| Study Period | 2021 - 2030 |

| Market Size (2025) | USD 4.73 Billion |

| Market Size (2030) | USD 6.24 Billion |

| CAGR (2025 - 2030) | 5.67 % |

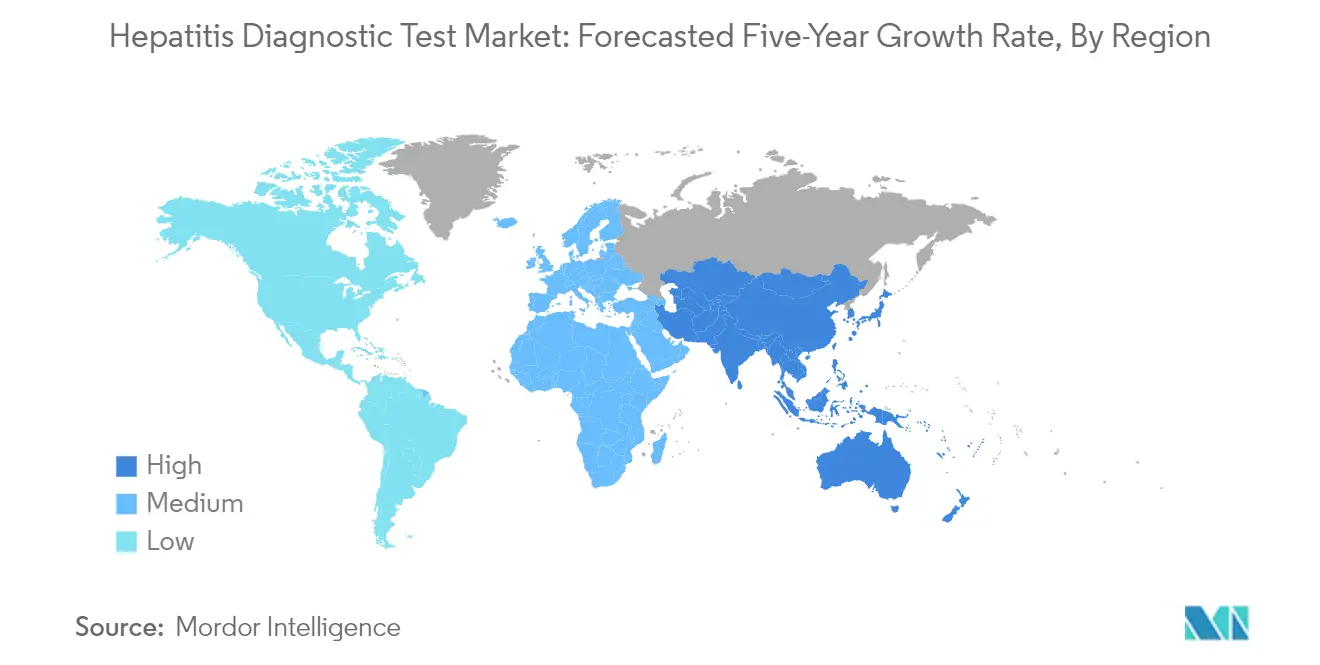

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

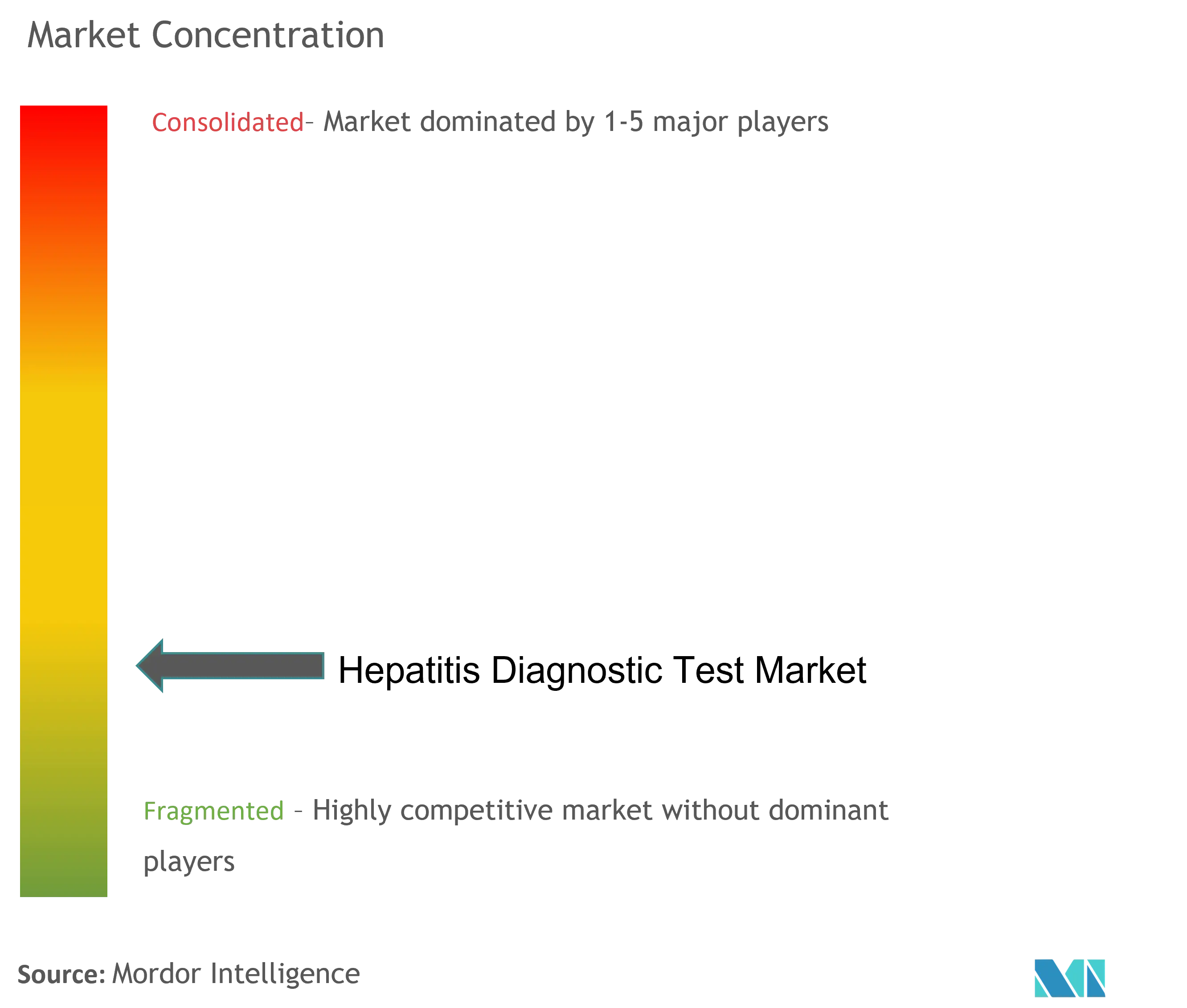

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Hepatitis Diagnostic Test Market Analysis

The Global Hepatitis Diagnostic Test Market size is estimated at USD 4.73 billion in 2025, and is expected to reach USD 6.24 billion by 2030, at a CAGR of 5.67% during the forecast period (2025-2030).

The hepatitis diagnostic testing landscape is experiencing significant transformation driven by technological innovations and changing healthcare delivery models. Point-of-care testing has emerged as a game-changing development, with recent studies demonstrating remarkable accuracy levels—achieving 100% sensitivity and 97% specificity in HCV viral load RNA testing compared to traditional laboratory-based methods. This shift towards rapid, accessible hepatitis testing is reshaping how healthcare providers approach hepatitis screening and monitoring, particularly in resource-limited settings and remote areas where traditional laboratory infrastructure may be limited.

The integration of artificial intelligence and digital health solutions is revolutionizing hepatitis diagnostic processes, enabling more precise and efficient testing. In February 2024, researchers at Chula made a breakthrough by developing an innovative wireless hepatitis B virus test kit, designed specifically for smaller hospitals and public health centers to conduct independent screening without relying on specialized diagnostic laboratories. This advancement represents a significant step toward democratizing access to viral hepatitis testing and illustrates the industry's movement toward more autonomous, decentralized diagnostic solutions.

The market is witnessing a notable shift toward multi-disease testing approaches, where diagnostic platforms are being developed to simultaneously screen for multiple infectious diseases, including HIV, tuberculosis, and various forms of hepatitis. This trend reflects healthcare providers' growing preference for comprehensive screening solutions that maximize efficiency and resource utilization while improving patient convenience. The emergence of integrated testing platforms is particularly significant in public health settings, where screening programs often need to address multiple health concerns simultaneously.

According to the World Health Organization's latest estimates, approximately 58 million people globally suffer from chronic hepatitis C virus infection, with about 1.5 million new cases occurring annually. This substantial disease burden has prompted increased investment in diagnostic innovation, particularly in high-risk populations where prevalence rates vary significantly—for instance, in Germany, rates range from 9.6% among homosexual men to 68.0% among individuals who inject drugs. These statistics underscore the critical need for targeted diagnostic strategies and have spurred the development of specialized hepatitis diagnostic test solutions for different population segments.

Hepatitis Diagnostic Test Market Trends

Growing Burden of Hepatitis

The escalating global burden of hepatitis continues to be a critical driver for hepatitis testing demand. According to the World Health Organization's 2023 Factsheet, approximately 354 million people worldwide are living with chronic hepatitis infections, with a significant portion remaining undiagnosed. The severity of this burden is particularly evident in regions such as Africa, where the WHO African region reported an estimated 82.3 million individuals living with chronic HBV infection as of July 2023. This substantial prevalence underscores the urgent need for comprehensive hepatitis blood test infrastructure and diagnostic capabilities to address this growing public health challenge.

The impact of this growing burden is further illustrated by recent epidemiological data from various regions. In the United Kingdom, as of March 2024, approximately 206,000 individuals (0.45% of the population) are living with chronic hepatitis B infection, while around 70,649 people (0.15% of the population) are affected by chronic hepatitis C infection. The European Center for Disease Prevention and Control (ECDC) highlighted in July 2023 that approximately 3 million new hepatitis B and C infections are reported annually worldwide, with an estimated 6 million individuals living with chronic hepatitis B and C infections in the European Union and European Economic Area alone. These statistics emphasize the critical need for enhanced hepatitis testing capabilities and infrastructure.

Understand The Key Trends Shaping This Market

Download PDF

Introduction of Molecular Diagnostics for the Diagnosis of Hepatitis

The advancement and introduction of molecular diagnostic technologies have revolutionized hepatitis testing, offering unprecedented precision and sensitivity in detecting viral infections. These molecular biology-based assays provide highly specific detection of viral nucleic acids, enabling accurate assessment of infection status, prognosis, and treatment response. Notably, Nucleic Acid Tests (NAT) have emerged as the gold standard for hepatitis diagnosis, becoming positive as early as 1-2 weeks after initial infection, even before seroconversion, thereby facilitating early detection and intervention.

Recent technological innovations and product launches have further enhanced the molecular diagnostics landscape. In November 2023, Roche introduced a new immunoassay designed to identify the hepatitis Be antigen (HBeAg), marking a significant advancement in hepatitis diagnosis. Similarly, Neglx Biotech Labs' launch of real-time PCR-based kits for infectious diseases, including hepatitis B and C, has streamlined testing processes for diagnostic centers and hospitals. These innovative assays offer advanced capabilities for precise and efficient detection of viral pathogens, revolutionizing the diagnostic landscape and enhancing patient care through improved accuracy and efficiency.

Increasing Awareness Regarding the Disease

The growing awareness about hepatitis, driven by global health initiatives and targeted campaigns, has become a significant catalyst for hepatitis testing demand. In July 2023, Egypt's '100 Healthy Days' healthcare campaign, targeting 105 million people nationwide, provided over 4.77 million services since its inception, including early detection of Hepatitis C. This comprehensive campaign exemplifies the impact of proactive health promotion efforts in reaching large populations and facilitating access to diagnostic services. Additionally, partnerships between organizations to organize awareness campaigns have significantly influenced testing adoption, with initiatives like the National Hepatitis C Finding 50,000 Project leveraging collaborative efforts to engage individuals living with hepatitis C nationwide.

The implementation of national screening programs and awareness initiatives has further strengthened the drive for hepatitis testing. In Uganda, through annual investments of approximately USD 3 million and collaboration with national stakeholders, the country initiated an extensive, complimentary hepatitis B screening program in 2023. This initiative was complemented by widespread community mobilization efforts and actions to raise awareness about the disease. The World Health Organization's support of such programs, coupled with its advocacy for integrated screening and treatment approaches for individuals living with HIV, has emphasized the importance of comprehensive testing strategies. WHO's recommendation for testing viral hepatitis B and C in individuals with HIV has led to enhanced screening protocols and increased awareness about the necessity of early detection and intervention.

Segment Analysis: By Test Type

Blood Tests Segment in Hepatitis Diagnostic Test Market

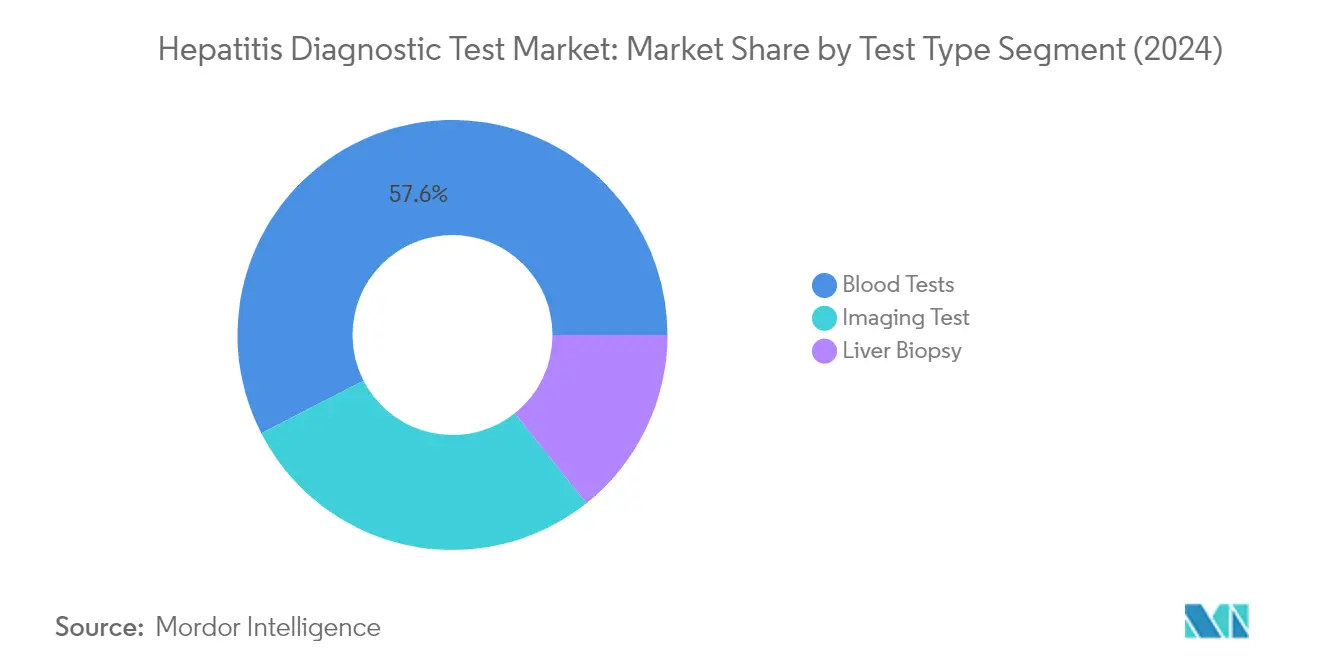

The hepatitis blood test segment dominates the hepatitis diagnostic test market, commanding approximately 58% of the market share in 2024. This segment's prominence is driven by several factors, including increasing awareness of hepatitis and the growing availability of cost-effective diagnostic tests. Hepatitis blood tests encompass various crucial testing methodologies such as liver function tests, immunoassays, and nucleic acid tests, each playing a vital role in hepatitis diagnosis and monitoring. The segment is also experiencing the fastest growth trajectory, with a projected growth rate of around 6% from 2024 to 2029, primarily attributed to the significant sensitivity of NAT against hepatitis, growing demand for POC NAT tests in point-of-care centers, and increasing demand for rapid detection. Recent technological advancements and product launches have further strengthened this segment's position, particularly in molecular diagnostics and automated testing platforms.

Remaining Segments in Hepatitis Diagnostic Test Market

The imaging test and liver biopsy segments complete the hepatitis diagnostic test market landscape, each serving distinct diagnostic purposes. Imaging tests, including ultrasound, computed tomography (CT) scans, and magnetic resonance imaging (MRI), provide crucial visual assessments of liver condition and help detect abnormalities such as liver enlargement, scarring, or tumors. The advancement in imaging technologies, particularly in ultrasound and elastography techniques, has enhanced the precision of liver assessment. Meanwhile, liver biopsy remains the gold standard for definitive diagnosis, offering detailed information about liver pathology and the extent of damage caused by hepatitis. The integration of these diagnostic approaches with hepatitis testing provides a comprehensive assessment framework, enabling healthcare providers to make more informed decisions about patient care and treatment strategies.

Global Hepatitis Diagnostic Test Market Geography Segment Analysis

Hepatitis Diagnostic Test Market in North America

North America represents a dominant force in the global hepatitis diagnostic test market, driven by sophisticated healthcare infrastructure and extensive hepatitis screening programs. The region's market dynamics are shaped by the United States, Canada, and Mexico, with each country contributing uniquely through their respective healthcare systems and diagnostic capabilities. The region's strength lies in its advanced diagnostic technologies, comprehensive insurance coverage, and strong emphasis on preventive healthcare measures for hepatitis testing and monitoring.

Hepatitis Diagnostic Test Market in United States

The United States leads the North American market with approximately 88% share in 2024, establishing itself as the region's largest market. The country's market dominance is attributed to its sophisticated healthcare infrastructure, extensive network of diagnostic laboratories, and comprehensive hepatitis screening programs. The Centers for Disease Control and Prevention's guidelines for hepatitis screening, particularly their recommendations for universal adult screening for hepatitis B using the triple panel test, have significantly influenced market growth. The country's focus on early detection and treatment, coupled with increasing awareness campaigns and strategic initiatives by key market players, continues to drive market expansion.

Hepatitis Diagnostic Test Market Growth Trajectory in United States

The United States also emerges as the fastest-growing market in North America, with a projected CAGR of approximately 6% from 2024 to 2029. This growth is fueled by increasing adoption of advanced hepatitis diagnostic technologies, expanding screening programs, and rising awareness about early detection. The country's robust research and development activities in diagnostic technologies, coupled with strategic collaborations between diagnostic companies and government agencies, are creating new opportunities for market expansion. The implementation of comprehensive screening protocols and the integration of innovative hepatitis testing solutions continue to drive market growth.

Hepatitis Diagnostic Test Market in Europe

The European market for hepatitis diagnostic tests demonstrates strong growth potential, supported by well-established healthcare systems and comprehensive disease surveillance programs. The region encompasses key markets including Germany, the United Kingdom, France, Italy, and Spain, each contributing significantly to the overall market landscape. The European market benefits from strong governmental support for hepatitis elimination programs, advanced healthcare infrastructure, and increasing awareness about early diagnosis and treatment.

Hepatitis Diagnostic Test Market in Germany

Germany emerges as the largest market in Europe, commanding approximately 21% of the regional market share in 2024. The country's market leadership is attributed to its proactive approach towards preventative healthcare and robust healthcare infrastructure. Germany's implementation of the 'BIS 2030' strategy to combat hepatitis infections, along with initiatives like the 'Check-Up 35' program, demonstrates its commitment to comprehensive hepatitis diagnostic screening and diagnosis. The country's focus on expanding screening programs and implementing innovative diagnostic solutions continues to strengthen its market position.

Hepatitis Diagnostic Test Market Growth Trajectory in Germany

Germany also leads the European market in terms of growth rate, with an expected CAGR of approximately 7% from 2024 to 2029. This robust growth is driven by the country's strong emphasis on technological advancement in diagnostic techniques and expanding screening initiatives. The implementation of comprehensive hepatitis elimination strategies, coupled with increasing awareness about early detection and diagnosis, continues to fuel market expansion. Germany's commitment to achieving WHO's elimination targets through enhanced hepatitis diagnostic test capabilities and screening programs supports this growth trajectory.

Hepatitis Diagnostic Test Market in Asia-Pacific

The Asia-Pacific region represents a significant market for hepatitis diagnostic tests, characterized by diverse healthcare systems and varying levels of diagnostic capabilities across countries. The market encompasses major economies including China, Japan, India, Australia, and South Korea, each contributing uniquely to the regional landscape. The region's market is driven by increasing healthcare expenditure, growing awareness about hepatitis testing, and improving healthcare infrastructure across various countries.

Hepatitis Diagnostic Test Market in China

China stands as the largest market in the Asia-Pacific region, demonstrating strong market presence through its extensive healthcare network and large patient population. The country's market leadership is supported by its robust healthcare infrastructure, increasing government initiatives for hepatitis control, and growing adoption of advanced hepatitis diagnostic test technologies. China's focus on expanding access to diagnostic services and implementing comprehensive screening programs continues to strengthen its position in the regional market.

Hepatitis Diagnostic Test Market Growth Trajectory in India

India emerges as the fastest-growing market in the Asia-Pacific region, showing remarkable growth potential in the hepatitis diagnostic test market. The country's growth is driven by increasing healthcare awareness, improving healthcare infrastructure, and growing government initiatives for hepatitis control. The expansion of diagnostic facilities, coupled with rising adoption of advanced testing technologies and increasing focus on early detection, continues to fuel market growth in India.

Hepatitis Diagnostic Test Market in Middle East & Africa

The Middle East & Africa region presents unique opportunities in the hepatitis diagnostic test market, with varying healthcare capabilities across different countries. The market encompasses the GCC countries and South Africa as key contributors, with each region demonstrating distinct market characteristics. The GCC emerges as the largest market in the region, while South Africa shows promising growth potential. The region's market is characterized by increasing healthcare investments, growing awareness about hepatitis diagnosis, and improving healthcare infrastructure across various countries.

Hepatitis Diagnostic Test Market in South America

The South American market for hepatitis diagnostic tests demonstrates steady growth potential, with Brazil and Argentina serving as key markets in the region. Brazil emerges as the largest market in the region, while also showing the fastest growth potential. The region's market is driven by increasing healthcare awareness, improving diagnostic infrastructure, and growing government initiatives for hepatitis control. The implementation of comprehensive screening programs and rising adoption of advanced diagnostic technologies continue to shape the market landscape in South America.

Get Analysis on Important Geographic Markets

Download PDF

Hepatitis Diagnostic Test Industry Overview

Top Companies in Hepatitis Diagnostic Test Market

The hepatitis diagnostic test market features prominent players like Abbott, Danaher Corporation, BioMérieux SA, Bio-Rad Laboratories, and F. Hoffmann-La Roche AG leading the innovation landscape. These companies are actively investing in research and development to introduce advanced diagnostic solutions, particularly focusing on point-of-care testing and rapid diagnostic capabilities. The competitive dynamics are characterized by strategic collaborations with healthcare providers, expansion of distribution networks, and continuous product portfolio enhancement through both internal development and acquisitions. Companies are increasingly emphasizing the development of multiplex testing platforms that can detect multiple hepatitis variants simultaneously, while also focusing on improving test sensitivity and reducing turnaround times. Market leaders are also investing in expanding their geographical presence, particularly in emerging markets, while simultaneously strengthening their position in established markets through enhanced service offerings and technical support.

Consolidated Market with Strong Regional Players

The hepatitis diagnostic test market exhibits a moderately consolidated structure, dominated by large multinational corporations with extensive research capabilities and global distribution networks. These major players leverage their broad product portfolios, established brand recognition, and strong financial resources to maintain their market positions. The market also features regional players who have carved out significant niches in specific geographical areas by offering customized solutions and maintaining strong relationships with local healthcare providers. The competitive landscape is characterized by ongoing merger and acquisition activities, as larger companies seek to acquire innovative technologies and expand their geographical footprint.

The market demonstrates varying levels of competition across different regions, with developed markets showing higher consolidation and emerging markets featuring more fragmented competitive dynamics. Companies are increasingly focusing on strategic partnerships with local distributors and healthcare facilities to enhance their market penetration. The competitive environment is further shaped by the presence of specialized diagnostic companies that focus exclusively on infectious disease diagnostic testing, including hepatitis, competing against diversified healthcare conglomerates that offer broader diagnostic solutions. These specialized players often drive innovation in specific testing technologies while larger companies provide comprehensive testing platforms.

Innovation and Accessibility Drive Market Success

Success in the hepatitis diagnostic test market increasingly depends on companies' ability to develop cost-effective, accurate, and user-friendly testing solutions while maintaining high sensitivity and specificity standards. Market leaders are focusing on expanding their test menu to include comprehensive hepatitis panels, while also investing in automation and digital connectivity features to enhance laboratory efficiency. Companies are also emphasizing the development of point-of-care testing solutions to address the growing demand for rapid results and decentralized testing capabilities. The ability to provide integrated solutions that combine diagnostic testing with data management and interpretation services is becoming increasingly important for maintaining competitive advantage.

Future success in this market will require companies to address several critical factors, including the need for increased hepatitis testing accessibility in resource-limited settings and the ability to adapt to evolving regulatory requirements. Companies must balance the development of innovative technologies with cost considerations to ensure broad market adoption. The competitive landscape is likely to be influenced by an increasing focus on preventive healthcare and screening programs, requiring companies to develop solutions that can support large-scale testing initiatives. Additionally, the ability to provide comprehensive support services, including training, maintenance, and technical assistance, will become increasingly important for maintaining market position and customer loyalty.

Hepatitis Diagnostic Test Market Leaders

-

Abbott Laboratories

-

Bio-Rad Laboratories Inc

-

F. Hoffmann-La Roche AG

-

BioMerieux SA

-

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Hepatitis Diagnostic Test Market News

- September 2022: Gilead Sciences, Inc. joined a public-private initiative with the Partnership for Health Advancement in Vietnam (HAIVN), a collaboration between Brigham and Women's Hospital, Harvard Medical School, and Beth Israel Deaconess Medical Center. The multi-year initiative is aimed at a phased approach to help address barriers that limit viral hepatitis diagnosis and care at primary healthcare institutions in Vietnam and the Philippines, two countries with high burdens of hepatitis B and C.

- July 2022: Roche launched Elecsys HCV Duo immunoassay. Elecsys HCV Duo is one of the first commercially available immunoassays that allows the simultaneous and independent determination of the hepatitis C virus (HCV) antigen and antibody status.

Hepatitis Diagnostic Test Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Growing Burden of Hepatitis

- 4.2.2 Introduction of Molecular Diagnostics for the Diagnosis of Hepatitis

- 4.2.3 Increasing Awareness Regarding The Disease

-

4.3 Market Restraints

- 4.3.1 Limited Facilities or Services For Hepatitis Testing

- 4.3.2 Limited Access to Reliable and Low-Cost HBV and HCV Diagnostics

-

4.4 Porter Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

-

5.1 By Test Type

- 5.1.1 Blood Tests

- 5.1.1.1 Liver Function Tests

- 5.1.1.2 Immunoassays

- 5.1.1.3 Nucleic Acid Tests

- 5.1.2 Imaging Test

- 5.1.3 Liver Biopsy

-

5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Danaher Corporation (Beckman Coulter Inc)

- 6.1.3 BioMerieux SA

- 6.1.4 Bio-Rad Laboratories Inc

- 6.1.5 Diasorin S.p.A

- 6.1.6 F. Hoffmann-La Roche AG

- 6.1.7 Hologic Inc

- 6.1.8 VWR International, LLC

- 6.1.9 Qaigen Inc

- 6.1.10 Grifols SA

- 6.1.11 Sysmex Corporation

- 6.1.12 Siemens Healthineers

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Hepatitis Diagnostic Test Industry Segmentation

As per the scope of the report, the term hepatitis broadly means inflammation of the liver. Heavy alcohol use, some medications, toxins, and certain medical conditions can cause hepatitis. However, hepatitis is often caused due to viral infection. The most common types of viral hepatitis are hepatitis A, hepatitis B, and hepatitis C. The Hepatitis Diagnostic Test Market is segmented by Test Type, (Blood Tests (Liver Function Tests, Immunoassays and Nucleic Acid Tests), Imaging Tests, and Liver Biopsy) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Test Type | Blood Tests | Liver Function Tests | |

| Immunoassays | |||

| Nucleic Acid Tests | |||

| Imaging Test | |||

| Liver Biopsy | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Hepatitis Diagnostic Test Market Research FAQs

How big is the Global Hepatitis Diagnostic Test Market?

The Global Hepatitis Diagnostic Test Market size is expected to reach USD 4.73 billion in 2025 and grow at a CAGR of 5.67% to reach USD 6.24 billion by 2030.

What is the current Global Hepatitis Diagnostic Test Market size?

In 2025, the Global Hepatitis Diagnostic Test Market size is expected to reach USD 4.73 billion.

Who are the key players in Global Hepatitis Diagnostic Test Market?

Abbott Laboratories, Bio-Rad Laboratories Inc, F. Hoffmann-La Roche AG, BioMerieux SA and Siemens Healthineers are the major companies operating in the Global Hepatitis Diagnostic Test Market.

Which is the fastest growing region in Global Hepatitis Diagnostic Test Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Global Hepatitis Diagnostic Test Market?

In 2025, the North America accounts for the largest market share in Global Hepatitis Diagnostic Test Market.

What years does this Global Hepatitis Diagnostic Test Market cover, and what was the market size in 2024?

In 2024, the Global Hepatitis Diagnostic Test Market size was estimated at USD 4.46 billion. The report covers the Global Hepatitis Diagnostic Test Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Global Hepatitis Diagnostic Test Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Global Hepatitis Diagnostic Test Market Research

Mordor Intelligence provides comprehensive insights into the hepatitis diagnostic test market. We leverage our extensive experience in infectious disease diagnostic research. Our latest report, available as a downloadable PDF, offers a detailed analysis of hepatitis testing methodologies. This includes viral hepatitis testing protocols and emerging hepatitis screening technologies. The research covers both traditional hepatitis blood test procedures and innovative hepatitis diagnostic solutions, giving stakeholders a complete market perspective.

The report explores various testing methodologies, such as hepatitis antibody test procedures, hepatitis antigen test technologies, and hepatitis rapid test solutions. Our analysis benefits healthcare providers, diagnostic manufacturers, and investors. It provides crucial insights into hepatitis detection test developments and hepatitis diagnostic test innovations. The comprehensive coverage of the infectious disease diagnostic market includes a detailed examination of testing protocols, regulatory frameworks, and technological advancements. This enables stakeholders to make informed decisions based on robust market intelligence.