| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 7.61 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

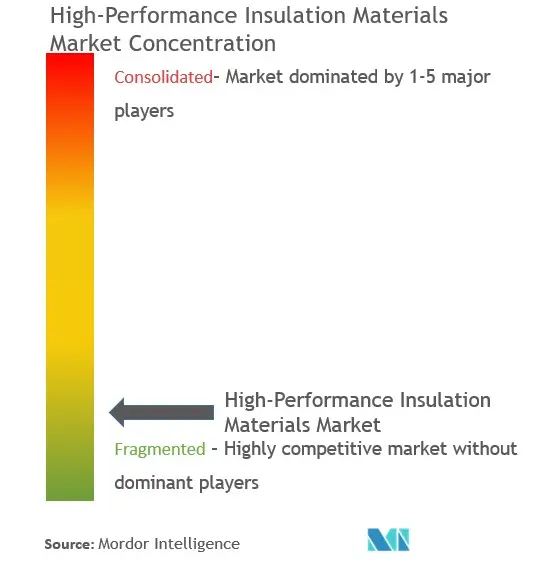

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

High Performance Insulation Materials Market Analysis

The High-Performance Insulation Materials Market is expected to register a CAGR of 7.61% during the forecast period.

The high-performance insulation materials industry is experiencing significant transformation driven by rapid industrialization and infrastructure development across major economies. The construction sector remains a primary growth catalyst, with Oxford Economics projecting the global construction market to expand by USD 4.5 trillion between 2020 and 2030, reaching USD 15.2 trillion. This unprecedented growth in construction activities has created substantial demand for advanced insulation solutions that can deliver superior thermal performance while meeting increasingly stringent building codes and environmental regulations. The integration of smart building technologies and sustainable construction practices has further accelerated the adoption of high-performance insulation materials in both residential and commercial applications.

The manufacturing sector's evolution towards energy-efficient insulation operations has emerged as a crucial factor shaping market dynamics. Industrial facilities are increasingly implementing comprehensive energy management systems that incorporate advanced insulation materials to optimize operational efficiency and reduce energy losses. The automotive and aerospace industries, in particular, are driving innovation in lightweight, high-performance insulation materials that can withstand extreme temperatures while contributing to overall vehicle efficiency. These sectors are actively seeking materials that can deliver exceptional thermal performance without compromising on weight or space requirements.

Technological advancements in material science have revolutionized the development of next-generation insulation solutions. Manufacturers are investing heavily in research and development to create innovative products that offer enhanced thermal resistance, improved fire safety, and reduced environmental impact. The emergence of aerogel-based thermal insulation materials, vacuum insulation panels (VIPs), and advanced ceramic fibers has expanded the application possibilities across various industries. These new materials are designed to address specific challenges such as space constraints, extreme temperature conditions, and the need for longer service life.

The market is witnessing a significant shift towards sustainable and eco-friendly insulation solutions, driven by stringent environmental regulations and corporate sustainability goals. Companies are focusing on developing products with a reduced environmental footprint, including materials with higher recycled content and lower embodied carbon. The industry is also experiencing increased collaboration between material manufacturers, construction companies, and research institutions to develop innovative solutions that can meet both performance requirements and sustainability objectives. This collaborative approach has led to the introduction of bio-based building insulation materials and other environmentally responsible alternatives that maintain high-performance characteristics while reducing environmental impact.

High Performance Insulation Materials Market Trends

Growing Usage in the Oil and Gas Industry

High-performance insulation materials have become indispensable in the oil and gas industry, particularly for subsea pipeline applications where they play a crucial role in maintaining operational efficiency. These materials, including aerogel insulation and cryogenic insulation, are extensively used to insulate vessels, tanks, industrial piping, pipe supports, sulfur recovery units, and fired heaters, offering protection in various forms, including thermal insulation for pipework, pumps, manifolds, exhausts, and burners. The materials also provide acoustic insulation for compressors and high-pressure piping systems, along with fire protection for oil rigs, petrochemical plants, and gas exploration and distribution systems.

The increasing oil and gas production activities globally have significantly boosted the demand for these materials. According to the National Bureau of Statistics China, the daily output of crude oil reached nearly 576,000 tons in 2022, with the first two months showing a 4.6% increase in production compared to the previous year. Similarly, in the United States, crude oil production rose significantly, with StatCan reporting a 10.8% increase to 24.4 million cubic meters in recent production figures. The expansion of oil and gas infrastructure, particularly in regions with growing energy demands, has created substantial opportunities for high-performance insulation materials, such as vacuum insulation panels, as they are critical for maintaining temperature stability and preventing energy loss in processing and transportation systems.

Understand The Key Trends Shaping This Market

Download PDF

Rising Awareness Regarding Greenhouse Emissions and Energy Savings

The increasing global focus on reducing greenhouse gas emissions and improving energy efficiency has emerged as a significant driver for high-performance insulation materials. These materials, including ceramic fiber insulation and industrial insulation materials, are being increasingly adopted as eco-friendly insulation solutions, with manufacturers developing innovative products such as soy-based materials, foam, wool, and hemp. While these alternatives may currently be less cost-effective than traditional insulation types, the growing consumer preference for green products is driving increased investment in research and development to optimize production costs and improve accessibility.

Various regions and countries have implemented ambitious targets for reducing greenhouse gas emissions, creating a strong demand for efficient insulation solutions. The European Union's Green Deal Investment Plan aims to ensure a climate-neutral European Union by 2050, with a commitment to reduce greenhouse gas emissions by 55% by 2030 compared to 1990 levels. Similarly, the UK government has set one of the world's most ambitious climate change targets, aiming to cut emissions by 78% by 2035 compared to 1990 levels. In support of these goals, the UK plans to incorporate international aviation and shipping emissions into its carbon budget for the first time, bringing the country more than three-quarters of the way to achieving net-zero by 2050. These environmental commitments are driving the adoption of high-performance insulation materials, including thermal insulation materials and cryogenic insulation, across various industries, particularly in construction and industrial applications.

Segment Analysis: By Material Type

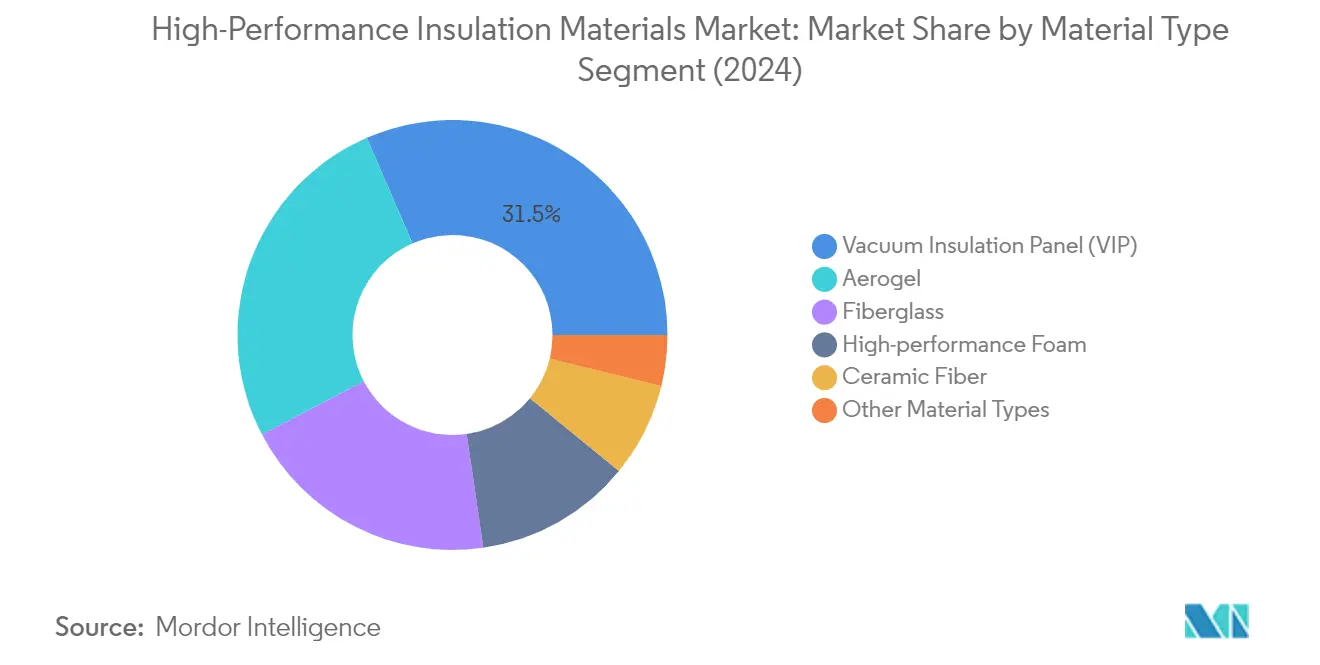

Vacuum Insulation Panel (VIP) Segment in High-Performance Insulation Materials Market

The vacuum insulation panels (VIP) segment dominates the global high-performance insulation materials market, holding approximately 32% of the market share in 2024. VIPs consist of an evacuated, open, porous material placed inside a gas barrier, with main components including an inner core, barrier envelope, opacifiers, and getters or desiccants. These panels are particularly valued in the construction industry for their ability to provide maximum thermal resistance while requiring minimal thickness. VIPs are increasingly being adopted in cooling and freezing devices, logistics, construction, aerospace, and other industrial applications. Their exceptional performance in upgrading insulation during refurbishment makes them ideal for situations where space constraints are a critical factor. The segment's growth is further driven by their superior thermal performance and ability to overcome construction thickness limitations, making them particularly valuable in urban development projects where space optimization is crucial.

Remaining Segments in Material Type Segmentation

The high-performance insulation materials market encompasses several other significant material types, including aerogel insulation, fiberglass, ceramic fiber, and high-performance foam. Aerogel materials are notable for their ultra-lightweight properties and exceptional thermal performance, finding applications in building insulation and industrial processes. Fiberglass continues to maintain a strong presence in the market due to its cost-effectiveness and versatility in both residential and commercial applications. Ceramic fiber insulation materials are particularly valued in high-temperature industrial applications, while high-performance foams offer excellent insulation properties for various construction and automotive applications. Each of these materials brings unique characteristics to the market, such as aerogel's superior thermal resistance, fiberglass's ease of installation, ceramic fiber's high-temperature stability, and high-performance foam's versatility in application.

Segment Analysis: By End-User Industry

Industrial Segment in High-Performance Insulation Materials Market

The industrial segment dominates the high-performance insulation materials market, holding approximately 33% of the market share in 2024. This significant market position is driven by the extensive use of high-performance insulation materials across various industrial applications, including iron and steel manufacturing, aluminum casting and processing, cement manufacturing, and food processing industries. The materials are particularly crucial in industrial furnaces where they help maintain high temperatures efficiently while protecting the external structure. The segment's dominance is further strengthened by the growing focus on energy efficiency in industrial processes, especially in regions like Asia-Pacific where industrial expansion continues at a rapid pace. The materials' ability to provide superior thermal insulation while maintaining structural integrity in extreme conditions makes them indispensable in industrial applications.

Building & Construction Segment in High-Performance Insulation Materials Market

The building and construction segment is projected to experience the fastest growth in the high-performance insulation materials market during the forecast period 2024-2029, with an expected growth rate of approximately 9%. This accelerated growth is primarily driven by the increasing emphasis on energy-efficient buildings and stringent building energy codes across major economies. The segment's growth is further supported by the rising adoption of advanced insulation solutions in both new construction and renovation projects, particularly in regions experiencing rapid urbanization. The materials' superior performance in maintaining optimal indoor temperatures while reducing energy consumption has made them increasingly popular in modern construction projects. Additionally, the growing trend toward green building certifications and sustainable construction practices is expected to further boost the demand for high-performance insulation materials in this segment.

Remaining Segments in End-User Industry

The other significant segments in the high-performance insulation materials market include oil and gas, transportation, power generation, and other end-user industries. The oil and gas sector utilizes these materials extensively in pipeline insulation and processing equipment. The transportation segment, encompassing automotive, aerospace, and marine applications, relies on these materials for thermal management and energy efficiency. The power generation sector employs high-performance insulation materials in thermal power plants, nuclear facilities, and renewable energy installations. Other end-user industries include chemical processing, electronics, and healthcare, where these materials play crucial roles in maintaining specific temperature requirements and ensuring energy efficiency across various applications.

High-Performance Insulation Materials Market Geography Segment Analysis

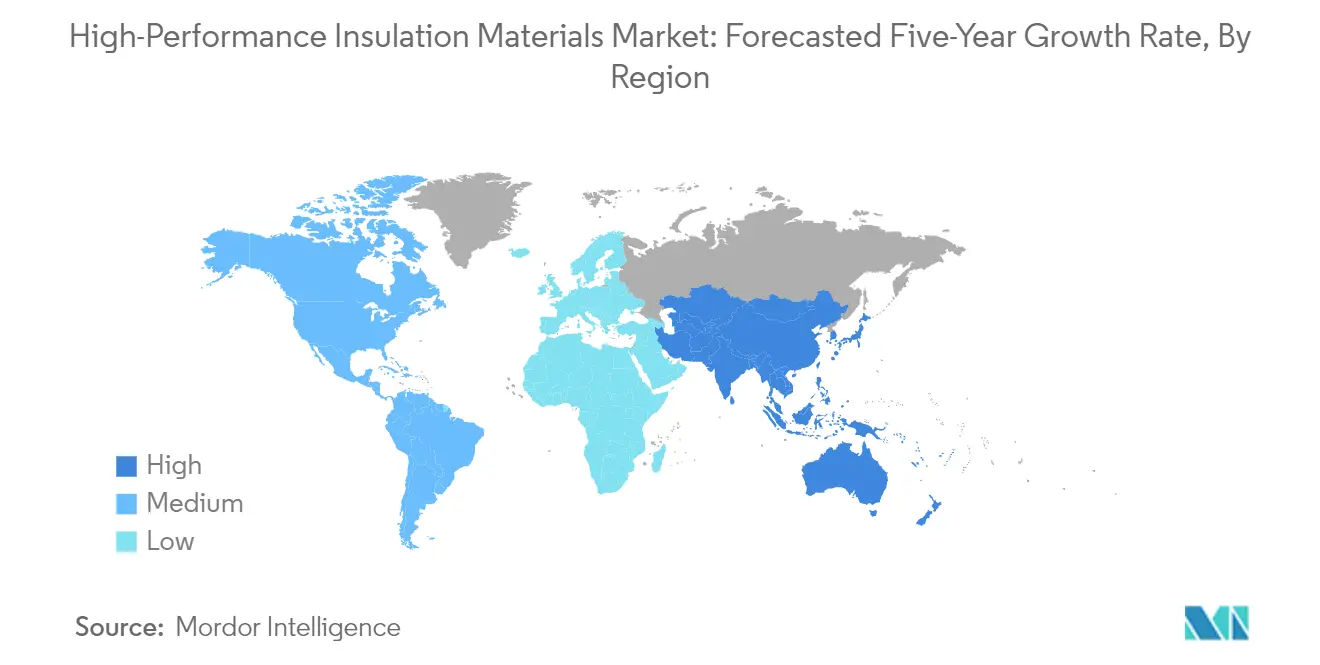

High-Performance Insulation Materials Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for high-performance insulation materials, driven by rapid industrialization and infrastructure development across multiple countries. The region's market is characterized by a strong presence in key countries like China, India, Japan, and South Korea, each contributing significantly to the overall demand. The growth is primarily fueled by expanding industrial sectors, increasing construction activities, and a rising focus on energy efficiency across these nations. The automotive and aerospace sectors in countries like Japan and South Korea are also creating substantial demand for these materials.

High-Performance Insulation Materials Market in China

China dominates the Asia-Pacific high-performance insulation materials market as the largest consumer and producer in the region. With approximately 41% share of the regional market, China's dominance is driven by its massive industrial base and construction sector. The country's robust manufacturing sector, particularly in automotive and electronics, continues to drive demand for these materials. China's focus on energy efficiency in buildings and industrial processes has led to increased adoption of high-performance insulation materials. The country's oil and gas sector expansion, along with growing investments in renewable energy infrastructure, further strengthens the market position.

High-Performance Insulation Materials Market in India

India emerges as the fastest-growing market in the Asia-Pacific region with an expected growth rate of approximately 9% during 2024-2029. The country's rapid industrial development and increasing focus on energy-efficient construction are major growth drivers. India's expanding manufacturing sector, particularly in automotive and electronics, is creating new opportunities for high-performance insulation materials. The government's push towards energy efficiency in buildings and industrial processes, coupled with growing investments in infrastructure development, is fostering market growth. The country's developing aerospace and defense sectors are also contributing to increased demand for these specialized materials.

High-Performance Insulation Materials Market in North America

The North American market for high-performance insulation materials is characterized by advanced technological adoption and stringent energy efficiency regulations. The region, comprising the United States, Canada, and Mexico, demonstrates strong demand across various end-use industries, including oil and gas, construction, and automotive sectors. The market benefits from continuous technological innovations and an increasing focus on sustainable building practices. The presence of major manufacturers and ongoing research and development activities further strengthens the regional market dynamics.

High-Performance Insulation Materials Market in United States

The United States leads the North American market with approximately 76% of the regional market share. The country's leadership position is supported by its extensive industrial infrastructure and advanced manufacturing capabilities. The robust aerospace industry, coupled with significant investments in energy-efficient building solutions, drives the demand for high-performance insulation materials. The country's focus on reducing energy consumption in industrial processes and buildings continues to create substantial market opportunities.

High-Performance Insulation Materials Market in United States

The United States also leads in terms of growth rate in North America, with an expected growth rate of approximately 8% during 2024-2029. The growth is driven by the increasing adoption of advanced insulation solutions in the construction sector and expanding industrial applications. The country's strong focus on energy efficiency and environmental regulations continues to boost market growth. The expanding oil and gas sector, coupled with growing investments in renewable energy infrastructure, further supports market expansion.

High-Performance Insulation Materials Market in Europe

The European market for high-performance insulation materials is characterized by strong environmental regulations and high adoption of energy-efficient solutions. The region, encompassing Germany, the United Kingdom, Italy, and France, shows consistent demand across various industrial sectors. The market is driven by strict building energy codes and a growing emphasis on sustainable industrial practices. The presence of established manufacturers and continuous technological innovations further strengthens the market dynamics.

High-Performance Insulation Materials Market in Germany

Germany maintains its position as the largest market for high-performance insulation materials in Europe. The country's leadership is driven by its strong industrial base, particularly in the automotive and manufacturing sectors. Germany's stringent energy efficiency regulations and focus on sustainable building practices continue to drive market growth. The country's robust chemical industry and growing investments in renewable energy infrastructure further support market expansion.

High-Performance Insulation Materials Market in Germany

Germany also leads the growth trajectory in Europe's high-performance insulation materials market. The country's market expansion is supported by increasing adoption in industrial applications and a growing focus on energy-efficient buildings. The automotive sector's transformation towards electric vehicles creates new opportunities for high-performance insulation materials. The country's commitment to energy efficiency and environmental protection continues to drive innovation in insulation technologies.

High-Performance Insulation Materials Market in South America

The South American market for high-performance insulation materials demonstrates growing potential, with Brazil and Argentina as key markets. The region's market is driven by expanding industrial activities and an increasing focus on energy efficiency. Brazil emerges as both the largest and fastest-growing market in the region, supported by its robust manufacturing sector and growing construction activities. The region's oil and gas sector development and increasing industrial investments continue to create new opportunities for market growth.

High-Performance Insulation Materials Market in Middle East & Africa

The Middle East & Africa region shows promising growth in the high-performance insulation materials market, with Saudi Arabia and South Africa as significant markets. The region's market is primarily driven by the oil and gas sector and growing industrial activities. Saudi Arabia represents the largest market in the region, while also showing the fastest growth rate, supported by its extensive petrochemical industry and increasing construction activities. The region's focus on energy efficiency and growing industrial infrastructure continues to create new opportunities for market expansion.

Get Analysis on Important Geographic Markets

Download PDF

High Performance Insulation Materials Industry Overview

Top Companies in High-Performance Insulation Materials Market

The high-performance insulation materials market is led by established players like Owens Corning, Knauf Gips KG, Rockwool, Johns Manville, Unifrax, and Armacell, who have demonstrated a strong market presence through continuous innovation and strategic expansion. Companies are focusing on developing sustainable and energy-efficient insulation solutions while investing in research and development to improve product performance and meet evolving industry requirements. The market has witnessed significant technological advancements in aerogel-based solutions, vacuum insulation panels, and ceramic fiber materials. Strategic acquisitions and partnerships have become crucial for expanding geographical presence and enhancing product portfolios, particularly in emerging markets. Manufacturing facilities are being modernized to incorporate advanced production techniques and improve operational efficiency, while distribution networks are being strengthened to ensure better market penetration and customer service.

Fragmented Market with Strong Regional Players

The high-performance insulation materials market exhibits a fragmented structure with a mix of global conglomerates and specialized regional manufacturers. Major players have established strong manufacturing and distribution networks across multiple regions, while local players maintain significant market share in their respective territories through specialized product offerings and strong customer relationships. The market has witnessed considerable consolidation through strategic acquisitions, particularly in Asia-Pacific and Europe, as companies seek to strengthen their market position and expand their technological capabilities. Companies are increasingly focusing on vertical integration to maintain better control over raw material supply and end-product quality.

The competitive landscape is characterized by intense rivalry among established players and new entrants, with companies differentiating themselves through product innovation, pricing strategies, and service capabilities. Market leaders are leveraging their extensive research and development capabilities to introduce advanced insulation materials, while regional players are focusing on customized solutions for specific applications and industries. The industry has seen a trend towards strategic partnerships between material manufacturers and end-user industries, particularly in the construction and industrial sectors, to develop application-specific solutions and ensure steady demand.

Innovation and Sustainability Drive Future Growth

Success in the high-performance insulation materials market increasingly depends on companies' ability to develop sustainable products while maintaining cost competitiveness. Market leaders are investing in eco-friendly manufacturing processes and developing products with reduced environmental impact to meet stringent regulatory requirements and changing customer preferences. Companies are also focusing on developing integrated solutions that combine multiple insulation technologies to provide enhanced performance and value proposition. The ability to provide technical support, application expertise, and after-sales service has become crucial for maintaining market position and customer loyalty.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized products and applications. Companies need to focus on developing strong relationships with end-users in high-growth sectors such as industrial manufacturing, construction, and oil and gas. The market presents opportunities for companies that can offer innovative solutions for emerging applications while maintaining competitive pricing. Building strong distribution networks and establishing strategic partnerships with local players in key markets will be crucial for sustainable growth. Additionally, companies need to maintain flexibility in their operations to respond quickly to changing market conditions and customer requirements. The demand for thermal insulation materials and industrial insulation materials is expected to rise, driven by the need for energy efficiency and regulatory compliance.

High Performance Insulation Materials Market Leaders

-

Owens Corning

-

Knauf Gips KG

-

Rockwool

-

Johns Manville

-

Unifrax

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

High Performance Insulation Materials Market News

- In Jan 2022, Armacell acquired the engineering business of SpiderPlus & Co. Ltd. Based in Tokyo, Japan, the engineering business of SpiderPlus & Co. Ltd manufactures and supplies thermal insulation solutions for piping and ductwork.

- In Jun 2021, BASF and Shanghai Harvest Insulation Engineering Co. Ltd (Harvest) signed a Joint Development Agreement (JDA) to create prefabricated cryogenic pipes using BASF's Elastopor Cryo polyurethane rigid foam technology.

High Performance Insulation Materials Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Usage in the Oil and Gas Industry

- 4.1.2 Rising Awareness Regarding Greenhouse Emissions and Energy Savings

-

4.2 Restraints

- 4.2.1 High Set-up and Maintenance Costs and Relatively Low Service Life

- 4.2.2 High Flammability with Insulated Materials and Foam Products that Contain CFC

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION

-

5.1 Material Type

- 5.1.1 Aerogel

- 5.1.2 Vacuum Insulation Panel (VIP)

- 5.1.3 Fiberglass

- 5.1.4 Ceramic Fiber

- 5.1.5 High-performance Foam

- 5.1.6 Other Material Types

-

5.2 End-user Industry

- 5.2.1 Oil and Gas

- 5.2.2 Industrial

- 5.2.3 Building and Construction

- 5.2.4 Transportation

- 5.2.5 Power Generation

- 5.2.6 Other End-user Industries

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.2.4 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Aerogel Technologies LLC

- 6.4.3 Armacell

- 6.4.4 Aspen Aerogels Inc.

- 6.4.5 BASF SE

- 6.4.6 Cabot Corporation

- 6.4.7 IBIDEN

- 6.4.8 Isolite Insulating Products Co. Ltd

- 6.4.9 Johns Manville

- 6.4.10 Knauf Gips KG

- 6.4.11 Luyang Energy-Saving Materials Co. Ltd

- 6.4.12 Morgan Advanced Materials

- 6.4.13 Owens Corning

- 6.4.14 Panasonic Corporation

- 6.4.15 PAR Group

- 6.4.16 Rath Group

- 6.4.17 ROCKWOOL Group

- 6.4.18 Saint-Gobain

- 6.4.19 Unifrax

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Investments in Infrastructural Activities in Asia-Pacific

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

High Performance Insulation Materials Industry Segmentation

High-Performance Insulation Materials help reduce heat transfer (i.e., the transfer of thermal energy between objects of differing temperatures) between objects in thermal contact or the range of radiative influence. Thermal insulation can be achieved with specially engineered methods or processes and suitable object shapes and materials. The High-Performance Insulation Materials Market is segmented by Material Type (Aerogel, Vacuum Insulation Panel, Fiberglass, Ceramic Fiber, High-performance Foam, and Other Material Types), End-user Industry (Oil and Gas, Industrial, Building and Construction, Transportation, Power Generation, and Other End-user Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report also covers the market sizes and forecasts for High-Performance Insulation Materials Market in 15 countries across the major region. For each segment, the market sizing and forecasts have been done based on value (USD million).

| Material Type | Aerogel | ||

| Vacuum Insulation Panel (VIP) | |||

| Fiberglass | |||

| Ceramic Fiber | |||

| High-performance Foam | |||

| Other Material Types | |||

| End-user Industry | Oil and Gas | ||

| Industrial | |||

| Building and Construction | |||

| Transportation | |||

| Power Generation | |||

| Other End-user Industries | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

High Performance Insulation Materials Market Research FAQs

What is the current High-Performance Insulation Materials Market size?

The High-Performance Insulation Materials Market is projected to register a CAGR of 7.61% during the forecast period (2025-2030)

Who are the key players in High-Performance Insulation Materials Market?

Owens Corning, Knauf Gips KG, Rockwool, Johns Manville and Unifrax are the major companies operating in the High-Performance Insulation Materials Market.

Which is the fastest growing region in High-Performance Insulation Materials Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in High-Performance Insulation Materials Market?

In 2025, the North America accounts for the largest market share in High-Performance Insulation Materials Market.

What years does this High-Performance Insulation Materials Market cover?

The report covers the High-Performance Insulation Materials Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the High-Performance Insulation Materials Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

High-Performance Insulation Materials Market Research

Mordor Intelligence provides a comprehensive analysis of the high performance insulation materials market. We leverage our extensive expertise in researching advanced insulation materials. Our detailed report examines key segments, including aerogel insulation, ceramic fiber insulation, vacuum insulation panels, and microporous insulation. These insights are crucial across applications ranging from building insulation materials to aerospace insulation materials. The analysis covers thermal insulation materials featuring low thermal conductivity materials properties. It addresses both industrial insulation materials and cryogenic insulation applications.

Stakeholders gain valuable insights through our downloadable report PDF. It covers emerging technologies like nano insulation materials and super insulation materials. The report examines energy efficient insulation solutions and reflective insulation materials. It also provides a detailed analysis of the aerogel insulation market, vacuum insulation panels market, and cryogenic insulation market. Our comprehensive coverage supports strategic decision-making across the building insulation materials market, microporous insulation market, and cryogenic insulation industry. This offers actionable intelligence for industry participants seeking to optimize their market positioning and investment strategies.