Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

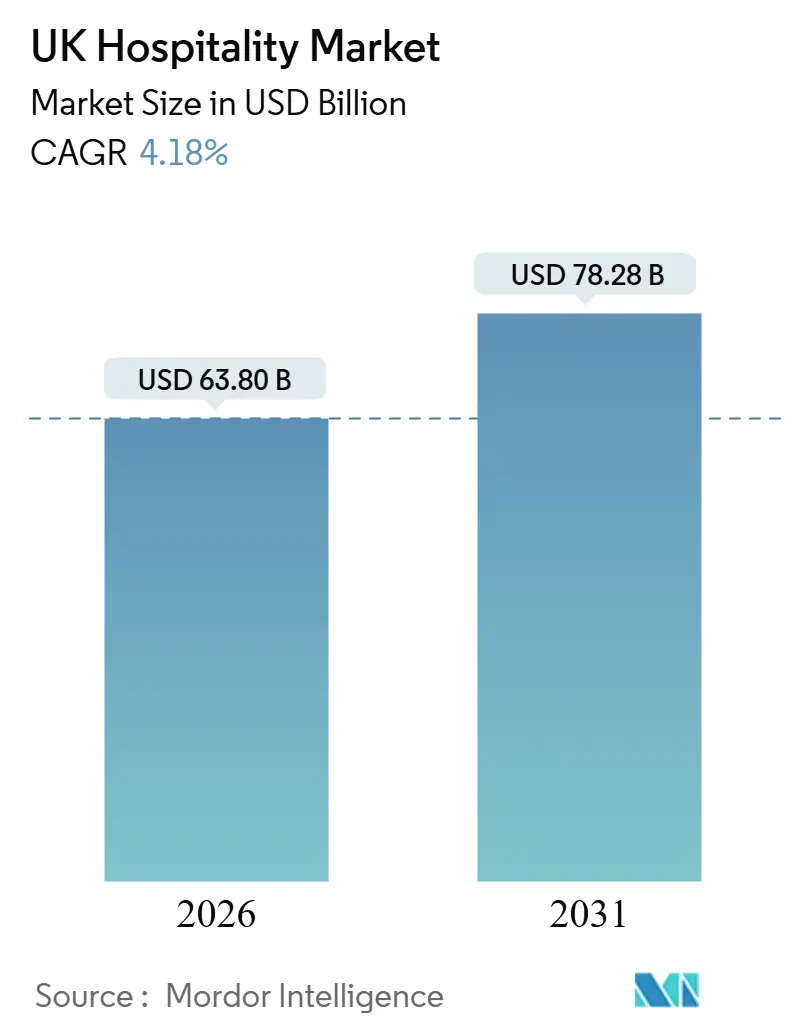

| Market Size (2026) | USD 63.80 Billion |

| Market Size (2031) | USD 78.28 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Hospitality Market Analysis by Mordor Intelligence

The United Kingdom hospitality market is valued at USD 63.80 billion in 2026 and is projected to reach USD 78.28 billion by 2031, reflecting a 4.18% CAGR. The United Kingdom hospitality market is growing steadily, providing a stable foundation for planning and investment, but uneven economic conditions and below pre-pandemic activity levels continue to slow demand recovery and limit pricing flexibility. Domestic travel demand has shown resilience, supported by strong growth in day visits and higher overall domestic spending. At the same time, a decline in overnight trips indicates a shift toward shorter stays and more localized spending patterns, shaping revenue mix and operational strategies for hospitality operators. Inbound tourism is expected to improve, with international visitor volumes and spending rising, although real-term expenditures remain below pre-pandemic benchmarks. This gap highlights continued price sensitivity among international travelers and its downstream effects on occupancy rates, average daily rates, and service positioning within the United Kingdom hospitality market[1]Source: UK Finance, “UK Payments Markets Summary 2025,” ukfinance.org.uk . Competitive dynamics within the market remain increasingly polarized. Large-scale operators are leveraging pricing power, brand visibility, and digital distribution to protect margins, while independent operators continue to face elevated cost pressures and limited access to capital. This divergence is accelerating consolidation activity and reshaping competitive structures, influencing near-term performance trends and long-term market configuration within the United Kingdom hospitality sector.

