| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 8.86 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Hazardous Location LED Lighting Market Analysis

The Hazardous Location LED Lighting Market is expected to register a CAGR of 8.86% during the forecast period.

The hazardous location LED lighting industry is experiencing rapid technological transformation, driven by innovations in automation, the Industrial Internet of Things (IIoT), and advanced energy efficiency solutions. LED technology has demonstrated remarkable progress in addressing the unique challenges of confined spaces and critical environments, with modern LED fixtures achieving up to 140 lumens per watt efficiency while maintaining an operational lifespan of 100,000 hours. The integration of smart sensors with LED networks has enabled dynamic illumination control and early hazard detection capabilities, allowing facilities to optimize both safety and energy consumption simultaneously.

The industry's landscape is being reshaped by stringent environmental sustainability initiatives and energy efficiency requirements across major industrial sectors. LED lighting solutions have proven particularly effective in reducing energy consumption, with studies indicating potential energy savings of up to 60% compared to traditional lighting systems. This efficiency gain is particularly significant in continuous operation environments like petrochemical facilities and offshore platforms, where lighting systems operate 24/7 and represent a substantial portion of energy costs.

The market is witnessing increased adoption across specialized industrial applications, particularly in the oil and gas, petrochemical, and mining sectors, where safety and reliability are paramount. Studies have shown that improved illumination through LED technology can decrease industrial accident rates by over 60%, highlighting the critical role of proper lighting in workplace safety. The industry has responded with innovations in explosion-proof LED lighting designs and enhanced durability features, specifically engineered to withstand harsh environmental conditions while maintaining consistent performance.

Manufacturing and supply chain dynamics are evolving with an increased focus on regional production capabilities and technological advancement. Leading manufacturers are investing in research and development to enhance product performance and reliability while reducing production costs. The industry is seeing a shift toward integrated solutions that combine lighting with smart monitoring and control systems, enabling predictive maintenance and enhanced operational efficiency. This trend is particularly evident in new industrial facility constructions and modernization projects, where integrated industrial LED lighting systems are becoming standard specifications rather than optional upgrades.

Hazardous Location LED Lighting Market Trends

Regulations Promoting Proper Lighting for Worker Safety in Hazardous Locations

Stringent workplace safety regulations across regions are mandating proper lighting solutions in hazardous environments to ensure worker safety and prevent accidents. According to the Management of Health and Safety at Work Regulations 1999 (MHSW), employers are required to conduct comprehensive workplace assessments covering lighting adequacy and suitability, particularly in areas with explosive or combustible materials. The Health & Safety at Work Act of 1974 further emphasizes that employers must ensure proper lighting to protect employees' health and eyesight, with specific guidance published by the Health and Safety Executive in HSG 38 stating that lighting must be safe and pose no health risks in non-domestic premises.

The regulations have become increasingly detailed in terms of illuminance requirements for different types of work environments. For specialized work like electronic assembly where workers need to differentiate between wire colors, employers must ensure lighting does not affect natural color appearance to prevent accidents. In meat and poultry processing areas, minimum illumination requirements range from 30 foot-candles for general areas to 200 foot-candles for quality control inspection zones. These strict illumination standards, combined with requirements for explosion-proof ratings and certifications like IP65-68 for water and dust resistance, are compelling industries to adopt advanced LED lighting solutions that meet multiple compliance needs while enhancing workplace safety. In particular, ATEX lighting and intrinsically safe lighting options are becoming essential to meet these stringent safety standards.

Understand The Key Trends Shaping This Market

Download PDF

Rising Demand for Cost-Effective and Energy-Efficient LED Lighting Solutions

The superior energy efficiency and cost-effectiveness of LED lighting solutions are driving their adoption across hazardous industrial environments. LED fixtures can reduce energy consumption by up to 75% compared to traditional lighting while providing better luminous intensity and color rendering. With an extended lifespan of approximately 100,000 hours and reduced maintenance requirements, LED solutions offer significant operational cost savings through lower energy bills and decreased replacement frequency. For instance, a major oil refinery in the United States achieved annual energy savings of USD 34,668 and reduced maintenance costs by USD 766,647 after implementing LED lighting solutions.

The industrial and manufacturing sector, which accounts for 32% of energy usage in the United States, represents one of the largest opportunities for energy cost reduction through LED adoption. Energy efficiency programs like ENERGY STAR certification, Lighting Design Lab certification, and the DLC Industrial Energy Efficiency Program are actively promoting LED solutions to help organizations reduce their carbon footprint. These initiatives, combined with the decreasing average selling price of LED fixtures and their ability to integrate with advanced control systems, are making them an increasingly attractive option for hazardous locations. LED fixtures also offer superior performance in extreme temperatures and high-vibration environments, with some advanced models featuring ratings of up to 100,000 hours compared to the maximum 25,000-hour lifespan of fluorescent and HID fixtures. The adoption of flameproof lighting and industrial LED lighting is particularly beneficial in these challenging environments.

Segment Analysis: By Class

Class I Segment in Hazardous Location LED Lighting Market

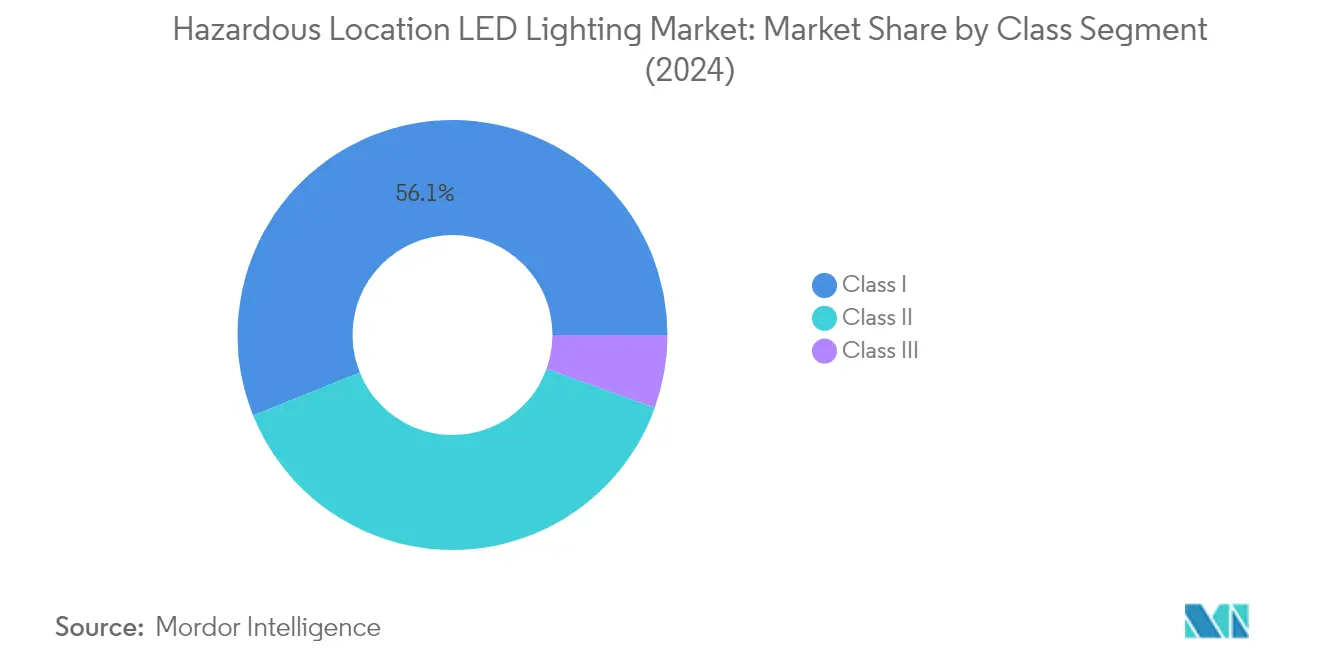

The Class I segment maintains its dominant position in the hazardous location LED lighting market, commanding approximately 56% market share in 2024. This segment primarily covers areas where flammable gases, vapors, or liquids are present in quantities that can ignite if they come into contact with open flames or electrical sparks. The segment's leadership is driven by extensive applications across critical industries including gas stations, utility gas plants, petroleum refining facilities, solvent extraction plants, ethanol facilities, aircraft hangars, fuel servicing areas, dry cleaning plants, and storage tanks containing flammable/combustible liquids. The widespread adoption of Class 1 Division 1 lighting solutions is attributed to their superior safety features, including vibration-proof, shock-proof, and corrosion-resistant materials, making them ideal for these high-risk environments.

Class II Segment in Hazardous Location LED Lighting Market

The Class II segment is emerging as the fastest-growing category in the hazardous location LED lighting market, projected to grow at approximately 9% CAGR from 2024 to 2029. This robust growth is driven by increasing applications in locations hazardous due to the presence of combustible dust, including granaries, coal mines, sugar or starch plants, medicine-producing factories, fireworks-producing factories, plastic-producing factories, and plants manufacturing or storing magnesium or aluminum powders. The segment's growth is further supported by the rising need for enclosed and gasketed fixtures that can prevent dust accumulation while maintaining low temperatures, particularly in grain silos and other agricultural and mineral processing plants where dust coverage can be extensive for prolonged periods. The adoption of Class 1 Division 2 lighting fixtures is crucial in these environments to ensure safety and compliance.

Remaining Segments in Hazardous Location LED Lighting Market by Class

The Class III segment, while smaller in market share, plays a crucial role in addressing specific hazardous location lighting needs where easily ignitable fibers or flyings are present. This segment primarily serves industries such as textile mills, wood processing facilities, cotton gins, and other manufacturing environments where combustible fibers are used in the manufacturing process. The segment's importance is particularly evident in facilities that shape, pulverize, or cut wood creating sawdust or flyings, as well as in leather goods workshops and shoe manufacturing plants where proper lighting is essential for both safety and operational efficiency.

Segment Analysis: By Device Type

Zone 2 Segment in Hazardous Location LED Lighting Market

Zone 2 dominates the hazardous location LED lighting market, commanding approximately 33% market share in 2024, while also demonstrating the strongest growth trajectory among all zones. This segment primarily serves areas where ignitable concentrations of flammable gas vapors or liquids are usually not present under normal operating conditions but may occur accidentally. The segment's prominence is driven by its widespread applications across oil and gas facilities, mining operations, power generation plants, and chemical/petroleum industries. Many major market vendors are initially targeting Zone 2 lighting applications before expanding into other zones, owing to the relatively lower certification requirements and broader application potential. The segment has witnessed significant product innovations, particularly in energy-efficient LED solutions that offer superior illumination while maintaining safety standards for potentially hazardous environments.

Remaining Segments in Device Type Segmentation

The hazardous location LED lighting market encompasses several other critical zones, each serving specific safety requirements and industrial applications. Zone 1 lighting and Zone 21 segments cater to areas where explosive atmospheres are likely to occur during normal operations, finding extensive use in petrochemical plants and processing facilities. Zone 0 and Zone 20, representing the highest risk categories, serve locations with continuous presence of explosive atmospheres, primarily in gas storage and dust-heavy environments. The Zone 22 segment addresses areas with lower risk of explosive atmospheres during normal operation, commonly found in food processing and pharmaceutical facilities. Each of these segments maintains distinct certification requirements and safety standards, contributing to the market's diverse product portfolio and application spectrum.

Segment Analysis: By End-User Industry

Oil and Gas Segment in Hazardous Location LED Lighting Market

The oil and gas industry continues to dominate the hazardous location LED lighting market, commanding approximately 26% of the total market share in 2024. This significant market position is driven by the extensive presence of dangerous chemical compounds, oil, and gas in refining and processing facilities, which poses high risks of electrical sparks igniting such compounds. The industry's stringent regulatory requirements for worker safety further contribute to the high demand for hazardous location LED lighting solutions. These LED fixtures in oil and gas facilities must meet specific certifications like C1D1 (Class 1, Division 1) and C1D2 (Class 1, Division 2) approval ratings set by the National Electric Code. Additionally, the fixtures must be corrosion and water-resistant due to their exposure to harsh solutions during regular maintenance and cleaning of such facilities, typically requiring IP67 ratings that offer protection against water and dust immersions up to 1 meter deep for 30 minutes.

Processing Segment in Hazardous Location LED Lighting Market

The processing segment, which includes food processing, plastic, chemical processing, coal, and storage facilities, is projected to witness the highest growth rate of approximately 10% during the forecast period 2024-2029. This accelerated growth is attributed to the diverse environmental challenges these facilities face, from high temperatures in chemical and plastic processing plants to low temperatures in food processing plants and cold storages. The increasing focus on energy efficiency and safety regulations in processing facilities is driving the adoption of LED lighting solutions. These environments contain dust, vapor, and water, requiring lighting solutions to be effective against the intrusion of dirt, dust, or water, leading to the widespread adoption of IP65-, IP66-, IP67-, and IP68-rated LED fixtures. The quality and accuracy of lighting are primary concerns in processing plants, particularly in dry environments where dust makes visibility difficult.

Remaining Segments in End-User Industry

The hazardous location LED lighting market encompasses several other crucial segments including petrochemical, industrial, power generation, and pharmaceutical sectors. The petrochemical segment is particularly significant due to the extensive network of production and processing facilities requiring specialized lighting solutions. The industrial segment covers various manufacturing facilities that deal with flammable materials and require different classes of LED lighting. The power generation sector demands high-performance LED solutions for both conventional and renewable energy facilities, while the pharmaceutical segment requires precise lighting solutions for maintaining clean room conditions and ensuring safety in drug manufacturing processes. Each of these segments presents unique challenges and requirements for hazardous location LED lighting, from temperature resistance to specific safety certifications and standards compliance.

Hazardous Location LED Lighting Market Geography Segment Analysis

Hazardous Location LED Lighting Market in North America

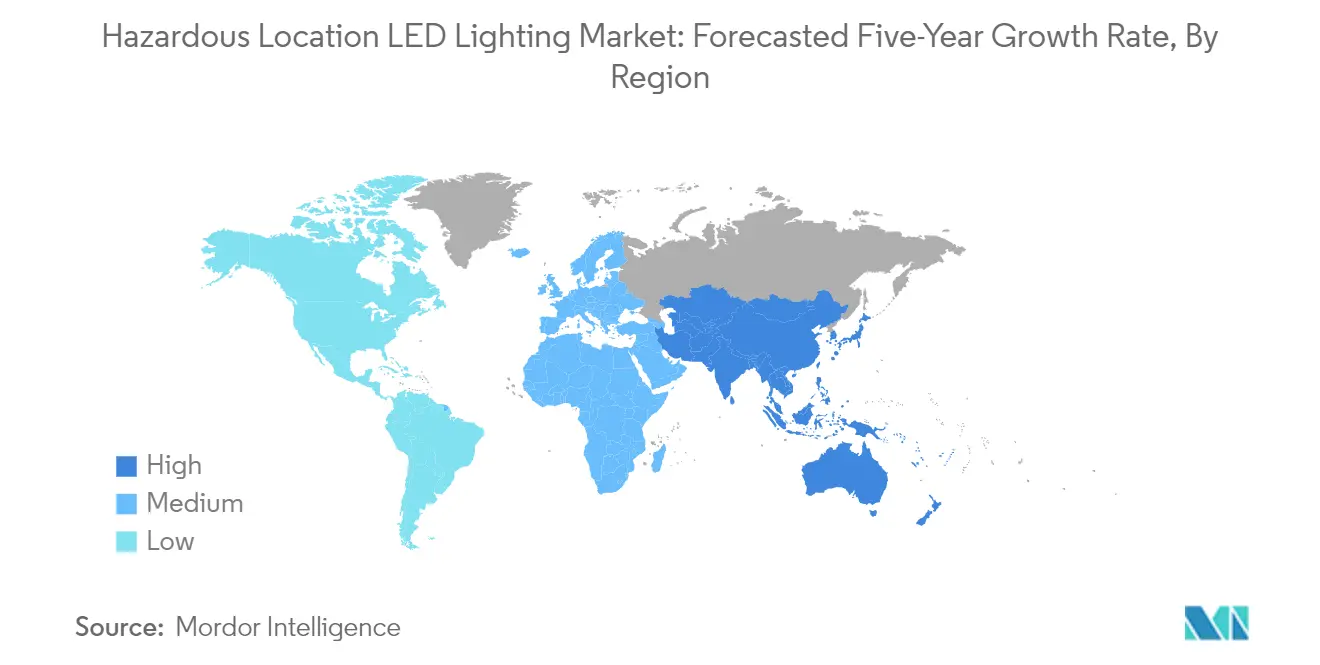

North America commands approximately 26% of the global hazardous location LED lighting market in 2024, establishing itself as a dominant region driven by stringent safety regulations and widespread industrial adoption. The region's leadership position is attributed to its advanced industrial infrastructure, particularly in the oil and gas, petrochemical, and manufacturing sectors. The market is characterized by high adoption rates of energy-efficient lighting solutions, supported by government initiatives promoting workplace safety and energy conservation. Industrial and manufacturing facilities across the United States and Canada are increasingly transitioning to LED lighting for hazardous areas systems to reduce operational costs and enhance workplace safety. The region's strong focus on technological innovation and automation in hazardous environments has created a robust demand for advanced LED lighting solutions. Additionally, the presence of major market players and their extensive distribution networks has facilitated greater market penetration. The region's commitment to industrial safety standards and environmental regulations continues to drive the adoption of LED lighting for hazardous areas systems across various industrial applications.

Hazardous Location LED Lighting Market in Europe

The European hazardous location LED lighting market demonstrated robust growth with approximately 8% CAGR from 2019 to 2024, driven by stringent safety regulations and increasing industrial modernization initiatives. The region's market dynamics are shaped by its strong focus on energy efficiency and workplace safety standards, particularly in countries like Germany, France, and the United Kingdom. The industrial sector's ongoing transition towards more sustainable and energy-efficient lighting solutions has been a key growth driver. European manufacturers are increasingly investing in advanced LED technologies for hazardous environments, particularly in chemical processing, pharmaceutical, and offshore facilities. The region's commitment to reducing carbon emissions has accelerated the adoption of energy-efficient lighting solutions across industrial sectors. The market is characterized by high technological standards and sophisticated product offerings, reflecting the region's advanced industrial infrastructure. Local manufacturers are focusing on developing innovative solutions that comply with both safety requirements and energy efficiency standards.

Hazardous Location LED Lighting Market in Asia-Pacific

The Asia-Pacific hazardous location LED lighting market is projected to maintain a strong growth trajectory with an expected CAGR of approximately 10% from 2024 to 2029, positioning it as the fastest-growing region globally. The market's expansion is driven by rapid industrialization across emerging economies, particularly in China, India, and Southeast Asian countries. The region's growth is characterized by increasing investments in manufacturing facilities, chemical processing plants, and oil and gas infrastructure. Rising awareness about industrial safety standards and energy efficiency requirements is reshaping the market landscape. The petrochemical and manufacturing sectors are primary growth drivers, with increasing adoption of advanced lighting solutions in hazardous environments. Local manufacturers are expanding their production capabilities to meet the growing demand, while international players are strengthening their presence through strategic partnerships and regional expansion initiatives. The region's focus on industrial modernization and safety compliance is expected to sustain market growth momentum.

Hazardous Location LED Lighting Market in Latin America

The Latin American hazardous location LED lighting market is experiencing steady growth driven by expanding industrial activities, particularly in Brazil, Mexico, and Chile. The region's market dynamics are influenced by increasing investments in mining operations, oil and gas exploration, and chemical processing facilities. Industrial safety regulations and energy efficiency requirements are becoming increasingly stringent, driving the adoption of advanced lighting solutions. The market is characterized by a growing focus on modernizing industrial infrastructure and improving workplace safety standards. Local manufacturers are expanding their product portfolios to meet specific regional requirements, while international players are strengthening their distribution networks. The region's ongoing industrial development and increasing focus on workplace safety are creating new opportunities for market expansion. The petrochemical and mining sectors remain key growth drivers, with increasing demand for LED lighting for mining and LED lighting for oil and gas solutions.

Get Analysis on Important Geographic Markets

Download PDF

Hazardous Location LED Lighting Industry Overview

Top Companies in Hazardous Location LED Lighting Market

The hazardous location LED lighting market is characterized by continuous product innovation focused on enhanced safety features, energy efficiency, and durability. Companies are investing heavily in research and development to create advanced LED solutions that meet stringent safety certifications while offering improved performance in extreme environments. Operational agility is demonstrated through vertically integrated manufacturing capabilities and robust supply chain networks that ensure consistent product quality and timely delivery. Strategic partnerships with distributors and system integrators have become crucial for market penetration, particularly in emerging economies. Geographic expansion strategies are primarily centered on establishing regional manufacturing facilities and strengthening local distribution networks, with particular focus on high-growth regions like the Middle East and Asia Pacific. Companies are also increasingly incorporating IoT capabilities and smart features into their hazardous location lighting solutions to differentiate their offerings and capture new market segments.

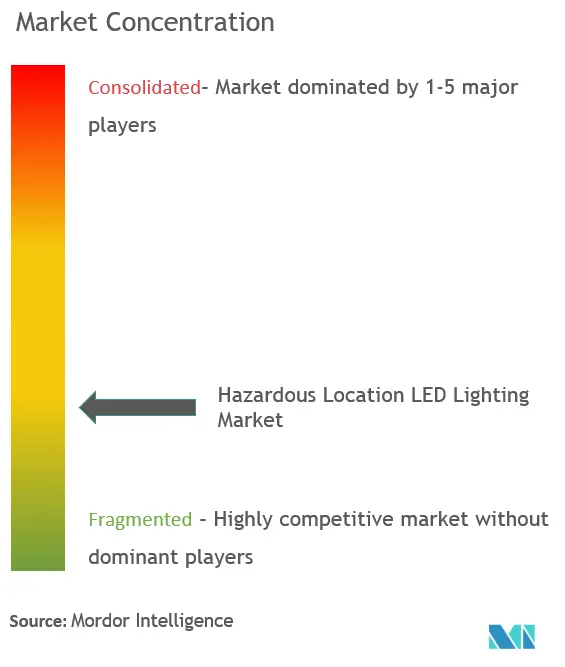

Market Dominated by Global Industrial Conglomerates

The competitive landscape is primarily dominated by large industrial conglomerates with diverse product portfolios, including established players like Emerson, ABB, and Eaton Corporation, who leverage their extensive distribution networks and brand recognition. These major players compete through their technological capabilities, comprehensive product offerings, and ability to provide integrated solutions across multiple industrial applications. Regional specialists and mid-sized companies maintain their market presence through focus on specific geographic markets or specialized application segments, often competing through customized solutions and local market expertise.

The market exhibits moderate consolidation with ongoing merger and acquisition activities aimed at expanding geographic presence and technological capabilities. Companies are increasingly pursuing strategic acquisitions to enhance their product portfolios and gain access to new markets or technologies. Vertical integration strategies are becoming more prevalent as companies seek to control key components of the value chain and ensure product quality. The competitive dynamics are further shaped by the presence of local manufacturers who compete primarily on price points and after-sales service in their respective regional markets.

Innovation and Service Drive Market Success

Success in the hazardous location LED lighting market increasingly depends on the ability to offer comprehensive solutions that combine product innovation with strong service capabilities. Incumbent players are focusing on developing integrated lighting solutions that incorporate advanced features like remote monitoring, predictive maintenance, and energy management capabilities. Market leaders are strengthening their positions through investments in research and development, expanding their distribution networks, and developing closer relationships with end-users through customized solutions and technical support services.

For contenders looking to gain market share, specialization in specific industry verticals or geographic regions offers a viable strategy for growth. The relatively high concentration of end-users in industries such as oil and gas, chemical, and mining provides opportunities for focused market penetration strategies. While substitution risk from traditional lighting solutions is minimal due to regulatory requirements and performance advantages of LED technology, companies must navigate increasingly stringent safety regulations and certification requirements. Success in this market requires maintaining strong relationships with certification bodies and staying ahead of evolving industry standards while managing the cost implications of compliance. Additionally, the integration of explosion-proof LED lighting and harsh environment lighting solutions is becoming crucial to meet the demands of these industries. Companies are also exploring ATEX lighting certifications to ensure compliance with European safety standards.

Hazardous Location LED Lighting Market Leaders

-

DCD Technologies ME FZCO

-

Nemalux Inc.

-

Luceco Middle East FZCO

-

WAROM Technology MENA FZCO

-

Shenzhen CESP Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Hazardous Location LED Lighting Market News

- Jan 2020 - ABB announced plans to launch its smart sensor for rotating machines operating in hazardous areas at Hannover Messe 2020. This new generation of smart sensors may provide high-quality data to enable ABB's advanced analytics to be used in hazardous locations. This product launch may further extend the existing scope of applications for ABB smart sensors with a new generation design for hazardous areas.

- June 2019 - The power management company, Eaton announced its latest product in industrial and hazardous lighting: Crouse-Hinds series CEAG ExLin linear LEDs, certified for Zone 1 and 2 hazardous area environments. The explosion-protected LED fixture provides reliable, energy efficient lighting that can yield cost savings compared to traditional fluorescent fixtures.

Hazardous Location LED Lighting Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Policies

5. TECHNOLOGY SNAPSHOT

6. MARKET DYNAMICS

-

6.1 Market Drivers

- 6.1.1 Regulations Promoting Proper Lighting for Worker Safety in Hazardous Locations

- 6.1.2 Rising Demand for Cost-effective and Energy-efficient LED Lighting Solutions

-

6.2 Market Challenges

- 6.2.1 High Cost of Replacement of Conventional Lamp to LED Lighting Solutions

- 6.3 Assessment of Impact of Covid-19 on the Industry

7. MARKET SEGMENTATION

-

7.1 Class

- 7.1.1 Class I

- 7.1.2 Class II

- 7.1.3 Class III

-

7.2 Device Type

- 7.2.1 Zone 0

- 7.2.2 Zone 20

- 7.2.3 Zone 1

- 7.2.4 Zone 21

- 7.2.5 Zone 2

- 7.2.6 Zone 22

-

7.3 End-User Industry

- 7.3.1 Oil & Gas

- 7.3.2 Petrochemical

- 7.3.3 Industrial

- 7.3.4 Power Generation

- 7.3.5 Pharmaceutical

- 7.3.6 Processing

- 7.3.7 Other End-user Industries

-

7.4 Geography

- 7.4.1 North America

- 7.4.2 Europe

- 7.4.3 Asia Pacific

- 7.4.4 Latin America

- 7.4.5 Middle East and Africa

8. COMPETITIVE LANDSCAPE

-

8.1 Company Profiles

- 8.1.1 DCD Technologies ME FZCO

- 8.1.2 Nemalux Inc.

- 8.1.3 Luceco Middle East FZCO

- 8.1.4 WAROM Technology MENA FZCO

- 8.1.5 Shenzhen CESP Co., Ltd

- 8.1.6 PROLUX International FZ LLC

- 8.1.7 Munira Lighting (AL Hatimi Trading FZE)

- 8.1.8 Emerson FZE (Emerson electric co.)

- 8.1.9 ABB Installation Products Inc.

- 8.1.10 R.Stahl Limited

- 8.1.11 Digital Lumens Inc. (OSRAM)

- 8.1.12 Eaton Corporation

- 8.1.13 Dialight PLC

- 8.1.14 Technology Co., Ltd.

- 8.1.15 Larson Electronics

- 8.1.16 GE Current

- 8.1.17 Hubbell Limited

- 8.1.18 Hilclare Lighting

- 8.1.19 Raytec Ltd.

- 8.1.20 SA Equip

- 8.1.21 Glamox UK

- 8.1.22 IKIO LED Lighting

- 8.1.23 Azz Inc

- 8.1.24 Worksite Lighting LLC

- *List Not Exhaustive

9. INVESTMENT ANALYSIS

10. FUTURE OF THE MARKET

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Hazardous Location LED Lighting Industry Segmentation

The hazardous location LED lighting market is in demand due to the replacement of conventional lighting. Explosion proof lighting is also playing a crucial role in the industrial operations of hazardous locations. From the end user perspective, the increasing oil extraction and refining activities coupled with the growing regional consumption and its growing demand worldwide is further anticipated to propel the growth of the Class I segment.

| Class | Class I |

| Class II | |

| Class III | |

| Device Type | Zone 0 |

| Zone 20 | |

| Zone 1 | |

| Zone 21 | |

| Zone 2 | |

| Zone 22 | |

| End-User Industry | Oil & Gas |

| Petrochemical | |

| Industrial | |

| Power Generation | |

| Pharmaceutical | |

| Processing | |

| Other End-user Industries | |

| Geography | North America |

| Europe | |

| Asia Pacific | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Hazardous Location LED Lighting Market Research FAQs

What is the current Hazardous Location LED Lighting Market size?

The Hazardous Location LED Lighting Market is projected to register a CAGR of 8.86% during the forecast period (2025-2030)

Who are the key players in Hazardous Location LED Lighting Market?

DCD Technologies ME FZCO, Nemalux Inc., Luceco Middle East FZCO, WAROM Technology MENA FZCO and Shenzhen CESP Co., Ltd are the major companies operating in the Hazardous Location LED Lighting Market.

Which is the fastest growing region in Hazardous Location LED Lighting Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Hazardous Location LED Lighting Market?

In 2025, the North America accounts for the largest market share in Hazardous Location LED Lighting Market.

What years does this Hazardous Location LED Lighting Market cover?

The report covers the Hazardous Location LED Lighting Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Hazardous Location LED Lighting Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Hazardous Location LED Lighting Market Research

Mordor Intelligence provides a comprehensive analysis of the hazardous location LED lighting industry. With decades of expertise in industrial LED lighting research, our latest report examines the full range of hazardous area LED lighting solutions. These include flame proof lighting, explosion proof LED lighting, and ATEX lighting systems. This detailed analysis, available as an easy-to-download report PDF, offers crucial insights into safety-certified lighting solutions. It focuses particularly on intrinsically safe lighting technologies and their applications.

The report offers in-depth coverage of various hazard classifications. These include Class 1 Division 1 lighting and Class 1 Division 2 lighting specifications, as well as Zone 1 lighting and Zone 2 lighting requirements. Our analysis encompasses lighting solutions for harsh environment lighting applications, ranging from LED lighting for mining operations to lighting for oil and gas facilities. Stakeholders across the industry value chain can leverage this comprehensive research to understand technical specifications, regulatory requirements, and emerging opportunities in the hazardous location lighting sector.