| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Market Volume (2025) | 93.90 tons |

| Market Volume (2030) | 122.09 tons |

| CAGR | 5.39 % |

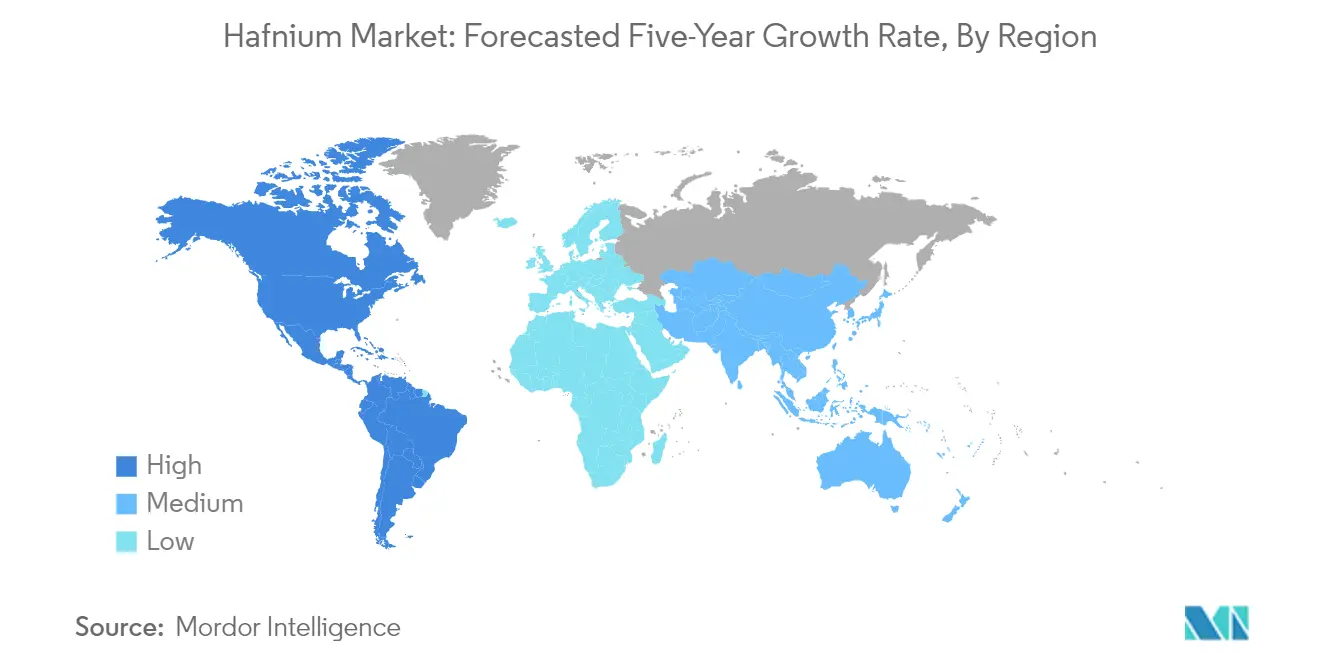

| Largest Market | Americas |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Hafnium Market Analysis

The Hafnium Market size is estimated at 93.90 tons in 2025, and is expected to reach 122.09 tons by 2030, at a CAGR of 5.39% during the forecast period (2025-2030).

The global hafnium industry is experiencing significant transformation driven by evolving energy policies and technological advancements across major economies. Nuclear power development has become a key focus area, particularly in China, where nuclear power currently accounts for only 2.2% of installed electricity generation capacity, presenting substantial growth potential. Several countries are expanding their nuclear infrastructure, with governments worldwide announcing plans for new reactor construction to achieve carbon neutrality goals. This shift towards nuclear energy is reshaping the demand dynamics of the hafnium market, as the material is crucial for nuclear reactor components.

The semiconductor industry is undergoing unprecedented expansion, marked by significant investments in manufacturing capabilities. In a notable development, Intel announced a USD 20 billion investment in January 2023 to construct two new leading-edge chip factories in Ohio, United States. This investment trend is being replicated across major economies as governments implement policies to strengthen domestic semiconductor materials production capabilities. The industry's evolution is particularly significant for hafnium demand, as the material is essential in advanced semiconductor materials manufacturing processes.

Supply chain dynamics in the hafnium market are experiencing substantial restructuring, influenced by geopolitical factors and industrial policies. The global supply of hafnium remains concentrated among a handful of producers, with production primarily centered in France, the United States, China, and Russia. This concentration has led to significant price volatility, with hafnium prices experiencing sharp fluctuations as manufacturers compete for limited supplies. The situation is further complicated by the dual-use nature of the material, requiring export licenses in certain jurisdictions.

The aerospace sector continues to be a fundamental driver of hafnium demand, with major manufacturers ramping up production to address growing order backlogs. Airbus, for instance, delivered 661 commercial aircraft in 2022, marking an 8% increase compared to the previous year. Looking ahead, the Boeing Commercial Outlook 2022-2041 projects total global deliveries of 41,170 new airplanes by 2041, indicating sustained long-term demand for hafnium-based components. This growth trajectory is supported by increasing requirements for high-performance materials in next-generation aircraft designs, particularly in engine components where hafnium's unique properties are essential.

Hafnium Market Trends

Growing Demand for Hafnium Superalloys from Aerospace Industry

Hafnium superalloys have become increasingly critical in aerospace applications due to their exceptional thermal stability and strength properties, particularly in jet and rocket engines where operating temperatures are extremely high. These superalloy materials, which typically contain 1-2% hafnium, are primarily used in manufacturing turbine blades and vanes, making them irreplaceable components in the hot sections of jet engines. The material's ability to strengthen grain boundaries of nickel-based superalloys while improving creep ductility and rupture lifetime has made it an essential element in aerospace manufacturing. In rocket engine applications, hafnium constitutes approximately 10% of the niobium-based alloy used in thruster nozzles, demonstrating its crucial role in space technology.

The aerospace industry's growing focus on fuel efficiency and enhanced engine performance has further accelerated the demand for hafnium-based superalloys. Major aircraft manufacturers are ramping up production to meet increasing air travel demands, with significant developments in wide-body aircraft for long-haul routes throughout 2023. This trend is exemplified by recent developments such as GE Vernova's Gas Power business and Harbin Electric's announcement in October 2023 regarding the installation of new gas turbines in China's Zhoushan archipelago, which will require hafnium-based components for high-temperature operations. The material's unique properties in allowing aircraft engines to operate at higher temperatures while maintaining safety and reducing fuel consumption have made it an indispensable element in modern aerospace manufacturing.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Utilization of Hafnium-based Materials in Semiconductors

The semiconductor industry has witnessed a significant surge in the adoption of hafnium oxide and other hafnium compounds, particularly due to their superior dielectric properties and compatibility with advanced manufacturing processes. Hafnium oxide's high dielectric constant, which is 4-6 times higher than traditional silicon oxide, makes it an ideal material for use in advanced metal-oxide semiconductor devices and DRAM capacitors. The material's ability to provide nonvolatile memory that can be integrated directly into circuits, coupled with its crucial role in maintaining the ferroelectric qualities of integrated circuit materials, has positioned it as a fundamental component in semiconductor fabrication processes at 45 nanometers and smaller feature lengths.

The global push towards semiconductor manufacturing self-sufficiency has created new opportunities for semiconductor materials in this sector. Countries are making substantial investments in domestic semiconductor production capabilities, with major manufacturers focusing on developing new fabrication facilities. This trend is particularly evident in China's strategic initiatives, where the government has announced ambitious plans to achieve 80% self-sufficiency in semiconductor production by 2030, with a targeted output of USD 305 billion. The establishment of new semiconductor manufacturing facilities across multiple cities, including Chongqing, Shanghai, Beijing, Chengdu, Hefei, Shenzhen, and Wuhan, demonstrates the growing importance of hafnium-based materials in semiconductor production. These developments are further supported by government subsidies and policy incentives aimed at building a robust domestic semiconductor materials industry.

Segment Analysis: Type

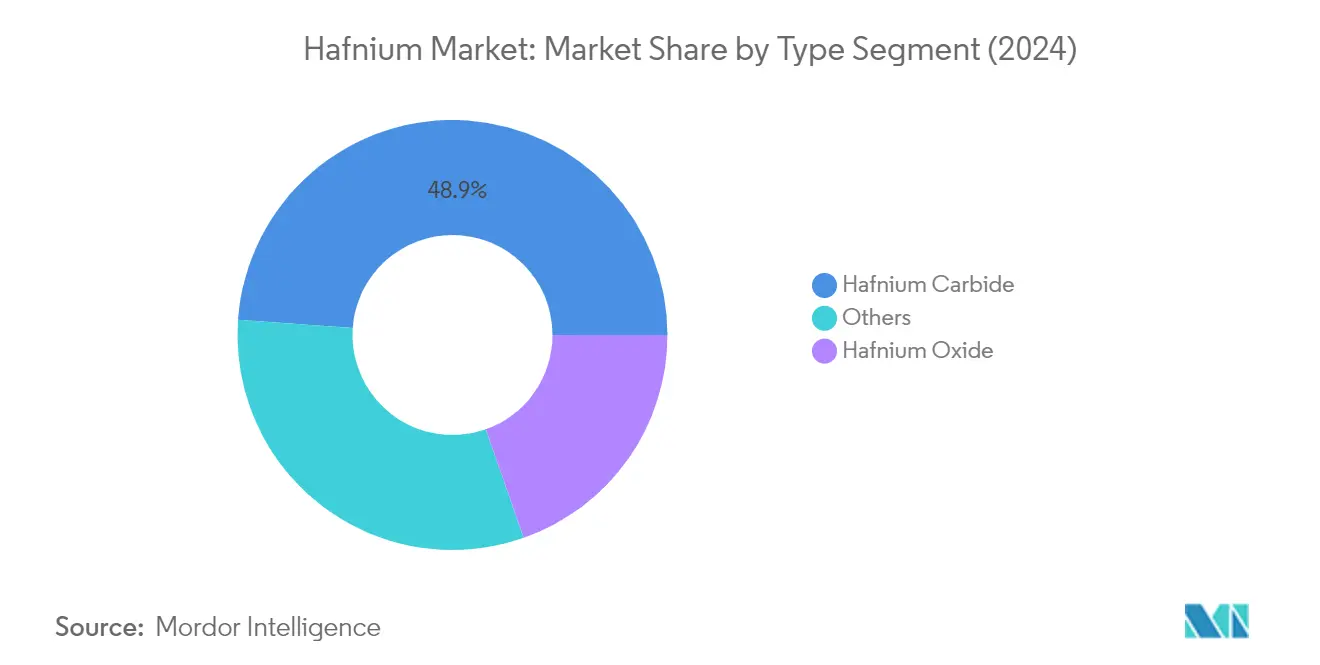

Hafnium Carbide Segment in Hafnium Market

Hafnium carbide dominates the global hafnium market, holding approximately 49% of the market share in 2024. This significant market position is attributed to its extensive applications in nuclear rocket propulsion, nuclear reactors, the space aircraft industry, and thermal-field emitters. The material's exceptional properties, including a high elasticity coefficient, good electrical and thermal conductivity, a small thermal expansion coefficient, and superior impact resistance, make it indispensable in these high-performance applications. Additionally, hafnium carbide's ability to form solid solutions with many compounds such as ZrC, TaC, and NbC further enhances its versatility in various industrial applications. The segment's dominance is further strengthened by the growing demand from the aerospace sector, particularly in applications requiring ultrahigh-temperature ceramics (UHTCs).

Hafnium Oxide Segment in Hafnium Market

The hafnium oxide segment is projected to experience the fastest growth in the hafnium market, with an anticipated growth rate of approximately 6% during the forecast period 2024-2029. This accelerated growth is driven by its increasing adoption in optical coatings and as a high-κ dielectric in DRAM capacitors and advanced metal-oxide-semiconductor devices. The material's exceptional properties, including its high dielectric constant and band gap of 5.3~5.7 eV, make it particularly valuable in semiconductor applications. Recent developments in multilayered films combining hafnium oxide with other materials for passive cooling of buildings have opened new application avenues. Furthermore, ongoing research into hafnium oxide's potential in bio-related applications, resistive-switching memories, and advanced circuit applications in ferroelectric devices is expected to fuel its growth trajectory.

Remaining Segments in Hafnium Type Segmentation

The other segments in the hafnium market, including pure hafnium metal, hafnium nitride, hafnium chloride, and various other forms, collectively play a vital role in diverse industrial applications. Pure hafnium metal finds extensive use as a control rod in nuclear reactors and in manufacturing various alloys. Hafnium nitride serves as a valuable refractory material, particularly in thermal spraying processes and protective coating applications. Hafnium chloride and hafnium tetrachloride are crucial intermediates in the production of hafnium metal and serve as catalysts in research laboratories. The continuous research and development activities exploring new hafnium compounds, such as hafnium polyhydrides with superconductivity properties, are expected to further diversify these segments' applications and market potential.

Segment Analysis: Application

Super Alloy Segment in Hafnium Market

The Super Alloy segment dominates the global hafnium market, accounting for approximately 55% market share in 2024. This significant market position is primarily driven by hafnium's crucial role in aerospace and industrial applications, particularly in jet engines and industrial gas turbines. Due to its superior properties, such as high strength and stability at high temperatures, hafnium serves as an essential composite material in superalloys. The metal is predominantly used in turbine blades and vanes, which operate under extreme temperature and pressure conditions. Major industrial players like Siemens utilize polycrystalline nickel-based alloys containing around 1.5% hafnium for their land-based turbines, operating at temperatures around 10,500°C. The segment's dominance is further reinforced by hafnium's irreplaceable role in manufacturing hot parts of jet engines, where it helps increase fuel efficiency and enhance engine safety at higher operating temperatures.

Nuclear Segment in Hafnium Market

The Nuclear segment is projected to experience the highest growth rate in the hafnium market, with an expected CAGR of approximately 6% during the forecast period 2024-2029. This accelerated growth is primarily attributed to the increasing global focus on nuclear power generation and the essential role of hafnium in nuclear reactor control rods. The segment's growth is being driven by significant nuclear power expansion plans across various countries, particularly in emerging economies. The metal's high microscopic cross-section of neutron absorption makes it an excellent material for control rods in nuclear reactors worldwide. These control rods serve multiple critical functions, including neutron flux shaping to form even flux profiles, temperature control, and safety mechanisms in reactor plant operations. The segment's growth is further supported by ongoing nuclear power plant construction projects and the increasing adoption of nuclear energy as a reliable baseload power source in many countries' energy mix.

Remaining Segments in Application Segmentation

The remaining segments in the hafnium market include Optical Coating, Plasma Cutting, and Other Applications, each serving distinct industrial purposes. The Optical Coating segment utilizes hafnium compounds, particularly hafnium oxide, for their high-index and low-absorption properties in coating applications ranging from near-UV to IR regions. The Plasma Cutting segment leverages hafnium's unique ability to shed electrons into the air, making it ideal for plasma torch welding tips and cathodes in plasma arc cutting applications. The Other Applications segment encompasses various specialized uses, including semiconductor manufacturing, where hafnium-based materials are employed in advanced circuit applications and ferroelectric devices, particularly in response to developments in cloud computing, artificial intelligence, and edge computing technologies.

Hafnium Market Geography Segment Analysis

Hafnium Market in the United States

The United States dominates the global hafnium market, commanding approximately 37% of the total market share. The country's strong position is primarily driven by its robust aerospace and defense sectors, where hafnium metal is extensively used in superalloys for aircraft engines and industrial turbines. The semiconductor industry in the United States, accounting for about 46% of the global semiconductor market, further strengthens the demand for hafnium, particularly in the form of hafnium oxide used in advanced semiconductor materials manufacturing. The presence of major semiconductor manufacturers like Intel, Samsung, and NVIDIA, coupled with significant investments in domestic chip manufacturing through initiatives like the CHIPS Act, continues to drive market growth. The country's substantial nuclear power sector, being the world's largest nuclear power producer, maintains a steady demand for hafnium in control rods. Additionally, the growing focus on plasma cutting applications in various manufacturing sectors contributes to the market's expansion.

Hafnium Market in Russia

Russia's hafnium market is projected to experience robust growth with an expected CAGR of approximately 7% during 2024-2029. The country's market dynamics are significantly influenced by its expanding nuclear energy sector, with 37 operational nuclear reactors and ambitious plans for future expansion. The government's commitment to increasing nuclear power's role in electricity generation has created sustained demand for hafnium-based control rods. Russia's strategic initiatives to develop its domestic semiconductor materials industry, supported by substantial government investments including a recent RUB 2.2 billion funding through the Ministry of Industry and Trade, are creating new growth opportunities. The aerospace sector, though facing some challenges, continues to maintain demand for hafnium superalloys, particularly with the government's support for domestic aircraft production programs. The country's focus on developing high-technology industries and reducing dependency on imports has led to increased investments in local manufacturing capabilities, further driving market growth.

Hafnium Market in the European Union

The European Union represents a significant market for hafnium, driven by its diverse industrial base and technological advancement initiatives. The region's aerospace sector, particularly in countries like France and Germany, maintains strong demand for hafnium-based superalloys in aircraft manufacturing. The EU's commitment to semiconductor manufacturing independence, exemplified by the European Chips Act and substantial investments in new fabrication facilities, is creating additional demand channels. France's position as the sole EU producer of hafnium adds strategic importance to the market. The region's industrial base, particularly in Germany's manufacturing sector, continues to drive demand for hafnium in various applications including plasma cutting and optical coatings. Despite the closure of some nuclear facilities in certain member states, the ongoing operations and maintenance of existing nuclear power plants, especially in France, ensure steady demand for hafnium in nuclear applications.

Hafnium Market in China

China's hafnium market demonstrates strong potential, supported by the country's ambitious industrial development plans and technological advancement initiatives. The nation's commitment to expanding its nuclear power sector, with plans to increase nuclear power's contribution to 10% of power generation by 2035, drives significant demand for hafnium-based products. The government's strategic focus on developing domestic semiconductor materials manufacturing capabilities, supported by initiatives like Made in China 2025, has created new growth opportunities in the market. The country's aerospace sector, particularly with the projected growth in air traffic and aircraft demand, continues to drive the need for hafnium-based superalloys. China's investments in wind energy and power generation infrastructure further contribute to market expansion. The nation's efforts to develop its domestic manufacturing capabilities across various high-technology sectors have positioned it as a key player in the global hafnium market.

Hafnium Market in Other Countries

The hafnium market in other countries, including Japan, India, and various nations across the Asia-Pacific and Americas regions, exhibits diverse growth patterns influenced by their respective industrial development stages and technological advancement initiatives. Japan's market is characterized by its strong focus on semiconductor manufacturing and growing investments in nuclear power. India's market is driven by its expanding nuclear power program and emerging semiconductor industry. South Korea's market benefits from its strong presence in the semiconductor industry and aerospace sector development. Countries in the Americas, particularly Canada and Brazil, show potential growth driven by their aerospace and nuclear power sectors. These markets collectively contribute to the global hafnium industry's dynamics, each bringing unique demand patterns based on their industrial focus and technological advancement levels.

Get Analysis on Important Geographic Markets

Download PDF

Hafnium Industry Overview

Top Companies in Hafnium Market

The hafnium market is characterized by companies focusing on continuous product innovation, particularly in developing high-purity grades for aerospace and semiconductor materials applications. Major players are investing in research and development to enhance production efficiency and develop novel applications, especially in nuclear and electronic sectors. Strategic partnerships with end-users, particularly in aerospace and defense industries, have become crucial for maintaining market position. Companies are expanding their production capabilities through facility upgrades and new plant establishments, particularly in regions with growing demand like Asia-Pacific. Operational agility is demonstrated through integrated supply chain management and the ability to adapt production according to varying industry demands, while sustainability initiatives and circular economy practices are gaining prominence in manufacturing processes.

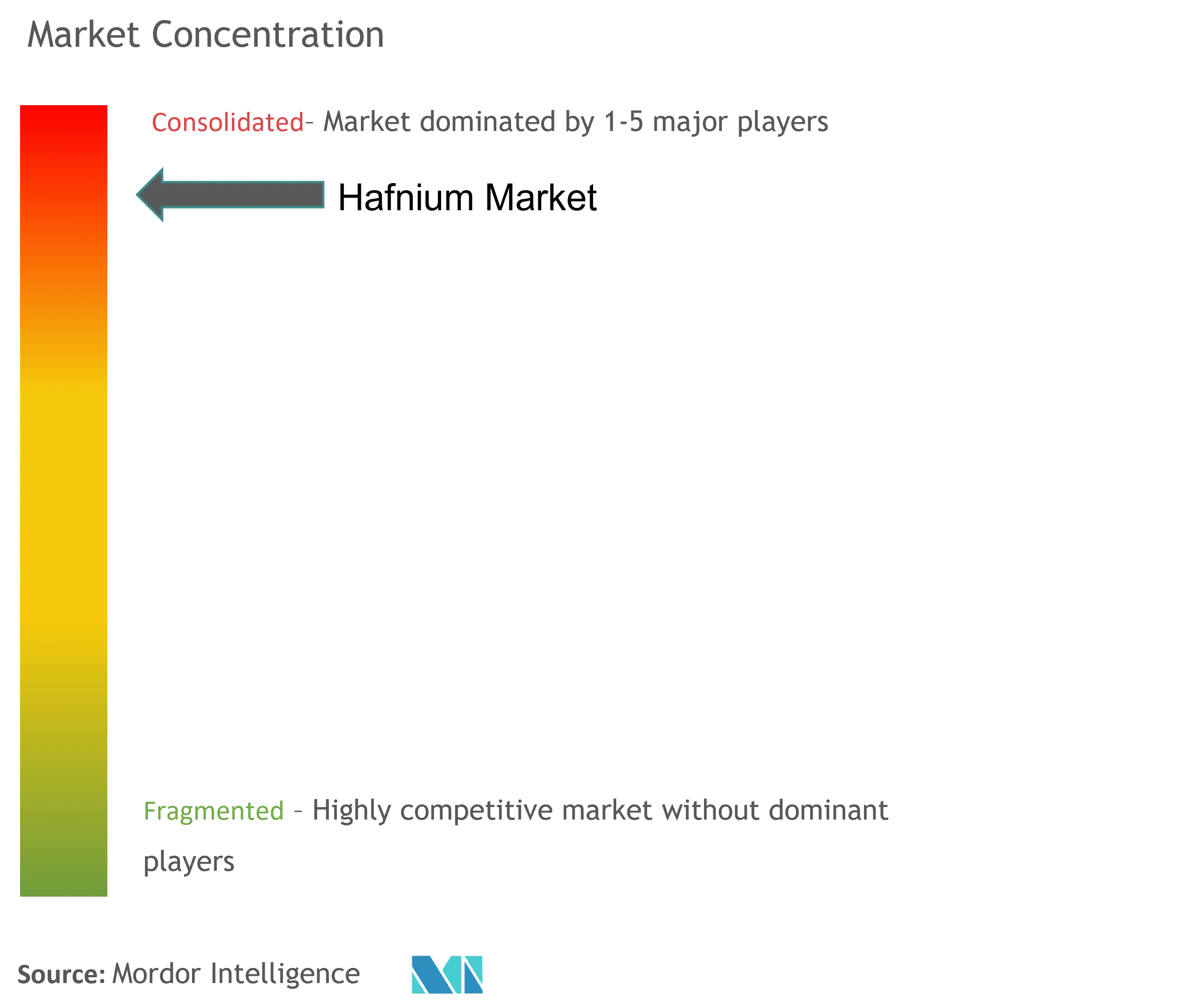

Consolidated Market with Limited Major Players

The global hafnium market exhibits a highly consolidated structure dominated by a small number of large-scale manufacturers, primarily led by ATI and Framatome, who together control a significant portion of the global production capacity. These established players have built their market positions through decades of expertise in metal processing, strong technological capabilities, and extensive distribution networks. The market is characterized by high entry barriers due to complex production processes, significant capital requirements, and the need for specialized technical knowledge in hafnium metal processing and purification.

The industry shows limited merger and acquisition activity due to the already consolidated nature of the market and the specialized nature of operations. Regional players, particularly in China and other Asian countries, are gradually emerging but face challenges in matching the quality standards and production capabilities of established global leaders. The market structure is further reinforced by long-term supply agreements with key customers in aerospace and nuclear industries, making it difficult for new entrants to gain significant market share.

Innovation and Supply Chain Control Drive Success

Success in the hafnium market increasingly depends on technological innovation capabilities, particularly in developing higher purity grades and new applications. Companies need to focus on vertical integration to ensure reliable access to raw materials, given that hafnium production is closely tied to zirconium processing. Establishing strong relationships with end-users in critical industries like aerospace and semiconductors is crucial, as is the ability to meet stringent quality requirements and industry certifications. Players must also invest in sustainable production methods and circular economy initiatives to align with growing environmental concerns.

For contenders looking to gain market share, specialization in specific applications or regional markets offers the most viable path forward. Success factors include developing proprietary processing technologies, establishing strategic partnerships with raw material suppliers, and building strong customer relationships in niche segments. The market's future will be shaped by the ability to navigate regulatory requirements, particularly in nuclear and aerospace applications, while managing the risk of substitution from alternative materials. Companies must also consider the concentrated nature of end-user industries and develop strategies to diversify their customer base while maintaining strong positions in core markets. The hafnium industry is poised for growth as it aligns with these strategic imperatives, leveraging its position within the rare metals sector.

Hafnium Market Leaders

-

Framatome (EDF)

-

American Elements

-

Nanjing Youtian Metal Technology Co. Ltd

-

ACI Alloys

-

ATI

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Hafnium Market News

- November 2023: Framatome declared its intention to invest in the expansion of its Jarrie site in France. This investment aims to enhance the production capacity of high-quality hafnium, catering to the needs of the nuclear, aerospace, defense, and space industries.

- August 2022: The Institute of Physics of the Chinese Academy of Sciences (IOPCAS) made a significant discovery by identifying new hafnium polyhydrides. This breakthrough resulted from the application of synergistic high-pressure techniques utilizing diamond anvil cells coupled with in situ laser heating. The research focused on exploring novel types of hydrogen-rich superconducting materials.

Hafnium Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Rising Demand from the Aerospace Industry

- 4.1.2 Increasing Utilization of Hafnium-Based Materials in Semiconductors

-

4.2 Restraints

- 4.2.1 Higher Prices and Difficulties in Seperation and Extraction

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Analysis

5. MARKET SEGMENTATION (Market Size in Volume)

-

5.1 Type

- 5.1.1 Hafnium Oxide

- 5.1.2 Hafnium Carbide

- 5.1.3 Other Types (including Hafnium Metal)

-

5.2 Application

- 5.2.1 Super Alloy

- 5.2.2 Optical Coating

- 5.2.3 Nuclear

- 5.2.4 Plasma Cutting

- 5.2.5 Other Applications

-

5.3 Geography

- 5.3.1 Production Analysis

- 5.3.1.1 France

- 5.3.1.2 United States

- 5.3.1.3 China

- 5.3.1.4 Rest of the World

- 5.3.2 Consumption Analysis

- 5.3.2.1 United States

- 5.3.2.2 European Union

- 5.3.2.3 Russia

- 5.3.2.4 China

- 5.3.2.5 India

- 5.3.2.6 Japan

- 5.3.2.7 Rest of the World

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis**

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 ACI Alloys

- 6.4.2 Alkane Resources Ltd

- 6.4.3 American Elements

- 6.4.4 Baoji ChuangXin Metal Materials Co. Ltd (CXMET)

- 6.4.5 China Nulear JingHuan Zirconium Industry Co. Ltd.

- 6.4.6 Framatome (EDF)

- 6.4.7 Nanjing Youtian Metal Technology Co. Ltd

- 6.4.8 Phelly Materials Inc.

- 6.4.9 Starfire Systems Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Inclination on Reusable Spacecrafts

- 7.2 Growing Research on Hafnium Oxide Nanoparticles for Radiotherapy

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Hafnium Industry Segmentation

Hafnium is a lustrous grey metal that has a similar appearance to stainless steel and is chemically comparable to zirconium metal. The metal maintains its stability and strength at high temperatures in both metallic and compound forms and is used for various high-strength and high-temperature applications.

The hafnium market is segmented by type, application, and geography. By type, the market is segmented into hafnium oxide, hafnium carbide, and other types (including hafnium metal). By application, the market is segmented into super alloy, optical coating, nuclear, plasma cutting, and other applications. The report also covers the market size and forecasts for hafnium in 6 countries across the major regions.

For each segment, market sizing and forecasts have been done based on volume (tons).

| Type | Hafnium Oxide | ||

| Hafnium Carbide | |||

| Other Types (including Hafnium Metal) | |||

| Application | Super Alloy | ||

| Optical Coating | |||

| Nuclear | |||

| Plasma Cutting | |||

| Other Applications | |||

| Geography | Production Analysis | France | |

| United States | |||

| China | |||

| Rest of the World | |||

| Consumption Analysis | United States | ||

| European Union | |||

| Russia | |||

| China | |||

| India | |||

| Japan | |||

| Rest of the World | |||

Need A Different Region or Segment?

Customize Now

Hafnium Market Research FAQs

How big is the Hafnium Market?

The Hafnium Market size is expected to reach 93.90 tons in 2025 and grow at a CAGR of 5.39% to reach 122.09 tons by 2030.

What is the current Hafnium Market size?

In 2025, the Hafnium Market size is expected to reach 93.90 tons.

Who are the key players in Hafnium Market?

Framatome (EDF), American Elements, Nanjing Youtian Metal Technology Co. Ltd, ACI Alloys and ATI are the major companies operating in the Hafnium Market.

Which region has the biggest share in Hafnium Market?

In 2025, the Americas accounts for the largest market share in Hafnium Market.

What years does this Hafnium Market cover, and what was the market size in 2024?

In 2024, the Hafnium Market size was estimated at 88.84 tons. The report covers the Hafnium Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Hafnium Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Hafnium Market Research

Mordor Intelligence provides a comprehensive analysis of the hafnium market and HF industry. We leverage our extensive experience in rare metals research to deliver valuable insights. Our detailed report examines the complete value chain of hafnium metal applications. This includes crucial compounds such as hafnium oxide, hafnium dioxide, hafnium carbide, hafnium chloride, and hafnium nitride. The analysis covers the growing demand for semiconductor materials and refractory metals. We pay particular attention to emerging applications in plasma spray materials and superalloy materials.

Stakeholders across the industry can access our report PDF for download. It features in-depth insights into hafnium crystal bar production, hafnium alloy developments, and specialized applications like hafnium sputtering target manufacturing. The report examines various hafnium compounds, including hafnium silicide. It also analyzes trends in the semiconductor materials industry and rare metals market. Our research provides valuable intelligence for businesses operating in the refractory metals market. This is supported by extensive HF industry data and market dynamics analysis. The comprehensive review of the HF market includes a detailed examination of supply chains, technological advancements, and future growth opportunities in this critical sector.