Key Report Takeaways

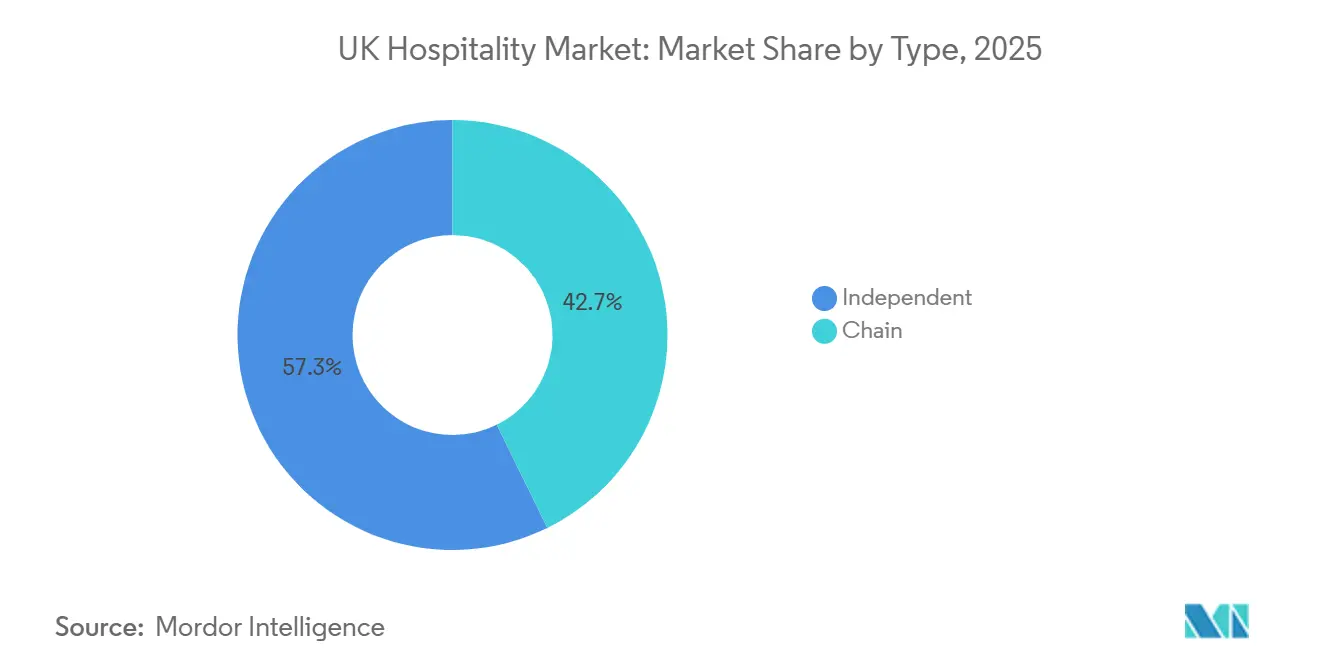

- By type, Independent Hotels held 57.28% of the United Kingdom hospitality market share in 2025, while Chain Hotels are forecast to expand at a 7.88% CAGR from 2026 to 2031.

- By accommodation class, Mid & Upper-Midscale Hotels accounted for 39.38% of the United Kingdom hospitality market share in 2025, while Luxury accommodations are expected to grow at a 7.98% CAGR through 2031.

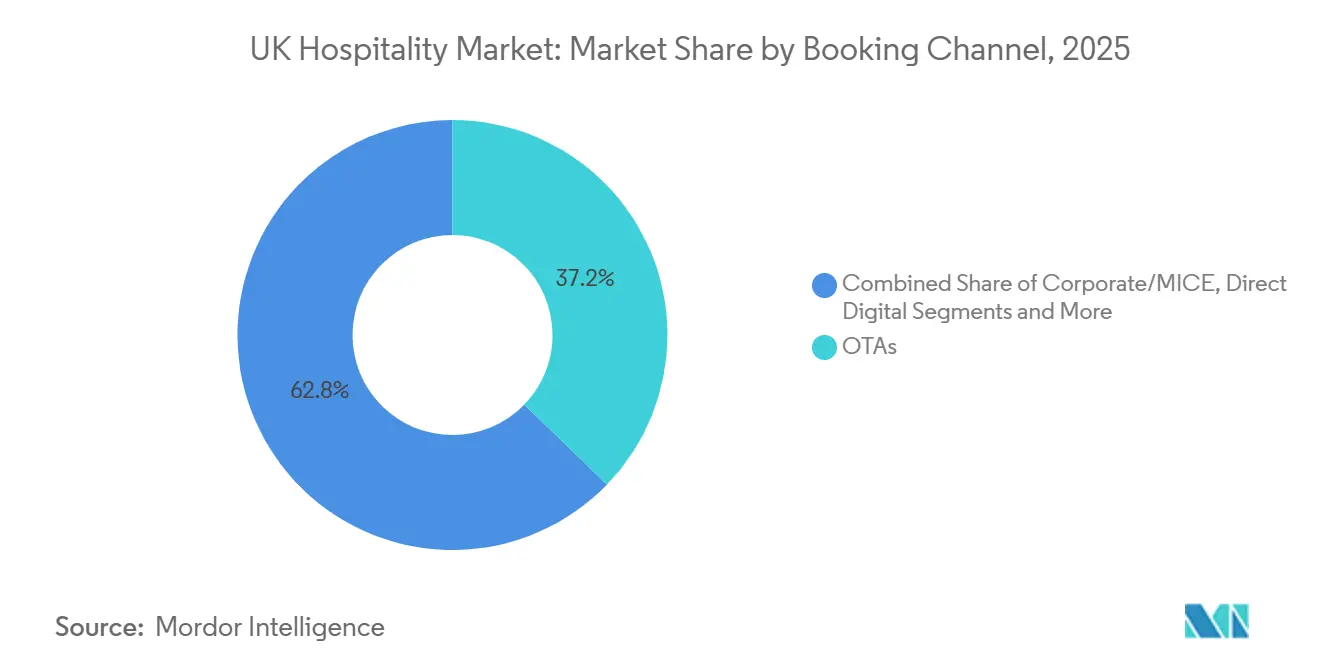

- By booking channel, OTAs captured a 37.24% of the United Kingdom hospitality market share in 2025, while Direct Digital channels are forecast to grow at a 7.34% CAGR through 2031.

- By geography, England led with 71.28% of the United Kingdom hospitality market share in 2025, while Northern Ireland is projected to record the fastest growth at an 8.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Hospitality Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Digital Ordering & Booking | +1.2% | Global, with the United Kingdom leading adoption at a 94.6% contactless transaction rate | Medium term (2-4 years) |

| Government VAT Relief and Incentive Programs | +0.6% | National, concentrated in high street retail/hospitality | Short term (≤ 2 years) |

| Increased Inbound Tourism Supported by a Weaker Currency | +0.9% | National, with London capturing 60% of incremental spending | Medium term (2-4 years) |

| Mid-Week Leisure Stays Driven by Hybrid Work | +0.7% | England and Scotland's urban corridors, particularly regional cities | Medium term (2-4 years) |

| Growth in Outsourcing for Institutional Catering | +0.4% | National, concentrated in the education and healthcare sectors | Long term (≥ 4 years) |

| Sustainability-Focused Refurbishments and ESG Compliance | +0.5% | National, strongest in London and major metropolitan markets | Medium to long term (2–4 years and beyond) |

| Source: Mordor Intelligence | |||

Expansion of Digital Ordering & Booking

Contactless payment reached 94.6% of all eligible in-store card transactions in 2024, with each consumer averaging 236 contactless purchases at USD 20.14, and hospitality categories like hotels and entertainment posted stronger gains than foodservice peers, signaling durable behavior that supports digital-first operating models in the United Kingdom hospitality market[2]Source: Barclays, “Barclays Data Shows Contactless Spending Broke New Record in 2024,” Barclays, home. barclays. Operators plan technology investment at scale, as 85% of restaurant leaders expect to deploy AI and automation in 2025 for staff marketing, inventory management, and menu optimization, which underpins throughput and margin control as labor costs rise. The competitive gap is widening because large chains can roll out AI revenue management, self-service kiosks, and app-based loyalty programs while 60% of independents lack the capital or skills to implement comparable systems, reinforcing a structural advantage for scaled operators in the United Kingdom hospitality market. Real-world examples show measurable savings, with Edinburgh Zoo’s Time2Eat table-ordering app saving USD 168.97 per day and USD 61,328 annually through lower labor requirements, an impact that compounds across high-volume venues[3]Source: Office for National Statistics, “Economic Activity and Social Change in the UK, Real-Time Indicators: 18 December 2025,” Office for National Statistics, ons.gov.uk. Consumer adoption supports these tools, as QR code ordering and mobile wallets are preferred by significant cohorts of Gen Z and Millennials for higher-ticket transactions, placing convenience and speed at the center of purchase journeys. The differentiator is not just payments, but platforms that unify point-of-sale, inventory, and customer data to enable dynamic pricing and personalized upsells, which is where chain brands can scale faster than smaller venues in the United Kingdom hospitality market.

Government VAT Relief and Incentive Programs

The Autumn Budget 2025 announced a USD 5.38 billion package for retail, hospitality, and leisure in England, anchored by permanently lower business-rate multipliers from April 2026 that are intended to ease operating costs during a period of persistent wage and input inflation in the United Kingdom hospitality market[4]Source: Office for National Statistics, “Economic Activity and Social Change in the UK, Real-Time Indicators: 18 December 2025,” Office for National Statistics, ons.gov.uk. Permanent reductions in business-rate multipliers and preferential treatment for smaller and mid-sized properties are improving short-term cash flow and providing relief during a period of elevated wage and input cost inflation. Transitional relief mechanisms are also helping smooth the impact of revaluations by limiting abrupt increases in tax liabilities, allowing operators greater visibility in budgeting and investment planning. While these measures provide meaningful near-term support, they do not fully offset broader cost headwinds, including rising labor expenses and the gradual removal of transitional protections over time. In parallel, the introduction of visitor levies in parts of the United Kingdom adds complexity to destination-level cost structures and underscores how local policy decisions can either reinforce or constrain pricing power. Overall, government relief and incentive schemes act as a stabilizing driver for the United Kingdom hospitality market in the near term, even as structural cost pressures persist.

Increased Inbound Tourism Supported by a Weaker Currency

Inbound tourism to the United Kingdom continued to improve, with international visitor volumes increasing and total inbound spending reaching approximately USD 44 billion in 2025. Despite this growth, inflation-adjusted expenditure remained below pre-pandemic levels, indicating that gains in visitor numbers outpaced real spending recovery across the United Kingdom hospitality market. Nominal spending exceeded pre-pandemic benchmarks, supported by favorable currency dynamics and pricing adjustments, while the persistent real-terms gap highlighted ongoing value sensitivity among international travelers and reinforced the need for targeted offerings in long-haul and regional markets. The United States remained the most valuable source market, with visitor spending reaching roughly USD 8.5 billion in 2025 and accounting for a significant share of total international tourism receipts. This concentration underscored the importance of the United States market in driving inbound-led revenue growth for the United Kingdom's hospitality sector. Additional momentum came from screen tourism and other experience-driven travel, which supported the geographic dispersion of visitor spend beyond London and aligned with regional development strategies. However, competitive pressures persisted due to the United Kingdom's relatively high-cost position versus peer destinations, increasing the need for coordinated efforts between operators and destination authorities to protect market share and sustain inbound growth.

Mid-Week Leisure Stays Driven by Hybrid Work

The expansion of hybrid working has reshaped weekday demand patterns in the United Kingdom hospitality market, blurring the line between business and leisure travel. Greater flexibility in work arrangements has encouraged guests to extend leisure stays into the working week, supporting stronger occupancy outside traditional peak periods and shifting demand toward mid-week leisure use. This behavior has been more pronounced in the United Kingdom than in several peer markets, requiring operators to adapt room products, amenities, and pricing to appeal to guests combining remote work with leisure travel. Regional cities have been key beneficiaries of this trend, leveraging strong transport links and local experiences to attract extended-stay guests. At the same time, reduced on-site workplace consumption has redirected spending toward hotel food and beverage outlets and nearby hospitality venues. Despite these positives, hybrid-led leisure demand typically generates lower yields than traditional corporate travel, suggesting that while this shift provides a structural uplift to baseline occupancy, it is unlikely to fully replace higher-margin business travel.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe Labour Shortages and Rising Wages | -1.8% | National, with the highest intensity in London and Southeast England | Short term (≤ 2 years) |

| Volatility in Food and Energy Costs | -0.9% | National, disproportionately affecting independent operators | Medium term (2-4 years) |

| Strict Planning and Licensing Regulations | -0.3% | National, with heightened enforcement in metropolitan boroughs | Long term (≥ 4 years) |

| High No-Show Rates for Reservations | -0.2% | National, concentrated in casual dining and mid-market restaurants | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Severe Labour Shortages and Rising Wages

The United Kingdom hospitality market continues to face significant cost pressures from rising wages and labor shortages. Increases to the minimum wage and related payroll obligations have substantially raised staffing costs, particularly for entry-level and part-time roles, tightening already thin margins. Employer contributions and regulatory changes have further intensified cost exposure for a sector that relies heavily on seasonal and part-time labor. Staffing shortages remain a challenge, with persistent vacancies for chefs, waitstaff, and kitchen teams, compounded by tighter immigration and skilled-worker requirements that limit the labor pipeline. Operators are responding through workforce management technology, scheduling tools, and retention initiatives to mitigate turnover and improve efficiency. Despite these measures, elevated labor costs and constrained staffing continue to act as a key restraint on profitability and growth in the United Kingdom hospitality market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute labor shortages and wage inflation | -1.2% | England and Scotland core, Wales emerging | Long term (≥ 4 years) |

| Food and energy cost volatility | -0.9% | England, Scotland, Wales, Northern Ireland | Medium term (2-4 years) |

| Stringent planning / licensing rules | -0.4% | England regulatory focus, Scotland variations | Medium term (2-4 years) |

| High reservation no-show rates | -0.3% | England urban centers, Scotland cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Food and Energy Costs

The United Kingdom hospitality market is under pressure from rising and unpredictable food and energy costs. Prices for key ingredients such as meat, poultry, dairy, and produce have increased due to supply constraints, creating uncertainty for operators. Smaller and independent operators are particularly affected, as they have limited ability to hedge against these fluctuations. Energy costs remain high, with electricity, heating, and hot water representing a significant portion of operational expenses. Many operators have been forced to adjust menus and raise prices to protect margins. At the same time, consumers are responding with more selective spending, which can limit revenue growth.

Segment Analysis

By Type: Franchise-Led Expansion Versus Independent Margin Pressure

Chain hotels in the United Kingdom are expected to grow at a 7.88 % CAGR from 2026–2031, outpacing the wider hospitality market as scale delivers centralized procurement, stronger brand visibility, and loyalty programs that boost repeat bookings. Premier Inn maintained a notable RevPAR advantage over the United Kingdom midscale and economy segment, while Whitbread’s statutory revenue in the United Kingdom and Ireland declined due to deliberate changes in food and beverage strategy, highlighting how larger portfolios preserve pricing power and operational efficiency. IHG recorded growth in both RevPAR and occupancy, supported by net system expansion that drives pipeline conversions and supply-led growth. Leading hotel groups are increasingly adopting digital tools, including room selection technology, AI assistants, automated scheduling, and invoice processing, which help improve asset utilization amid elevated wage and energy costs. In contrast, independent operators controlled a majority of market share, but a significant portion operated at a loss, reflecting the financial pressures they face without the benefits of scale procurement and brand-led distribution.

The investment cycle now favors owners and brands that can execute conversions and use balance-sheet flexibility to renew assets for higher returns, with private equity activity rising in 2025, targeting premium independents for roll-ups or asset-light platforms, and distressed sales accelerating via pre-pack administrations and quick portfolio realignments. Budget chains like Travelodge continued site additions through H1 2025, aiming to consolidate share as mid-market independents exit. Complex policy issues such as tip allocation rules and business-rate revaluation increase compliance costs that larger groups absorb with centralized HR/finance systems, while independents manage changes property-by-property. Overall, the United Kingdom hospitality market is shifting to a more scalable structure, expanding franchise and management contracts across branded portfolios, while owner-operators pivot to differentiated concepts or location-driven advantages. For investors and lenders, cash-flow visibility and diversified distribution now weigh more heavily than before 2020, driving a stronger appetite for brands with proven direct channels and loyalty economics.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Accommodation Class: Luxury Premiums and Budget-Hotel Resilience

Luxury is the fastest-growing class in the United Kingdom hospitality market, projected to expand at a 7.98 % CAGR from 2026–2031 as high-net-worth travelers emphasize experiential stays and fine dining. A large majority of top-tier travelers dedicate significant portions of their budgets to travel, with many anticipating that their spending will increase noticeably over the coming months. London remains the anchor for this pipeline momentum, with marquee openings such as Waldorf Astoria’s Admiralty Arch and Six Senses London reinforcing the city’s role as a gateway for luxury demand and culinary brands. Regional luxury is also broadening, with new assets in Northern Ireland and across England’s countryside and coastal destinations leveraging heritage properties and wellness-led formats to extend guest stays. Investor interest in premium casual dining and lifestyle brands that monetize loyal communities and higher average checks continues to support strong pricing power across the sector.

Mid and upper-midscale hotels control about 39.38% of the market but are squeezed at both ends of the spectrum as consumers gravitate toward either experience-led luxury or value-focused budget options, prompting the need for targeted refurbishments and proposition upgrades. Budget and economy formats show structural resilience by leaning on consistent product, streamlined operations, and direct distribution channels to maintain occupancy and repeat traffic. Whitbread aims to expand its open rooms across the United Kingdom and Ireland, funding growth through asset recycling and reinforcing its confidence in the long-term efficiency of its business model. Travelodge has continued its development program with multiple new hotel openings this year, navigating cost pressures while reporting improved trading that aligns with seasonal demand recovery. Extended-stay and serviced apartments, such as the dual-branded Hyatt Place and Hyatt House in Leeds, continue to capture longer stays and hybrid work travel, illustrating a bifurcation in the market where luxury wins on experience and budget on efficiency while middle segments recalibrate to defend share.

By Booking Channel: Direct Digital Gains Versus OTA Dominance

Direct digital channels are projected to grow at a 7.34% CAGR through 2031, reflecting operators’ increasing focus on owning guest data, optimizing yield, and strengthening loyalty ecosystems within the United Kingdom hospitality market. By steering bookings toward proprietary platforms, hotels can reduce reliance on intermediaries while enabling personalized cross-selling and targeted offers that enhance guest lifetime value. Despite this shift, online travel agencies still accounted for 37.24% of bookings in 2025, supported by their global reach and demand-generation capabilities, particularly for independent hotels that depend on marketplace visibility. Large brand systems demonstrate the power of scale, with World of Hyatt reaching 54 million members by end-2024, anchoring direct traffic and enabling tailored guest experiences. These loyalty-driven ecosystems reinforce repeat visitation while improving margin retention across branded portfolios.

Major United Kingdom operators are also investing in digital functionality to improve conversion and engagement, as seen in Premier Inn’s choose-your-room tools and AI assistant pilots designed to enhance customer control and service responsiveness. Industry research indicates that direct booking strategies not only lower commission costs but can also increase average spend per night when guests personalize their stay. This dynamic is driving continued investment in CRM platforms, data analytics, and digital user experience to support higher-value transactions. Alongside leisure demand, corporate and MICE segments remain strategically important, with rising inquiry levels across Europe supporting a steady pipeline of event-led business. Together, these trends strengthen the outlook for United Kingdom city-center assets through 2026 as operators balance leisure, business, and group demand through diversified distribution strategies.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

England accounted for 71.28% of the United Kingdom hospitality market in 2025 and continues to dominate investment activity and new supply, with London ranked as the most attractive city for hotel investment. A strong pipeline of openings scheduled across 2025 and 2026 reinforces the capital’s global appeal and role as the primary gateway for international demand. The supply outlook is led by high-profile luxury and lifestyle debuts, including new flagship brands, alongside extensive asset repositioning and refurbishment programs that enhance inventory quality and support higher average daily rates. Beyond London, regional cities such as Manchester, Birmingham, and Leeds are sustaining momentum through diversified demand drivers, including events, culture, and business travel. Looking ahead to 2026, forecasts point to moderate RevPAR growth underpinned by stable occupancy and disciplined pricing as demand patterns normalize.

Scotland held a significant market share, with Edinburgh consistently identified as the most attractive regional city for hotel investment in the United Kingdom. The city continues to attract boutique and lifestyle hotel openings, supported by a strong calendar of festivals and a resilient year-round corporate base. From 2026, however, the introduction of a 5% visitor levy adds a new consideration for operators as they balance pricing strategies and occupancy levels. Wales, representing 4.0% of the market, is seeing selective upscale development in coastal and resort locations that appeal to domestic leisure and wellness-focused travelers. Across both regions, hybrid working patterns are elevating the importance of regional connectivity, flexible meeting spaces, and event-driven demand to smooth midweek performance.

Northern Ireland is the fastest-growing United Kingdom region, with a forecast 8.24% CAGR through 2031, driven by cross-border tourism, infrastructure investment, and a comparatively lower cost base. Growth is supported by steady expansion in quick-service and casual dining formats, alongside rising hotel and mixed-use development activity. Belfast, in particular, benefits from its position within the wider Belfast–Dublin corridor, enabling joint itineraries that blend urban tourism with scenic routes. Ongoing reviews of licensing and regulatory frameworks could further improve operating conditions for hospitality venues. Overall, the United Kingdom hospitality market offers multiple geographic investment plays, with London anchoring luxury demand, Edinburgh leading boutique growth, regional English cities forming lifestyle clusters, and Northern Ireland accelerating from a smaller but rapidly expanding base.

Competitive Landscape

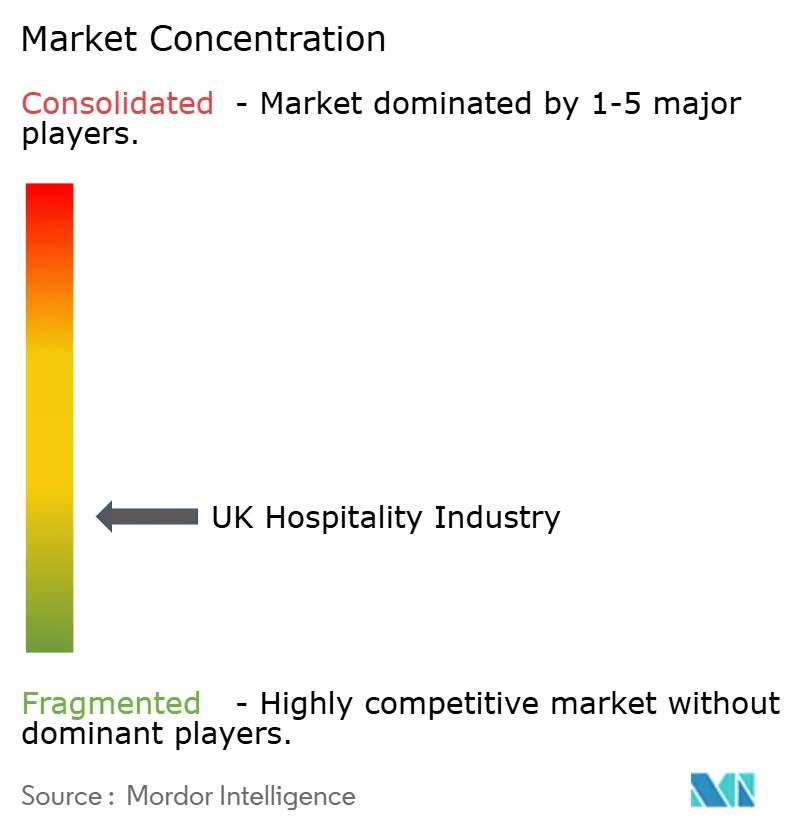

The United Kingdom hospitality market remains highly fragmented, with a small group of leading operators accounting for a minority of total market share while the balance is spread across regional chains, franchise networks, and owner-operated independents. Consolidation activity accelerated as investors increasingly pursued scale advantages, platform efficiencies, and portfolio rationalization. Private equity participation intensified, reflecting confidence in asset repositioning and operational leverage despite ongoing cost pressures. Strategic reviews within the pub sector highlighted debt-led optimization, as operators evaluated divestments to rebalance capital structures and focus on higher-return assets. At the same time, global hotel brands signaled confidence in recovery across extended-stay and business travel by committing to meaningful portfolio expansion in the United Kingdom.

Technology adoption has emerged as a key competitive differentiator for large hospitality platforms. Leading operators have expanded digital tools such as room-selection features, artificial intelligence assistants, automated invoice processing, and workforce scheduling to reduce overhead and improve consistency at scale. These investments support margin resilience as labor, energy, and compliance costs remain elevated. Independent operators often lag in digital adoption due to capital constraints and limited in-house expertise, widening the productivity gap between chains and single-site venues. Distribution strategy further amplifies this divide, as branded groups push direct bookings through loyalty ecosystems while independents continue to rely more heavily on third-party marketplaces to capture demand.

Recent strategic activity underscores ongoing repositioning across pubs, quick-service, and lifestyle segments. Operators have streamlined management structures and shifted assets into partnership or franchise models to simplify operations and stabilize returns. Mid-market casual dining has faced particular pressure, with several portfolios changing hands through restructuring processes. In contrast, quick-service and value-led concepts continue to expand, supported by compact formats, supply-chain investment, and consumer demand for affordable indulgences. Looking ahead, regulatory conditions around business rates, licensing, and tipping practices will play an important role in shaping margins, investment decisions, and the pace of growth across local markets.

United Kingdom Hospitality Industry Leaders

Whitbread PLC

InterContinental Hotels Group (IHG)

Compass Group PLC

Greene King

Mitchells & Butlers

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Burger King United Kingdom announced plans to open approximately 30 new restaurants annually starting in 2026, supported by a new 20-year master franchise agreement extending its reach into the Republic of Ireland for the first time, with private-equity backer Bridgepoint investing USD 18.77 million recently and a further USD 25.03 million expected over the next 18 months.

- November 2025: Stonegate Group, the United Kingdom's largest pub operator with over 4,300 sites, confirmed it is exploring strategic options for its "Platinum" portfolio of approximately 1,000 premium leased and tenanted pubs, valued at up to USD 1.25 billion, to reduce its USD 3.75 billion plus debt burden.

- October 2025: Whitbread PLC announced it secured final planning permission for its second Premier Inn hotel in Cork, Ireland (174 rooms), with construction expected to begin in early 2026, marking a step toward the company's uplifted network target of 5,000 Premier Inn rooms across Ireland.

- March 2025: Hyatt Hotels Corporation announced a plan to grow its United Kingdom portfolio by more than 30% between 2025 and 2026, adding over 1,000 rooms to the market and creating approximately 250 new United Kingdom jobs, with the dual-branded Hyatt Place Leeds and Hyatt House Leeds (305 combined keys) opening in March 2025 to kick off the expansion, followed by Hyatt Place London Paddington and Hyatt Regency London Olympia.

United Kingdom Hospitality Market Report Scope

The hospitality industry includes businesses that provide services to guests and travelers. This sector includes lodging (hotels and resorts), food and beverage services, event planning, theme parks, transportation, and other related services. The hospitality industry in the United Kingdom is segmented by type and segment. By type, the market is segmented into chain hotels and independent hotels. By segment, the market is segmented into luxury hotels, mid and upper-mid-scale hotels, budget and economy hotels, and service apartments. The report offers market sizing and forecasts in value (USD) for all the above segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Midscale Hotels |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate/MICE |

| Wholesale & Traditional Agents |

By Geography (Value)

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Midscale Hotels | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate/MICE | |

| Wholesale & Traditional Agents | |

| By Geography (Value) | England |

| Scotland | |

| Wales | |

| Northern Ireland |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the United Kingdom hospitality market?

The United Kingdom hospitality market is valued at USD 63.80 billion in 2026 and is projected to reach USD 78.28 billion by 2031, reflecting a 4.18% CAGR.

Which categories are growing fastest and which hold the largest shares?

Independent hotels held a 57.28% share in 2025, while chain hotels are forecast to grow at a 7.88% CAGR. Luxury accommodations are the fastest-growing class at 7.98% CAGR England held 71.28% share in 2025, OTAs held 37.24% of bookings in 2025, and Direct Digital channels are set to grow at 7.34% CAGR.

What demand drivers should executives track through 2026?

Key tailwinds include accelerating digital ordering and booking, rising inbound tourism supported by a weak GBP, hybrid work boosting mid-week leisure stays, outsourcing momentum in institutional catering, and targeted tax and rates relief measures.

What are the biggest headwinds to profitability in the United Kingdom hospitality landscape?

Persistent wage inflation and labor shortages, elevated food and energy input costs, higher business rates and local visitor levies, reliance on high-commission OTA channels for independents, and price-sensitive demand patterns are the main constraints.

Where are the most attractive geographic opportunities right now?

London remains the anchor for international demand and luxury, Northern Ireland shows the fastest growth at 8.24% CAGR, Edinburgh leads in regional investment appeal, and major English cities like Manchester, Birmingham, and Leeds continue to add branded supply and lifestyle concepts.