

- By geography, Ontario controlled 30.8% of 2024 revenue, whereas British Columbia is set to deliver the quickest 5.09% CAGR through 2030.

Canada Hospitality Real Estate Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Population growth and tourism recovery | +1.2% | Ontario, British Columbia, Quebec | Medium term (2–4 years) |

| Weak CAD, events travel, restored air routes | +0.9% | Border provinces and gateway cities | Short term (≤ 2 years) |

| Extended-stay and select-service resilience | +0.7% | Calgary, Edmonton, Toronto, Vancouver | Medium term (2–4 years) |

| Urban office-to-hotel conversions | +0.5% | Toronto, Vancouver, Montreal, Calgary | Long term (≥ 4 years) |

| ESG retrofits unlock green financing | +0.3% | Ontario and British Columbia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Population Growth and Tourism Recovery Lifting Occupancy and ADR

Immigration added a record 1.3 million residents in 2024, and domestic overnight trips reached 105.6 million, up 8.8% year-over-year, directly supporting hotel demand[1]Statistics Canada, “National Travel Survey, second quarter 2024,” statcan.gc.ca. Accommodation revenue already sat 9.6% above 2019 by 2022, and Q4 2024 lodging consumption advanced 2.6% quarter-over-quarter. Although international arrivals remain 12% below 2019, ongoing visa-processing gains suggest more upside. Average daily rates climbed 2.9% in Q1 2025 despite a marginal occupancy dip, underscoring pricing power in capacity-tight metros. New event infrastructure, such as Calgary’s expanded BMO Centre, layers incremental group demand for nearby rooms.

U.S. and International Demand Buoyed by Weaker CAD and Air Capacity Rebuild

The CAD traded between 1.35 and 1.44 per USD through 2024–2025, making Canada cost-competitive for Americans and long-haul visitors. U.S. travelers logged 23.5 million trips in 2024, and international air capacity exceeded 2019 levels in four straight quarters. Europe and Asia arrivals each rose more than 8% year-over-year in August 2024, cushioning a slide in Canadian outbound travel. Leisure and event-driven trips, including high-profile concerts and sports tournaments, funneled spend into hotels across Toronto, Vancouver, and Ottawa. That inbound tailwind directly lifts urban RevPAR, given the concentration of international visitors in gateway markets.

Extended-Stay, Select-Service, and Limited-Service Formats Showing Resilient Margins

Focused-service brands accounted for half of Hilton’s Canadian openings in the past decade, while its extended-stay keys doubled, signaling franchisee preference for lean-staff models. Cap-rate evidence aligns: select-service assets transacted at 6.0–9.5% yields, yet reached breakeven faster than full-service counterparts. Staffing efficiencies matter when accommodation-sector weekly pay trails the national norm by nearly 50%, and vacancies still hover above 4%. Home-like amenities and lower food-and-beverage overheads keep margins firm even during demand wobble. Pipeline data—20-plus openings slated in the next year—points to durable developer appetite.

Urban Repositioning—Office/Retail Conversions and Mixed-Use Projects—Expanding Supply

Persistently high downtown office vacancies coax owners toward hotel or aparthotel conversions. Quebec City’s Îlot Dorchester, a 150-room hotel within a 17-story mixed-use tower, and Vancouver’s 464-unit Granville Street hotel exemplify this reuse path. Adaptive projects leverage existing utility and transit lines, shortening pre-development phases relative to greenfields. Heritage retrofits also align with municipal carbon targets; the Fairmont Royal York’s deep-carbon overhaul cut emissions 80% and unlocked USD 46.5 million of low-rate debt via Canada Infrastructure Bank. Nonetheless, approvals often stretch 18–36 months, lengthening carry periods and pressuring developer returns.

Restraints Impact Analysis

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High financing costs and tighter underwriting | -0.8% | Toronto and Vancouver debt-sensitive projects | Short term (≤ 2 years) |

| Construction inflation and permitting delays | -0.6% | British Columbia and Ontario | Medium term (2–4 years) |

| Acute labor shortages and rising wages | -0.4% | Alberta and British Columbia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Financing Costs and Tighter Underwriting Slowing Transactions

The overnight rate eased to 2.25% by December 2025, yet five- and ten-year yields remain 100 basis points above pre-2022 norms, sustaining higher debt-service burdens. OSFI’s November 2024 notice tightened provisioning rules, compelling lenders to demand more equity and stronger sponsor track records. Morguard’s sale of 14 hotels for USD 410 million typifies landlords reallocating capital to less-risky sectors. Development leverage has fallen, often capping at 55% loan-to-cost, slowing ground-up starts. This tighter capital climate drags on the Canada hospitality real estate market expansion pace despite healthy demand fundamentals.

Construction Inflation, Supply-Chain Delays, and Permitting Complexity Elevating Capex and Timelines

Building-cost indices continued to rise through 2024 as material tariffs and wage escalation fed into bids. Municipal approvals in Vancouver or Toronto frequently exceed two years, layering soft-cost inflation on stalled projects. Contractors price supply-chain risk premiums into hotel scopes because mechanical systems often depend on imported components. These hurdles raise per-key costs and push project IRRs below hurdle rates unless ADR forecasts are reset higher. Consequently, some developers pivot to converting existing buildings to sidestep both expense and red-tape drag.

Segment Analysis

By Property Type: Hotels Anchor Revenue, Resorts Capture Wellness Demand

Hotels captured 80.2% of 2024 revenue in the Canada hospitality real estate market, reflecting their extensive footprint in every major urban corridor. Revenue comes from a balanced corporate, leisure, and group mix, enabling chains to spread fixed costs across high-occupancy seasons. Branded operators continue to refurbish lobbies into co-working lounges, monetizing non-room square footage and increasing ancillary spend. Resorts & spas, although representing a smaller base, are forecast to expand at a 4.12% CAGR through 2030, outstripping the broader Canada hospitality real estate market as wellness tourism gains mainstream traction.

Investor interest pivots toward experience-rich properties such as Therme Canada’s Ontario Place redevelopment, which layers water-park, botanical, and thermal attractions under one roof. Legacy icons like Fairmont Chateau Lake Louise add eco-friendly thermal facilities to secure year-round occupancy premiums. Tight land availability near national parks and lakes protects ADR, while brands pursue asset-light management agreements to cap downside. Overall, hotels will keep dominating transaction volume, yet resorts are tipped to deliver higher RevPAR growth as affluent travelers prioritize holistic wellness experiences.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Type: Chains Leverage Scale, Independents Gain Through Soft Brands

Chain hotels controlled 62.8% of 2024 rooms, a figure backed by powerful loyalty ecosystems and procurement savings that widen EBITDA margins. Their pipeline favors focused-service and lifestyle concepts that require smaller banquet and kitchen footprints yet drive comparable RevPAR. Independents, aided by soft-brand affiliations, are on track for a 4.51% CAGR, the quickest growth rate in this segmentation. Ascend Hotel Collection and Tapestry Collection extend CRS and loyalty reach to boutique owners that retain design autonomy.

Domestic operator Germain Hotels illustrates the strength of the hybrid model after securing USD 118 million to expand its Alt and Le Germain banners. Franchise structures attract newcomers by offering standardized operating manuals, but rising fee loads motivate some owners to renegotiate or switch to emerging white-label managers. Over 2025-2030, the Canada hospitality real estate market size tied to independents will expand as digital marketing lowers distribution barriers, while chains maintain dominance through scale and brand equity.

By Asset Class: Midscale Dominates Volume, Luxury Commands Premium Growth

Midscale captured 40.9% of 2024 revenue in the Canada hospitality real estate market, leveraging highway, airport, and suburban demand nodes[2]Cushman & Wakefield, “Hospitality Insights Q1 2025,” cushmanwakefield.com. These properties operate lean, with automated breakfast service and reduced banquet space, keeping fixed costs low. Loyalty points and consistent mattress standards continue to resonate with cost-conscious travelers and small corporate accounts.

Luxury, projected to grow at a 4.81% CAGR, outperforms as high-net-worth travelers seek personalized, experience-centric stays. Hilton’s lifestyle push—Curio, Canopy, and forthcoming Tempo in Toronto—illustrates the chain's ambitions to capture boutique-luxury wallet share. Capital follows: downtown conversions of heritage buildings into five-star hotels often achieve cap-rate compression to near-6%, reflecting investors’ confidence in rate resilience. Midscale will remain the market’s volume backbone, yet luxury assets will disproportionately drive incremental RevPAR and attract trophy-seeking capital.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Ontario generated 30.8% of 2024 revenue, anchored by Toronto’s convention demand, Ottawa’s government traffic, and Niagara Falls’ leisure inflows. British Columbia leads growth with a 5.09% CAGR forecast, fueled by Vancouver’s restored Asia-Pacific lift and Victoria’s resort pull. Quebec holds a strong cultural tourism base; Montreal’s festival calendar shores up summer occupancy, while Quebec City benefits from heritage travel and government business. Alberta, still linked to energy-sector cycles, leverages the new BMO Centre to diversify group bookings, though Calgary’s RevPAR slipped in early 2025 before stabilizing as commodity prices rebounded.

Saskatchewan and Atlantic provinces show volatile RevPAR swings tied to event clusters and contract demand. Manitoba’s 13% RevPAR decline in Q1 2025 illustrates that one-off government housing contracts can skew comps. Conversely, Saskatchewan’s 8% rise underscores the upside when provincial events align with limited room supply. Northern territories remain niche, servicing resource projects and adventure tourism, but limited pipeline pockets keep ADR firm. Across regions, rising air capacity, especially at Vancouver International and Toronto Pearson, concentrates international guest nights in gateway metros, whereas highway-fed areas rely on domestic leisure drive trips.

ESG mandates also vary geographically: British Columbia and Ontario municipalities offer tax incentives for electrification, leading to a higher share of certified green hotels in these provinces. Meanwhile, Alberta’s abundant natural gas pushes some operators toward co-generation solutions. Provincial tourism agencies increasingly coordinate with Indigenous communities, as shown by the First Nations’ majority stake in Hilton Québec, to ensure equitable development and cultural authenticity[3]Gowling WLG, “Four First Nations and InnVest REIT finalize Hilton Québec acquisition,” gowlingwlg.com. These regional nuances shape capital allocation and brand rollout strategies in the Canada hospitality real estate market.

Competitive Landscape

Global chains control roughly 60–65% of branded keys, giving them procurement clout and loyalty capture that underpin stable occupancy. Hilton surpassed 200 open hotels in September 2025 and has more than 100 projects in the pipeline, with emphasis on focused-service and lifestyle banners. Marriott, IHG, Hyatt, and Choice pursue similar multi-brand layering to fill white spaces across price points and trip purposes.

Domestic contenders compete through agility and localized design. Germain Hotels’ coast-to-coast push, financed with USD 118 million of long-dated capital, demonstrates how a strong regional brand can secure prime urban sites. Sunray Group’s acquisition of the historic Walper Hotel for USD 13.7 million signals an independent appetite for heritage assets in tech-hub markets. Indigenous investment vehicles enter marquee properties, aligning economic returns with community development mandates.

Institutional capital treats hospitality as a tactical allocation. Brookfield monetized USD 40 billion of real estate in 2024, including hotel exits, to recycle into higher-yielding bets. Morguard’s USD 410 million divestiture and InnVest REIT’s continued acquisitions illustrate portfolio re-balancing along risk-adjusted lines. Technology adoption—revenue-management AI, mobile key, and guest analytics—emerges as a decisive edge. ESG credentials, now considered in RFPs by Fortune 500 meeting planners, further differentiate winners in the Canada hospitality real estate market.

Canada Hospitality Real Estate Industry Leaders

-

Brookfield Asset Management

-

InnVest Hotels

-

Westmont Hospitality Group

-

Superior Lodging Corp

-

Coast Hotels

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Hilton exceeded 200 open hotels in Canada, with more than 100 in development focusing on focused-service, extended-stay, and lifestyle brands.

- May 2025: Germain Hotels secured USD 118 million to speed up national expansion and merge operating entities.

- January 2025: First Nations investors partnered with InnVest REIT to acquire Hilton Québec, marking a milestone for Indigenous economic advancement.

- June 2024: Calgary’s USD 500 million BMO Centre expansion opened, adding 565,000 sq ft of exhibit and meeting space.

Canada Hospitality Real Estate Market Report Scope

A complete background analysis of the hospitality real estate sector in Canada, which includes an assessment of the industry associations, overall economy, and emerging market trends by segments, significant changes in the market dynamics, and market overview is covered in the report.

By Property Type

| Hotels |

| Resorts & Spas |

| Others (Serviced Apartments, Boutique Inns, etc.) |

By Type

| Chain Hotels |

| Independent Hotels |

By Asset Class

| Affordable / Budget |

| Midscale |

| Luxury |

By Province

| Ontario |

| Quebec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Property Type | Hotels |

| Resorts & Spas | |

| Others (Serviced Apartments, Boutique Inns, etc.) | |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Asset Class | Affordable / Budget |

| Midscale | |

| Luxury | |

| By Province | Ontario |

| Quebec | |

| British Columbia | |

| Alberta | |

| Rest of Canada |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the expected value of the Canada hospitality real estate market by 2030?

The market is projected to reach USD 61.21 billion by 2030, reflecting a 3.62% CAGR over 2025–2030.

Which province is forecast to grow fastest in Canadian hospitality real estate?

British Columbia leads with a 5.09% CAGR through 2030, buoyed by Vancouver’s international air lift and Victoria’s resort appeal.

Why are extended-stay and select-service hotels attractive to investors?

They ramp occupancy faster, run with leaner staffing, and traded at competitive 6.0–9.5% cap rates in early 2025.

How are ESG retrofits influencing hotel returns?

Deep-carbon projects like the Fairmont Royal York cut energy costs by more than 35% and unlock preferential green financing, boosting NOI.

What financing hurdles confront new hotel development in Canada?

Higher policy rates, stricter OSFI underwriting, and lower leverage availability have slowed ground-up starts despite healthy demand fundamentals.

Which segment shows the fastest revenue growth within asset classes?

Luxury hotels, projected to expand at a 4.81% CAGR through 2030, driven by high-net-worth traveler demand and heritage-building conversions.

Page last updated on: