Haptic Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

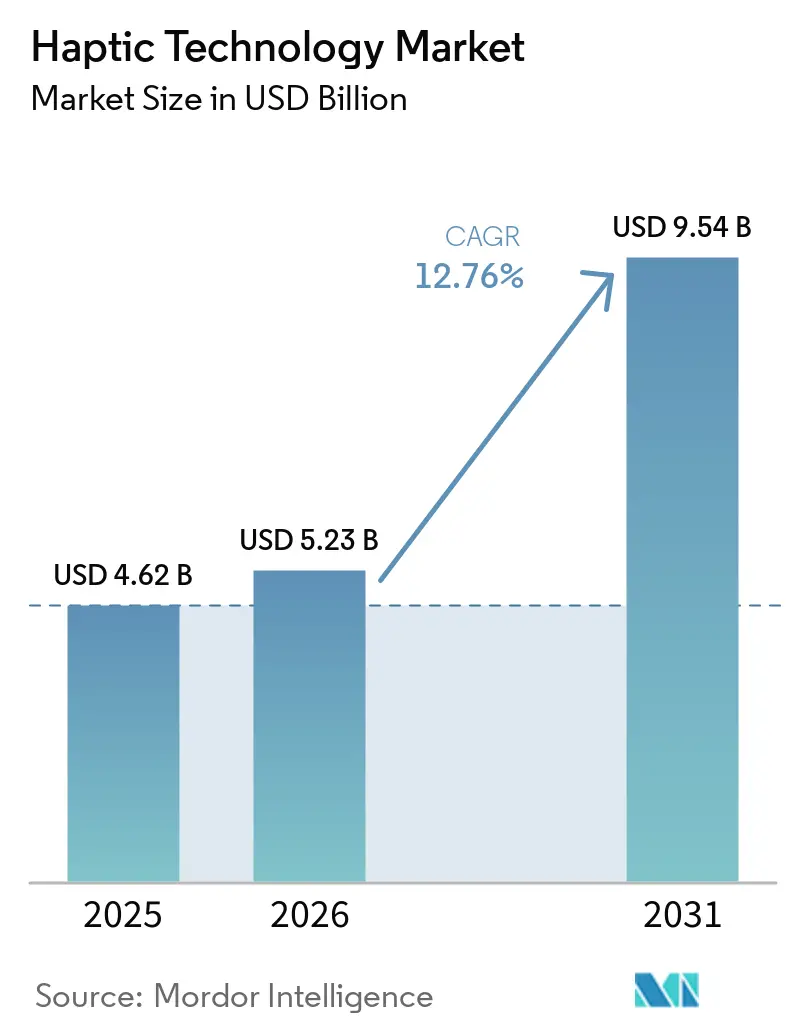

| Market Size (2026) | USD 5.23 Billion |

| Market Size (2031) | USD 9.54 Billion |

| Growth Rate (2026 - 2031) | 12.76% CAGR |

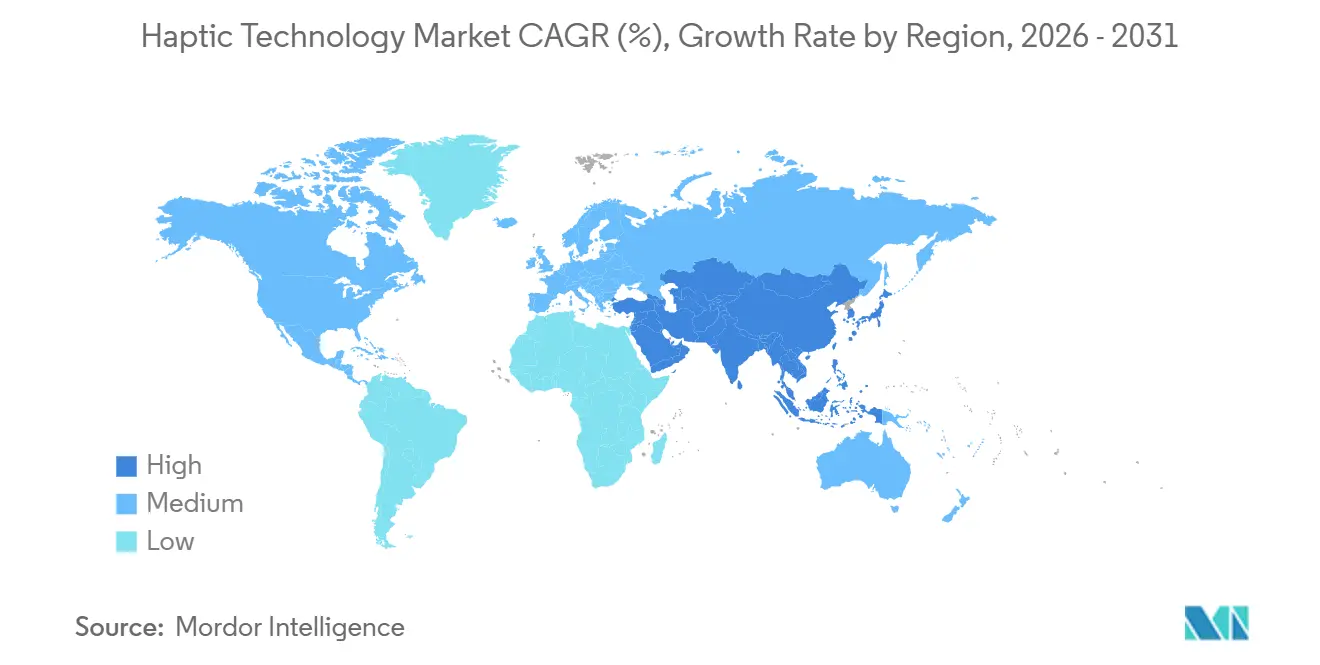

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Haptic Technology Market Analysis by Mordor Intelligence

The haptic technology market size is expected to increase from USD 4.62 billion in 2025 to USD 5.23 billion in 2026 and reach USD 9.54 billion by 2031, growing at a CAGR of 12.76% over 2026-2031. A confluence of smartphone tactile-interface upgrades, automotive advanced driver-assistance systems, extended-reality (XR) hardware proliferation, and gaming peripheral standardization is driving demand across consumer and professional domains. Hardware continues to dominate revenue, yet software is rising as cross-platform authoring tools gain traction. Asia-Pacific remains the volume fulcrum due to concentrated smartphone supply chains, while the Middle East is emerging as the fastest-growing region on the back of sovereign XR programs. Industry standards published in 2024 and 2025 are laying the groundwork for cross-platform content portability, reducing integration friction for developers even as intellectual property (IP) licensing issues persist.

Key Report Takeaways

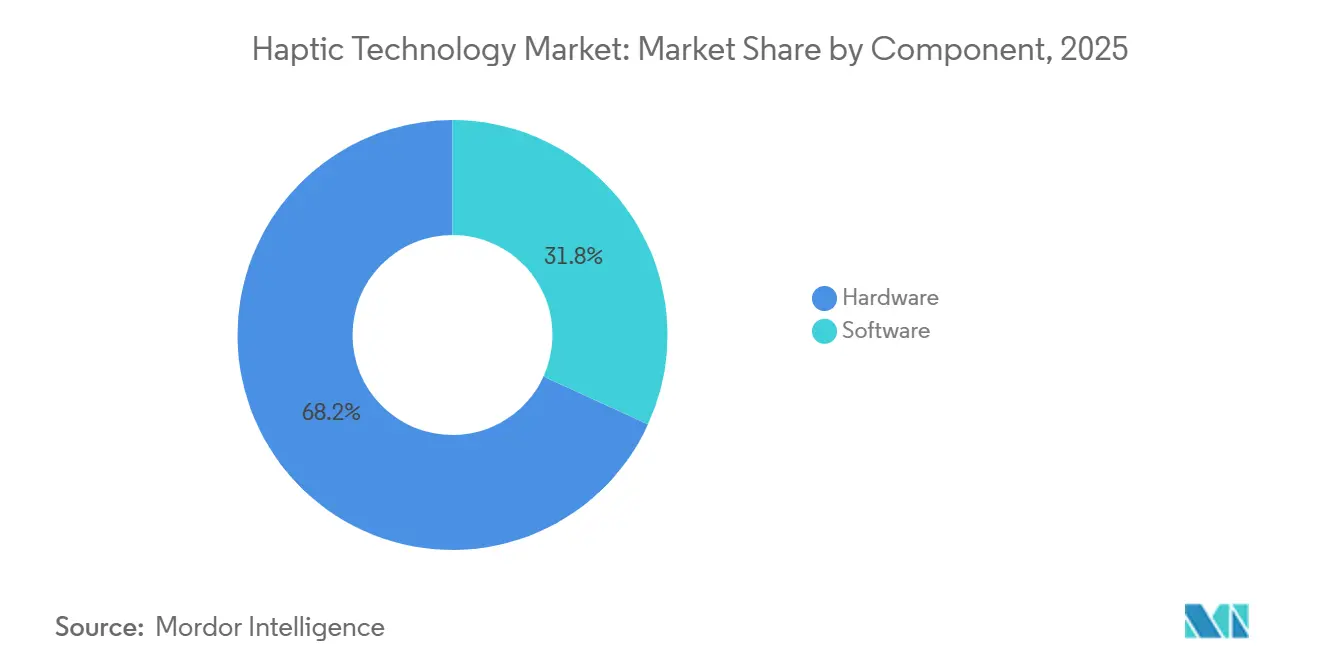

- By component, hardware commanded 68.19% of the haptic technology market share in 2025, reflecting its entrenched position in smartphones and automotive human-machine interfaces, whereas software is projected to expand at a 13.45% CAGR through 2031.

- By application, consumer electronics accounted for 57.49% of 2025 revenue, while gaming and XR devices are forecast to post the fastest growth, with a 13.83% CAGR between 2026 and 2031.

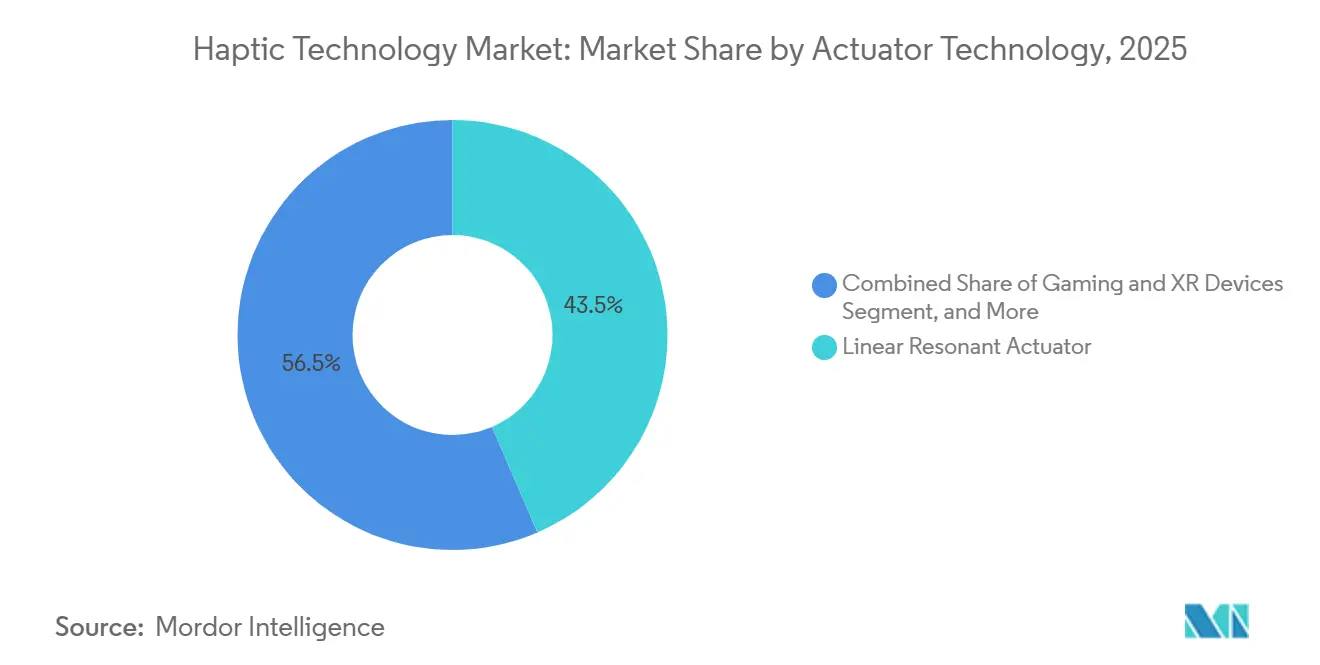

- By actuator technology, linear resonant actuators (LRAs) accounted for 43.54% of revenue in 2025, but piezoelectric actuators are set to grow at a 13.78% CAGR through 2031 as electric-vehicle steer-by-wire systems multiply.

- By feedback type, tactile feedback accounted for 61.33% of revenue in 2025, whereas force and kinesthetic feedback are projected to grow at a 13.41% CAGR, driven by surgical-robotics upgrades and collaborative-robot deployments.

- By geography, Asia-Pacific captured 38.22% of 2025 revenue; in contrast, the Middle East is expected to register a 13.68% CAGR through 2031 owing to large-scale XR initiatives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Haptic Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone Proliferation and Tactile-Rich UX Demand | +3.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Automotive HMIs for ADAS and Safety Alerts | +2.8% | Europe, North America, China | Medium term (2-4 years) |

| XR Hardware Boom (VR/AR/MR Headsets and Gloves) | +2.4% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Gaming Peripherals and Console Haptics Standardization | +1.9% | Global, led by North America, Europe, Japan | Short term (≤ 2 years) |

| MPEG-I and IEEE P1918.1 Standards Enabling Cross-Platform Haptic Content | +1.5% | Global | Long term (≥ 4 years) |

| 5G Tactile-Internet Pilots for Remote Operations | +1.0% | Asia-Pacific, Europe, select Middle East markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smartphone Proliferation and Tactile-Rich UX Demand

Mobile device makers are now embedding multi-actuator arrays that localize feedback to specific on-screen elements, raising user satisfaction scores and aiding accessibility. Flagship platforms feature dual LRAs tuned to different frequency ranges so that keyboards feel crisp, notifications pulse discreetly, and gesture confirmations mimic physical buttons. Foldable form factors benefit from flexible actuators that curve without dampening amplitude, opening new design latitude for upcoming rollable phones. Because replacement cycles continue to lengthen in mature markets, tactile differentiation is emerging as a decisive retention lever. That shift has persuaded original-equipment manufacturers to raise bill-of-materials allocations for haptic subsystems, enhancing per-unit value in the haptic technology market.

Automotive HMIs for ADAS and Safety Alerts

Steer-by-wire and driver-monitoring features rely on vibration pulses and variable-resistance cues delivered through wheels, pedals, and seat structures. Kia deployed steering-wheel haptic warnings in its 2026 model-year vehicles, pulsing the rim when lane-departure or forward-collision systems detect imminent risk, a modality that proved 30% faster than dashboard-icon recognition in controlled studies.[1]Kia Motors, “Steering-Wheel Haptic Warning System,” kia.com Euro NCAP rules taking effect in 2026 require physical climate and hazard controls for a five-star rating, indirectly boosting demand for tactile-confirmed buttons. Premium automakers are also experimenting with adaptive haptic profiles that shift steering feel between comfort and sport modes, deepening software-defined revenue prospects inside connected-car ecosystems.

XR Hardware Boom (VR-AR-MR Headsets and Gloves)

Enterprise and defense segments are fueling next-generation XR rollouts for medical simulation, oil-and-gas training, and remote collaboration. Gloves integrating per-finger force feedback and thermal cues let learners feel tissue tension or hot equipment surfaces inside virtual environments, slashing practical-training hours. Microfluidic skin-displacement arrays achieve sub-3 millimeter resolution, enabling precise texture simulation that improves retention and task accuracy. Middle East governments are subsidizing immersive-learning suites as part of digital-economy initiatives, driving the fastest regional revenue upswing within the haptic technology market. Hardware vendors are, in turn, bundling content-authoring subscriptions that provide recurring software revenue streams.

Gaming Peripherals and Console Haptics Standardization

Console refresh cycles have converged on dual-actuator architectures capable of broad frequency bandwidths, smooth amplitude curves, and adaptive-trigger tension modulation. OpenXR profiles reduce middleware fragmentation, enabling developers to port unified haptic events across gaming PCs, consoles, and XR headsets without rewriting code. Surveys conducted in 2025 reveal that two-thirds of studios now build vibration cues into core gameplay loops, acknowledging that carefully tuned haptics boost player retention and in-game purchase conversion rates. Anticipation of Nintendo’s rumored Switch successor with HD Rumble 2 is spurring a secondary-market upgrade cycle, injecting fresh unit demand into the haptic technology market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Power and Thermal Budgets of Precision Actuators | -1.8% | Global, acute in battery-constrained devices | Short term (≤ 2 years) |

| Bill-of-Materials Cost and Mechanical Design Complexity | -1.5% | Global, particularly cost-sensitive emerging markets | Medium term (2-4 years) |

| Concentrated IP Portfolio, Royalty Exposure to Immersion | -1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Fragmented Cross-Platform Interoperability | -0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Power and Thermal Budgets of Precision Actuators

Piezoelectric stacks and electrostatic films demand elevated drive voltages that drain batteries and create hot spots, pressing engineers to add heat spreaders or scale back feedback intensity. Smartphones with sub-5 millimeter chassis depth face the starkest trade-offs because higher temperatures can throttle central-processing units, degrading overall performance. Wearables share similar constraints, magnified by tiny battery capacities that prioritize Bluetooth and sensor workloads. Automotive cabins endure ambient temperatures above 70 °C, forcing engineers to select materials with high Curie points and to integrate redundant thermal fuses, both of which increase system cost. These limitations slow design-in cycles and temper the short-term growth pace of the haptic technology market.

Bill-of-Materials Cost and Mechanical Design Complexity

Integrating LRAs or piezo plates requires tight mechanical tolerances, shock isolation, and frequency-response calibration, which add weeks to development schedules and increase unit prices. Alps Alpine's Compact Haptic Reactor U-Type, launched for mass production in November 2024, achieved a 90% volume reduction compared to prior-generation linear resonant actuators by vertically stacking the coil and magnet.[2]Alps Alpine Co. Ltd., “Compact Haptic Reactor U-Type Launch,” alpsalpine.com Even compact actuators with 90% volume reduction still carry rare-earth magnets and must be shielded against electromagnetic interference. In automotive steer-by-wire systems, redundant actuators double the component count to meet fail-safe standards, contributing USD 200-300 in incremental cost per vehicle. Smartwatches present an opposite constraint: enclosures leave only millimeters of vertical clearance, so teams must weigh actuator mass against battery size. These cost and complexity hurdles particularly hamper adoption in budget smartphones and emerging markets, restraining penetration rates within the haptic technology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Monetization Trails Hardware Scale

Hardware dominated revenue with a 68.19% haptic technology market share in 2025 because smartphones, automobiles, and gaming consoles require physical actuators and driver ICs in every shipped unit. Although unit growth moderates over time, hardware revenue retains heft thanks to the replacement of eccentric rotating mass motors with faster LRAs and, increasingly, piezoelectric stacks. Software, capturing a smaller slice of the haptic technology market, is on a sharper 13.45% CAGR trajectory through 2031, as cross-platform middleware such as TouchSense and Lofelt shortens development cycles by abstracting device-specific waveform libraries.

The software revenue model remains in flux. Most middleware licenses ride along with actuator procurement, limiting recurring revenue opportunities. To counter that ceiling, vendors are piloting cloud-rendered tactile streams synchronized with audiovisual content, positioning haptic effects as a service similar to spatial-audio libraries. That pivot hinges on solving latency overheads and securing codec support embedded in recent ISO and IEEE standards. If cloud haptics proves viable, software could tilt the overall value pool of the haptic technology market toward higher-margin recurring contracts.

By Feedback Type: Force Sensing Gains in Surgical and Industrial Niches

Tactile modalities, including vibration, skin stretch, and electro-tactile stimulation, accounted for 61.33% of 2025 revenue because of their low power draw and compact footprints, which map neatly onto smartphones and wearables. Yet force and kinesthetic feedback are forecast to outpace tactile, expanding at a 13.41% CAGR as surgical-robot and collaborative-robot installations multiply. Medical systems such as the da Vinci 5 route real-time tissue-resistance vectors back to surgeons, lowering perforation risk and shortening learning curves, while industrial cobots equipped with six-degree-of-freedom force handles yield 25% higher first-pass assembly yields.

Electrotactile interfaces remain laboratory curiosities due to variable skin impedance, which hampers user-to-user consistency. Mid-air ultrasonic arrays, although force-limited, find hygienic niches in automotive infotainment and public kiosks. Skin-stretch devices in premium XR gloves convey shear forces that facilitate virtual texture recognition but still carry premium costs, limiting adoption to enterprise bundles. Overall, the shift toward kinesthetic hardware in specialized domains boosts average selling prices, expanding the haptic technology market even as consumer-electronics volume growth stabilizes.

By Actuator Technology: Piezoelectric Efficiency Challenges LRA Incumbency

Linear resonant actuators held 43.54% of 2025 revenue, benefiting from mature tooling, low cost, and 10-20 millisecond response times suitable for most consumer touchpoints. Piezoelectric actuators, however, are advancing rapidly, projected to grow at a 13.78% CAGR through 2031 as electric-vehicle steer-by-wire mandates reward their 60% lower energy draw and higher bandwidth. Automotive suppliers such as Boréas and TDK have validated piezo stacks that deliver 4 g peak acceleration at moderate voltages, meeting stringent automotive qualification norms.[3]Boréas Technologies, “CapDrive in NIO ET9,” boreas.ca

Eccentric rotating mass motors persist only in low-end feature phones and entry-level wearables, where price ceilings eclipse experiential gains. Ultrasonic mid-air haptics remains a niche, but offers germ-free interaction for medical and public devices. Electrostatic friction modulation films are entering pilot phases for touchscreens that mimic button clicks and surface textures. Continuous yield and cost improvements in piezo ceramics and driver ICs suggest LRAs may cede high-margin automotive and enterprise niches, yet retain share in sub-USD 300 smartphones, maintaining balance in the haptic technology market.

By Application: Gaming and XR Outpace Consumer Electronics Volume

Consumer electronics accounted for 57.49% of revenue in 2025, driven by shipments of more than 1.2 billion smartphones and 200 million smartwatches, with embedded baseline LRAs and MP-Wideband drivers. Despite that volume, growth moderates as replacement cycles elongate. Gaming and XR are the fastest-growing use cases, projected to grow at a 13.83% CAGR, buoyed by adaptive-trigger controllers, motion-simulator peripherals, and enterprise XR training suites. Console makers anchor dual-actuator standards that ripple into third-party racing wheels and VR controllers, while XR gloves bundle enterprise subscriptions that foster recurring revenue within the haptic technology industry.

Automotive growth accelerates as tactile-encoded alerts satisfy upcoming Euro NCAP and Chinese New Car Assessment Program safety norms. Healthcare remains a premium but narrow niche, fetching high unit prices for surgical consoles that add force feedback, underscoring the value of realism in minimally invasive procedures. Industrial teleoperation feeds incremental volumes as cobots migrate onto factory floors in response to aging workforces. Ancillary verticals, including education, smart retail, and defense training, continue to run project-based procurements that have yet to reach mass-production volumes, but they expand the addressable market for haptic technology.

Geography Analysis

Asia-Pacific remained the revenue anchor with a 38.22% share in 2025, sustained by China’s vast smartphone-assembly clusters in Shenzhen and Dongguan, Japan’s piezoelectric ceramics leadership, and South Korea’s display-integrated module know-how. The region where Japanese shipments of tactile and force sensors will grow 18% annually through 2030, propelled by demand for collaborative robots in electronics and medical equipment. Chinese electric-vehicle production exceeding 9 million units in 2025 is driving the insertion of LRAs and piezo stacks into steering wheels and touch consoles, keeping regional component makers at capacity. Korean companies are riding the wave of foldable-phone adoption, embedding curved actuators that function across 180-degree bends without degrading haptic intensity.

The Middle East is forecast to post the fastest CAGR of 13.68% through 2031, catalyzed by Saudi Vision 2030 investments that fund VR medical and defense simulators and by the United Arab Emirates’ procurement of XR workforce-training modules. Israel’s defense contractors are fielding haptic-enabled unmanned-vehicle stations that cut mission failure rates, diversifying applications beyond consumer devices. Qatar-based startups securing 2026 funding for VR medical courses demonstrate home-grown expansion that complements imported hardware, collectively uplifting the haptic technology market size in the region.

North America and Europe maintain steady mid-single-digit CAGRs on the back of ADAS mandates, surgical-robot installations, and console refresh cycles, although smartphone saturation places a ceiling on upside. Apple’s multiyear USD 500 billion domestic investment, which doubles its Advanced Manufacturing Fund, underlines continued R&D focus on custom actuator design that minimizes third-party royalties. Texas Instruments’ USD 60 billion analog-fab expansion secures local supply chains for driver ICs, buffering geopolitical shocks. Euro NCAP’s 2026 requirement for tactile-verified climate and hazard controls reverses earlier touchscreen-only trends, set to stimulate demand for haptic-equipped mechanical buttons, particularly among premium German marques. South America and Africa trail because of import tariffs and lower purchasing power, yet rising smartphone penetration keeps a simmering baseline for future growth in the haptic technology market.

Competitive Landscape

Immersion Corporation commands the most extensive IP portfolio, with around 400 issued patents spanning waveform algorithms and surface-encoding techniques that generated healthy licensing revenue in 2025.[4]U.S. SEC, “Immersion Corporation 2025 Form 10-K,” sec.gov Ongoing litigation against major device makers underscores the leverage intrinsic to hard-to-design-around vibration patents. Apple and Samsung circumvent royalty exposure by vertically integrating Taptic Engines and proprietary LRAs, but that insularity hampers cross-platform compatibility and complicates third-party app support.

Component suppliers, including AAC Technologies, Alps Alpine, TDK, and Texas Instruments, compete on miniaturization, power efficiency, and automotive qualification. Alps Alpine’s U-Type LRA delivered a 90% volume reduction while meeting 8,000-cycle durability targets, illustrating incremental gains that keep LRAs relevant. Piezo specialist Boréas Technologies is leveraging 60% energy savings and finer bandwidth control to win steer-by-wire slots in Chinese electric vehicles, signaling a potential pivot point if cost curves cooperate. Ultraleap, the leading ultrasonic mid-air pioneer, partners with automotive tier-ones to integrate touchless infotainment controls into high-end dashboards, delivering a hygiene value proposition.

Industry standards loom large in shaping future competition. ISO/IEC 23090-31 and IEEE 1918.1.1-2024 codify parametric and wavelet encoding that, once widely adopted, could lower switching costs between actuator types and soften lock-in advantages of entrenched vendors. Ecosystem fragmentation persists, however, because automotive and medical OEMs still rely on proprietary firmware stacks tied to specific hardware suppliers. As cloud-streamed haptics matures, service providers may emerge that bypass device-resident libraries altogether, potentially redrawing the revenue map of the haptic technology market.

Haptic Technology Industry Leaders

Immersion Corporation

AAC Technologies Holdings Inc.

Alps Alpine Co., Ltd.

Ultraleap Holdings Ltd.

TDK Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: NTT DOCOMO and Keio University demonstrated 5G-enabled robot teleoperation with Real Haptics at Mobile World Congress Barcelona, achieving 40% higher force-feedback accuracy versus 4G.

- March 2026: TDK Corporation expanded U.S. sensor production for Apple, supporting rising demand for Taptic Engine components in iPhones and Apple Watches.

- January 2026: Qatar-based iQtech secured Series A funding to deploy haptic-enabled VR surgical simulators across Gulf Cooperation Council medical schools.

- November 2025: Alps Alpine began mass production of its Compact Haptic Reactor U-Type, cutting volume 90% relative to prior LRAs.

Global Haptic Technology Market Report Scope

The haptic technology market is the global industry focused on the development, production, and integration of technologies that enable tactile and force-based feedback to simulate the sense of touch across digital and physical interfaces. These systems enhance user interaction by providing realistic sensations such as vibration, pressure, texture, and motion, thereby improving immersion, control, and user experience across a wide range of devices and applications.

The Haptic Technology Market Report is Segmented by Component (Hardware, and Software), Feedback Type (Tactile, and Force/Kinesthetic), Actuator Technology (ERM Motors, LRA, Piezoelectric, Ultrasonic, and Electrostatic Films), Application (Consumer Electronics, Gaming and XR, Automotive, Healthcare, Industrial, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Tactile (Vibration, Skin-Stretch, Electro-Tactile) |

| Force / Kinesthetic |

| Eccentric Rotating Mass (ERM) Motors |

| Linear Resonant Actuators (LRA) |

| Piezoelectric Actuators |

| Ultrasonic / Mid-Air Ultrasound |

| Electrostatic and Electro-Hydrodynamic Films |

| Consumer Electronics (Smartphones, Wearables, Tablets, PCs) |

| Gaming and XR Devices |

| Automotive and Transportation (HMI, ADAS, Infotainment) |

| Healthcare and Medical Devices |

| Industrial and Robotics |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | |

| Software | ||

| By Feedback Type | Tactile (Vibration, Skin-Stretch, Electro-Tactile) | |

| Force / Kinesthetic | ||

| By Actuator Technology | Eccentric Rotating Mass (ERM) Motors | |

| Linear Resonant Actuators (LRA) | ||

| Piezoelectric Actuators | ||

| Ultrasonic / Mid-Air Ultrasound | ||

| Electrostatic and Electro-Hydrodynamic Films | ||

| By Application | Consumer Electronics (Smartphones, Wearables, Tablets, PCs) | |

| Gaming and XR Devices | ||

| Automotive and Transportation (HMI, ADAS, Infotainment) | ||

| Healthcare and Medical Devices | ||

| Industrial and Robotics | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is forecast for the haptic technology market through 2031?

The haptic technology market is projected to grow at a 12.76% CAGR between 2026-2031.

Which component segment is expanding faster, hardware or software?

Software is on a steeper 13.45% CAGR, while hardware continues to hold the majority of revenue.

Why are piezoelectric actuators gaining traction in vehicles?

They consume about 60% less power than LRAs, meeting energy-efficiency goals in electric-vehicle steer-by-wire systems.

Which region is expected to grow the quickest?

The Middle East leads with an anticipated 13.68% CAGR to 2031, driven by large-scale XR investments.

How are recent standards affecting cross-platform haptics?

ISO/IEC 23090-31 and IEEE 1918.1.1-2024 provide unified codec baselines, easing content portability and lowering integration costs.

What is the primary restraint for premium haptic actuators in smartphones?

Elevated power draw and resulting thermal load challenge battery life in ultra-thin handheld designs.

Page last updated on: