Hair Restoration Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

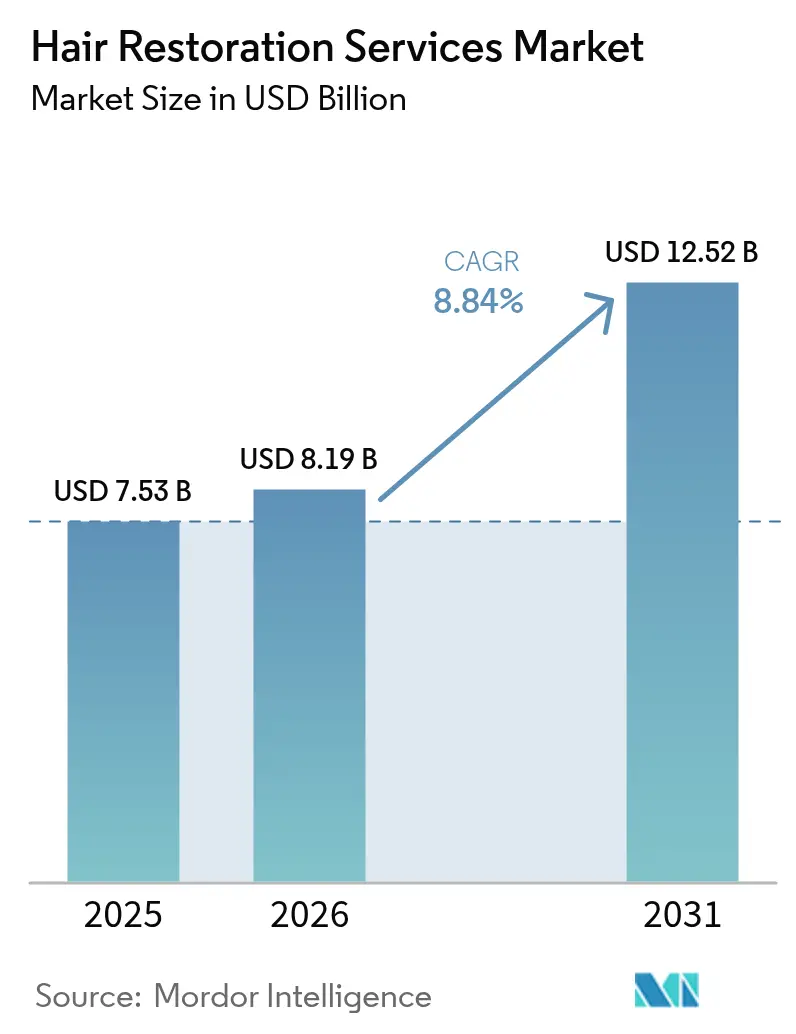

| Market Size (2026) | USD 8.19 Billion |

| Market Size (2031) | USD 12.52 Billion |

| Growth Rate (2026 - 2031) | 8.84% CAGR |

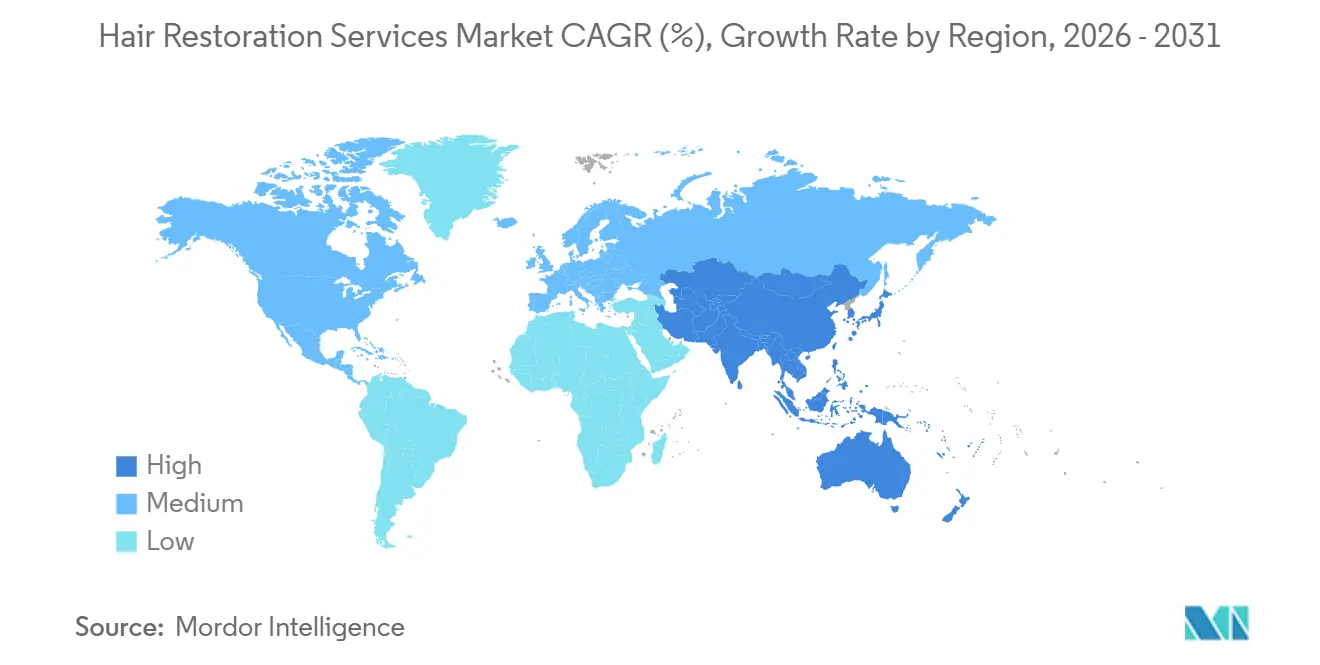

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hair Restoration Services Market Analysis by Mordor Intelligence

The Hair Restoration Services Market size is expected to grow from USD 7.53 billion in 2025 to USD 8.19 billion in 2026 and is forecast to reach USD 12.52 billion by 2031 at 8.84% CAGR over 2026-2031.

Rising prevalence of androgenetic alopecia, the clinical validation of minimally invasive follicular unit extraction (FUE) and robotic systems, and the growing acceptance of aesthetic procedures among younger adults collectively underpin this growth trajectory. Momentum is driven by the clinical success of regenerative compounds such as Pelage Pharmaceuticals’ PP405, next-generation devices like the ARTAS iXi robot with 44-micron resolution, and a widening pool of prospective patients aware of permanent, confidence-enhancing outcomes. Wider social acceptance, influencer visibility, and flexible payment plans are accelerating first-time procedures among adults aged 26-35, while device-based adjuncts such as FoLix fractional laser therapy extend care to consumers unwilling or unfit for surgery. Parallel growth in medical tourism, notably to Turkey and India, lowers cost barriers and adds volume, whereas supportive regulation, evident in the FDA’s Class II rules for scalp-cooling systems, signals institutional recognition of hair loss as a quality-of-life issue.[1]U.S. Food & Drug Administration, “Class II Special Controls for Scalp Cooling Systems,” fda.gov

Key Report Takeaways

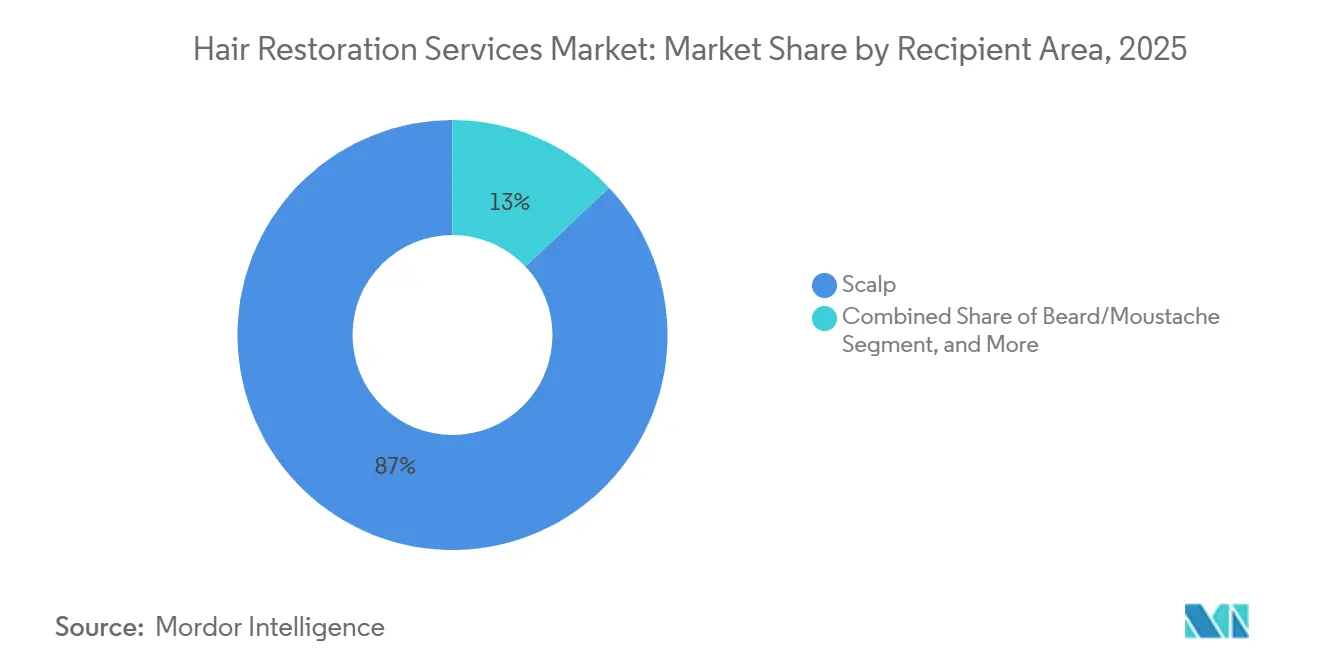

- By recipient area, scalp procedures accounted for 87.02% of the hair restoration services market share in 2025, while eyebrow restoration is projected to grow at a 10.22% CAGR through 2031.

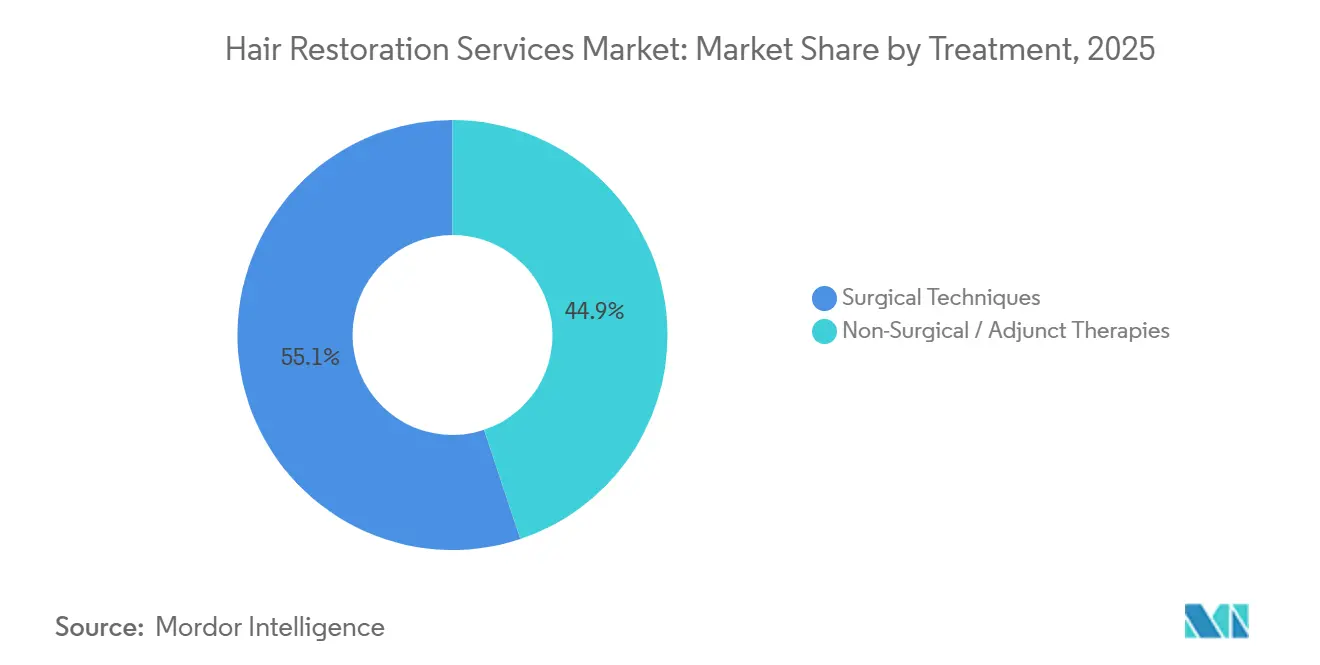

- By treatment, surgical techniques commanded 55.12% of the hair restoration services market in 2025; non-surgical therapies are forecast to grow at a 11.04% CAGR through 2031.

- By end user, specialty hair clinics captured 62.45% of the revenue share in 2025, whereas medical spas are expanding at a 11.20% CAGR through 2031.

- By geography, North America led the hair restoration services market with a 40.05% share in 2025, while Asia-Pacific is set to post the fastest 9.44% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hair Restoration Services Market Trends and Insights

Driver Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing global burden of alopecia and hair loss disorders | +1.8% | Global, with higher prevalence in North America and Europe | Long term (≥ 4 years) |

| Rising disposable income and willingness to spend on aesthetic procedures | +1.5% | Asia-Pacific core, spill-over to Middle East and South America | Medium term (2–4 years) |

| Continuous technological advancements in surgical and non-surgical hair restoration | +2.1% | North America and Europe lead adoption, Asia-Pacific follows | Medium term (2–4 years) |

| Expansion of specialized hair transplant clinics and franchise chains | +1.3% | Global, rapid growth in Turkey, India, and UAE | Short term (≤ 2 years) |

| Increasing acceptance of cosmetic tourism for cost-effective procedures | +1.6% | Turkey, India, Thailand as destinations; demand from Europe, Middle East, North America | Short term (≤ 2 years) |

| Proliferation of social media marketing and influencer endorsements | +1.2% | Global, strongest impact in North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Global Burden of Alopecia and Hair Loss Disorders

Androgenetic alopecia now afflicts up to 50% of adults worldwide, a prevalence climbing as dihydrotestosterone (DHT) sensitivity intensifies across generations. More than 700,000 hair restoration procedures were performed globally in 2024, up 16% from 2016, underscoring unmet clinical need.[2]American Med Spa Association, “2024 Medical Aesthetics State of the Industry Report,” americanmedspa.org Younger patients aged 26-35 are acting earlier, generating higher lifetime procedure demand and improving compliance with maintenance regimens. Expanding research into autoimmune-related alopecia and chemotherapy-induced hair loss enlarges the candidate pool beyond traditional male pattern baldness. As populations age in high-income countries, awareness, affordability, and access combine to keep demand on a steep upward curve. Androgenetic alopecia affects about 50% of men by age 50 and 15% of women, creating a persistent demand pool that enlarges as populations age and diagnostic awareness improves. Patients aged 25-35 already account for nearly 40% of consultations at specialty clinics, indicating earlier intervention driven by workplace visibility and social media self-presentation.

Rising Disposable Income and Willingness to Spend on Aesthetic Procedures

Disposable income growth in the United States, Germany, China, and Gulf Cooperation Council economies is steering healthcare dollars toward appearance-enhancing services. First-time transplant patients now average 26-35 years old, when surgery is simpler and yields superior density over time. Consumer surveys indicate 77% of decisions are career- or relationship-motivated, equating fuller hair with social capital. Financed payment plans, zero-interest clinic loans, and buy-now-pay-later apps expand affordability to middle-income cohorts.

Continuous Technological Advancements in Surgical and Non-Surgical Restoration

Robotic systems have reduced harvesting error rates below 2% and increased extraction speeds to 700 grafts per hour, making large sessions feasible in a single day. Pelage Pharmaceuticals’ PP405 delivered >20% density gains in 31% of recipients within eight weeks during Phase 2a trials, reinforcing a regenerative pivot away from symptom-management. The University of Sheffield’s deoxyribose sugar gel replicated minoxidil-level efficacy in preclinical work, hinting at a topical with fewer side effects.[3]University of Sheffield, “Sugar Molecule Promotes Hair Growth,” sheffield.ac.uk FDA-cleared FoLix fractional laser broadens non-invasive choices and creates a bridge for medical spas lacking surgical capacity. PRP, exosomes, and combination therapy regimens now yield higher survival and faster growth than monotherapy, optimizing both patient experience and clinic revenue.

Increasing Acceptance of Cosmetic Tourism for Cost-Effective Procedures

Turkey performs follicular unit extraction (FUE) at USD 3,500-8,000 versus USD 7,500-15,000 in the United States without compromising on JCI-accredited facilities. India’s comparable range of USD 3,000 effectively halves the price tag for Western patients, a spread that persists even when factoring flights and lodging. Integrated travel-surgery packages cover consultation, airport transfers, and follow-up visits, reducing logistical uncertainty. Tele-consultation lets surgeons preapprove candidates remotely, compressing stay durations to under one week. Accreditation and surgeon-certification programs mitigate historical safety concerns, accelerating patient mobility for premium robotic or ethnic-specific techniques.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High procedure costs and limited reimbursement coverage | -1.4% | North America and Europe primarily, moderate in Asia-Pacific | Long term (≥ 4 years) |

| Shortage of skilled hair transplant surgeons | -0.9% | Global, acute in North America and Europe | Medium term (2–4 years) |

| Post-operative risks and variable success rates | -0.7% | Global, higher concern in unregulated markets | Medium term (2–4 years) |

| Availability of less-invasive cosmetic alternatives | -0.6% | North America and Europe lead adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure Costs and Limited Reimbursement Coverage

Surgical outlays at USD 4,000-15,000 in developed regions remain prohibitive, while private insurers classify hair transplantation as elective, leaving patients to self-fund. The disparity is sharper in emerging markets where per-capita income trails procedure fees, even as awareness rises. Financing plans and third-party credit mitigate sticker shock, yet many prospects delay treatment, risking further follicular miniaturization. Medical tourism narrows cost gaps but adds travel costs that can offset savings for intra-regional patients. Meanwhile, device-based therapies such as low-level laser caps enter the market below USD 1,000, offering an entry point for price-sensitive consumers but diverting some volume from surgical channels.

Shortage of Skilled Hair Transplant Surgeons

Modern FUE and robotic workflows require a learning curve of 800-1,000 cases to reach peak proficiency, slowing the pipeline of qualified practitioners. Demand in Asia-Pacific and Latin America often outstrips local training capacity, prompting clinics to import surgeons on rotation or pursue franchising to leverage scarce expertise. Robotic extraction lowers dependence on manual dexterity, yet expert oversight for design and implantation remains mandatory. Inadequate training occasionally fuels substandard results, jeopardizing reputation and prompting tighter licensing rules in India, Thailand, and Brazil. Remote mentoring via augmented-reality headsets is emerging as a stopgap, but widespread adoption awaits higher bandwidth and legal clarity on cross-border medical supervision.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Recipient Area: Scalp Dominance Drives Volume

Scalp procedures accounted for 87.02% of the Hair Restoration Services market in 2025, reflecting the prevalence of androgenetic alopecia and well-established surgical protocols. Eyebrow restoration, propelled by social media beauty standards, is forecast to expand at a 10.22% CAGR and diversify clinic revenue beyond traditional male segments. Beard procedures hold niche appeal among millennials seeking a fuller facial aesthetic, while eyelash and body-hair work remains limited by donor-hair scarcity and surgical complexity. Robotic direct-hair-implantation (DHI), designed for Afro-textured follicles, unlocks underserved demographic clusters, sharpening competitive positioning for clinics that adopt early. Growing awareness among female patients and advanced micropunch tools decreases downtime and scarring, reinforcing scalp surgery’s centrality yet widening the portfolio of high-margin facial services.

By Treatment: Surgical Leadership Meets Non-Surgical Innovation

Surgical techniques accounted for 55.12% of 2025 revenue, with FUE surpassing follicular-unit transplantation on the strength of minimal scarring and robotic precision, which are linked to 98% graft survival. Direct Hair Implantation’s no-touch approach is gaining traction through specialized franchises promising faster recovery. In parallel, non-surgical modalities, such as PRP, exosome solutions, and low-level laser helmets, are projected to post an 11.04% CAGR, fueled by patients wary of anesthesia or downtime. The hair restoration services market size for combination surgery-plus-PRP packages is on track to rise 11.70% annually as clinicians prove synergistic density gains.

Stem-cell and exosome injections, though investigational, are available in loosely regulated markets at USD 3,000-5,000 per dose, exploiting patients' desire for cutting-edge solutions. For clinics, selling adjunct packages elevates average revenue per patient and counters lengthening revisit cycles. This hybrid model expands the hair restoration services market by monetizing both the surgical and maintenance phases of the patient journey.

By End-User: Medical Spas Disrupt Traditional Clinic Models

Specialty hair clinics retained 62.45% of global revenue in 2025 by pairing surgeon expertise with capital-intensive tools such as USD 500,000 ARTAS robots, thereby delivering premium outcomes that justify higher price points. Franchise chains standardize protocols and marketing, allowing rapid rollouts into secondary cities while maintaining quality. Multispecialty hospitals remain a steady channel for combined cosmetic procedures, but grow more slowly due to longer capital-approval cycles.

Medical spas and wellness centers are the breakout channel, expanding at 11.20% CAGR by leveraging FDA-cleared devices and lifestyle-oriented branding that resonates with younger, wellness-focused clients. Service menus bundle hair regrowth with skin and body treatments, raising average spend per visit without requiring surgical accreditation. Ambulatory surgery centers offer cost-optimized packages for routine FUE, facilitating capacity expansion in regions lacking full-service clinics. Together, these shifts underscore a decentralizing map in which Hair Restoration Services market access broadens beyond traditional hospital corridors into consumer-friendly venues.

Geography Analysis

North America led the Hair Restoration Services market with a 40.05% share in 2025, buoyed by high income and early adoption of AI-assisted robotics. United States clinics such as Bosley have diversified into fractional laser and exosome add-ons, deepening wallet share per patient. Canada’s favorable medical-device approval pathway catalyzes cross-border patient inflow seeking newer technologies unavailable elsewhere. Reimbursement gaps persist, but third-party financing and employer wellness stipends soften cost obstacles.

Europe represents a mature yet innovative arena. Germany mandates specialized certification for PRP and device operators, raising quality while compressing provider counts. Patient flows run both ways: cost-conscious Germans travel to Istanbul for budget FUE, whereas Gulf residents fly to Berlin for combined transplant-plus-filler packages. Smile Hair Clinic’s 2025 expansion into Hamburg signals confidence in premium European demand. EU vigilance on advertising standards ensures transparent outcome claims, bolstering trust in the Hair Restoration Services market.

Asia-Pacific is the growth engine with a 9.44% CAGR projection. China has more than 3,000 transplant providers, yet consolidation pressures are elevating quality as consumers favor branded networks over mom-and-pop rooms. India leverages English-language teleconsultations and pricing at one-quarter U.S. levels to draw Westerners chasing affordability. Turkey, though technically in Europe, serves APAC, MEA, and U.S. clients alike, illustrating geographic crossover. Afro-hair optimized robotics debuting in Istanbul, and Lagos, widens inclusion and fortifies medical-tourism positioning. Government agencies in Thailand and South Korea now target cosmetic-tourism visas, formally integrating hair restoration into national health-export strategies. Collectively, these factors align to expand the Hair Restoration Services market beyond historical Western confines.

Competitive Landscape

The hair restoration services market is moderately fragmented: the top five providers account for roughly 28% of global revenue, leaving room for venture-backed entrants. Strategic alliances typify competitive moves, as seen in Bosley’s licensing of Lumenis FoLix to capture non-surgical clientele and Venus Concept’s purchase of Restoration Robotics to fuse hardware and service revenue. Biotech pipelines teem with more than 100 investigational molecules; Pelage Pharmaceuticals’ USD 75 million Series B underscores capital appetite for first-in-class regenerative therapies. Patent fortification is another front: Pola Chemical’s follicle organoid claims could lock competitors out of lab-grown grafts for a decade.

Digital platforms emerge as soft disruptors, matching patients to clinics through AI diagnostics, virtual try-ons, and outcome simulators. Clinics adopting omnichannel engagement online consult, in-person surgery, and device-based aftercare report 15% higher conversion. Cost-efficient med-spa chains pressure premium clinics on volume pricing, while outcome-guarantee models gain popularity among high-net-worth patients. Regulatory depth remains a barrier; FDA pre-submission timelines and CE marking costs favor incumbents with established quality systems.

Hair Restoration Services Industry Leaders

Illumiflow

NovaGenix

Theradome Inc.

Venus Concept Inc.

Apira Sciences Inc. (iGrow)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Dr. Serkan Aygın Clinic in Istanbul expanded its all-inclusive hair transplant packages for international travelers, reinforcing Turkey’s leadership in bundled medical tourism.

- September 2025: MedPark Hospital launched a dedicated Hair Restoration Center offering FUE, FUT, and combination protocols supported by a multidisciplinary team.

- February 2025: Smile Hair Clinic entered the German market, marking its first Western European site.

Global Hair Restoration Services Market Report Scope

As per the scope of the report, hair restoration is a procedure in which the hair is moved from the back and sides of the scalp, where the hair is permanent (donor area), to the areas that are thinning or bald on the front, top, or crown of the scalp (recipient area). Once transplanted, the hair is likely to grow normally.

The hair restoration market is segmented by recipient area, treatment, end users, and geography. By recipient area, the market is segmented into scalp and non-scalp. By treatment, the market is segmented into follicular unit extraction (FUE), follicular unit transplant (FUT), laser therapy, stem cell therapy, and other treatments. By end user, the market is segmented into hospitals, clinics, and other end users). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers the market size in value terms in USD for all the abovementioned segments.

| Scalp |

| Beard / Moustache |

| Eyebrows |

| Eyelashes |

| Other Body Areas |

| Surgical Techniques | Follicular Unit Extraction (FUE) |

| Follicular Unit Transplant (FUT) | |

| Direct Hair Implantation (DHI) | |

| Robotic FUE | |

| Non-Surgical / Adjunct Therapies | Low-Level Laser Therapy (LLLT) |

| Platelet-Rich Plasma (PRP) | |

| Stem-Cell & Exosome Therapy | |

| Topical & Injectable Adjuvants |

| Specialty Hair Clinics |

| Multispecialty Hospitals |

| Ambulatory Surgical Centers |

| Medical Spas & Wellness Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Recipient Area | Scalp | |

| Beard / Moustache | ||

| Eyebrows | ||

| Eyelashes | ||

| Other Body Areas | ||

| By Treatment | Surgical Techniques | Follicular Unit Extraction (FUE) |

| Follicular Unit Transplant (FUT) | ||

| Direct Hair Implantation (DHI) | ||

| Robotic FUE | ||

| Non-Surgical / Adjunct Therapies | Low-Level Laser Therapy (LLLT) | |

| Platelet-Rich Plasma (PRP) | ||

| Stem-Cell & Exosome Therapy | ||

| Topical & Injectable Adjuvants | ||

| By End-User | Specialty Hair Clinics | |

| Multispecialty Hospitals | ||

| Ambulatory Surgical Centers | ||

| Medical Spas & Wellness Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the hair restoration services market in 2026?

The hair restoration services market size stands at USD 8.19 billion in 2026.

What is the projected growth rate for Hair Restoration Services to 2031?

Revenue is forecast to expand at an 8.84% CAGR, reaching USD 12.52 billion by 2031.

Which geographic region is growing fastest for hair-restoration demand?

Asia-Pacific is set to grow at the highest 9.44% CAGR through 2031, driven by rising incomes and medical tourism.

What segment currently dominates recipient-area procedures?

Scalp treatments lead with 87.02% share of global procedures.

Are non-surgical therapies gaining traction?

Yes, non-surgical modalities such as PRP, laser, and regenerative compounds are forecast to grow at 11.04% CAGR.

Why do patients travel abroad for hair transplants?

Comparable quality at 50-70% lower fees motivates travel to hubs like Turkey and India.

Page last updated on: