Health Caregiving Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

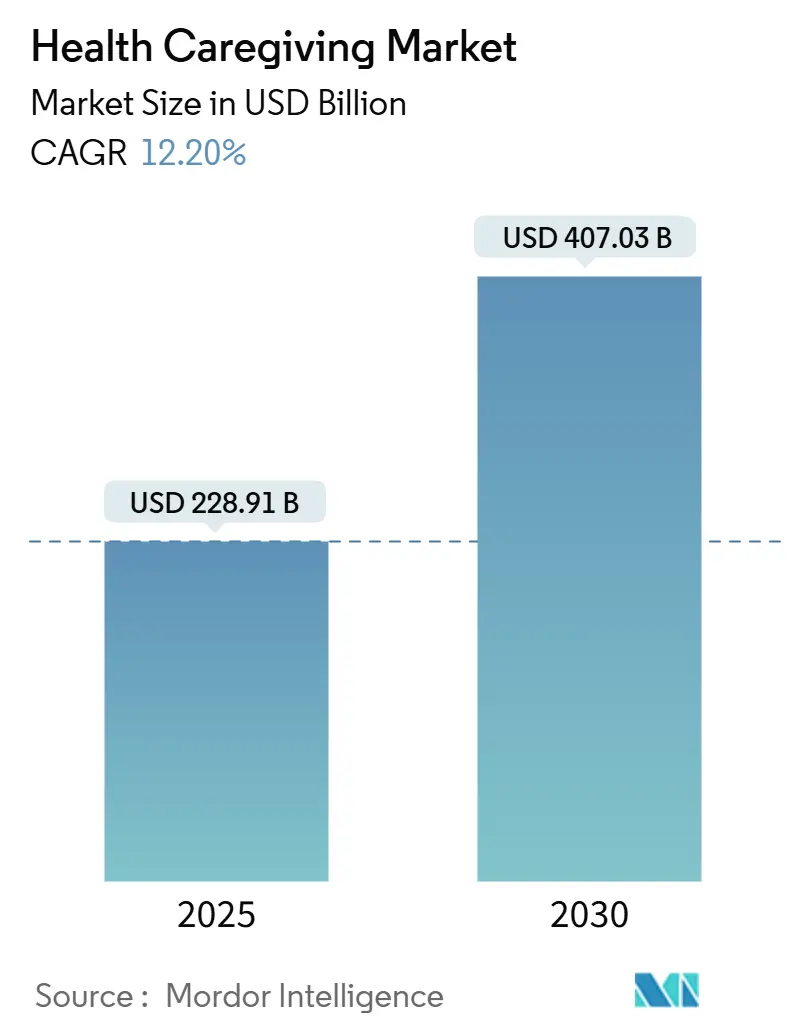

| Market Size (2025) | USD 228.91 Billion |

| Market Size (2030) | USD 407.03 Billion |

| Growth Rate (2025 - 2030) | 12.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

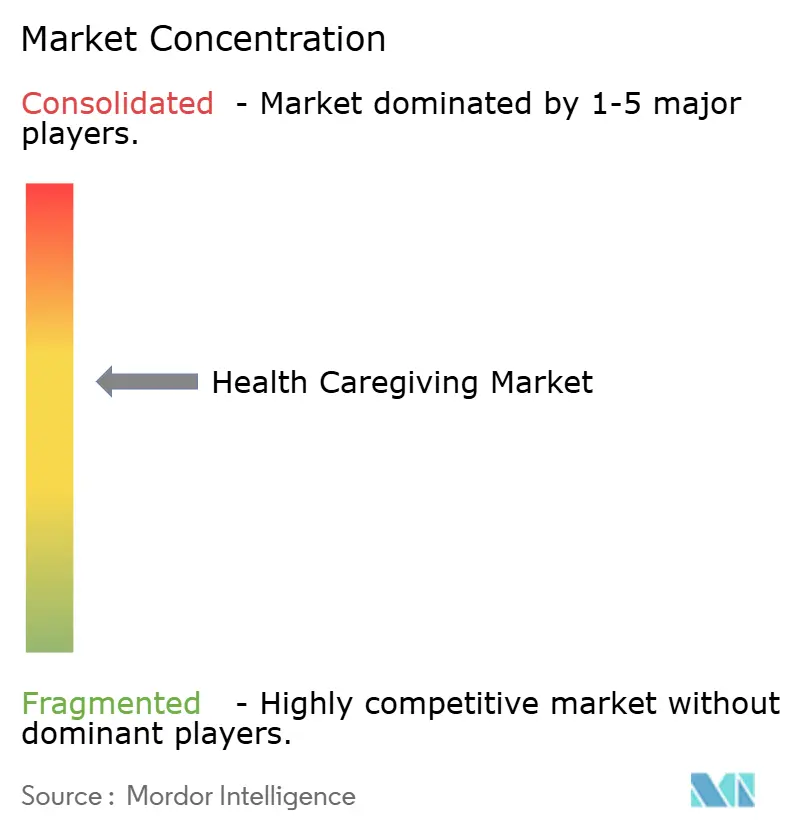

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Health Caregiving Market Analysis by Mordor Intelligence

The health caregiving market size stands at USD 228.91 billion in 2025 and is projected to reach USD 407.03 billion by 2030, advancing at a 12.2% CAGR. Growing preference for aging in place, accelerated uptake of connected-care technology, and payer incentives that reward home-based outcomes continue to propel the health caregiving market. Adoption of value-based reimbursement models pushes providers to reduce avoidable hospitalizations, while artificial-intelligence-enabled analytics already cut emergency-department visits by 23% among high-risk groups. Rapid growth of gig-economy caregiver platforms eases labor shortages in urban centers, and expanded public funding for home- and community-based services widens eligibility for remote monitoring benefits. The regulatory framework remains supportive but complex; proposed CMS margin caps coexist with expanded reimbursement for virtual care, and cybersecurity obligations intensify as data breaches affected 133 million people in 2024.

Key Report Takeaways

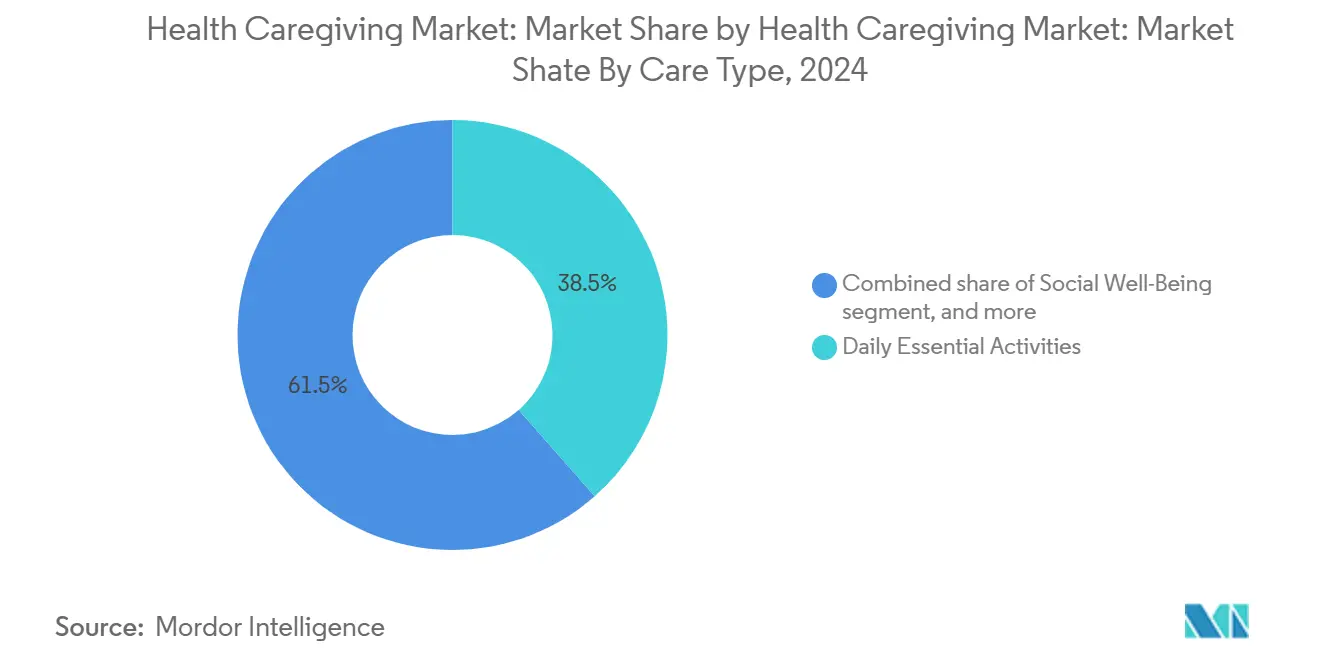

- By care type, daily essential activities led with 38.54% health caregiving market share in 2024, while Institutional/Nursing Care is forecast to expand at a 14.11% CAGR through 2030.

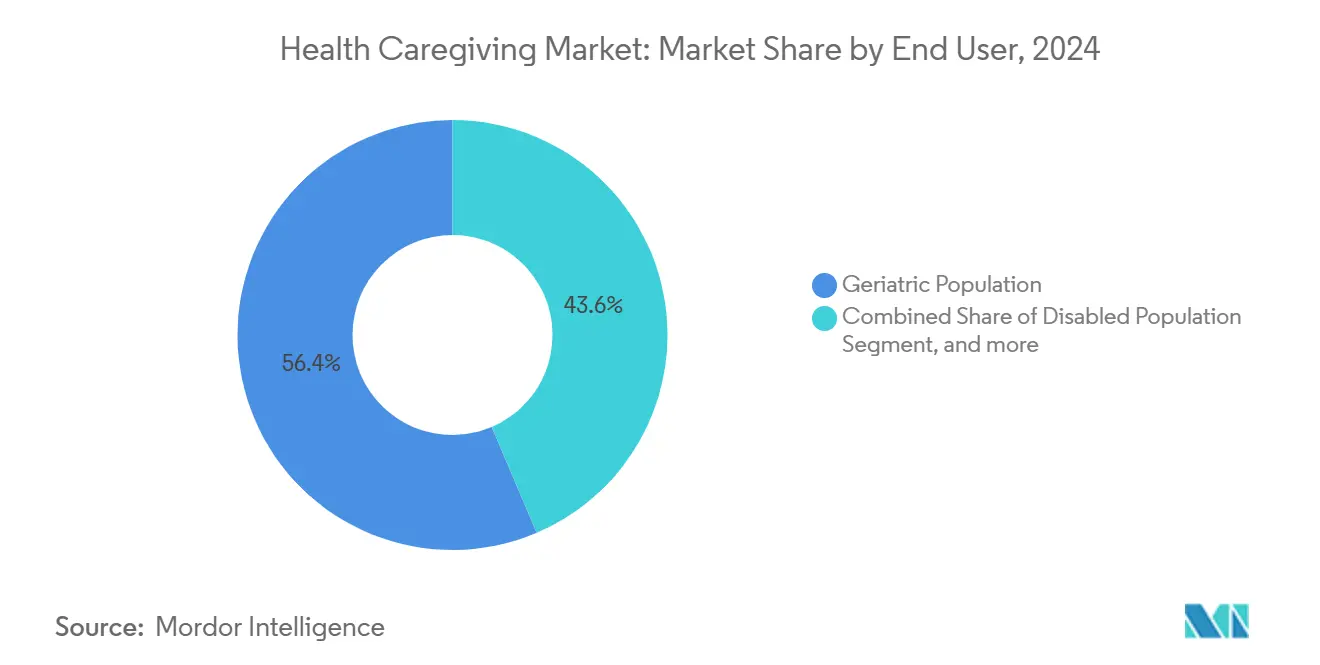

- By end user, the geriatric group accounted for 56.43% of the health caregiving market size in 2024, whereas post-partum mothers and infants are projected to grow at a 14.54% CAGR to 2030.

- By payment source, public funding sources held 58.53% share of the health caregiving market in 2024; private insurance shows the fastest trajectory with a 13.67% CAGR through 2030.

- By geography, North America commanded 41.23% health caregiving market share in 2024, yet Asia-Pacific is expected to register a 13.45% CAGR between 2025 and 2030.

Global Health Caregiving Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly Expanding Geriatric Population | +3.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Growing Burden Of Chronic Diseases | +2.8% | Global, particularly APAC emerging markets | Medium term (2-4 years) |

| Accelerated Adoption Of Telehealth & Remote-Patient-Monitoring Platforms | +2.1% | North America & EU leading, APAC following | Short term (≤ 2 years) |

| Expansion Of Value-Based Reimbursement Models | +1.9% | North America primary, EU selective adoption | Medium term (2-4 years) |

| Gig-Economy Caregiver Platforms | +1.4% | Urban centers globally, strongest in North America | Short term (≤ 2 years) |

| AI-Driven Predictive Analytics | +1.0% | Developed markets initially, scaling globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapidly Expanding Geriatric Population

Adults aged 65 and above increasingly choose to remain at home, with 77% stating this preference in 2024[1]AARP Public Policy Institute, “2024 Home and Community Preference Survey,” aarp.org. Family-care capacity declines as dual-career households and geographic dispersion limit informal support, creating a gap filled by professional services. The monthly cost difference between home-based and nursing-home care averages USD 2,800, steering families and payers toward community options. Medicare Advantage plans reacted by offering supplemental in-home benefits in 89% of plans in 2025, up from 67% two years earlier. These shifts anchor long-term demand and reinforce a supply pipeline for specialized home-care providers.

Growing Burden of Chronic Diseases

Multiple chronic conditions affected 67% of Medicare beneficiaries in 2024. Integrated platforms that combine clinical oversight and daily living support have reduced hospitalizations and emergency visits, demonstrating 38% fewer readmissions among heart-failure patients when remote monitoring pairs with home nursing. Continuous data capture unlocks new revenue streams for providers while lowering payer costs, sustaining healthy margins within the health caregiving market.

Accelerated Adoption of Telehealth & Remote-Patient-Monitoring Platforms

The FDA cleared 47 new remote patient-monitoring devices in 2024, including fall-detection sensors and medication-adherence tools that integrate with electronic health records. Machine-learning systems now predict hospitalization risk 30 days ahead with 84% accuracy. Providers layer these insights onto caregiver workflows, forming hybrid models that deliver clinical accuracy and human empathy, which in turn bolsters user trust and outcome performance across the health caregiving market.

Expansion of Value-Based Reimbursement Models

Medicare Advantage spending on supplemental home-care benefits reached USD 23.7 billion in 2024. CMS launched 12 demonstration projects to test integrated home-based delivery that merges medical and social services. Early evidence shows coordinated home care matches institutional outcomes at 15-25% lower cost, providing a durable catalyst for provider investment and payer alignment in the health caregiving market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Caregiver Workforce Shortages & High Turnover | -2.1% | Global, most severe in rural areas | Medium term (2-4 years) |

| High Cost Of Care And Uneven Insurance Reimbursement | -1.8% | North America & EU primarily | Short term (≤ 2 years) |

| Escalating Cybersecurity And Data-Privacy Liabilities | -1.2% | Global, regulatory focus in EU & North America | Long term (≥ 4 years) |

| Regulatory Uncertainty From Proposed CMS Access Rule | -0.9% | United States primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute Caregiver Workforce Shortages & High Turnover

Home-health turnover reached 82% in 2024, straining care continuity[2]National Association for Home Care & Hospice, “2024 Home Care Workforce Report,” nahc.org. Wage gaps versus hospital roles widen attrition risk, and rural vacancy rates run 34% higher than urban averages. Skill-mix shortages emerge as chronic-disease management and device proficiency become mandatory. These constraints limit near-term expansion capacity in parts of the health caregiving market.

High Cost of Care and Uneven Insurance Reimbursement

Medicare home-health rates rose 2.1% in 2024 while provider costs climbed 6.8%, compressing margins. Private-insurance benefit designs vary, causing coverage gaps and administrative delays. Smaller agencies face resource burdens when juggling multiple payers, hindering entry into new regions and tempering competitive intensity within the health caregiving industry.

Segment Analysis

By Care Type: Institutional Services Accelerate Home-Based Complexity

Daily essential activities commanded 38.54% of the health caregiving market in 2024, signaling demand for help with bathing, meals, and mobility. Institutional/Nursing Care is poised for a 14.11% CAGR, reflecting rising acceptance of higher-acuity services at home. Advanced monitoring devices cleared by the FDA in 2024 enable hospital-grade oversight that supports this shift. In a parallel trend, Health & Safety Awareness services pair devices with rapid response teams, while Social Well-Being programs reduce isolation risks. Collectively, these lines are reshaping the health caregiving market size through bundled clinical and non-clinical offerings.

Growth in Institutional/Nursing Care underscores the blurring boundary between medical and supportive functions. Providers integrate skilled nursing, physical therapy, and social services under unified care plans, boosting patient retention and reimbursement rates. As clinical oversight deepens, technology platforms track vitals, medication adherence, and environmental safety in real time, helping agencies scale without escalating labor hours. These changes reinforce the long-term expansion path of the health caregiving market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Post-Partum Care Catalyzes New Demand

The geriatric cohort held 56.43% share of the health caregiving market size in 2024, underpinned by Medicare coverage expansion. Disabled individuals, post-acute patients, and chronic-disease populations require blended support that merges personal assistance and medical supervision. Post-partum mothers and infants, while a smaller share, present a 14.54% CAGR through 2030 as Medicaid coverage for doula services spreads to 23 states[3]National Conference of State Legislatures, “State Medicaid Coverage of Doula Services,” ncsl.org.

As family structures evolve, professional post-partum support gains traction, improving maternal outcomes and reducing hospital readmissions for newborn complications. Insurers benefit from lower acute-care costs, encouraging broader coverage. Providers specializing in lactation consulting and maternal mental-health check-ins achieve operational efficiencies due to short episode durations and higher payment rates. These dynamics diversify the health caregiving market and ease reliance on geriatric revenue streams.

Note: Segment shares of all individual segments available upon report purchase

By Payment Source: Private Insurance Expands Benefit Scope

Public programs supplied 58.53% of health caregiving market funding in 2024 through Medicare, Medicaid, and allied waivers. These programs anchor baseline demand and set quality standards. Private insurance, however, is tracking a 13.67% CAGR, driven by competitive benefit designs and employer interest in workforce well-being.

Large insurers increased home-care coverage to manage total cost of care and enhance member satisfaction. Multiline carriers integrate digital triage, home-care nurse visits, and social-needs assessments into bundled products. As private payors scale, reimbursement bureaucracy eases, accelerating credentialing for agencies and spurring tech adoption that supports evidence-based quality metrics across the health caregiving market.

Geography Analysis

North America retained 41.23% of the health caregiving market in 2024 thanks to mature reimbursement structures and high remote-monitoring penetration. U.S. Medicare Advantage enrollment in RPM programs reached 34% in 2024. Canada leverages universal coverage to pivot more services into communities, and Mexico’s rising middle class is fueling private-insurance uptake. Providers focus on technology-driven efficiency that offsets wage pressures and wide service areas.

Asia-Pacific is forecast to grow at 13.45% CAGR, led by China and India. China’s demographic inversion accelerates demand, while policy shifts invite private capital into elder-care ventures. Japan pioneers robotics for personal assistance, modeling workforce solutions for the region. India’s middle-class growth and expanding insurance base create fertile ground for organized care networks. Australia’s National Disability Insurance Scheme underwrites comprehensive home supports, offering a blueprint for neighboring markets.

Europe enjoys steady progress as universal systems reposition around home-based care. Germany’s long-term-care insurance funds extensive in-home benefits, France incentives home modifications through tax credits, and the United Kingdom’s NHS sets community-care targets to cut hospital occupancy. Strict GDPR rules raise compliance costs but also heighten public trust in digital solutions, supporting adoption of secure data flows and connected devices in the health caregiving market.

Competitive Landscape

The health caregiving market shows moderate fragmentation. Regional leaders such as Amedisys and LHC Group leverage Medicare certification and clinical depth, while digital players like Honor Technology and Care.com deploy matching algorithms to optimize scheduling and staffing. Health-system entrants, including Encompass Health, extend rehabilitation expertise into the home, combining therapy and nursing within single episodes of care.

Technology integration serves as the primary differentiator. Providers deploying machine-learning risk tools, such as Vesta Healthcare, record a 31% drop in emergency-department use among managed members. Gig-platform models increase caregiver availability in metropolitan areas, helping agencies flex staffing without fixed overhead. Rural markets remain underserved, delivering white-space opportunities for tele-enabled hybrids that coordinate across dispersed geographies. Regulatory guardrails, including CMS conditions of participation and state licensure, elevate entry barriers and reinforce compliance as a competitive asset.

Health Caregiving Industry Leaders

-

Vesta Healthcare

-

Seniorlink, Inc.

-

Lively

-

Cariloop

-

HomeTeam

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Home Helpers Home Care in Freehold, New Jersey, launched a Home Health Aide Training Program in partnership with Ocean County Vocational Technical School. The initiative aims to address the shortage of certified home health aides by building a new pipeline of skilled caregivers

- October 2025: GE HealthCare launched CareIntellect for Perinatal, a cloud‑first application designed to streamline maternal and fetal care workflows. Developed with input from clinicians and in collaboration with HCA Healthcare, the platform helps optimize care delivery and supports families in going home healthy

- July 2025: Home Helpers Home Care in Freehold, New Jersey, launched a Home Health Aide Training Program in partnership with Ocean County Vocational Technical School. The initiative aims to address the shortage of certified home health aides by building a new pipeline of skilled caregivers

- January 2025: Merck announced a new Caregiver Leave Benefit, offering employees at least 10 days of financially protected leave to care for critically or terminally ill immediate family members.

Global Health Caregiving Market Report Scope

As per the scope, health caregiving is the act of providing support and assistance to individuals who cannot fully care for themselves due to illness, disability, or aging. Caregivers may be family members, professionals, or volunteers, and their roles span from basic daily assistance to complex medical support.

The health caregiving market is segmented by Care Type (Daily Essential Activities, Health & Safety Awareness, Social Well-Being, Institutional/Nursing Care, Other Care Types), End User (Geriatric Population, Disabled Population, Post-Acute/Chronic-Disease Patients, Post-partum Mothers & Infants), Payment Source (Public, Private Insurance, Out-of-Pocket/Self-Pay), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Daily Essential Activities |

| Health & Safety Awareness |

| Social Well-Being |

| Institutional / Nursing Care |

| Other Care Types |

| Geriatric Population |

| Disabled Population |

| Post-Acute / Chronic-Disease Patients |

| Post-partum Mothers & Infants |

| Public |

| Private Insurance |

| Out-of-Pocket / Self-Pay |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Care Type | Daily Essential Activities | |

| Health & Safety Awareness | ||

| Social Well-Being | ||

| Institutional / Nursing Care | ||

| Other Care Types | ||

| By End User | Geriatric Population | |

| Disabled Population | ||

| Post-Acute / Chronic-Disease Patients | ||

| Post-partum Mothers & Infants | ||

| By Payment Source | Public | |

| Private Insurance | ||

| Out-of-Pocket / Self-Pay | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the health caregiving market in 2025?

The health caregiving market size is USD 228.91 billion in 2025.

What is the projected growth rate for health caregiving through 2030?

The market is expected to grow at a 12.2% CAGR, reaching USD 407.03 billion by 2030.

Which care type is expanding the fastest?

Institutional/Nursing Care shows the highest growth at a 14.11% CAGR through 2030.

Which region is growing quickest in health caregiving?

Asia-Pacific is projected to post a 13.45% CAGR between 2025 and 2030.

What is the main driver behind increased home-based care demand?

A rapidly aging global population combined with consumer preference for aging in place underpins long-term demand.

How are insurers encouraging home-based caregiving?

Medicare Advantage and private insurers expand supplemental benefits and value-based models that reimburse remote monitoring and in-home services.

Page last updated on: