Saudi Arabia Hospitality Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

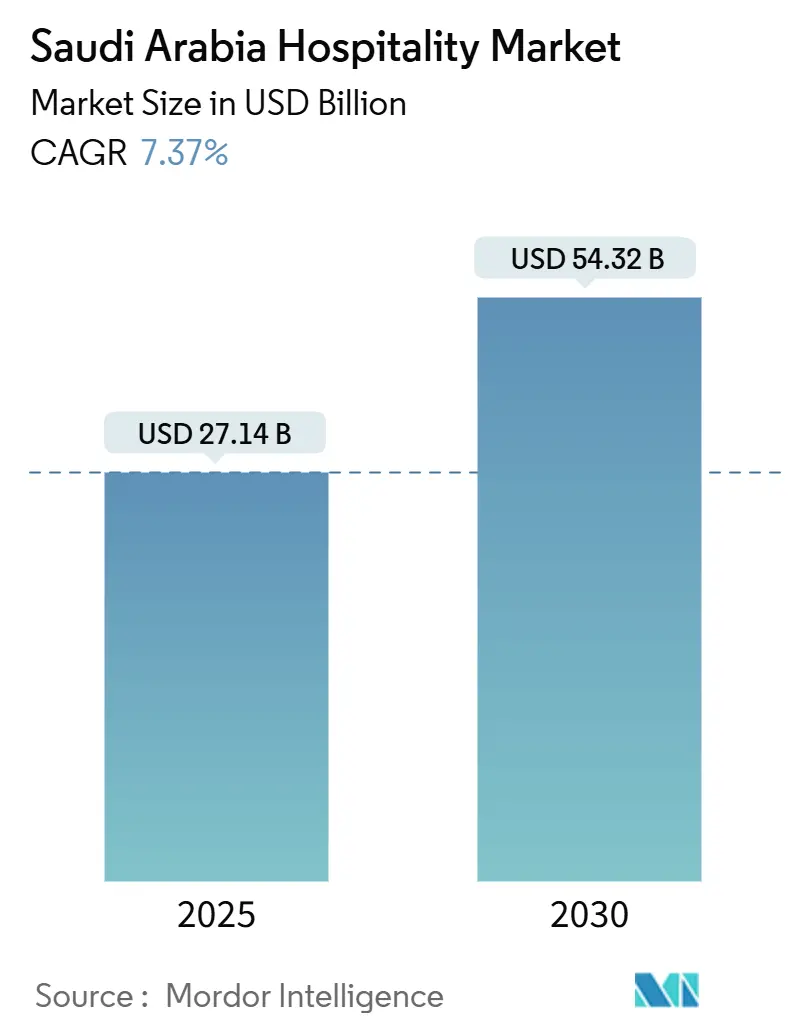

| Market Size (2025) | USD 27.14 Billion |

| Market Size (2030) | USD 54.32 Billion |

| Growth Rate (2025 - 2030) | 7.37% CAGR |

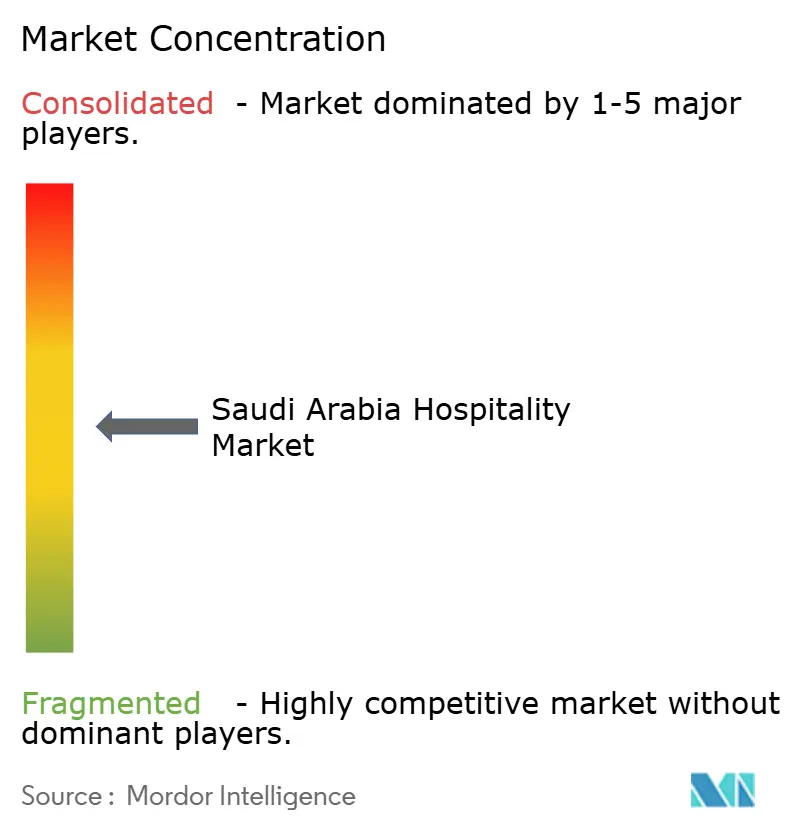

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Hospitality Market Analysis by Mordor Intelligence

The Saudi Arabia Hospitality Market size is estimated at USD 27.14 billion in 2025, and is expected to reach USD 54.32 billion by 2030, at a CAGR of 7.37% during the forecast period (2025-2030).

Demand continues to broaden as Vision 2030 funnels fresh capital into giga-projects, strengthens domestic leisure infrastructure, and simplifies visa processes, all of which lift both business and leisure arrivals. Chain operators accelerate brand rollouts to secure prime sites, while luxury and serviced-apartment formats diversify the offer, ensuring alignment with shifting traveller preferences. Digital distribution strategies deepen hotel-to-guest engagement, prompting an upswing in direct bookings and loyalty-program enrolments even as OTAs retain a large share of transactional volume. Continuous RevPAR outperformance relative to pre-2019 levels underscores healthy pricing power in key cities despite an intensive construction pipeline.

Key Report Takeaways

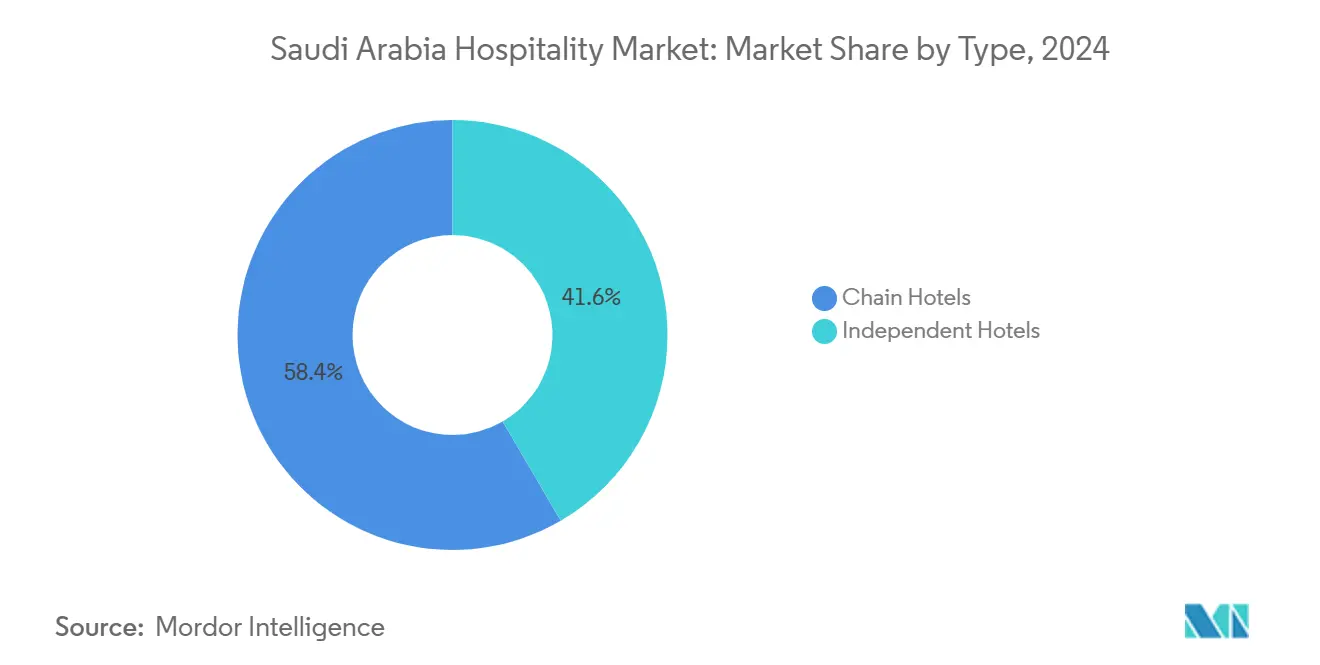

- By type, chain hotels commanded 58.38% of the Saudi Arabia hospitality market share in 2024; independent hotels are forecast to trail as chain operators outpace them with a 12.36% CAGR through 2030.

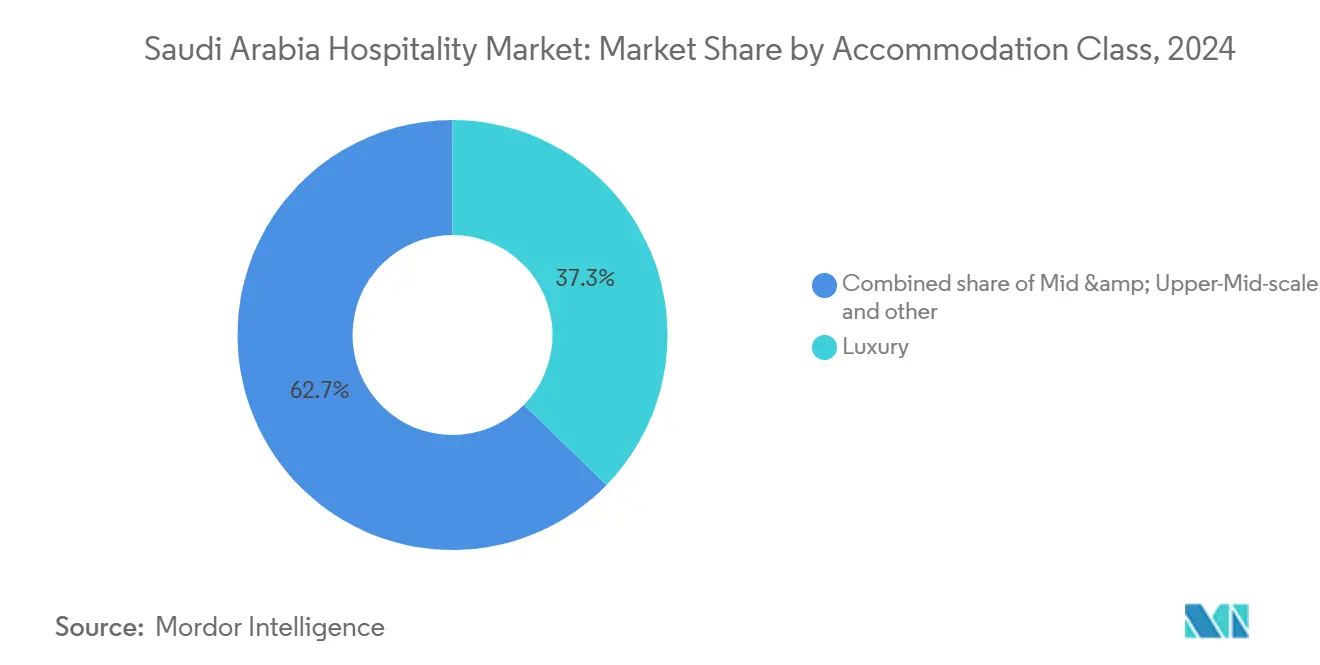

- By accommodation class, the luxury segment led with 37.33% of the Saudi Arabia hospitality market size in 2024, whereas serviced apartments are advancing at a 13.33% CAGR through 2030.

- By booking channel, OTAs captured 42.33% of transactions of the Saudi Arabia hospitality market share in 2024, while direct digital channels are growing at 15.65% CAGR as hoteliers invest in proprietary platforms.

- By geography, the Makkah–Jeddah corridor held 27.14% of the Saudi Arabia hospitality market size in 2024, yet the Red Sea and wider western coast are set to expand at a 19.38% CAGR to 2030.

Saudi Arabia Hospitality Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 tourism mega-investment programme | 2.8% | Global, concentrated in NEOM, Red Sea, Diriyah | Long term (≥ 4 years) |

| Rapid growth in religious tourism (Hajj & Umrah) | 2.1% | Makkah & Medina corridors, spill-over to Jeddah | Medium term (2-4 years) |

| Luxury demand from giga-projects (NEOM, Red Sea, Diriyah) | 1.9% | Red Sea & Western Coast, Northern Frontier | Long term (≥ 4 years) |

| Rising domestic leisure travel & disposable income | 1.2% | National, with early gains in Riyadh, Eastern Province | Short term (≤ 2 years) |

| Extended-stay demand from giga-project workforces | 0.8% | NEOM, Red Sea, Qiddiya project zones | Medium term (2-4 years) |

| Unified e-visa schemes boosting transit & short stays | 0.7% | Global, concentrated in Riyadh and Jeddah gateways | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Tourism Mega-Investment Program Transforms Market Dynamics

Public Investment Fund commitments totalling USD 500 billion to NEOM alone redraw the development map, ushering in a pipeline of ultra-luxury, upper-upscale, and lifestyle properties unprecedented in the region. Sindalah Island’s debut in 2024 delivered an initial 440 keys, serving as proof-of-concept for sustainability-driven resort clusters that cap visitor numbers to protect fragile ecosystems[1]NEOM, “Sindalah Opening,” neom.com . Complementary projects such as the USD 20 billion Diriyah Gate reinforce the Kingdom’s positioning beyond religious tourism by curating heritage-focused hospitality anchored in premium cultural experiences. Collectively, the giga-projects are slated to create roughly 380,000 jobs, some of which fall inside hotel and F&B operations, thereby elevating local workforce participation in the Saudi Arabia hospitality market. Forward bookings for first-phase assets confirm resilient demand from high-net-worth individuals seeking new luxury frontiers.

Rapid Growth in Religious Tourism Drives Infrastructure Expansion

In 2024, the kingdom recorded over 18.5 million pilgrim arrivals, comprising 16.9 million for Umrah and 1.61 million for Hajj, according to data from Skift and the Ministry of Hajj and Umrah. The government has set a strategic target to attract 30 million Umrah pilgrims annually by 2030. Projects such as the USD 26.6 billion Masar Destination integrate retail promenades with 41,000 hotel rooms[2]Lodging Econometrics, “Middle East Hotel Pipeline,” lodgingeconometrics.com . Medina’s Knowledge Economic City brings over 2,000 keys within walking distance of the Prophet’s Mosque. AI-enabled crowd-management platforms under the Smart Hajj initiative streamline pilgrim flows, scaling occupancy rates during peak seasons without compromising safety. As religious travel remains less vulnerable to macroeconomic cycles, hotel developers lock in long-term cash flow via master leases and strategic alliances with pilgrimage operators.

Luxury Demand from Giga-Projects Creates Premium Market Segment

Resorts in NEOM, the Red Sea Project, and AlUla are implementing innovative, low-density, high-yield operational models that emphasize environmental sustainability and cultural preservation. Properties such as Rosewood Amaala and Aman Hegra are strategically positioning themselves to compete with established benchmarks in the Mediterranean and Indian Ocean markets. However, their differentiation lies in leveraging desert landscapes and heritage-driven narratives, integrated with zero-carbon architectural designs. These luxury developments are benefiting from strategic collaborations with the Public Investment Fund, which facilitates expedited permitting processes and infrastructure development while enforcing stringent design and operational standards. The phased introduction of these resorts is expected to attract a higher proportion of affluent visitors, thereby increasing the average expenditure per visitor and contributing to the overall growth of Saudi Arabia hospitality market.

Rising Domestic Leisure Travel Expands Market Base

Domestic tourism spends rose 43% year-on-year to almost USD 40 billion in 2023, anchored in expanding disposable incomes and a youthful population where 60% are under 30 years old. Projects like Soudah Peaks in the Asir Highlands diversify the calendar by offering summer mountain retreats. Enhanced rail and air connectivity shortens travel times, prompting multi-city leisure itineraries that lengthen average stays. Government-backed events ranging from Riyadh Season festivals to Qiddiya sports fixtures tilt stay patterns toward weekends, smoothing seasonality dips in business demand. As locals grow more comfortable booking direct, hoteliers refine loyalty programs to capture repeat visits and cultivate lifetime value in the Saudi Arabia hospitality market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imminent oversupply is pressuring ADRs in key cities | -1.8% | Riyadh, Jeddah, are concentrated in business districts | Short term (≤ 2 years) |

| Seasonality of religious tourism causes demand swings | -1.2% | Makkah & Medina corridors, secondary impact on Jeddah | Medium term (2-4 years) |

| Mid-scale supply gap limiting domestic affordability | -0.9% | National, particularly secondary cities | Medium term (2-4 years) |

| Saudization quotas are inflating operating costs | -0.7% | National, with higher impact in the labor-intensive luxury segment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imminent Oversupply Pressures Average Daily Rates

The pipeline of 316 projects, comprising 83,275 rooms currently under construction, presents potential near-term rate-compression challenges. This is particularly evident in Riyadh, where inventory is projected to witness substantial growth before 2028[3]Arab News Staff, “Makkah Hotel Prices Dive,” arabnews.com. Upscale and luxury projects account for a significant share of future supply, leaving the mid-scale segment under-represented and intensifying competition at the top end. Jeddah witnessed a 10% year-on-year ADR decline in select quarters, signalling sensitivity to incremental keys during ramp-up phases. Operators respond by sharpening segmentation strategies, leveraging data-driven revenue tools, and broadening ancillary income streams. While long-term fundamentals remain positive, near-term rate volatility requires disciplined phasing and agile asset management within the Saudi Arabia hospitality market.

Seasonality of Religious Tourism Creates Demand Volatility

Hotel operators in Makkah encounter operational complexities due to significant fluctuations in occupancy rates. These rates peak during Hajj and drop sharply during off-peak periods, creating challenges in optimizing workforce management, inventory control, and cash flow strategies. Peak-season suite rates can jump from SAR 70,000 to SAR 80,000 (USD 18,667 to 21,333), yet soft shoulder months require tactical promotions to attract domestic visitors[4]Gulf Construction, “Masar Destination Investment,” gulfconstructiononline.com . Visa allotment adjustments tied to public-health or geopolitical considerations introduce further unpredictability, amplifying revenue swings. Operators diversify into F&B-led concepts and flexible meeting spaces to buffer room-rate cyclicality. In the medium term, the Kingdom’s push for year-round events and cultural festivals aims to stabilize occupancy patterns across the Saudi Arabia hospitality market.

Segment Analysis

By Type: Chain Hotels Accelerate Market Consolidation

Chain hotels held 58.38% of the Saudi Arabia hospitality market share in 2024 and are projected to advance at a 12.36% CAGR through 2030 as international groups race to secure flagship locations. Portfolio depth enables multi-brand clusters in mega-projects, granting operators economies of scale across staffing, procurement, and technology. Loyalty ecosystems amplify direct-booking growth, reducing reliance on high-commission intermediaries. Independent hotels respond by spotlighting hyper-local experiences in cultural destinations such as AlUla yet face distribution-cost headwinds absent chain affiliation. As Vision 2030 accelerates project openings, the Saudi Arabia hospitality market size associated with chain hotels is poised to nearly double, reinforcing branded dominance.

Momentum favours chains because they leverage global pipelines and standardized training programs to meet Saudization requirements efficiently. Cross-segment brand families from economy concepts to ultra-luxury flags allow chains to absorb oversupply stresses by flexing rate fences across their portfolios. Joint ventures with sovereign-backed developers accelerate capital deployment, while asset-light management contracts safeguard balance sheets. Independent operators must carve out niches in heritage or eco-resort segments where authenticity trumps corporate uniformity.

By Accommodation Class: Serviced Apartments Emerge as Growth Leaders

Luxury accommodations commanded 37.33% of the Saudi Arabia hospitality market size in 2024, underpinned by giga-project resorts that target high-net-worth travellers with experiential value propositions. However, serviced apartments post the fastest expansion at a 13.33% CAGR, fuelled by extended-stay demand from construction and corporate workforces attached to Vision 2030 sites. Residential-style layouts cater to longer average lengths of stay, while integrated digital platforms support self-service guest journeys. Mid-scale and economy stock remains thin, limiting affordability for domestic travellers and pilgrims outside peak seasons. Brands such as Wyndham’s Super 8 seek to close this gap, signalling latent upside in budget supply as disposable incomes diversify.

Serviced apartments benefit from lower operating costs per available unit, enabling competitive pricing while preserving margins. Investors are attracted to favourable lease structures and reduced seasonality volatility compared with traditional hotels. Luxury’s pipeline remains sizable but is increasingly scrutinized for sustainability and experiential authenticity metrics that justify premium ADRs. Budget-segment whitespace persists, offering room for disruptive models to capture under-served price-sensitive segments in the Saudi Arabia hospitality market. Consequently, room-count contributions from serviced apartments could triple by 2030, recalibrating product-mix economics across the sector.

Note: Segment shares of all individual segments available upon report purchase

By Booking Channel: Direct Digital Channels Surge Despite OTA Dominance

OTAs controlled 42.33% of bookings in 2024, sustained by price transparency and regional super-app integrations. Yet direct digital transactions are projected to climb at a 15.65% CAGR as hotels deploy mobile-first engines, dynamic packaging, and personalized promotions. Loyalty-linked rate parity and member-only perks improve conversion, enhancing net revenue through commission savings. MICE and corporate travel leverage centralized procurement tools that favour direct connections for duty-of-care compliance and spend analytics. Wholesale agents remain relevant in group pilgrimage tourism where tailored pre- and post-sales support is critical.

Technology adoption across revenue-management, CRM, and payment-gateway stacks accelerates digital shift momentum, particularly given the Kingdom’s young, high-smartphone-penetration demographic. Government digitization campaigns streamline identity verification and e-visa issuance, further simplifying direct booking flows. OTAs respond by bundling value-added services and strengthening Arabic-language content to sustain engagement. As direct channels gain ground, the Saudi Arabia hospitality market will likely witness net-rate improvement and stronger brand-to-guest relationships, reinforcing long-run profitability.

Geography Analysis

In the Saudi Arabia hospitality market, the Makkah & Jeddah Corridor is projected to remain the largest geographic sub-segment in 2024, accounting for 27.14% of the market, while the Red Sea & Western Coast region is expected to be the fastest-growing between 2025 and 2030, with a CAGR of 19.38%. The Riyadh Region continues to serve as the Kingdom's central hub for political and corporate activities, with ADRs reaching unprecedented levels during high-profile events such as the Future Investment Initiative. A robust pipeline of projects indicates substantial room-count growth; however, the concurrent development of the King Abdullah Financial District and the addition of new convention facilities are expected to mitigate oversupply risks by driving consistent corporate demand throughout the year. Uptake of mixed-use precincts combining offices, retail, and entertainment prolongs visitor stay and spend. Meanwhile, leisure-oriented mega-developments like Qiddiya broaden appeal beyond weekday corporate traffic, smoothing weekend occupancy dips.

Peak performance during Hajj underscores reliable compression periods for rate yield, though pronounced seasonality warrants agile revenue strategies. Upcoming airport expansions and cruise-terminal upgrades will likely channel additional leisure traffic into the corridor outside pilgrimage seasons. Six Senses Southern Dunes’ LEED Platinum certification sets sustainability benchmarks for future openings, while Sindalah Island’s phased roll-out positions the archipelago as a year-round yachting hub. International airport connectivity and renewable-energy infrastructure underscore the region’s long-range viability and premium pricing profile. Secondary coastal cities eye spill-over prospects, prompting early-stage feasibility studies for mid-scale beach resorts. Altogether, the western seaboard is poised to emerge as a credible alternative to traditional sun-and-sand destinations across the Mediterranean.

Competitive Landscape

International hotel groups drive the pace of development in Saudi Arabia, collectively managing approximately half of the market share. These operators demonstrate varied strengths across luxury, lifestyle, and mid-scale segments. While asset-light management and franchise models dominate, some players are taking equity stakes in marquee projects to align closely with sovereign partners. Meanwhile, domestic consolidation is gaining momentum, highlighted by Taiba Investments’ merger with Dur Hospitality, creating a sizable 7,700-room platform that enhances negotiation leverage with global distribution networks. Technology adoption is accelerating, with innovations like Mandarin Oriental Al Faisaliah’s AI-driven mobile ordering app boosting guest personalization and ancillary revenues.

Strategic partnerships and market segmentation are shaping growth, as seen with Wyndham’s rollout of 100 Super 8 economy properties and Hilton’s introduction of the Tapestry Collection in Madinah. These moves deepen brand presence across diverse market tiers. Collaborations with digital distribution providers such as Sabre’s SynXis and SHR’s loyalty platforms strengthen revenue management and reduce reliance on online travel agencies (OTAs). Boutique hotels are also making their mark by leveraging cultural heritage, exemplified by The Chedi Hegra in AlUla, which achieves premium rates through immersive local experiences. This diversification in offerings reflects a maturing and increasingly sophisticated market landscape.

Labor market dynamics and regulatory compliance play a critical role in operational success. Operators who effectively implement Saudization policies and integrate local supply chains gain a cost advantage amid tightening labor conditions. The steady conversion of development pipelines and entry of prominent global brands signal strong market confidence. As brand storytelling and operational excellence become key competitive differentiators, Saudi Arabia’s hospitality sector is poised for sustained growth. The industry’s focus on innovation, strategic alliances, and cultural relevance positions it well for future challenges and opportunities.

Saudi Arabia Hospitality Industry Leaders

-

Accor SA

-

Radisson Hotel Group

-

Marriott International Inc.

-

Hilton Worldwide Holdings

-

InterContinental Hotels Group (IHG)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Hilton signed its first Tapestry Collection by Hilton in Saudi Arabia, the 221-room Diyar Ajwa in Madinah, slated to open late 2025.

- May 2025: IHG entered into agreements with Ashaad Company for three properties in Jeddah and Al Khobar, adding over 1,700 rooms scheduled between 2028 and 2030.

- May 2025: Wyndham and Le Park Concord announced a 100-hotel Super 8 development plan spanning a decade, with first delivery in 2026.

- April 2025: HMH confirmed expansions in Al Khobar and Makkah, including a flagship 460-room project in the holy city.

Saudi Arabia Hospitality Market Report Scope

Hospitality falls under the broad umbrella of the service industry, a tertiary sector of the economy. It includes food & beverages, stay, travel, theme parks, hotels, and event planning, amongst others. The Saudi Arabian hospitality industry is segmented by type and segment. By type, the market is segmented into chain hotels & independent hotels. By segment, the market is segmented into service apartments, budget and economy hotels, and mid-scale and upper-mid-scale luxury hotels. The report offers market size and forecasts for the Saudi Arabian Hospitality Market in value (USD) for all the above segments.

| Chain Hotels |

| Independent Hotels |

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Serviced Apartments |

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

| Riyadh Region |

| Makkah & Jeddah Corridor |

| Medina |

| Eastern Province (Dammam/Al-Khobar) |

| Red Sea & Western Coast (incl. NEOM) |

| Southern Highlands (Asir & Abha) |

| Northern Frontier (Tabuk/Al-Ula) |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Serviced Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Riyadh Region |

| Makkah & Jeddah Corridor | |

| Medina | |

| Eastern Province (Dammam/Al-Khobar) | |

| Red Sea & Western Coast (incl. NEOM) | |

| Southern Highlands (Asir & Abha) | |

| Northern Frontier (Tabuk/Al-Ula) |

Key Questions Answered in the Report

How large is the Saudi Arabia hospitality market in 2025?

The market is valued at USD 27.14 billion in 2025 and is forecast to reach USD 54.32 billion by 2030, growing at 7.37% CAGR.

Which segment shows the highest growth through 2030?

Serviced apartments lead with a 13.33% CAGR, fuelled by extended-stay demand from giga-project workforces.

Why are direct digital bookings rising so quickly?

Hotels invest heavily in mobile-first engines and loyalty programs, pushing direct channels toward a 15.65% CAGR while reducing OTA commission costs.

Which region is projected to grow fastest?

The Red Sea and western coast are set to expand at a 19.38% CAGR, driven by eco-luxury resorts and new international gateway airports.

What is the main risk to average daily rates in key cities?

A pipeline of 83,275 rooms—especially luxury inventory concentrated in Riyadh and Jeddah could temporarily pressure ADRs until demand fully absorbs new supply.

How concentrated is the competitive landscape?

The top five global operators hold about half of existing rooms, indicating moderate concentration and room for differentiated new entrants.

Page last updated on: