High-Strength Concrete Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

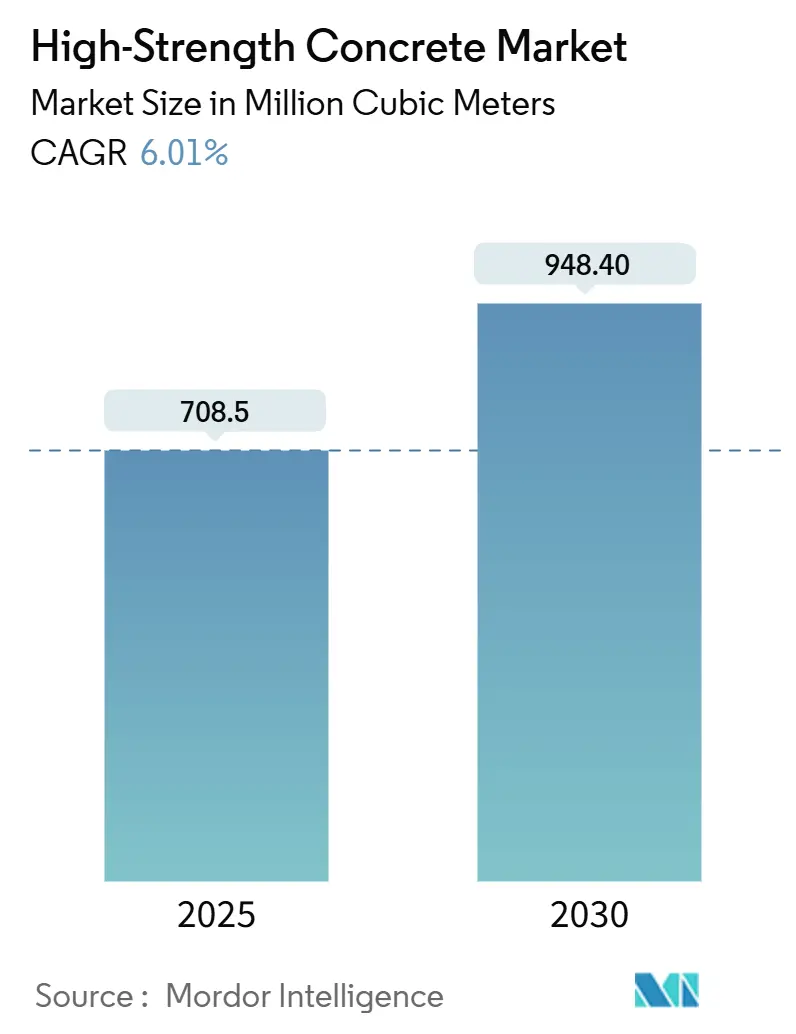

| Market Volume (2025) | 708.5 Million cubic meters |

| Market Volume (2030) | 948.40 Million cubic meters |

| Growth Rate (2025 - 2030) | 6.01% CAGR |

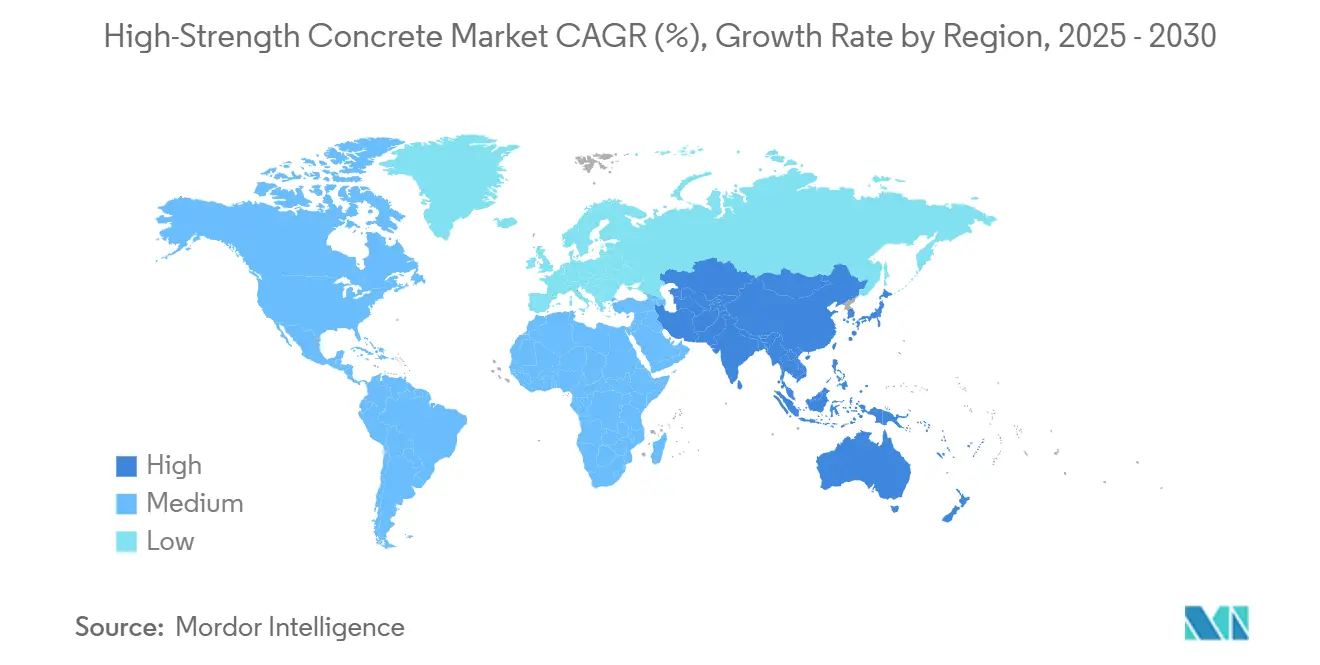

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

High-Strength Concrete Market Analysis by Mordor Intelligence

The High-Strength Concrete Market size is estimated at 708.5 Million cubic meters in 2025, and is expected to reach 948.40 Million cubic meters by 2030, at a CAGR of 6.01% during the forecast period (2025-2030). Demand grows as builders pursue taller structures, deeper foundations, and longer-span bridges that exceed conventional material limits. Government megaproject pipelines, offshore wind foundations needing 100 MPa-plus mixes, and AI-guided batching systems that guarantee consistent performance all reinforce expansion. Contractors increasingly weigh life-cycle savings against upfront cost, favoring high-strength mixes that reduce repair cycles and extend asset service life. Supply chain investments in supplementary cementitious materials and digital quality controls further accelerate the adoption of these materials, while regional policies that price carbon heighten the business case for cement-efficient, high-strength formulations.

Key Report Takeaways

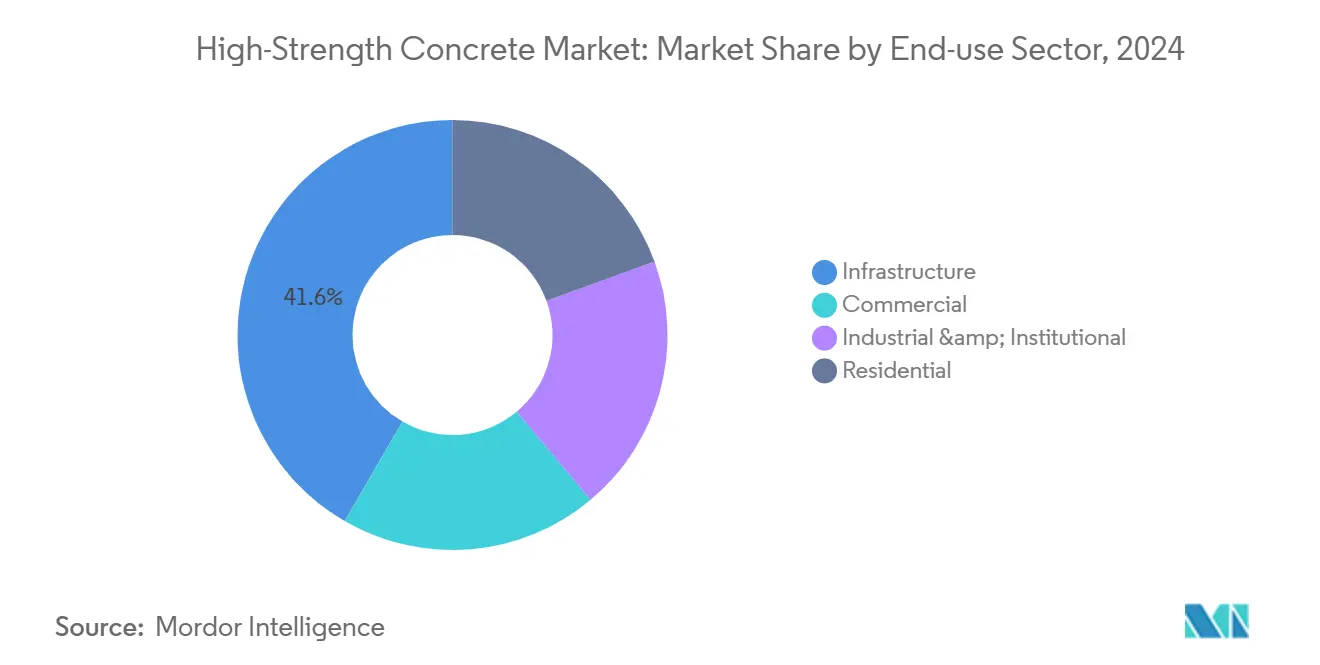

- By end-use sector, infrastructure led with a 41.64% share of the high-strength concrete market in 2024; the commercial segment is projected to expand at a 6.68% CAGR through 2030.

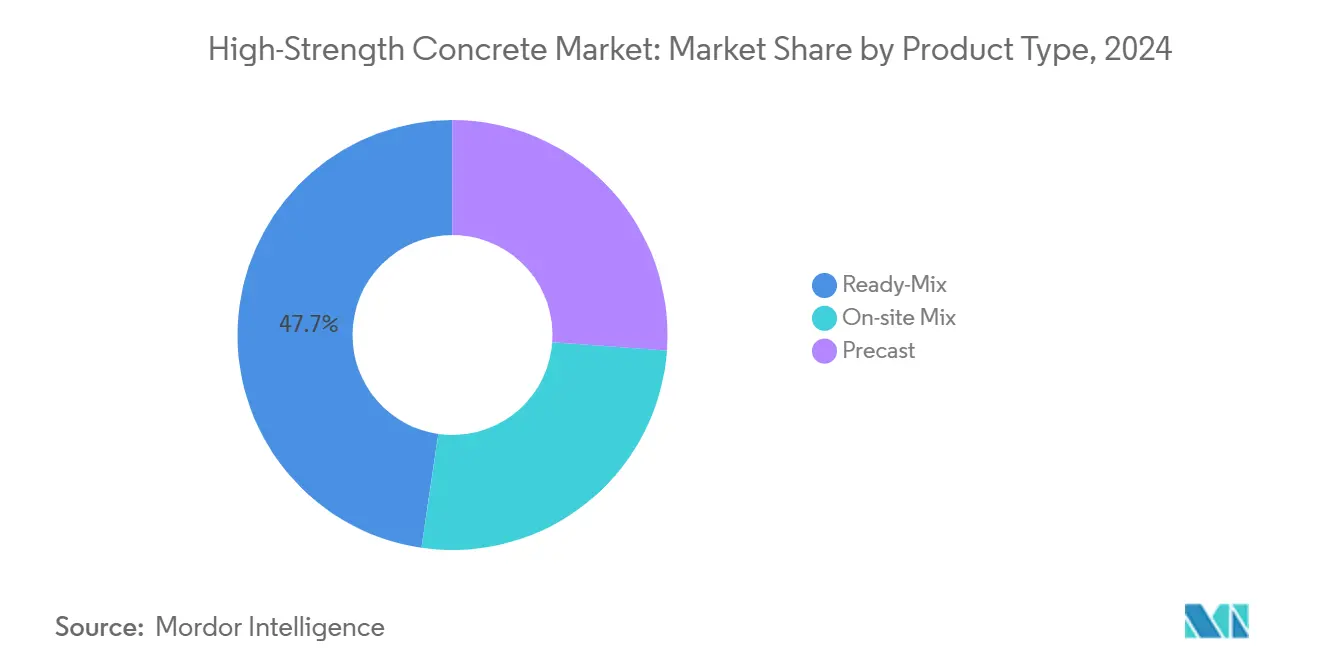

- By product type, ready-mix captured a 47.71% share of the high-strength concrete market size in 2024, while precast is expected to advance at a 6.54% CAGR through 2030.

- By region, the Asia-Pacific region accounted for a 52.36% share of the high-strength concrete market size in 2024 and is projected to advance at a 6.17% CAGR through 2030.

Global High-Strength Concrete Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public-sector megaproject pipeline surge | +1.2% | Global with concentration in APAC and Middle East | Medium term (2-4 years) |

| High-rise & mixed-use urban redevelopment | +0.8% | North America and core EU markets, expanding to APAC | Short term (≤ 2 years) |

| Life-cycle cost savings over conventional concrete | +0.9% | Global with early adoption in developed markets | Long term (≥ 4 years) |

| AI-controlled batching & digital twins raise specifications consistency | +1.1% | North America and EU leading, APAC following | Medium term (2-4 years) |

| Carbon pricing pushes high-strength, cement-lean mix adoption | +0.7% | EU and California leading, expanding globally | Long term (≥ 4 years) |

| Offshore-wind foundations demand 100 MPa-plus concretes | +1.0% | North Sea, Baltic, and East Asian coasts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Public-Sector Megaproject Pipeline Surge

State-funded energy corridors, rail networks, and bridge replacements standardize specifications that favor concrete with a minimum compressive strength of 60 MPa or higher. The European Union’s REPowerEU plan allocates EUR 300 billion for energy infrastructure that must meet higher durability standards. India’s National Infrastructure Pipeline earmarks USD 1.4 trillion for projects through 2030, driving a steady call-off schedule that lets producers amortize investments in specialized batching plants. Multi-year tenders lower demand volatility, so manufacturers introduce dedicated high-strength product lines to secure framework agreements. Agencies also revise procurement codes to prioritize the total cost of ownership over the lowest bid, a move that fosters high-strength concrete market penetration. The trend favors firms with vertically aligned cement, admixture, and logistics operations that can guarantee timely supply to megaproject sites.

High-Rise & Mixed-Use Urban Redevelopment

Super-tall developments in New York, London, and Shanghai specify 80 MPa concrete for core walls and transfer girders, enabling thinner elements and higher leasable area. Fifteen towers exceeding 300 m in Manhattan alone are planned through 2028, each requiring tens of thousands of cubic meters of high-strength mixes[1]Council on Tall Buildings and Urban Habitat, “Skyscraper Center Project List,” ctbuh.org. Architects in Singapore and Seoul replicate the approach to optimize land use within height-restricted zones. Municipal density bonuses reward slender buildings, making high-strength concrete a design enabler rather than an optional upgrade. Developers working on mixed-use podiums integrate retail, office, and residential floors, all supported by high-load transfer slabs that rely on robust compressive strength. The fastest uptake occurs where building codes already recognize high-strength classes, allowing streamlined approvals and shorter construction schedules.

Life-Cycle Cost Savings Over Conventional Concrete

The American Concrete Institute reports 25%–40% life-cycle cost reduction when designers specify high-strength mixes for bridges and marine structures. Lower permeability cuts chloride ingress, shrinking maintenance budgets tied to rebar corrosion. For a four-lane viaduct, cost modeling shows total savings exceeding USD 3 million over 50 years, despite a 20% premium on initial concrete. Asset owners in freight rail and port authorities internalize these savings because service disruptions cost more than materials. Insurance firms also offer discounts on premiums when structures adopt proven high-strength designs, providing additional financial incentives. As asset management shifts toward availability-based contracts, contractors adopt high-strength concrete market solutions to meet performance guarantees without inflating maintenance contingencies.

AI-Controlled Batching & Digital Twins Raise Specifications Consistency

Automated dosage systems monitor moisture, temperature, and real-time slump, delivering 95% specification compliance across thousands of loads, according to Command Alkon field data. Digital twins simulate hydration and thermal profiles, helping producers tailor mixes for dense rebar cages or aggressive marine exposure. Contractors using these platforms report a 15% reduction in material waste while avoiding costly on-site rework. Sensors embedded in trial pours feed back into the twin, fine-tuning subsequent deliveries for uniform performance on multi-tower jobs. The capabilities shorten approval cycles because owners gain data-driven assurance that every batch meets tight strength corridors. Producers able to demonstrate such precision gain preferred-supplier status in the high-strength concrete market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium raw-material & admixture costs | -0.60% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Skilled-labour & QC capability gap in emerging markets | -0.40% | APAC emerging markets, Latin America, Africa | Medium term (2-4 years) |

| Silica-fume supply volatility post-chip-industry shifts | -0.50% | Global, with concentration in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Raw-Material & Admixture Costs

Silica fume averaged USD 255 /t in 2024, triple the price of fly ash, while polycarboxylate superplasticizers add USD 20–25 per m³ to production costs. Such inputs increase delivered prices by 40%–80% above conventional mixes, limiting uptake in budget-constrained housing and municipal projects. Semiconductor demand tightened silica fume supply, resulting in spot shortages that forced batching plants to ration their high-strength output. Specialty admixture markets remain concentrated among a handful of chemical companies, limiting price competition and increasing exposure to supply chain disruptions. Contractors locked into lump-sum contracts face margin erosion when input costs spike, leading risk-averse specifiers to lean toward lower-grade alternatives. These dynamics dampen short-term volume growth until supply diversification and formulations based on locally sourced SCMs mature.

Skilled-Labour & QC Capability Gap in Emerging Markets

Producing 80 MPa concrete demands rigorous batching, placement, and curing controls that many emerging-market contractors have yet to master. On-site testing often lacks the necessary equipment for rapid chloride permeability or maturity monitoring, which can lead to increased rejection rates and project delays. Ministries still draft codes with a 40–50 MPa baseline strength, leaving design teams without standardized guidance for higher classes. Local labs capable of ASTM C1202 testing cluster in capital cities, forcing remote projects to ship samples hundreds of kilometers. Shortages of certified concrete technologists slow technology transfer, and language barriers limit uptake of international training modules. Until vocational programs ramp up, specifiers hedge by selecting conventional grades that align with existing skill sets, thereby constraining the growth of the high-strength concrete market in those regions.

Segment Analysis

By End Use Sector: Infrastructure Dominance Drives Volume

Infrastructure captured 41.64% of the high-strength concrete market share in 2024. Road, rail, and port owners mandate 60 MPa mixes for bridge decks, tunnels, and quay walls to double design life without major rehab. The commercial sector is projected to post the fastest 6.68% CAGR to 2030, as mixed-use towers in dense urban cores utilize 80 MPa columns that free up floor area. Industrial demand centers on chemical plants and data centers where heavy loads and aggressive environments favor high-strength specifications. Institutional users, such as hospitals, adopt the material for long-span slabs that accommodate flexible interior layouts. Although residential volume remains modest, luxury high-rise developers in Hong Kong and Dubai pilot 70 MPa walls to maximize views on limited footprints. Asset managers value reduced downtime, so infrastructure owners continue to anchor demand, while private real estate accelerates overall volume expansion.

The commercial segment benefits from rapid permitting cycles that favor thin structural members, reaching a forecast volume of 210 million m³ by 2030. Institutional and industrial segments continue to grow steadily as design-build teams become more familiar with higher-strength classes. Residential penetration remains opportunistic, tied to premium locations where structural efficiency offsets cost premiums. Across categories, owners converge on life-cycle cost models that quantify 25% maintenance savings, further entrenching high-strength concrete market adoption in capital-intensive projects.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Ready-Mix Leadership Meets Precast Innovation

Ready-mix held 47.71% of the high-strength concrete market share in 2024, leveraging dense batching networks that deliver loads of 60–80 MPa within tight time windows. Established producers invest in automated calibration and GPS-tracked fleets to maintain slump and temperature specifications during transit. Precast units are projected to grow at a 6.54% CAGR to 2030, as factory controls achieve 100 MPa strengths with low variability, enabling the production of modular façades, bridge girders, and wind-turbine tower sections. On-site mixing remains a niche application for remote hydroelectric dams and island wind farms, where logistics constraints necessitate the use of field batching plants.

The high-strength concrete market size for ready-mix is forecast to reach 450 million m³ by 2030, supported by urban infrastructure upgrades. Precast expansion outpaces overall growth, reaching over 275 million m³ in the same year, thanks to accelerated setting lines and the introduction of digital curing chambers. Producers integrate RFID tags to trace each element’s batch data, simplifying quality audits. Hybrid supply chains emerge where ready-mix delivers core walls while precast supplies façade panels, optimizing schedule and cost. Field mixing technology advances with containerized micro-plants that blend local aggregates with imported ultra-fine SCMs, unlocking applications in developing islands and mountainous terrain.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The Asia-Pacific region accounts for 52.36% of the high-strength concrete market size in 2024 and is expected to expand at a 6.17% CAGR through 2030. China dominates the volume through Belt and Road rail corridors and coastal LNG terminals, which rely on 70 MPa concrete to resist abrasion and freeze-thaw cycles. India rapidly scales high-strength adoption across economic corridors with National Infrastructure Pipeline funding, pushing local suppliers to qualify 60 MPa mixes under government quality audits. Japan rebuilds coastal defenses with ultra-high-performance concrete after typhoon damage, while South Korea earmarks smart-city districts that showcase 80 MPa eco-efficient slabs. Southeast Asian nations, including Vietnam and Indonesia, are piloting carbon-priced procurement frameworks that reward cement-lean, high-strength formulations.

North America leverages the USD 550 billion Infrastructure Investment and Jobs Act, targeting bridge replacements and port upgrades, where 80 MPa concrete halves maintenance cycles[2]U.S. Department of Transportation, “Infrastructure Investment and Jobs Act Fact Sheet,” transportation.gov . Private developers in New York, Toronto, and Seattle specify 90 MPa cores for mixed-use towers to unlock additional rentable area under height caps. The region also pioneers AI-guided batching, with cloud platforms aggregating sensor data from ready-mix fleets to ensure compliance across dispersed job sites. Stricter Buy-Clean rules in California drive demand for cement-efficient high-strength mixes, encouraging local innovation in calcined clay and limestone filler blends.

Europe’s Green Deal channels emissions budgets toward materials with better strength-to-cement ratios. Scandinavian agencies now prequalify 70 MPa bridge decks as standard, citing 30% lower life-cycle CO₂. Germany upgrades Autobahn interchanges with high-strength precast girders that cut nighttime lane closures, while the Netherlands pilots 100 MPa lock gates for inland waterways. Carbon pricing embeds the cost advantage of cement-lean designs, advancing the high-strength concrete market across EU member states. Eastern European countries draw on cohesion funds to modernize rail viaducts, creating nascent high-strength supply chains.

South America shows emerging momentum as Brazil’s concession program modernizes 15,000 km of highways, specifying 60 MPa pavement slabs for heavy freight corridors. Chile’s copper ports demand chloride-resistant high-strength concrete to lengthen maintenance intervals. However, limited access to silica fume keeps adoption uneven across the continent. Middle East & Africa record project-specific spikes: Saudi Arabia’s NEOM megacity employs 80 MPa mixes for wind-resistant façades, while South Africa tests high-strength precast panels for affordable housing pilot blocks. Technical training partnerships with European producers begin closing skill gaps, signaling potential acceleration beyond 2027.

Competitive Landscape

The High-Strength Concrete market features moderate fragmentation, with global majors and regional specialists competing on formulation know-how, digital integration, and supply reliability rather than sheer volume. Digital twin services differentiate suppliers as owners demand data transparency. Sasol-BASF admixture alliances enable real-time rheology adjustments within batching trucks, minimizing on-site QC rejects. Producers integrate blockchain-based traceability for carbon accounting, positioning their high-strength concrete market offers within net-zero tenders. Market share shifts hinge on the ability to guarantee 95% specification compliance under tropical heat or desert humidity, areas where only a subset of contenders currently excel.

High-Strength Concrete Industry Leaders

-

CEMEX, S.A.B. de C.V.

-

CRH

-

Heidelberg Materials

-

HOLCIM

-

UltraTech Cement Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Shree Cement Limited made its debut in the southern Indian market, inaugurating its inaugural Ready-Mix Concrete (RMC) plant in Yelahanka, located in North Bengaluru. This facility boasts a designed capacity of 101 cubic meters per hour and is also equipped to produce high-strength concrete.

- May 2025: Holcim bolstered its portfolio by acquiring Compañia Minera Luren. This Peruvian producer of specialty building solutions boasts an annual revenue exceeding USD 40 million. The company in the building materials industry offers a range of specialized concrete products, including high-strength, rapid-setting, self-compacting, and high-density options.

Global High-Strength Concrete Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. On-site Mix, Precast, Ready-Mix are covered as segments by Product. Asia-Pacific, Europe, Middle East and Africa, North America, South America are covered as segments by Region.| Commercial |

| Industrial & Institutional |

| Infrastructure |

| Residential |

| On-site Mix |

| Precast |

| Ready-Mix |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By End Use Sector | Commercial | |

| Industrial & Institutional | ||

| Infrastructure | ||

| Residential | ||

| By Product Type | On-site Mix | |

| Precast | ||

| Ready-Mix | ||

| By Region | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Market Definition

- END-USE SECTOR - High strength concrete consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of high-strength concrete including ready-mix, precast, and on-site mix is considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms