| Study Period | 2019 - 2030 |

| Market Volume (2025) | 16.89 Billion square meters |

| Market Volume (2030) | 22.76 Billion square meters |

| CAGR | 6.15 % |

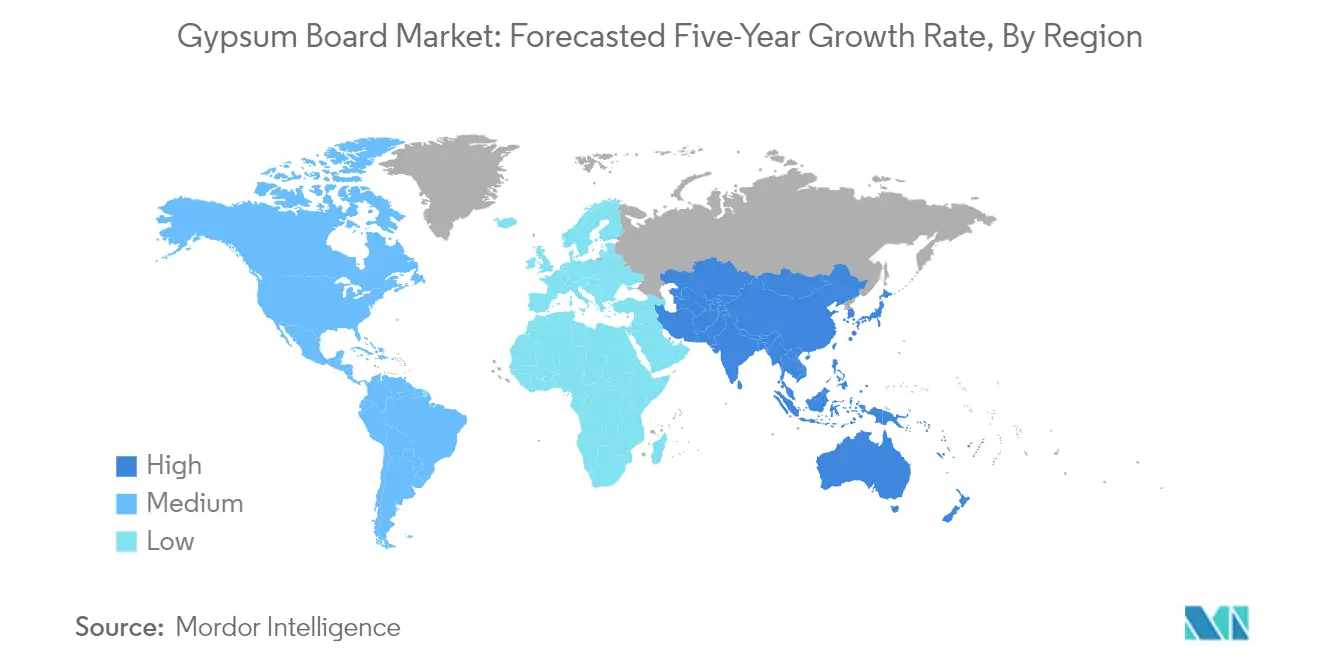

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Gypsum Board Market Analysis

The Gypsum Board Market size is estimated at 16.89 billion square meters in 2025, and is expected to reach 22.76 billion square meters by 2030, at a CAGR of 6.15% during the forecast period (2025-2030).

The global construction industry is experiencing significant transformation driven by urbanization and infrastructure modernization initiatives worldwide. Construction spending in the United States demonstrated robust growth, reaching USD 1,677.2 billion in January 2022, reflecting a 1.3% increase compared to the previous month. This trend is mirrored across major economies as governments prioritize infrastructure development and urban renewal projects. The construction sector's evolution has been particularly notable in emerging economies, where rapid urbanization and industrial development are creating unprecedented demand for building materials and solutions.

Technological advancements and sustainability considerations are reshaping the gypsum board market landscape. Manufacturers are increasingly focusing on developing eco-friendly products with enhanced performance characteristics, including improved fire resistance, acoustic properties, and moisture resistance. The integration of smart manufacturing processes and automation has led to more efficient production methods, resulting in higher quality products with consistent performance characteristics. These innovations are particularly crucial as the industry adapts to stricter building codes and environmental regulations, highlighting the gypsum board market trends.

Major infrastructure development initiatives are driving market dynamics across regions. Saudi Arabia's Vision 2030 encompasses a massive USD 1.1 trillion project pipeline, including megaprojects such as the Neom super-city and the Red Sea Project, which are creating substantial demand for construction materials. Similar large-scale development programs are being implemented across various regions, with governments investing heavily in transportation infrastructure, healthcare facilities, and educational institutions to support growing urban populations.

The commercial and institutional construction sectors are witnessing remarkable growth, supported by increasing investments in office spaces, retail developments, and educational facilities. China's manufacturing sector, accounting for 28.8% of the country's GDP in the first half of 2022, has driven significant industrial construction activities. The trend toward sustainable building practices has led to increased adoption of green building materials, with many projects seeking environmental certifications. This shift is particularly evident in commercial construction, where energy efficiency and environmental impact are becoming critical considerations in material selection and building design, further influencing the building materials industry.

Gypsum Board Market Trends

INCREASING DEMAND FROM RESIDENTIAL CONSTRUCTION

The residential construction sector has emerged as a primary growth driver for the gypsum board market, driven by rapid urbanization and increasing housing demands across major economies. Gypsum boards have become essential components in modern residential construction, being widely used as plasterboards, drywall boards, and decorative plasters for partitions, wall linings, ceilings, roofs, and floors. These materials offer significant advantages, including soundproofing capabilities and resistance to shocks and humidity, making them ideal for residential applications. According to Oxford Economics, China's residential building construction output demonstrated strong growth potential with a 4.5% increase in 2022 compared to the previous year, while Indian companies planned investments exceeding INR 3.5 trillion in infrastructure and real estate development, including substantial residential infrastructure projects.

The surge in residential construction is further supported by government initiatives and urbanization trends across various regions. In Japan, construction companies initiated projects for 258 high-rise buildings comprising 103,100 apartments in the Tokyo region, demonstrating the robust demand for residential infrastructure. The trend is particularly notable in emerging economies where major cities are expanding rapidly to accommodate increasing urban migration. This expansion has led to the implementation of various government housing schemes and initiatives, such as India's Housing for All program and Smart City schemes, which aim to address the significant housing undersupply. The residential construction sector is also witnessing a shift towards more sustainable and efficient building practices, with countries like China focusing on increasing the construction of prefabricated buildings to reduce pollution and construction waste.

Understand The Key Trends Shaping This Market

Download PDF

RISING REPAIR ACTIVITIES

The growing focus on renovation and repair activities has become a significant driver for the gypsum board market, particularly in established markets where building maintenance and upgrades are prioritized. Gypsum boards are extensively used in renovation projects due to their ease of installation, requiring only basic tools such as nails, screws, and staples, while offering excellent fire resistance, sound insulation properties, and economic benefits. The lightweight nature of gypsum boards makes them particularly suitable for renovation work, as they can be easily transported and installed in existing structures without requiring significant structural modifications.

The repair and renovation sector has received substantial support through government initiatives and increasing consumer investment in home improvements. In Japan, the value of orders for dwelling renovations received by construction companies reached JPY 3.75 trillion, marking a significant commitment to building maintenance and improvement. This trend is further supported by various government programs, such as tax-break systems for home renovation, which aim to promote the sales of used homes and address the issue of vacant properties across the country. The renovation market has been expanding steadily, driven by a growing focus on enhanced living environments and increasing investments in housing improvements, including both structural and aesthetic upgrades. These activities have created a consistent demand for gypsum boards, as they are essential materials for interior modifications, ceiling repairs, and wall panel renovations.

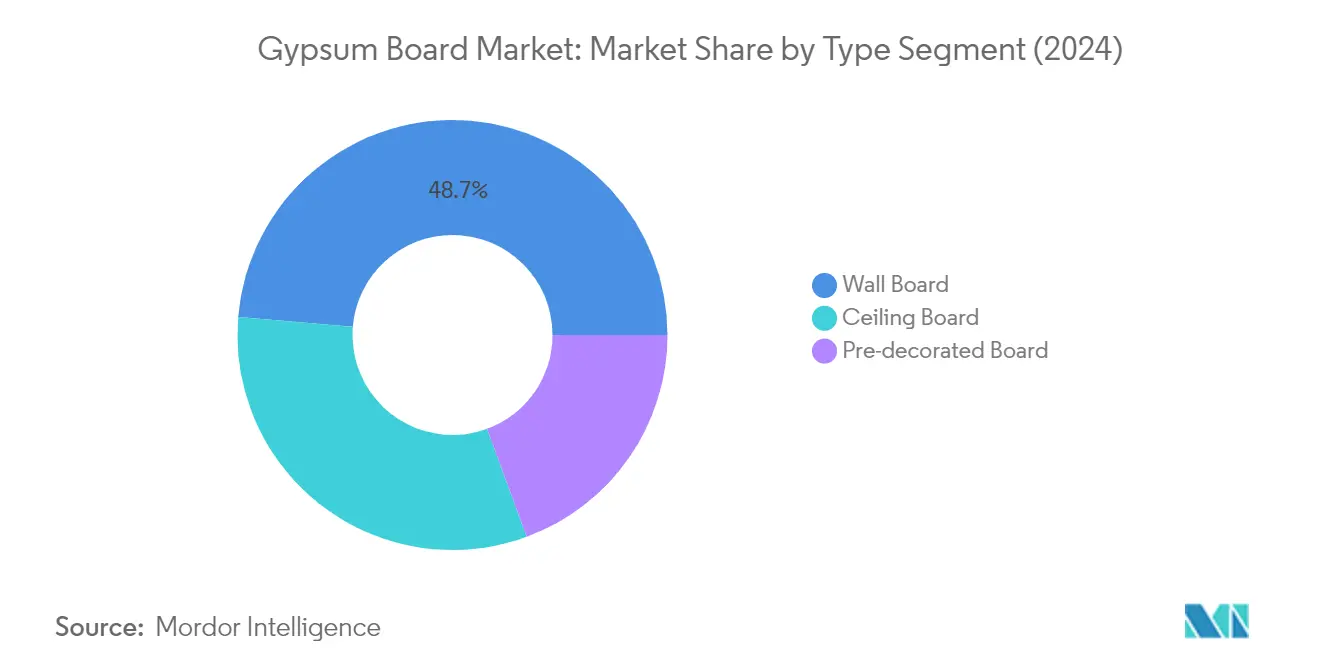

Segment Analysis: By Type

Wall Board Segment in Gypsum Board Market

The wall board segment dominates the global gypsum board market, accounting for approximately 49% of the total market share in 2024. Wall boards have emerged as the preferred choice in both residential and commercial construction due to their widespread acceptance as a replacement for traditional plaster and lath. The segment's strong position is driven by the rising demand for sustainable construction materials and continuous product innovation, which has increased its penetration in high-end construction applications. Wall boards are commonly used to improve the interior design of both residential and commercial buildings, offering benefits such as simple installation, cost-effectiveness, and versatility in space customization. The segment has particularly benefited from the rising trend of residential remodeling, repair, and renovation, with growing demand seen among consumers for DIY projects due to the product's ease of installation.

Ceiling Board Segment in Gypsum Board Market

The ceiling board segment represents a significant portion of the gypsum board market, offering high levels of performance in terms of fire rating, mold and moisture resistance, acoustic insulation, and thermal insulation. These boards are frequently utilized with noise-canceling acoustic ceiling tiles, enabling designers to hide MEP fixtures, including pipes and wiring. The segment's growth is particularly driven by its applications in residential, schools, hospitals, offices, cinemas, and hotels, where ceiling boards help create modern internal environments that provide occupants with comfort and safety. Ceiling boards are significantly lighter than traditional 15mm panels while maintaining equal resistance to sagging when used in ceiling assemblies, making them increasingly popular in construction projects.

Remaining Segments in Gypsum Board Market

The pre-decorated board segment completes the gypsum board market portfolio, offering specialized solutions for specific applications. Pre-decorated gypsum boards feature decorative surface coverings or coatings applied in-plant rather than on-site, providing a finished look without requiring additional treatment. These boards are particularly valued in commercial applications as they allow for changes in workspace configuration while providing maximum stability and color retention to surfaces. The segment has gained traction in various construction projects due to its low maintenance properties and ease of installation, though it should not be used in areas with high humidity or severe temperatures.

Segment Analysis: By Application

Residential Segment in Gypsum Board Market

The residential sector dominates the global gypsum board market, accounting for approximately 48% of the total market share in 2024. This significant market position is driven by the extensive use of gypsum boards in residential construction applications, including interior wall panels, ceilings, and partitions. The segment's dominance is further strengthened by increasing urbanization rates and growing housing demands across major economies. The residential sector is also experiencing the fastest growth trajectory, projected to expand at nearly 7% from 2024 to 2029, driven by substantial government initiatives for affordable housing projects worldwide. Major markets like China, India, and the United States are witnessing robust residential construction activities, with China planning to add 6.5 million new low-cost rental housing units across 40 major cities, while India's residential sector is expected to witness investments worth over USD 1.3 trillion in housing development projects.

Remaining Segments in Gypsum Board Market by Application

The institutional sector represents the second-largest segment in the gypsum board market, driven by increasing construction of educational facilities, healthcare centers, and government buildings. The sector benefits from gypsum boards' acoustic properties and fire-resistance capabilities, making them ideal for institutional buildings. The industrial sector utilizes gypsum boards primarily in manufacturing facilities, power plants, and industrial complexes, where durability and safety requirements are paramount. The commercial sector, encompassing offices, retail spaces, and hospitality buildings, leverages gypsum boards for their versatility in creating modern interior environments, particularly in high-traffic areas where sound insulation and aesthetic appeal are crucial. These segments collectively contribute to the market's diverse application portfolio, each serving specific construction requirements and safety standards.

Gypsum Board Market Geography Segment Analysis

Gypsum Board Market in Asia-Pacific

The Asia-Pacific region represents a dynamic gypsum board market, driven by rapid urbanization and infrastructure development across major economies. The region encompasses diverse markets, including China, India, Japan, and South Korea, each with unique construction trends and regulatory frameworks. The construction sector's growth, particularly in residential and commercial segments, continues to fuel demand for gypsum wallboard across these countries. Sustainable building practices and an increasing focus on interior aesthetics have also contributed to market expansion in the region.

Gypsum Board Market in China

China dominates the Asia-Pacific gypsum board market, holding approximately 78% of the regional market share. The country's construction sector remains robust, supported by ongoing urbanization initiatives and infrastructure development projects. The government's focus on sustainable construction practices and energy-efficient buildings has increased the adoption of gypsum boards. The residential construction sector, particularly in major urban centers, continues to be a primary driver of demand. Additionally, the country's commitment to developing smart cities and modern infrastructure projects has created substantial opportunities for gypsum board manufacturers.

Growth Dynamics in Chinese Market

China is experiencing the fastest growth in the Asia-Pacific region, with a projected CAGR of approximately 8% from 2024-2029. This growth is primarily driven by the country's ambitious construction plans and urban development initiatives. The government's focus on improving housing conditions and developing new urban areas continues to create strong demand for construction materials, including gypsum boards. The increasing adoption of modern construction techniques and the growing preference for quality interior finishing materials further support this growth trajectory. The commercial and institutional construction sectors also contribute significantly to market expansion.

Gypsum Board Market in North America

The North American gypsum board market is characterized by mature infrastructure and advanced construction practices across the United States, Canada, and Mexico. The region demonstrates strong demand driven by renovation activities and new construction projects. Technological advancements in manufacturing processes and an increasing focus on sustainable building materials have shaped market dynamics. The region's construction industry's emphasis on fire safety and acoustic insulation has further boosted the adoption of specialized gypsum board products.

Gypsum Board Market in United States

The United States maintains its position as the largest market in North America, commanding approximately 79% of the regional market share. The country's construction sector demonstrates robust demand across residential, commercial, and institutional segments. The growing trend of home renovation and remodeling activities has significantly contributed to market growth. The country's emphasis on energy-efficient buildings and sustainable construction practices has also driven the adoption of advanced gypsum board products. The commercial construction sector, particularly in major metropolitan areas, continues to be a significant consumer of gypsum boards.

Growth Dynamics in United States Market

The United States is projected to maintain the highest growth rate in North America, with an expected CAGR of approximately 6% from 2024-2029. This growth is supported by increasing construction activities across various sectors and rising demand for sustainable building materials. The country's focus on infrastructure development and urban renewal projects continues to drive market expansion. The growing trend toward prefabricated construction and modular buildings has also created new opportunities for gypsum board applications. Additionally, stringent building codes and safety regulations continue to support the adoption of fire-resistant gypsum board products.

Gypsum Board Market in Europe

The European gypsum board market demonstrates sophisticated demand patterns influenced by stringent building regulations and sustainability requirements across Germany, the United Kingdom, France, and Italy. The region's construction industry emphasizes energy efficiency and environmental sustainability, driving innovation in gypsum board products. The renovation and modernization of existing buildings, particularly in Western European countries, contribute significantly to market growth.

Gypsum Board Market in France

France represents the largest market for gypsum boards in Europe, driven by extensive construction and renovation activities across residential and commercial sectors. The country's strong focus on sustainable construction practices and energy-efficient buildings has fostered the adoption of advanced building materials. The government's initiatives to modernize infrastructure and improve housing conditions have created sustained demand for gypsum boards. The commercial construction sector, particularly in major urban centers, continues to be a significant consumer of these products.

Growth Dynamics in French Market

France demonstrates the strongest growth potential in the European region, supported by ongoing construction activities and renovation projects. The country's commitment to sustainable building practices and energy efficiency standards continues to drive market expansion. The increasing focus on interior aesthetics and acoustic comfort in both residential and commercial buildings has boosted demand for specialized gypsum board products. The renovation sector, particularly in historical buildings and urban areas, provides consistent demand for gypsum boards.

Gypsum Board Market in South America

The South American gypsum board market, primarily represented by Brazil and Argentina, shows growing adoption of modern construction materials and techniques. The region's construction industry is gradually shifting from traditional building methods to more efficient and sustainable practices. Brazil emerges as both the largest and fastest-growing market in the region, driven by urbanization and infrastructure development initiatives. The residential construction sector remains a key driver of demand, while commercial and institutional construction projects also contribute significantly to market growth.

Gypsum Board Market in Middle East and Africa

The Middle East and Africa region, with key markets in Saudi Arabia and South Africa, demonstrates growing adoption of modern construction materials and techniques. The region's construction industry is experiencing significant transformation, particularly in Gulf Cooperation Council countries. Saudi Arabia stands out as both the largest and fastest-growing market in the region, supported by ambitious infrastructure development plans and housing initiatives. The region's focus on developing sustainable cities and modern infrastructure continues to drive demand for quality construction materials, including gypsum boards.

Get Analysis on Important Geographic Markets

Download PDF

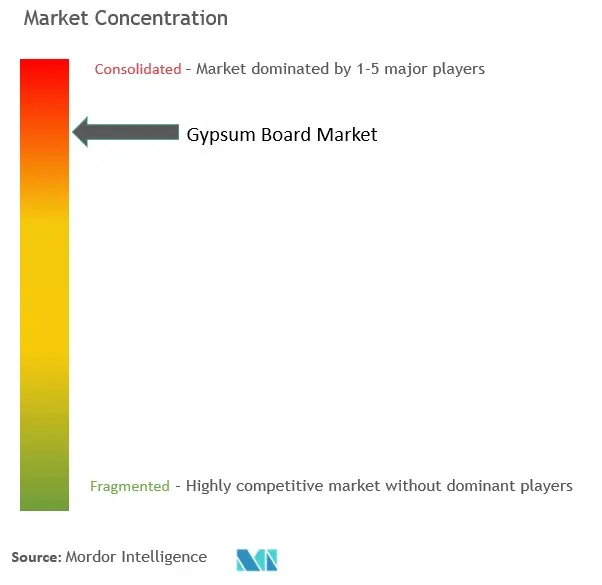

Gypsum Board Industry Overview

Top Companies in Gypsum Board Market

The global gypsum board companies market is led by major players like Saint-Gobain, USG Knauf, Etex Group, and Georgia-Pacific, who have established strong market positions through extensive manufacturing networks and brand portfolios. These gypsum board companies are driving product innovation through the development of specialized gypsum boards with enhanced properties like fire resistance, moisture resistance, and acoustic performance to meet evolving construction requirements. Operational excellence is being achieved through strategic plant locations, vertical integration into raw material supply, and investments in modern manufacturing technology. Companies are expanding their geographic presence through acquisitions and joint ventures, particularly in emerging markets with high construction growth. The focus is also on sustainability through initiatives like recycling programs and the development of eco-friendly products. Market leaders are strengthening their competitive advantage through comprehensive product offerings, technical support services, and strong distribution networks.

Consolidated Market with Strong Regional Players

The gypsum board market exhibits a consolidated structure at the global level with the top players controlling a significant market share, while remaining fragmented at regional levels with numerous local manufacturers. The market is characterized by the presence of both large diversified building material conglomerates who leverage their broad product portfolios and specialized plasterboard companies who focus on product expertise and regional strength. Major players are vertically integrated across the value chain, from gypsum mining to manufacturing and distribution, providing them with cost and supply chain advantages.

The industry has witnessed significant merger and acquisition activity as companies seek to expand their geographic footprint and manufacturing capacity. Strategic partnerships and joint ventures are common, particularly in emerging markets where local knowledge and distribution networks are crucial. Market entry barriers are relatively high due to the capital-intensive nature of manufacturing, established distribution channels, and technical expertise requirements. Regional players maintain competitiveness through local market knowledge, established customer relationships, and a focus on specific market segments or applications.

Innovation and Sustainability Drive Future Success

For established players to maintain and grow market share, the focus needs to be on continuous product innovation, particularly in developing high-performance and sustainable products that meet evolving construction standards and environmental regulations. Investment in research and development, manufacturing technology upgrades, and digital solutions for customer service will be crucial. Companies must also optimize their supply chain networks and strengthen relationships with key stakeholders, including architects, contractors, and distributors. Building strong brand equity through quality consistency and technical support services will remain important for maintaining a competitive advantage.

New entrants and smaller players can gain ground by focusing on specific market segments or geographic regions where they can build strong positions. Success factors include developing specialized products for specific applications, establishing efficient distribution networks, and building strong relationships with local construction industry stakeholders. Companies need to consider potential regulatory changes regarding building materials sustainability and safety standards. The ability to adapt to changing end-user preferences and construction practices while maintaining cost competitiveness will be crucial. Strategic partnerships with established players or complementary building material manufacturers could provide routes to market expansion. The drywall industry is poised for growth, and companies that align with these trends will likely succeed.

Gypsum Board Market Leaders

-

Saint Gobain

-

Georgia-Pacific LLC

-

USGKnauf

-

Etex Group

-

American Gypsum Company, LLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Gypsum Board Market News

- October 2023: Etex Group acquired the plasterboard and fiber cement businesses of BGC, an Australian construction materials company. This acquisition would allow Etex Group to broaden its footprint in Australia. With a wide range of products and good access to the channels, this acquisition would reinforce the company's plasterboard offerings and position it well for increasing fiber cement production.

- October 2022: USGKnauf announced its plans to build a new gypsum wallboard plant in Huedin, Cluj County. The investment is expected to support Romania's energy savings campaign, encouraging renovation in the country's dwellings.

Gypsum Board Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Increasing Demand From Residential Construction

- 4.1.2 Rising Renovation and Remodeling Activities

-

4.2 Restraints

- 4.2.1 Fluctuating Raw Material Prices

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

-

5.1 Type

- 5.1.1 Wall Board

- 5.1.2 Ceiling Board

- 5.1.3 Pre-decorated Board

-

5.2 Application

- 5.2.1 Residential Sector

- 5.2.2 Institutional Sector

- 5.2.3 Industrial Sector

- 5.2.4 Commercial Sector

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Nigeria

- 5.3.5.3 Egypt

- 5.3.5.4 Qatar

- 5.3.5.5 South Africa

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 American Gypsum Company LLC

- 6.4.2 Beijing New Building Material Public Limited Company (BNBM)

- 6.4.3 Etex Group

- 6.4.4 Everest Industries Limited

- 6.4.5 Georgia-Pacific Gypsum LLC

- 6.4.6 Global Gypsum Board Co. LLC (Gypcore)

- 6.4.7 Gypsotonne (VOLMA0)

- 6.4.8 HOLCIM Ltd

- 6.4.9 Jason Plasterboard (Jiaxing) Co. Ltd

- 6.4.10 National Gypsum Services Company

- 6.4.11 Osman Group

- 6.4.12 PABCO

- 6.4.13 Saint-Gobain

- 6.4.14 USGKnauf

- 6.4.15 VANS Gypsum

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Future Investments in the Construction Sector

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Gypsum Board Industry Overview

Gypsum board, also known as drywall or plasterboard, is a building material composed of gypsum core sandwiched between paper facings. It is commonly used for interior wall and ceiling construction in residential, commercial, and institutional buildings. Gypsum boards are available in various thicknesses and sizes to suit different applications and construction requirements. They provide a smooth and durable surface for painting, wallpapering, or decorative finishes.

The gypsum board market is segmented by type, application, and geography. By type, the market is segmented into wallboard, ceiling board, and pre-decorated board. By application, the market is segmented into the residential, institutional, industrial, and commercial sectors. The report also covers the market sizes and forecasts for the gypsum board market in 27 countries across major regions. For each segment, the market sizes and forecasts are provided in terms of volume (million square meters).

| Type | Wall Board | ||

| Ceiling Board | |||

| Pre-decorated Board | |||

| Application | Residential Sector | ||

| Institutional Sector | |||

| Industrial Sector | |||

| Commercial Sector | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Thailand | |||

| Malaysia | |||

| Indonesia | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Turkey | |||

| Russia | |||

| NORDIC | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| Nigeria | |||

| Egypt | |||

| Qatar | |||

| South Africa | |||

| UAE | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Gypsum Board Market Research FAQs

How big is the Gypsum Board Market?

The Gypsum Board Market size is expected to reach 16.89 billion square meters in 2025 and grow at a CAGR of 6.15% to reach 22.76 billion square meters by 2030.

What is the current Gypsum Board Market size?

In 2025, the Gypsum Board Market size is expected to reach 16.89 billion square meters.

Who are the key players in Gypsum Board Market?

Saint Gobain, Georgia-Pacific LLC, USGKnauf, Etex Group and American Gypsum Company, LLC are the major companies operating in the Gypsum Board Market.

Which is the fastest growing region in Gypsum Board Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Gypsum Board Market?

In 2025, the North America accounts for the largest market share in Gypsum Board Market.

What years does this Gypsum Board Market cover, and what was the market size in 2024?

In 2024, the Gypsum Board Market size was estimated at 15.85 billion square meters. The report covers the Gypsum Board Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Gypsum Board Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Gypsum Board Market Research

Mordor Intelligence offers a comprehensive analysis of the gypsum board and building material industry. We leverage decades of expertise in construction material research. Our extensive coverage includes the complete ecosystem of drywall, plasterboard, and wallboard segments. This includes a detailed analysis of regular gypsum board, acoustic gypsum board, and type x gypsum board varieties. The report PDF, available for immediate download, provides in-depth insights into wall panel technologies and building material innovations.

The report examines crucial segments such as ceiling board applications, interior wall panel systems, and partition board solutions across the construction material market. Stakeholders gain valuable insights into wall finishing trends, interior finishing developments, and wall lining technologies. Our analysis covers the entire wall system spectrum, from gypsum ceiling installations to building board applications. We provide comprehensive construction board market intelligence that helps industry leaders make informed decisions about their interior wall system strategies.