High-Pressure Die Casting Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 42.53 Billion |

| Market Size (2031) | USD 57.43 Billion |

| Growth Rate (2026 - 2031) | 6.19% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

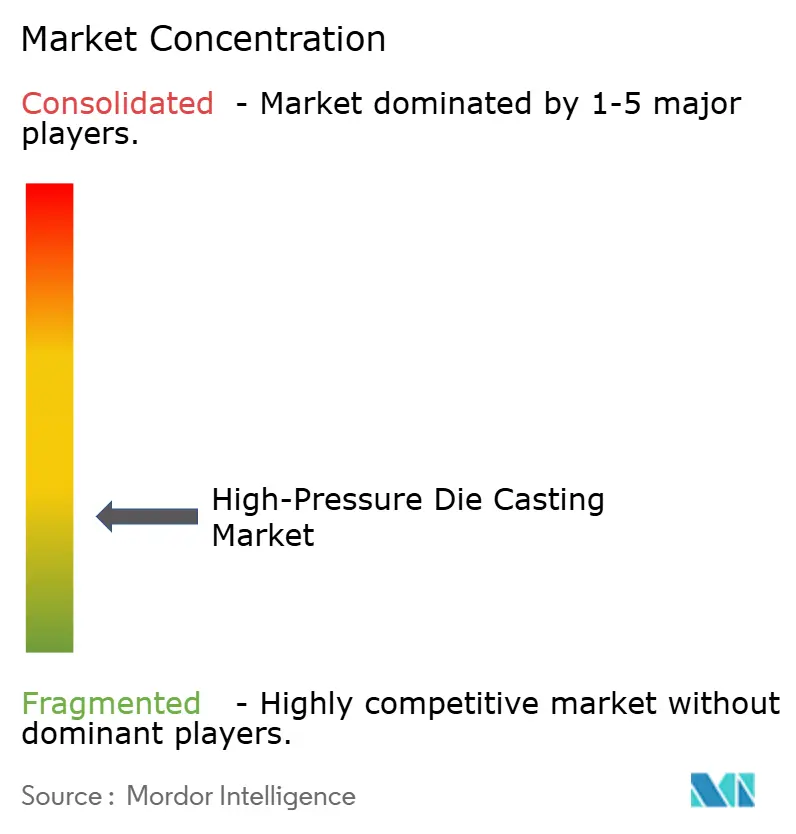

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

High-Pressure Die Casting Market Analysis by Mordor Intelligence

The high-pressure die casting market size was USD 42.53 billion in 2026 and is forecast to reach USD 57.43 billion by 2031 at a 6.19% CAGR. Continuous light-weighting initiatives, giga-press adoption, and closed-loop alloy recycling accelerate demand as automakers transition from internal-combustion engines to full battery-electric platforms. Regional carbon-border tariffs, beginning staged enforcement in 2026, are pushing offshore suppliers to localize casting capacity to avoid penalties and meet embodied-emission benchmarks. At the same time, alloy price volatility is strengthening the business case for in-house recycling loops that cut feedstock costs and satisfy tightening ESG targets. Overall, investments in magnesium and vacuum or squeeze casting cells signal a structural shift toward higher-value, safety-critical components that demand exceptionally low porosity.

Key Report Takeaways

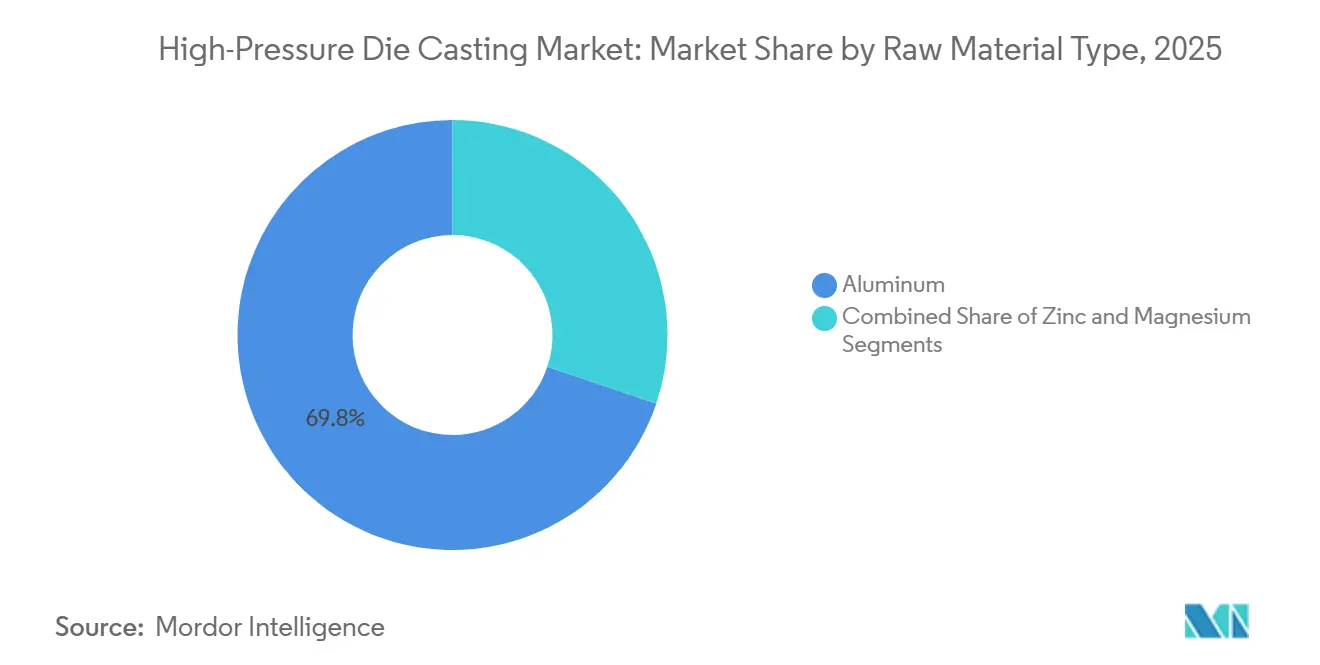

- By raw material type, aluminum dominated with 69.84% revenue share in 2025; magnesium is projected to expand at an 8.32% CAGR through 2031.

- By application, automotive commanded 61.23% of the high pressure die casting market share in 2025, while EV and electrified powertrain components are set to grow at an 8.89% CAGR through 2031.

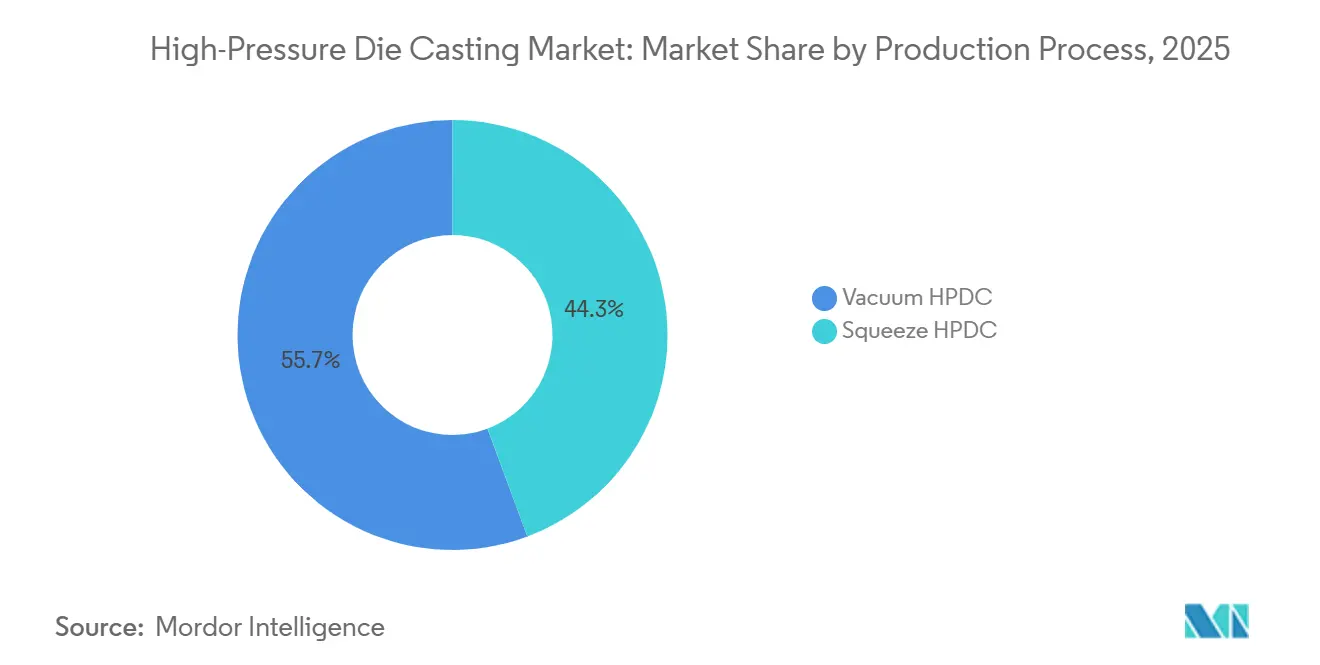

- By production process, vacuum HPDC led with 55.67% share of the high pressure die casting market size in 2025 and squeeze HPDC is advancing at a 7.74% CAGR through 2031.

- By end-use component, body and structural parts accounted for 44.53% of 2025 revenue, and EV battery housing and motor components are climbing at a 10.35% CAGR to 2031.

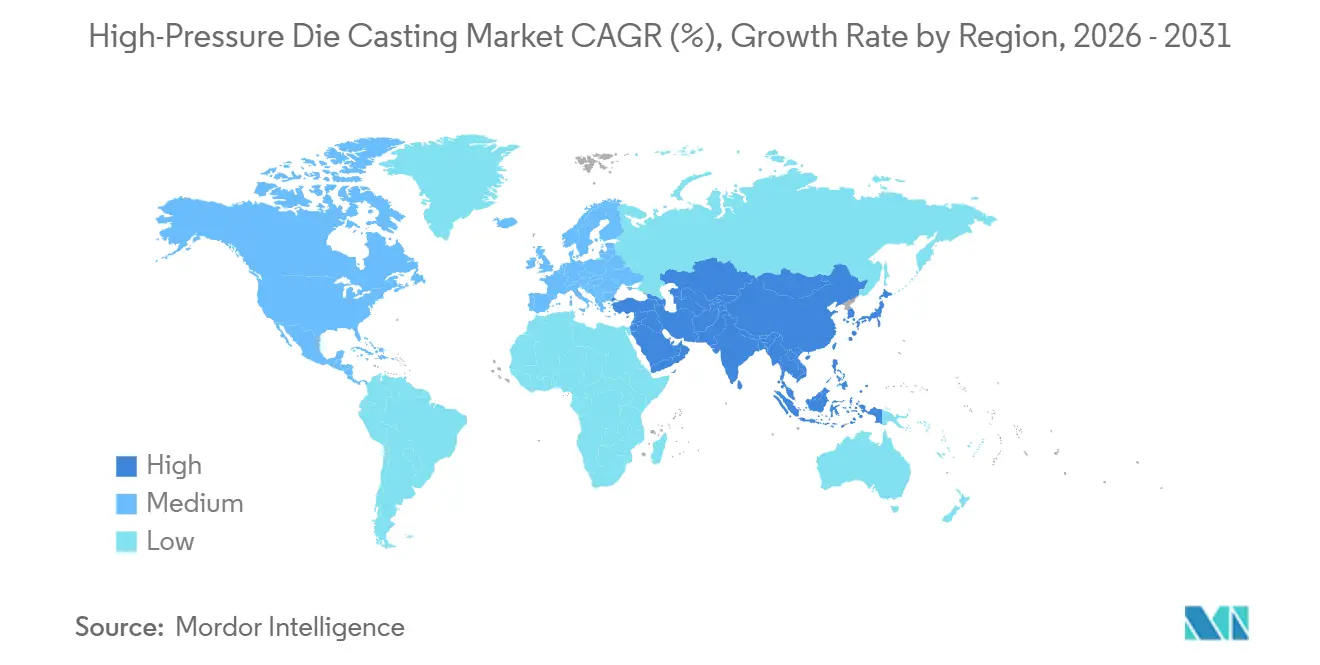

- By geography, Asia-Pacific held 47.37% of 2025 sales and is forecasted to rise at a 7.57% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High-Pressure Die Casting Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Giga-Press Installations | +1.6% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Light-Weighting | +1.3% | Global | Long term (≥ 4 years) |

| Thermal-Management Requirements | +1.1% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Demand for Near-Net-Shape Parts | +0.8% | Global | Short term (≤ 2 years) |

| Regional Carbon-Border Tariffs | +0.5% | Europe, North America | Medium term (2-4 years) |

| Rising Alloy Price Volatility | +0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Next-Gen Giga-Press Installations

Automakers are rolling out over 6,000-ton presses to cast full underbodies in one shot, slashing part counts from over 170 stampings to fewer than five structural castings. Tesla pioneered this template at Fremont and Berlin and operates 9,000-ton cells that run 24-hour cycles[1]“Single-Piece Rear Underbody Casting,” Tesla, tesla.com. Asian OEMs such as BYD and NIO have since installed similar presses, while European brands like Volvo followed suit in Slovakia. This consolidation eliminates multiple stamping dies and welding stations, cuts line-side inventory, and reduces assembly time significantly. However, a single-press failure can halt an entire final-assembly line, so redundancy and predictive-maintenance software have become critical risk-mitigation tools. Foundries unable to fund giga-presses either move into niche magnesium castings or seek joint ventures with equipment suppliers to remain in high-volume programs.

Light-Weighting Push From ICE-to-EV Shift

Battery packs add 400-700 kg to a vehicle, driving engineers to cut mass elsewhere. High pressure die casting market demand for thin-wall aluminum and magnesium parts is rising because these substrates deliver 30%–50% weight savings over stamped steel. Euro 7 particulate limits that took effect in 2025 reward lighter vehicles with lower brake- and tire-wear emissions. Major global OEMs are consequently transferring die-casting from engine blocks to seat frames, cross-members, and battery trays. Magnesium’s strength-to-weight edge is boosting take-up for motor housings and interior brackets, though material cost and galvanic corrosion risks remain adoption hurdles. Asia-Pacific leads this trend due to China’s stringent new-energy vehicle quotas and India’s export incentives.

Battery-Housing Thermal-Management Requirements

Lithium-ion cells must stay within tight temperature windows to avoid runaway events. Vacuum HPDC embeds cooling channels directly into aluminum battery enclosures, eliminating separate heat exchangers and trimming assembly steps. Novelis’ Advanz e-series alloys satisfy crash performance and 150 W/m·K thermal conductivity thresholds. Foundries investing in vacuum or squeeze cells can meet flatness tolerances below 0.2 mm, essential for gasket integrity in large battery trays. As battery energy density rises, the technical bar for leak-free and porosity-free castings continues to move upward.

OEM Demand for Near-Net-Shape Parts

High pressure die casting achieves ±0.1 mm dimensional accuracy, cutting post-machining up to 70% versus gravity casting. Honda installed 6,000-ton machines in Ohio in 2025 that feed finished transmission housings directly to the assembly line, reducing cycle time and scrap. Near-net-shape capability is especially valuable in North America and Europe, where labor costs make extensive machining uneconomical. Tier-1 suppliers that automate trimming, x-ray inspection, and robotic deburring capture higher margins, whereas manual-finish foundries face quality variance and rising labor inflation.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Tooling Cost | -0.7% | Global | Short term (≤ 2 years) |

| Weld-Line Quality Issues | -0.4% | Global | Medium term (2-4 years) |

| ESG Mandates | -0.3% | Europe, North America | Long term (≥ 4 years) |

| Skilled-Operator Shortage | -0.2% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for Complex Parts

A single giga-press line can cost around USD 30 million, while dies for a large structural casting add USD 5-10 million with 12-18-month lead times. Only suppliers with strong balance sheets, or those sharing risk through joint ventures, can justify these investments. Consolidation is accelerating as large players acquire niche foundries to amortize tooling across multiple programs. Without committed EV volumes, smaller operators delay capex, which in turn limits regional capacity growth and elongates supply chains for OEMs.

Porosity and Weld-Line Quality Issues

Rapid metal injection can trap gas, forming voids that reduce fatigue life. Vacuum HPDC cuts porosity but raises equipment cost and cycle time, while squeeze casting improves density yet lowers throughput. These trade-offs keep forging and low-pressure casting relevant for the most safety-critical parts. Weld-line cracks still emerge in single-piece rear underbodies, prompting some OEMs to run CT scans on every batch before assembly, a step that adds cost and delays.

Segment Analysis

By Raw Material Type: Aluminum’s Dominance Amid Magnesium’s Niche Surge

Aluminum captured 69.84% of the 2025 market size, supported by fluidity, corrosion resistance, and mature scrap streams. Recycled content averaged 75% and leading automakers require verification certificates when awarding contracts. Magnesium is rising at an 8.32% CAGR due to significant weight savings for motor housings and steering brackets, but higher raw-material cost and galvanic-corrosion management confine it to premium EV platforms. Zinc remains favored for small connectors and EMI-shielded housings, but now faces polymer substitution pressure.

Closed-loop alloy programs lower aluminum feedstock costs and slash Scope 3 emissions, giving integrated processors a pricing edge. Magnesium recycling efforts are advancing via inert-atmosphere remelters launched in Japan and Germany, though oxidation losses still exceed 10%. The high-pressure die casting market size for aluminum parts is projected to sustain mid-single-digit growth, while the magnesium niche expands from a lower base but at the fastest rate through 2031.

Note: Segment shares of all individual segments available upon report purchase

By Application: Automotive Leads, EV Powertrain Shows Breakout Growth

Automotive contributed 61.23% of 2025 revenue, reflecting decades of die-cast engine blocks and transmission cases. The EV and electrified powertrain subset is forecast to grow 8.89% annually, capturing the expansion premium within the high-pressure die casting market. Electrical and electronics applications grow at a slower clip because LED heatsinks and connector shells are increasingly extruded or molded, whereas industrial equipment requires die casting for compressor and pump geometries but lacks the volume to match automotive.

Regulatory incentives in China and India underpin automotive casting demand, with local suppliers forming joint ventures to secure giga-presses. Conversely, electronics demand is fragmenting due to miniaturization and lower-power devices that shift to composites or plastics. As a result, automotive will deepen its revenue share, while other applications maintain low-to-mid-single-digit growth.

By Production Process: Vacuum HPDC’s Quality Edge vs. Squeeze HPDC’s Momentum

Vacuum HPDC held 55.67% of the 2025 revenue owing to less than 2% porosity levels essential for heat-treatable alloys and battery enclosures. Squeeze HPDC is forecasted to have a 7.74% CAGR, making it appealing for suspension knuckles and steering components where fatigue tolerance is paramount. Conventional HPDC remains the workhorse for non-critical housings.

The high-pressure die casting market share for vacuum cells is highest in Europe and Japan, where OEM quality specs drive adoption. Squeeze HPDC installations are clustering in China to satisfy domestic safety-critical contracts, employing hybrid machines that switch modes by program. Capital outlay and slower cycle times limit widespread squeeze deployment, but margins justify investment when defect-free density is compulsory.

By End-Use Component: Body Parts Still Lead, Battery Housings Accelerate

Body and structural parts delivered 44.53% of 2025 revenue, reflecting long-standing substitution of stamped steel. EV battery housings and motor components, although smaller today, are growing at a rate of 10.35% annually, the fastest segment expansion within the high-pressure die casting market. Engine and traditional powertrain parts will decline gradually but retain steady cash flows through hybrid powertrains.

Mega-cast rear underbodies compress welding, inventory, and inspection costs, turning die casting into a chassis technology. Battery trays must meet 200 kN crash loads and stringent thermal-runaway tests, pushing foundries toward vacuum or squeeze processes and high-silicon alloys. Transmission housings in multi-gear hybrids sustain demand, yet their long-term outlook dims as single-speed reducers dominate pure EVs.

Geography Analysis

Asia-Pacific accounted for 47.37% of 2025 sales and is projected to rise at a 7.57% CAGR through 2031, outpacing all regions. China’s over 15 million new-energy vehicles in 2025 created unprecedented pull for battery enclosures and giga-press underbodies. India’s export-linked incentives galvanized die-cast capacity expansions, while Japanese and South Korean foundries upgraded to vacuum cells to win premium contracts. Despite skilled-labor shortages and rising power prices, regional supply chains remain cost-competitive and integrated.

Europe posted a solid 2025 base and will grow 5.19% through 2031, buoyed by local content rules tied to battery-gigafactory investments. Carbon-border tariffs are prompting non-EU suppliers to localize fused alloy lines, and giga-press installations in Slovakia and Sweden secure supply for leading OEMs. High energy costs pressurize margins, accelerating automation and renewable-power purchase agreements.

North America is set to expand 4.99% through 2030, reflecting steady EV adoption but slower press installations. U.S. foundries add vacuum cells to serve domestic assembly plants, while Mexican facilities leverage lower labor costs yet must upgrade for safety-critical parts. Canada remains niche but may gain traction as battery-supply hubs emerge in Ontario and Quebec. South America’s 3.87% forecasted CAGR mirrors stagnant vehicle output and low EV penetration; Brazil anchors limited growth. Middle East and Africa will post 2.56% CAGR, with only Turkey and South Africa hosting notable die-casting clusters; local EV initiatives are nascent and volumes low.

Competitive Landscape

The high pressure die casting market continues to show moderate fragmentation. Equipment manufacturers such as Buhler and Idra are monetizing giga-press technology by licensing presses directly to automakers, a move that trims lead times and bypasses traditional foundry margins. Foundries without 6,000-ton capacity risk disqualification from single-piece underbody programs, forcing them toward niche magnesium castings or regional service work.

Acquisition activity accelerated in 2025 as suppliers sought scale to fund advanced presses and vacuum cells. Nemak’s USD 336 million purchase of GF Casting Solutions, strengthening its battery-tray and motor-housing footprint in North America and Europe[2]STAFF EDITOR, "Nemak acquires GF Casting Solutions’ automotive unit with a USD 336 million deal", AL CIRCLE, alcircle.com. Investors are channeling capital into automation, x-ray inspection, and scrap-loop furnaces that lift margins and satisfy OEM sustainability audits. Consolidation gives larger groups the volume needed to amortize multi-cavity tooling across multiple vehicle platforms.

Strategic models are coalescing around vertical integration, technology licensing, and quality differentiation. Tesla operates in-house giga-press lines that eliminate foundry mark-ups and enable rapid design iteration, a template that BYD and Volvo have begun to replicate. Mid-tier suppliers in India and Japan are installing vacuum or squeeze cells to offer porosity levels below 2% for safety-critical parts, trading throughput for premium pricing. Chinese contenders such as Bohai Automotive leverage subsidies and lower labor costs to undercut incumbents on commodity housings, forcing established players to automate or exit low-margin segments.

High-Pressure Die Casting Industry Leaders

-

GF Casting Solutions AG

-

Shiloh Industries Inc.

-

Ryobi Die Casting

-

Nemak SAB De CV

-

Rheinmetall AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Jaya Hind Industries committed INR 2 billion (~USD 24 million) to expand a Tamil Nadu facility for HPDC structural castings aimed at domestic EV programs.

- November 2025: SAGA Poland introduced in-cell heat-treatment technology that hardens castings at the press station, trimming total cycle time by approximately 20%.

- October 2025: Costamp Group opened a Turkish branch to serve regional die-casting and molding clients with localized engineering support.

Global High-Pressure Die Casting Market Report Scope

High-pressure die casting (HPDC) is a manufacturing process wherein molten metal is injected at high speed and pressure into a steel mold or die to form products. This method is favored for mass-producing complex metal parts with high precision, excellent surface finish, and enhanced mechanical properties.

The high-pressure die-casting market is segmented by raw material type, production process, application, end-use component, and geography. Based on raw materials, the market is segmented into aluminum, zinc, and magnesium. By application, the market is segmented into automotive, electrical and electronics, industrial applications, and other applications. Based on the production process, the market is bifurcated into vacuum high-pressure die casting and squeeze high-pressure die casting. By end-use component, the market is segmented into engine and powertrain parts, body and structural parts, transmission parts, and ev battery housing and motor components. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. The report offers market size and forecasts in terms of value (USD) for all the above segments.

| Aluminum |

| Zinc |

| Magnesium |

| Automotive |

| Electrical and Electronics |

| Industrial Applications |

| Other Applications |

| Vacuum HPDC |

| Squeeze HPDC |

| Engine and Powertrain Parts |

| Body and Structural Parts |

| Transmission Parts |

| EV Battery Housing and Motor Components |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Raw Material Type | Aluminum | |

| Zinc | ||

| Magnesium | ||

| By Application | Automotive | |

| Electrical and Electronics | ||

| Industrial Applications | ||

| Other Applications | ||

| By Production Process | Vacuum HPDC | |

| Squeeze HPDC | ||

| By End-Use Component | Engine and Powertrain Parts | |

| Body and Structural Parts | ||

| Transmission Parts | ||

| EV Battery Housing and Motor Components | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the high pressure die casting market be by 2031?

It is forecasted to reach USD 57.43 billion, expanding at a 6.19% CAGR from 2026.

Which region shows the fastest growth in high pressure die casting demand?

Asia-Pacific leads with a projected 7.57% CAGR through 2031, lifted by China’s and India’s EV production boom.

Why are giga-presses important for die casting suppliers?

Presses above 6,000 tons enable single-piece underbodies that cut part counts and assembly time, securing long-term OEM contracts.

What raw material is gaining the most momentum after aluminum?

Magnesium castings are rising at 8.32% annually owing to significant weight savings for EV motor housings.