Healthcare Regulatory Affairs Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

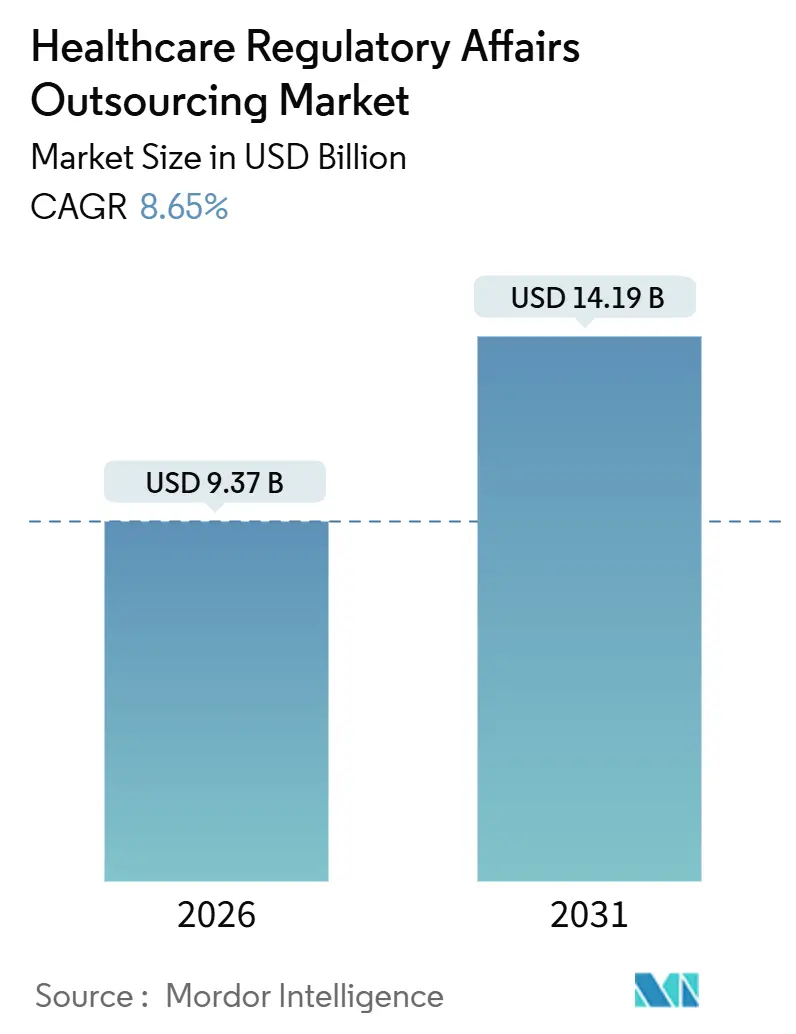

| Market Size (2026) | USD 9.37 Billion |

| Market Size (2031) | USD 14.19 Billion |

| Growth Rate (2026 - 2031) | 8.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Regulatory Affairs Outsourcing Market Analysis by Mordor Intelligence

The Healthcare Regulatory Affairs Outsourcing Market size is estimated at USD 9.37 billion in 2026, and is expected to reach USD 14.19 billion by 2031, at a CAGR of 8.65% during the forecast period (2026-2031).

The growth path mirrors rising demand from virtual biotechs that lack in-house regulatory capabilities, the migration of high-volume dossier preparation to specialized vendors, and ever-stricter global submission standards. Sponsors continue to prioritize speed-to-market over document production volume, a shift that explains why product registration and clinical trial applications outpace all other services. At the same time, regulators require continuous real-world evidence, turning post-approval activities into a multiyear revenue stream for outsourcing providers. North America remains the anchor of revenue, yet the rise of multilingual hubs in India and China is reshaping the competitive landscape. Vendors that integrate AI into submission workflows compress cycle times, secure larger work packages, and differentiate themselves on value rather than labor cost.

Key Report Takeaways

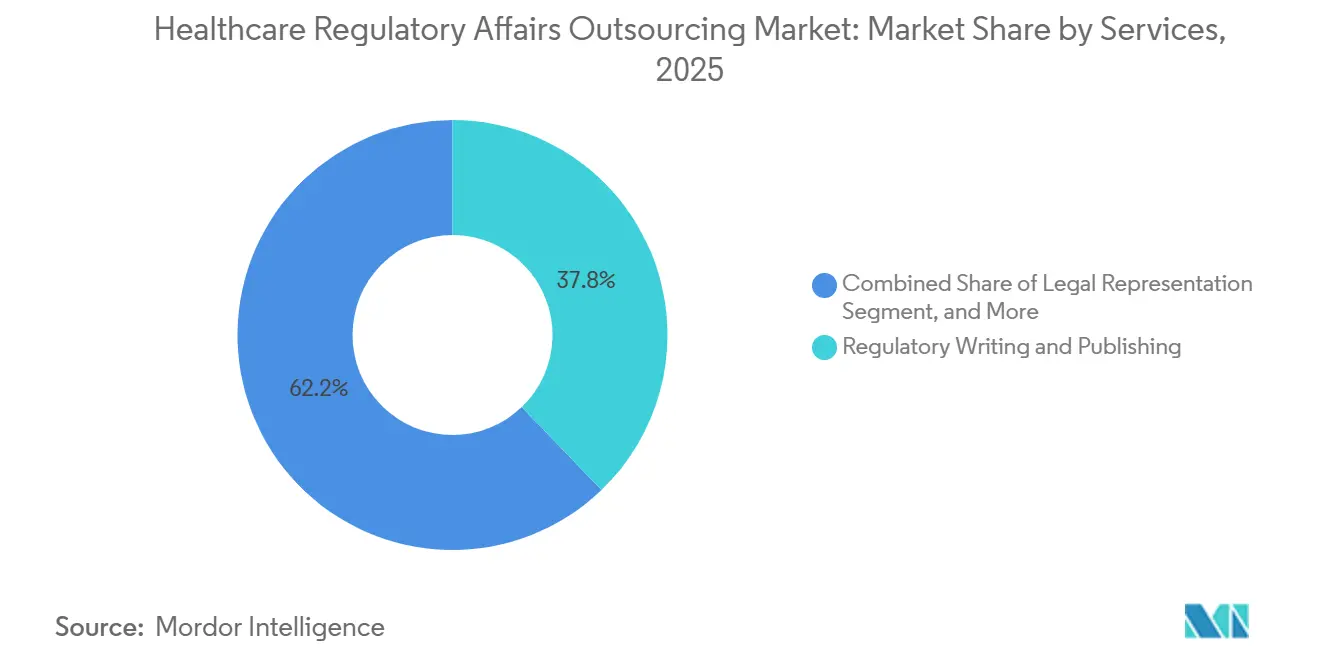

- By service, regulatory writing & publishing led with a 37.81% revenue share in 2025; product registration & clinical trial applications are projected to expand at an 11.66% CAGR through 2031.

- By product lifecycle stage, clinical-phase work held 44.73% of the healthcare regulatory affairs outsourcing market share in 2025, while post-approval & post-market services advanced at a 12.42% CAGR to 2031.

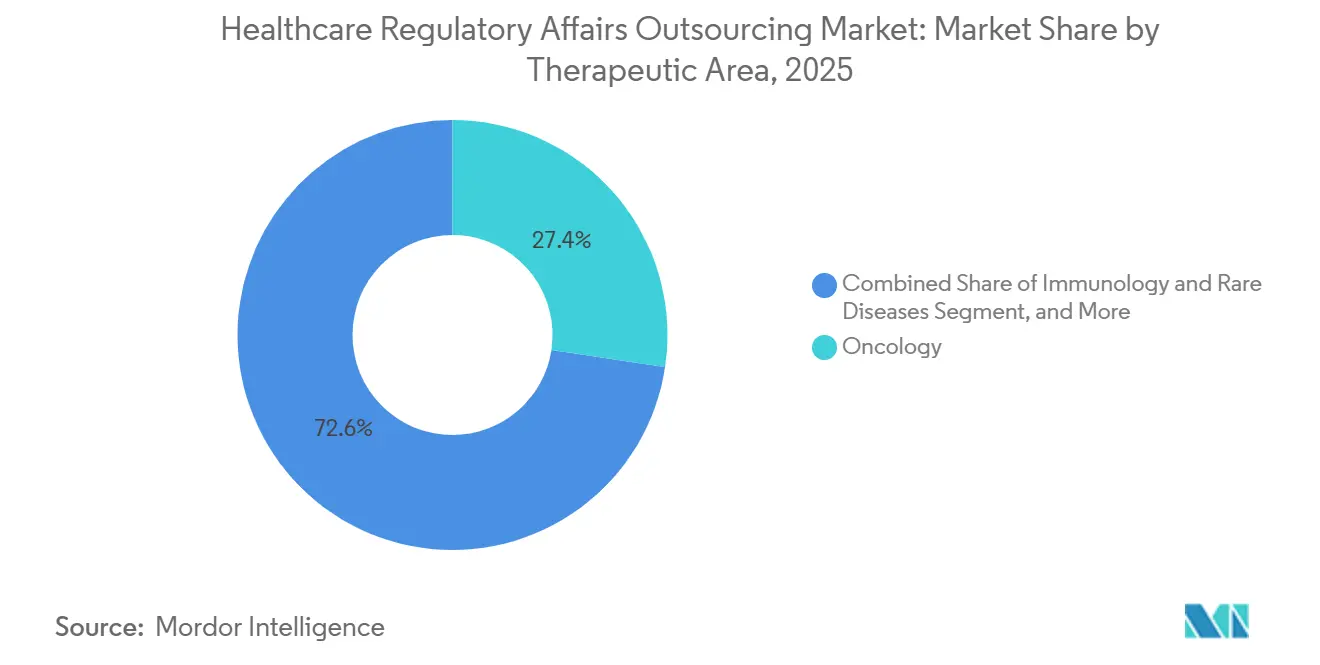

- By therapeutic area, oncology captured 27.38% of the spend in 2025; immunology & rare diseases grew fastest at a 10.19% CAGR through 2031.

- By end user, pharmaceutical companies accounted for 58.36% spending in 2025, whereas medical-device manufacturers recorded the highest projected CAGR at 9.36% through 2031.

- By geography, North America accounted for 42.36% of the revenue in 2025; the Asia-Pacific region is the fastest-growing, with a 13.06% CAGR forecasted to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Regulatory Affairs Outsourcing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Number of Clinical Trials | +1.8% | Global, with concentration in North America, Europe, and emerging APAC hubs | Medium term (2-4 years) |

| Life-Science Companies Focusing on Core Competencies | +1.5% | Global, particularly strong in North America and Europe where virtual biotechs proliferate | Long term (≥4 years) |

| Growing Complexity of Global Regulatory Frameworks | +1.4% | Global, acute in markets with recent regulatory overhauls (EU MDR, China NMPA reforms) | Long term (≥4 years) |

| Expansion of Virtual/Small-Molecule Biotech Start-Ups | +1.3% | North America and Europe core, spillover to Israel and Singapore | Medium term (2-4 years) |

| AI-Driven Regulatory-Intelligence Adoption | +1.2% | North America and EU early adopters, gradual diffusion to APAC | Short term (≤2 years) |

| Emergence of Low-Cost Regulatory Hubs in Developing Countries | +1.1% | APAC core (India, China, Philippines), spillover to Eastern Europe and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Number of Clinical Trials

ClinicalTrials.gov listed 487,000 studies by December 2024, 6.2% higher than in 2023, and nearly half of the new trials involved oncology or rare diseases.[1]National Library of Medicine, “ClinicalTrials.gov,” CLINICALTRIALS.GOV Each study generates IND submissions, protocol amendments, and safety narratives that sponsors prefer to externalize. The FDA’s Project Optimus requires oncology programs to include dose-optimization studies, adding layers of documentation that strain small teams. Decentralized models now encompass roughly 30% of Phase II and III protocols, which combine electronic consent and remote monitoring, inviting regulatory ambiguity that specialist vendors can better manage. Demand also rises for writers who can integrate digital biomarker data into dossiers. Together, these forces enlarge contract values and fortify the healthcare regulatory affairs outsourcing market.

Life-Science Companies Focusing on Core Competencies

Virtual biotechs often operate with lean staff, outsourcing every compliance task from pre-IND to post-market surveillance. Established pharmaceutical companies keep their strategies in-house but outsource high-volume activities, such as regional dossier adaptation, labeling revisions, and serialization updates. This bifurcation pushes vendors to support both premium advisory work and commoditized document assembly. Fee structures shift toward outcome-based pricing tied to approval milestones, rewarding providers able to deliver first-cycle approvals. As investors scrutinize regulatory readiness before funding rounds, early-stage companies engage consultants sooner, cementing outsourcing as a structural, not cyclical, choice.

Growing Complexity of Global Regulatory Frameworks

The EU Medical Device Regulation, fully implemented in 2024, expanded clinical evidence requirements and post-market obligations across the 27 member states. China’s National Medical Products Administration overhauled its electronic submission format the same year, tightening timelines and data-integrity checks. The FDA’s Real-World Evidence program authorizes observational data for label expansions yet offers limited design guidance, driving sponsors to experts who can craft defensible methodologies.[2]U.S. Food and Drug Administration, “AI/ML-Enabled Medical Devices,” FDA.GOV Japan introduced conditional approval for regenerative medicines, necessitating long-term follow-up studies that further expand the roles of vendors. Overlapping frameworks for software-as-a-medical-device and AI health tools introduce additional compliance layers, transforming regulatory navigation into a specialized profession that is often unavailable in most in-house groups.

AI-Driven Regulatory-Intelligence Adoption

Draft FDA guidance on AI-enabled drug-development tools, issued in May 2024, legitimized machine-learning models for protocol design and adverse-event prediction. Vendors responded by embedding natural-language processing that auto-compiles eCTD modules, cutting submission cycles by up to 40%. IQVIA’s Orchestrated Clinical Trials platform flags compliance gaps during protocol creation, shifting quality control upstream. The EMA’s IRIS portal requires structured data submissions, motivating sponsors to deploy AI tools that transform legacy PDFs into formats that are regulator-ready. Despite the promise, agencies have not finalized validation standards for AI-generated content, so sponsors hire consultants with dual expertise in data science and regulatory affairs. This premium-tier service fuels revenue growth in the healthcare regulatory affairs outsourcing market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Security & IP-Leak Risks | -0.9% | Global, acute in regions with cross-border data-transfer restrictions (EU GDPR, China PIPL) | Short term (≤2 years) |

| Lack of Global Process Standardisation | -0.7% | Global, particularly challenging for multinational sponsors managing multi-region submissions | Long term (≥4 years) |

| Escalating Cost of Specialised Regulatory Talent | -0.5% | North America and Western Europe, where competition for experienced professionals is intense | Medium term (2-4 years) |

| Rapid Policy Shifts in Digital Therapeutics | -0.4% | North America and EU, where regulatory frameworks for digital health are still maturing | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Data-Security & IP-Leak Risks

Sponsors must transfer confidential study data and formulation details to third parties; however, cross-border rules, such as the GDPR and China’s Personal Information Protection Law, impose heavy fines for breaches. Ransomware incidents that halted several regulatory submissions in 2024 highlighted vulnerability, prompting demand for SOC 2 Type II certifications and annual penetration tests. Intellectual property leakage is subtler: when one vendor serves competing sponsors in the same therapeutic class, strategic insights may unintentionally migrate. Contract negotiations now include detailed cyber controls, data residency clauses, and audit rights, adding time and cost to outsourcing deals and tempering segment growth. Vendors that invest early in zero-trust architectures, dedicated clean rooms, and strict conflict-management policies protect their revenue and client confidence.

Rapid Policy Shifts in Digital Therapeutics

The FDA issued 11 guidance documents in 2024 on clinical decision support and change-control for AI devices, but most remain draft, leaving compliance targets fluid. EU rules classify many digital therapeutics as Class II medical devices under the Medical Device Regulation; however, only 23 notified bodies were in existence by the end of 2024, creating an approval bottleneck.[3]European Commission, “Medical Devices – New Regulations,” EC.EUROPA.EU Reimbursement pathways differ by country, adding commercial uncertainty. The expiration of the U.S. enforcement-discretion policy, which had waived premarket review for many low-risk health apps during the COVID-19 emergency, triggered a surge of retrospective submissions that overwhelmed both sponsors and vendors. Because frameworks evolve faster than internal teams can retrain, clients hire consultants only for short, tactical projects, which caps multi-year contract values and restrains some expansion of the healthcare regulatory affairs outsourcing market.

Segment Analysis

By Services: Document Production Anchors Revenue, Speed-to-Market Drives Growth

Regulatory Writing & Publishing generated the largest share, at 37.81%, in 2025, underscoring the persistent demand for compliant clinical study reports, investigator brochures, and eCTD dossiers that meet ICH formatting rules. Product Registration & Clinical-Trial Applications are projected to grow at an 11.66% CAGR through 2031, as sponsors seek to compress timelines by outsourcing parallel filings across multiple regions. The FDA’s eCTD 4.0 mandate, effective January 2025, has intensified outsourcing among firms lacking the necessary systems or trained staff. Pricing remains highest for Regulatory Consulting assignments tied to modalities like CRISPR-edited therapies, where agency precedent is scarce and early scientific advice sessions demand senior experts. Legal Representation continues as a niche but high-margin activity for patents and exclusivity negotiations.

Labeling & Artwork Management is modest in size but grows steadily due to serialization mandates and multilingual packaging needs. Post-market and Lifecycle Management surges at a 12.42% CAGR, driven by the FDA Sentinel Initiative and EMA EudraVigilance requirements, which mandate continuous safety monitoring. Vendors offering real-time safety-signal detection and expedited periodic safety update reports win long-term contracts. Subscription-based regulatory intelligence, gap assessments, and mock inspections form Other Niche Services that expand during audit cycles or when new guidance emerges. The cumulative effect of these service trends maintains strong momentum in the healthcare regulatory affairs outsourcing market.

Note: Segment shares of all individual segments available upon report purchase

By Product-Lifecycle Stage: Post-Approval Surge Reflects Regulatory Vigilance

Clinical-phase activities held 44.73% of spending in 2025, covering IND filings, protocol amendments, and safety updates. Post-approval and post-market work is forecast to grow at 12.42% CAGR to 2031 as regulators mandate confirmatory studies for accelerated approvals and impose stricter pharmacovigilance standards. The FDA granted accelerated approval to 15 oncology drugs in 2024, each requiring post-launch trials to sustain demand for external regulatory support. Registration-stage projects peak just before initial approval, but now involve iterative interactions as agencies adopt rolling reviews. EMA’s Regulatory Science Strategy emphasizes adaptive pathways, compelling sponsors to maintain dialogue even after dossier submission. The healthcare regulatory affairs outsourcing market size for post-approval commitments is therefore projected to expand more rapidly than traditional clinical-phase outsourcing over the forecast period.

Pre-clinical advisory, though smaller, is trending upward because sponsors value agency feedback early, seeking to avoid costly redesigns later. Continuous real-world evidence generation blurs lines between post-market and clinical operations, prompting clients to prefer integrated vendors that can nurture products across their lifespan.

By Therapeutic Area: Rare Diseases Outpace Oncology’s Established Lead

Oncology accounted for 27.38% of the 2025 spend, as combination regimens and biomarker-driven trials made submissions more complex. Immunology & Rare Diseases, benefiting from 301 orphan drug designations in 2024, is projected to grow at a 10.19% CAGR. Surrogate endpoints accepted under orphan and breakthrough programs shorten timelines but demand nuanced benefit-risk narratives that few internal staff can craft. Infectious Disease programs gained fresh life under the Qualified Infectious Disease Product incentive, again enlarging document volume.

Cardio-metabolic therapies extend labels for GLP-1 agonists into obesity and liver disease, generating statistical complexities that push sponsors to external biostatisticians and writers. CNS & Neurology remains high-risk after multiple Alzheimer’s setbacks, yet any program reaching Phase III now involves heavy advisory engagement to align endpoints with agency expectations. Gene and cell therapies attract premium fees because vendors must address comparability, potency, and long-term safety questions unique to these modalities. Collectively, these dynamics ensure that therapeutic segmentation continues to drive depth in the healthcare regulatory affairs outsourcing market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Device Makers Accelerate as Pharma Dominates

Pharmaceutical companies accounted for 58.36% of 2025 revenue, reflecting their large pipelines and complex multi-region filings. Medical-device manufacturers are expected to show a 9.36% CAGR outlook to 2031, as the EU Medical Device Regulation and FDA Unique Device Identification rules introduce additional documentation burdens. Biotechnology companies, often operating virtually, outsource nearly every regulatory task, and their numbers continue to swell as venture investment persists. Contract Research and Manufacturing Organizations embed regulatory services into turnkey offers, compressing margins for standalone boutiques.

Combination products, such as drug-device autoinjectors, blur the jurisdictional boundary between CDER and CDRH, making dual-pathway expertise highly valuable. Device firms pursuing de novo classification rely on external strategists to present analytical and clinical data that meet the reasonable assurance standards. The cumulative complexity across end users underpins sustained expansion in the healthcare regulatory affairs outsourcing market.

Geography Analysis

North America accounted for 42.36% of the revenue in 2025, supported by more than 5,000 active biotech startups and the FDA’s position as a global reference regulator. The Asia-Pacific region is forecast to grow at a 13.06% CAGR, reflecting India’s policy reforms and China’s aggressive digitalization of submissions, which lower entry barriers for localized vendors. India’s Central Drugs Standard Control Organisation approved 62 new drug applications in 2024, representing a 28% increase, which signals improved review efficiency. China processed more than 1,100 drug registrations in the same year, 80% from domestic players, further catalyzing local consulting demand.

The Middle East & Africa are accelerating as Gulf Cooperation Council members harmonize drug pricing and registration processes, thereby lowering submission variability. South America remains fragmented, with Brazil’s ANVISA timelines diverging from those of Argentina’s ANMAT, allowing regional firms to maintain a dominant position. Mutual-recognition agreements between the FDA and regulators in the EU, Canada, and Australia streamline inspections, favoring global CROs equipped with standardized processes. These regional contrasts shape vendor expansion strategies in the healthcare regulatory affairs outsourcing market.

Competitive Landscape

The healthcare regulatory affairs outsourcing market remains moderately fragmented. Full-service CROs such as IQVIA, Charles River Laboratories, and ICON integrate regulatory affairs into end-to-end development packages, leveraging operational data to speed submissions. Thermo Fisher Scientific’s USD 17.4 billion acquisition of PPD signaled the value of in-house regulatory talent for diversified life-science suppliers. Smaller consultancies differentiate themselves by specializing in rare diseases, cell- and gene-therapies, or AI-enabled submission platforms.

Technology adoption is the main competitive lever. ICON and Microsoft use generative AI to cut eCTD compilation time by 35%. Thermo Fisher’s PPD division launched a regulatory-intelligence dashboard that aggregates updates from 50 authorities, providing predictive review timelines that sponsors value. Vendors without digital tools face margin pressure as clients demand faster cycle times at lower cost. Mergers and acquisitions target boutique firms with geographic depth or software assets that streamline document processing. Despite consolidation, white-space exists in digital therapeutics and software-as-a-medical-device consulting, areas with few seasoned advisors yet rising submission volume, keeping competitive intensity stable.

Healthcare Regulatory Affairs Outsourcing Industry Leaders

IQVIA

Parexel International Corporation

ICON PLC

Charles River Laboratories

Labcorp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Medispend and RLDatix Life Sciences have completed their merger, forming a unified organization that will operate under the Medispend name. The combined company now delivers a comprehensive suite of enterprise software and services, covering global regulatory and commercial compliance, medical affairs, field enablement, and revenue management solutions. This strategic move is designed to empower life sciences companies to expand their business while maintaining compliance across diverse markets.

- October 2025: Thermo Fisher Scientific's PPD division has launched an AI-enabled regulatory intelligence platform that aggregates real-time updates from 50 global health authorities, including the FDA, EMA, PMDA, and NMPA. The platform uses machine learning to predict review timelines and flag potential compliance gaps, offering sponsors a proactive tool to de-risk submissions and avoid costly amendments.

- January 2025: ICON plc partnered with Microsoft to deploy generative AI tools for eCTD compilation, reducing document-assembly time by an estimated 35%. The collaboration integrates Microsoft's Azure OpenAI Service with ICON's regulatory workflows, enabling automated generation of clinical study reports and investigator brochures that comply with ICH formatting standards.

Global Healthcare Regulatory Affairs Outsourcing Market Report Scope

Regulatory affairs outsourcing is the services utilized by pharmaceutical, biotech, and medical devices manufacturing companies for fast regulatory approvals from various organizations and cost-saving. Healthcare Regulatory Affairs Outsourcing market is segmented by Services (Regulatory Consulting, Legal Representation, Regulatory Writing & Publishing, Product Registration & Clinical Trial Applications, and Other Services), End User (Pharmaceutical and Biotechnology Companies and Medical Device Companies), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.

| Regulatory Consulting |

| Legal Representation |

| Regulatory Writing & Publishing |

| Product Registration & Clinical-Trial Applications |

| Labeling & Artwork Management |

| Post-Market / Lifecycle Management |

| Other Niche Services |

| Pre-Clinical |

| Clinical (Phase I-III) |

| Registration |

| Post-Approval / Post-Market |

| Oncology |

| Infectious Diseases |

| Cardio-Metabolic |

| CNS & Neurology |

| Immunology & Rare Diseases |

| Other Therapeutic Area |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Medical-Device Manufacturers |

| Contract Research & Manufacturing Organisations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Services | Regulatory Consulting | |

| Legal Representation | ||

| Regulatory Writing & Publishing | ||

| Product Registration & Clinical-Trial Applications | ||

| Labeling & Artwork Management | ||

| Post-Market / Lifecycle Management | ||

| Other Niche Services | ||

| By Product-Lifecycle Stage | Pre-Clinical | |

| Clinical (Phase I-III) | ||

| Registration | ||

| Post-Approval / Post-Market | ||

| By Therapeutic Area | Oncology | |

| Infectious Diseases | ||

| Cardio-Metabolic | ||

| CNS & Neurology | ||

| Immunology & Rare Diseases | ||

| Other Therapeutic Area | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Medical-Device Manufacturers | ||

| Contract Research & Manufacturing Organisations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the healthcare regulatory affairs outsourcing market?

The healthcare regulatory affairs outsourcing market stands at USD 9.37 billion in 2026.

What is the projected growth rate of the healthcare regulatory affairs outsourcing market?

It is forecast to expand at an 8.65% CAGR, reaching USD 14.19 billion by 2031.

Which service segment generates the highest revenue?

Regulatory writing & publishing leads, accounting for 37.81% of 2025 revenue.

Which region will see the fastest growth?

Asia-Pacific is projected to grow at a 13.06% CAGR through 2031.

Why are post-approval services gaining traction?

Regulators now demand continuous real-world evidence and intensified pharmacovigilance, driving a 12.42% CAGR in post-market outsourcing.