Hair Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 82.5 Billion |

| Market Size (2031) | USD 108.59 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

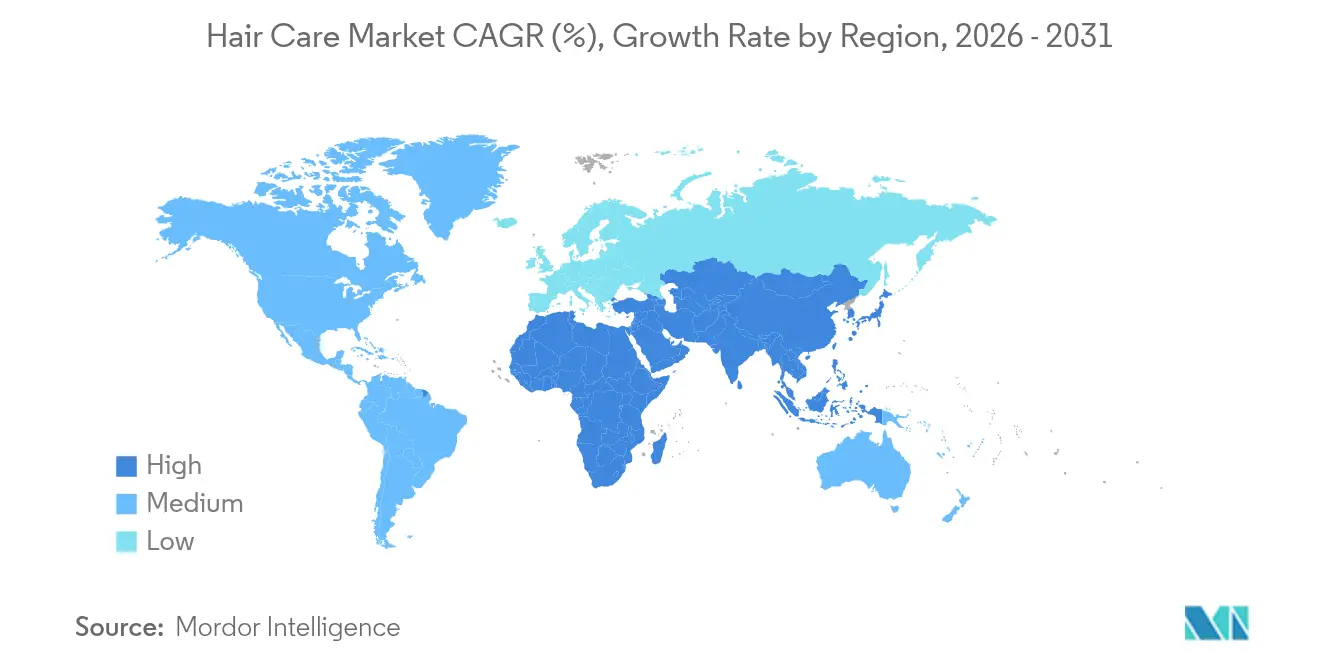

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

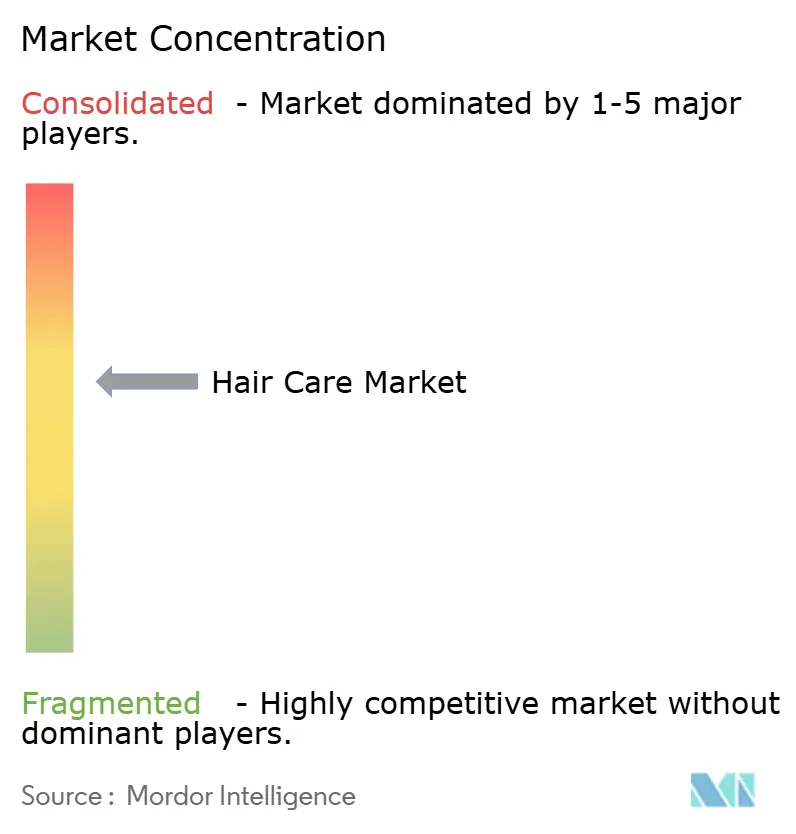

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hair Care Market Analysis by Mordor Intelligence

Hair care market size in 2026 is estimated at USD 82.5 billion, growing from 2025 value of USD 78.06 billion with 2031 projections showing USD 108.59 billion, growing at 5.69% CAGR over 2026-2031. This growth is primarily driven by the increasing awareness among consumers regarding the ingredients used in hair care products, the implementation of stricter safety regulations, and the rising popularity of salon-quality hair care routines that can be performed at home. These factors are encouraging consumers to invest in high-quality products that align with their preferences and safety standards. Companies that can quickly adapt to new allergen restrictions, provide evidence of clinical efficacy, and incorporate artificial intelligence (AI) diagnostics into their offerings are successfully capturing a larger share of premium consumer spending. At the same time, consolidation among multinational corporations is creating significant entry barriers for smaller, independent competitors. However, opportunities continue to emerge in niche areas such as scalp health, ingestible supplements, and clean formulations, which cater to evolving consumer demands. Despite these opportunities, the market faces certain challenges, including rising compliance costs due to regulatory requirements, inflationary pressures on raw material prices, and growing consumer fatigue with subscription-based models. Nevertheless, these challenges are outweighed by the structural demand for preventive wellness solutions and personalized hair care experiences, which continue to drive the market forward.

Key Report Takeaways

- By revenue stream, services held 72.88% of hair care market share in 2025, while products are forecast to grow at a 7.21% CAGR through 2031.

- By end use, female consumers commanded 66.45% of the 2025 total and are expected to post the fastest 6.72% CAGR to 2031.

- By structure, independent salons led with 61.10% share in 2025, but chained salons are on track for a 7.02% CAGR through 2031.

- By geography, North America dominated with 38.20% in 2025, whereas Asia-Pacific is projected to record the quickest 6.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hair Care Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ingredient-conscious consumers prefer sulfate-free, silicone-free, and low-toxicity premium hair care products | +1.2% | Global, with North America and Europe leading adoption; Asia-Pacific following | Medium term (2-4 years) |

| Increased awareness of pollution and ultraviolet damage drives demand for protective hair care products | +0.8% | Asia-Pacific core (China, India, Japan), spillover to Middle East and Africa | Medium term (2-4 years) |

| Professional-grade treatments like bond-repair and keratin boost salon applications and maintenance product demand | +1.5% | Global, with North America and Europe accounting for majority of salon spend | Short term (≤ 2 years) |

| High usage of hair coloring services increases visits and sales of color-care products | +1.0% | North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Personalization through scalp analysis and artificial intelligence supports customized product regimens and services | +0.9% | Global, with early adoption in North America, Japan, and South Korea | Medium term (2-4 years) |

| Subscription models for hair care products enhance recurring revenue streams for businesses | +0.6% | North America and Europe; emerging in Asia-Pacific urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ingredient-conscious consumers prefer sulfate-free, silicone-free, and low-toxicity premium hair care products

Clean beauty mandates are reshaping formulation priorities as consumers increasingly scrutinize ingredient labels with the same attention previously given to food products. The United States Food and Drug Administration (FDA) Modernization of Cosmetics Regulation Act, effective from July 2024, requires manufacturers to substantiate product safety, register facilities, and report adverse events. This regulation raises the entry barrier for brands lacking comprehensive toxicology data [1]Source: U.S. Food & Drug Administration, “Compliance Policy for Cosmetic Product Facility Registration and Cosmetic Product Listing,” fda.gov. Brands such as Living Proof and Briogeo have adapted to this shift by promoting sulfate-free and silicone-free formulations, appealing to health-conscious millennials and Generation Z consumers who associate synthetic polymers with scalp irritation and environmental concerns. The natural and organic personal care market is experiencing moderate annual growth; however, premium hair care segments within this category are achieving double-digit growth. This growth is driven by the positioning of botanical actives, such as niacinamide, peptides, and hyaluronic acid, as science-backed alternatives to traditional silicones. Additionally, state-level restrictions in California and New York on formaldehyde-releasing preservatives and certain phthalates are accelerating reformulation efforts. These regulations are prompting brands to invest in preservative systems that ensure shelf stability while avoiding regulatory or consumer pushback. Ingredient transparency has transitioned from a niche demand to a baseline expectation, distinguishing premium brands from mass-market competitors.

Increased awareness of pollution and Ultraviolet damage drives demand for protective hair care products

Urban pollution and ultraviolet exposure are increasingly important concerns for consumers living in densely populated Asian cities. Particulate matter and ozone contribute to the degradation of hair cuticles and accelerate color fading. The anti-pollution ingredients market for personal care is growing as brands focus on incorporating chelating agents, antioxidants, and film-forming polymers to protect hair from environmental damage. In China and India, where air quality indices often exceed World Health Organization (WHO) guidelines, there is a rising demand for pre-shampoo treatments and leave-in serums that aim to neutralize free radicals and prevent heavy metal deposition on the hair shaft. Similarly, Japan's beauty market, which has traditionally emphasized ultraviolet protection in skincare, is now extending this focus to hair care. Brands are introducing sprays and oils containing sun protection factor (SPF)-equivalent filters to prevent photo-oxidation of melanin. In the Middle East, where consumers face intense solar radiation and arid climates, there is a growing preference for products that combine hydration and ultraviolet defense. This has led to the development of hybrid formulations that include ingredients such as argan oil, vitamin E, and ultraviolet absorbers. The regulatory landscape for ultraviolet filters in hair care remains fragmented, as approvals vary by jurisdiction. Furthermore, the International Fragrance Association's 51st amendment, which introduced 48 new restricted materials, is indirectly influencing formulation decisions for protective products.

Professional-grade treatments like bond-repair and keratin boost salon applications and maintenance product demand

Bond-repair technology, developed by Olaplex's patented Bis-Aminopropyl Diglycol Dimaleate, has significantly advanced professional hair treatments by addressing disulfide bonds at the molecular level. This innovation enables stylists to deliver noticeable results that clients can maintain at home. Olaplex has secured over 160 patents worldwide, with approximately 100 patents protecting its core product families set to expire around 2034. Additionally, about 50 patents provide protection against competitors using non-Bis-Amino formulations, with most of these patents expiring in 2035. In February 2025, the company launched its No.0.5 Scalp Longevity Treatment, highlighting the importance of scalp health as the basis for long-term hair vitality. This product introduction reflects a strategic shift from focusing solely on damage repair to emphasizing preventive care. Keratin treatments, which smooth the hair cuticle through heat-activated protein infusion, have evolved from using formaldehyde-based formulations to aldehyde-free alternatives. These updated formulations comply with European Union Regulation 1003/2014 on isothiazolinone preservatives and Regulation 2021/850 on titanium dioxide and salicylic acid.

High usage of hair coloring services increases visits and sales of color-care products

Hair coloring services continue to play a crucial role in salon revenue, with the global hair colorants market growing at a moderate pace. Permanent, semi-permanent, and demi-permanent color formulations require specialized aftercare to maintain vibrancy and prevent oxidative fading. This has driven demand for sulfate-free shampoos, purple toners, and color-depositing conditioners. L'Oréal's acquisition of Color Wow in June 2025 highlights the strategic importance of color-care products, as the brand's Dream Coat and Color Security lines have gained a strong consumer following for delivering salon-quality results between appointments. Salons are increasingly upselling color-care regimens at the point of service by bundling take-home products with in-chair treatments to enhance color longevity and reduce the need for frequent touch-ups. The growing popularity of balayage and lived-in color techniques, which require less frequent root maintenance compared to traditional single-process coloring, has paradoxically boosted product sales. Consumers are investing in toning shampoos and glosses to preserve dimensional hues. In the Asia-Pacific region, where hair coloring has historically been less common, there is rapid adoption among younger demographics influenced by Korean and Japanese pop culture. In India, the cosmetics industry projects hair care and color cosmetics to be the fastest-growing categories through 2025.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High salon service costs reducing visit frequency and premium treatment adoption | -0.7% | North America and Europe; emerging in urban Asia-Pacific | Short term (≤ 2 years) |

| Stringent regulations increasing compliance and reformulation costs for cosmetic ingredients | -0.5% | Global, with Europe and North America most affected | Medium term (2-4 years) |

| Rising costs of specialty ingredients and sustainable materials compressing profit margins | -0.6% | Global, with impact on premium and indie brands | Medium term (2-4 years) |

| Consumer skepticism increasing demand for clinical proof and prolonging decision cycles | -0.4% | Global, with highest intensity in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High salon service costs reducing visit frequency and premium treatment adoption

Premium salon treatments, such as bond-repair sessions, keratin smoothing, and balayage coloring, are priced at a premium per visit. This often makes them inaccessible to middle-income consumers, prompting a shift toward at-home alternatives or lower-tier salons. Olaplex's professional channel sales experienced a decline in the fourth quarter of 2024, reflecting reduced salon traffic and the challenges faced by stylists in justifying premium add-ons in a cost-conscious environment. Independent salons, which held the majority structural share in 2024, are under pressure as rising labor costs and extended intervals between client visits from six weeks to eight or ten weeks compress margins. Chained salons are responding to these challenges by introducing membership models that bundle services at discounted rates. However, these programs reduce per-visit revenue and shift profitability toward retail product sales. The United States Bureau of Labor Statistics (BLS) Producer Price Index for hair preparations reached 154.277 in March 2025, up from a base of 100 in June 2007. This increase highlights sustained input cost inflation, which salons find difficult to pass on to price-sensitive consumers [2]Source: U.S. Bureau of Labor Statistics, “Producer Price Indexes – September 2025,” bls.gov. Economic stagnation in Europe and uneven post-pandemic recovery in the Asia-Pacific region are further widening the affordability gap, particularly in markets where salon services are considered discretionary luxuries rather than routine maintenance. In response, brands are introducing professional-quality retail lines to help consumers extend salon results at home. However, this strategy risks undermining the professional channel that originally established their credibility.

Stringent regulations increasing compliance and reformulation costs for cosmetic ingredients

The United States Food and Drug Administration (FDA) Modernization of Cosmetics Regulation Act, effective July 2024, introduces requirements for facility registration, product listing, adverse event reporting, and safety substantiation. These compliance measures bring significant costs, which are particularly challenging for small and mid-sized brands to manage. In the European Union, the expansion of the fragrance allergen list from 26 to 82 substances has created the need for reformulating thousands of stock-keeping units. Each reformulation process involves conducting stability testing, submitting regulatory documentation, and updating product labels across various jurisdictions. Similarly, the International Fragrance Association's 51st amendment has added 48 new restricted materials, requiring brands to find alternative fragrance compounds that may not deliver the same performance or cost efficiency as the original ingredients. In the European Union, brands must also perform product safety assessments and notify formulations through the Cosmetic Products Notification Portal. This process requires specialized toxicological expertise and extends the time needed to bring new products to market. Smaller independent brands, which often lack dedicated regulatory affairs teams, are increasingly outsourcing compliance tasks to consultants such as Obelis, incurring additional costs ranging from USD 5,000 to USD 20,000 per product line. Moreover, the regulatory differences between the United States, European Union, and Asia-Pacific markets hinder the ability to achieve economies of scale in formulation. As a result, brands are compelled to maintain region-specific product variants, which increases inventory complexity and working capital requirements. Although these regulations are designed to improve consumer safety and strengthen trust in premium brands, they also tend to consolidate market share among multinational corporations that have the resources to handle multi-jurisdictional compliance. This situation places smaller, innovative brands, which depend on speed and flexibility, at a competitive disadvantage.

Segment Analysis

By Revenue Stream: Services Anchor Salons While Products Scale Faster

Hair care services accounted for 72.88% of the market share in 2025, highlighting the continued significance of salons in offering professional treatments such as coloring, keratin smoothing, and bond-repair applications. However, hair care products are expected to grow at a compound annual growth rate (CAGR) of 7.21% through 2031, surpassing the growth of services as consumers increasingly maintain salon results at home using shampoos, conditioners, and serums. The professional channel has shown signs of weakness, with Olaplex's professional sales declining by 27.1% in the fourth quarter of 2024, indicating a structural shift toward retail and direct-to-consumer channels that provide greater convenience and lower per-use costs.

In response, salons are focusing on upselling take-home products during service appointments and bundling professional treatments with retail kits that include color-care shampoos, bond-repair boosters, and styling oils. The emergence of hybrid models, where salons operate as both service providers and product retailers, is blurring the distinction between revenue streams and enabling stylists to capture a larger share of consumer spending.

Note: Segment shares of all individual segments available upon report purchase

By End Use: Female Dominance Persists as Male Segment Awakens

Female consumers accounted for 66.45% of end-use demand in 2025 and are expected to grow at a compound annual growth rate (CAGR) of 6.72% through 2031. This growth is attributed to higher usage frequency, a willingness to pay premiums for scalp-health formulations, and the adoption of multi-step regimens inspired by Korean and Japanese beauty practices. Olaplex reported that scalp health was its fastest-growing segment in the first quarter of 2025, expanding at twice the rate of the overall prestige hair care market. This trend reflects female consumers' focus on preventive wellness rather than reactive damage repair. Additionally, the shift toward ingestible hair supplements, as seen in Unilever's acquisition of Nutrafol in January 2025, highlights a holistic approach to hair health. Female consumers are increasingly linking topical treatments with nutritional solutions to address root causes such as hormonal imbalances and nutrient deficiencies.

Male consumers, while representing a smaller share of the market, are driving incremental growth by adopting grooming routines that extend beyond basic shampoo and conditioner. This segment is showing a growing preference for scalp-health products, anti-hair-loss treatments, and styling aids that provide natural-looking hold without leaving residue. Hims & Hers, a company offering personalized hair-loss treatments through a subscription-based model, has demonstrated the commercial viability of targeting male consumers with clinically validated formulations designed to address androgenetic alopecia.

By Structure: Independents Lead Share but Chains Scale Technology

Independent salons accounted for 61.10% of the structural market share in 2025, driven by personalized services, stylist expertise, and a loyal customer base that values the intimacy of single-location operations. However, chained salons are projected to grow at a compound annual growth rate (CAGR) of 7.02% through 2031, leveraging economies of scale to implement artificial intelligence (AI)-powered scalp analysis tools, subscription models, and centralized training programs that ensure consistent service quality across multiple locations. For example, Kérastase's K-Scan device, trained on over 12,000 images, highlights the technological advantage that chains can distribute across hundreds of locations, whereas independent salons often find it challenging to justify the capital investment for such equipment. Similarly, becon's 2-second scalp analysis system is gaining traction among chained salons in the Asia-Pacific region, where consumers demand data-driven recommendations and are willing to pay premiums for personalized care regimens.

Chains are also extending their reach through digital tools, as demonstrated by Sally Beauty's Licensed Colorist on Demand service, which connects consumers with professional colorists for remote diagnostics, capturing at-home application opportunities. Despite these advancements, independent salons maintain a competitive edge in high-touch services such as balayage coloring and bond-repair treatments, where stylist artistry and strong client relationships foster repeat visits and word-of-mouth referrals. Nevertheless, rising labor costs and challenges in attracting skilled talent are compressing margins for independent salons, prompting many to increase prices or streamline their service offerings. While the International Organization for Standardization (ISO) and national cosmetology boards establish minimum training standards for stylists, enforcement varies by jurisdiction, leading to quality inconsistencies. This variability often benefits chains with comprehensive onboarding and training programs that ensure uniform service quality.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America emerged as the leading segment, capturing 38.20% of the market share in 2025. This dominance is attributed to high per-capita spending on salon services, the widespread adoption of bond-repair and keratin treatments, and mature distribution networks that span professional, specialty retail, and direct-to-consumer channels. The implementation of the United States Food and Drug Administration (FDA) Modernization of Cosmetics Regulation Act in July 2024 is reshaping the competitive landscape. This regulation introduces requirements such as facility registration, adverse event reporting, and safety substantiation, which favor established brands with robust regulatory affairs capabilities. Additionally, L'Oréal's acquisition of Color Wow in June 2025 strengthens its color-care portfolio in the region, while Unilever's purchase of Nutrafol in January 2025 positions the company to address the needs of 114 million United States consumers experiencing hair health issues.

The Asia-Pacific region will emerge as the fastest-growing segment, boasting a compound annual growth rate of 6.95% through 2031. This surge is largely attributed to urbanization, increasing disposable incomes, and a growing inclination towards Korean and Japanese-inspired multi-step hair care routines. In India, the beauty and personal care market is on an upward trajectory, outpacing global averages and carving out a significant slice of the worldwide cosmetics pie. Within this landscape, hair care and color cosmetics are leading the charge . The Indian market stands out for its innovative fusion of traditional Ayurvedic elements, like neem and turmeric, with contemporary actives such as peptides and hyaluronic acid. This distinctive blend presents a golden opportunity for brands adept at marrying heritage with modern science. Concurrently, both China and Japan are rapidly embracing scalp-health products and anti-pollution solutions, a shift largely spurred by concerns over urban air quality and a growing consumer consciousness regarding environmental challenges.

Other regions, such as Europe, are navigating a complex regulatory environment. The European Union has expanded its fragrance allergen list from 26 to 82 substances and is enforcing Regulation 1003/2014 on isothiazolinone preservatives and Regulation 2021/850 on titanium dioxide and salicylic acid. These mandates are driving reformulation cycles that benefit multinational brands with dedicated research and development teams, while smaller indie brands face challenges in absorbing compliance costs. L'Oréal's EUR 4 billion (USD 4.6 billion) acquisition of Kering's beauty division in October 2025, which includes 50-year exclusive licenses for Gucci, Bottega Veneta, and Balenciaga, underscores aggressive consolidation efforts aimed at capturing the luxury and prestige segments.

Competitive Landscape

The global hair care market shows moderate concentration, with multinational corporations such as L'Oréal, Unilever, Procter & Gamble, Henkel, and Kao actively acquiring indie brands to expand their portfolios. These acquisitions target brands with loyal customer bases and unique technologies. For example, L'Oréal's EUR 4 billion (USD 4.6 billion) acquisition of Kering's beauty division in October 2025 secured 50-year exclusive licenses for luxury brands like Gucci, Bottega Veneta, and Balenciaga, emphasizing the focus on the luxury and prestige segments. Similarly, Unilever acquired Nutrafol in January 2025 to enter the ingestible hair supplement category and purchased Wild in April 2025 to strengthen its clean-beauty positioning. Procter & Gamble expanded its prestige portfolio by acquiring Ouai, a celebrity-founded hair and lifestyle brand, to appeal to millennial and Generation Z consumers.

Technology adoption is emerging as a significant competitive advantage in the market. Innovations such as Kérastase's K-Scan device, Becon's 2-second scalp analysis system, and Perfect Corporation's artificial intelligence-based hair type analysis enable brands to provide personalized recommendations at scale. Indie brands like Briogeo, Virtue Labs, and Moroccanoil are carving out niches through clean formulations, proprietary ingredients, and direct-to-consumer models that bypass traditional retail markups. However, their growth is constrained by smaller distribution networks and limited marketing budgets compared to multinational competitors.

The regulatory landscape is also reshaping the market. The United States Food and Drug Administration (FDA) Modernization of Cosmetics Regulation Act and the European Union's expanded allergen list are consolidating market share among brands with the resources to manage multi-jurisdictional compliance. This environment poses challenges for smaller disruptors, which often rely on speed and agility but lack the capacity to navigate complex regulatory requirements.

Hair Care Industry Leaders

L'Oréal S.A.

Unilever PLC

The Procter & Gamble Company

Henkel AG & Co. KGaA

Kao Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: L’Oréal acquired Color Wow, a rapidly expanding professional haircare brand from the United States and United Kingdom, which had garnered acclaim for its award-winning products that controlled frizz, thickened, and added volume. With this acquisition, L’Oréal bolstered its Professional Products Division and set its sights on propelling Color Wow's global presence, targeting salons, selective retail outlets, and e-commerce platforms.

- March 2025: It’s a 10 Haircare launched the Clear Collection, a vegan and eco-friendly professional haircare line, in recyclable clear packaging. The collection's Gel, Leave-In, and Shine Elixir featured plant-based ingredients such as ashwagandha, amla, and reishi. These products met Sephora and Ulta's clean standards, held Leaping Bunny certification, and were free from SLS, SLES, parabens, and phthalates.

- February 2025: OLAPLEX unveiled a refreshed brand identity focused on “foundational hair health,” highlighting its science‑driven Complete Bond Technology and stronger engagement with stylists, and launched No.0.5 Scalp Longevity Treatment, a scalp serum used with No.3 Hair Perfector to promote long‑term scalp and hair health.

Global Hair Care Market Report Scope

Hair care products are grooming and nourishing products used for styling, cleaning, and maintaining a person's hair. The scope of the report covers an analysis of the type of hair care products, including shampoo, conditioner, hair loss treatment products, hair colorants, hair styling products, and perms and relaxants. The global hair care market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into shampoos, conditioners, hair loss treatment products, hair colorants, hair styling products, perms and relaxants, and other product types. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, specialty stores, online stores, pharmacies/drug stores, and other distribution channels. The study also covers the global level analysis of major regions such as North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Hair Care Products |

| Hair Care Services |

| Male |

| Female |

| Chained Salons |

| Independent Salons |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Chile | |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Turkey | |

| Rest of Middle East and Africa |

| By Revenue Stream | Hair Care Products | |

| Hair Care Services | ||

| By End Use | Male | |

| Female | ||

| By Structure | Chained Salons | |

| Independent Salons | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global hair care market in 2026?

The hair care market size is USD 82.5 billion in 2026.

What is the expected growth rate for hair care through 2031?

The sector is forecast to expand at a 5.69% CAGR, reaching USD 108.59 billion by 2031.

Which region will grow the fastest in hair treatment demand?

Asia-Pacific is projected to post the quickest 6.95% CAGR through 2031, driven by urbanization and K-beauty routines.

What segment of the category is outpacing overall growth?

Retail hair care products, especially bond-repair and color-care lines, are climbing at 7.21% CAGR, faster than salon services.

How are new regulations affecting product development?

MoCRA in the U.S. and expanded European Union allergen lists force costly safety substantiation and reformulation, favoring well-capitalized firms.