Gynecology Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

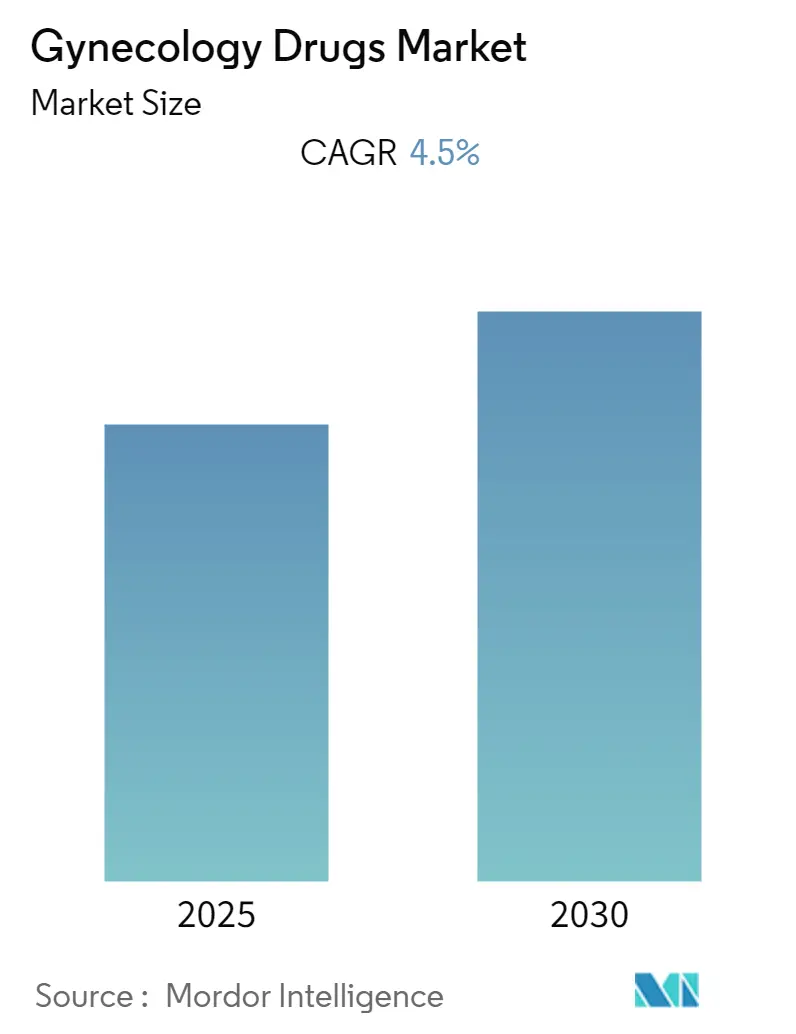

| Market Size (2025) | USD 72.97 Billion |

| Market Size (2030) | USD 92.25 Billion |

| Growth Rate (2025 - 2030) | 4.50% CAGR |

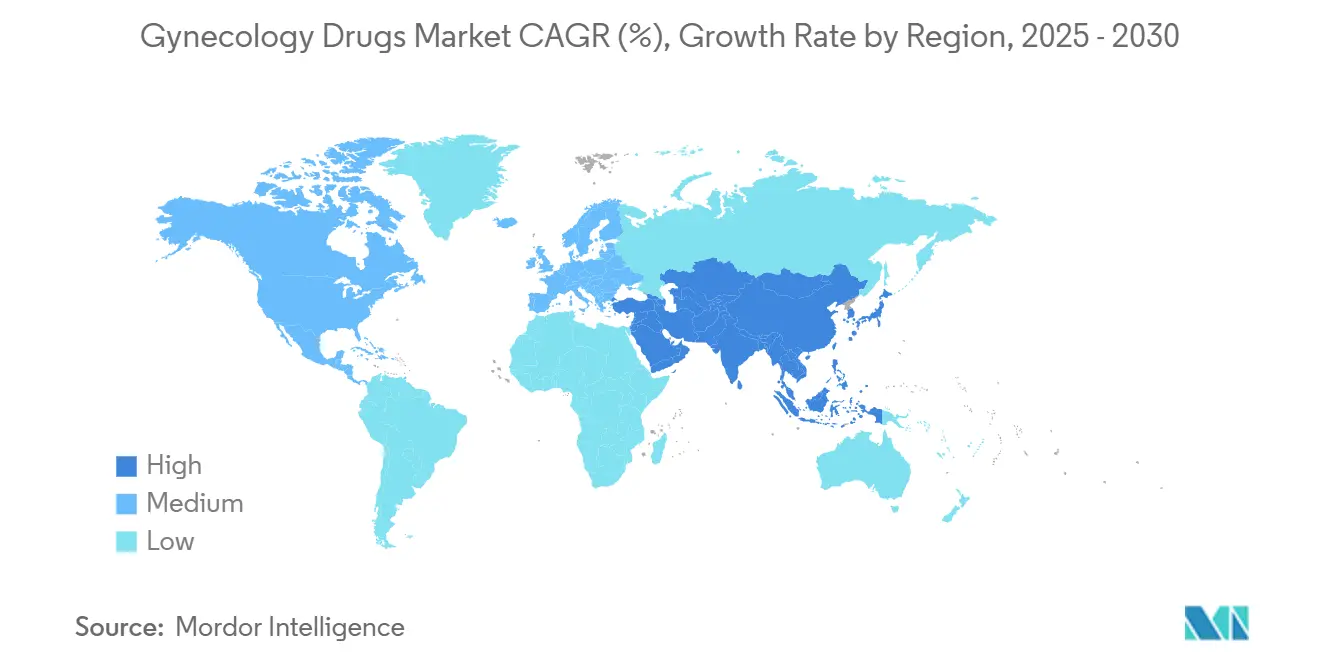

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gynecology Drugs Market Analysis by Mordor Intelligence

The gynecology drugs market size reached USD 72.97 billion in 2025 and is projected to climb to USD 92.25 billion by 2030 at a 4.8% CAGR, underscoring steady momentum despite supply-chain headwinds and patent expiries. Demographic aging, rapid diagnostic advances, and the FDA’s ongoing reassessment of black-box warnings on hormone therapy together create a supportive regulatory climate that could widen therapeutic adoption. Breakthrough antibody-drug conjugates (ADCs) such as mirvetuximab soravtansine are rewriting standards of care in ovarian cancer, while digital pharmacy models expand contraceptive reach beyond brick-and-mortar outlets. Meanwhile, fem-tech startups secure venture capital to address polycystic ovary syndrome (PCOS) and endometriosis, adding competitive pressure on incumbents with legacy contraceptive portfolios.

Key Report Takeaways

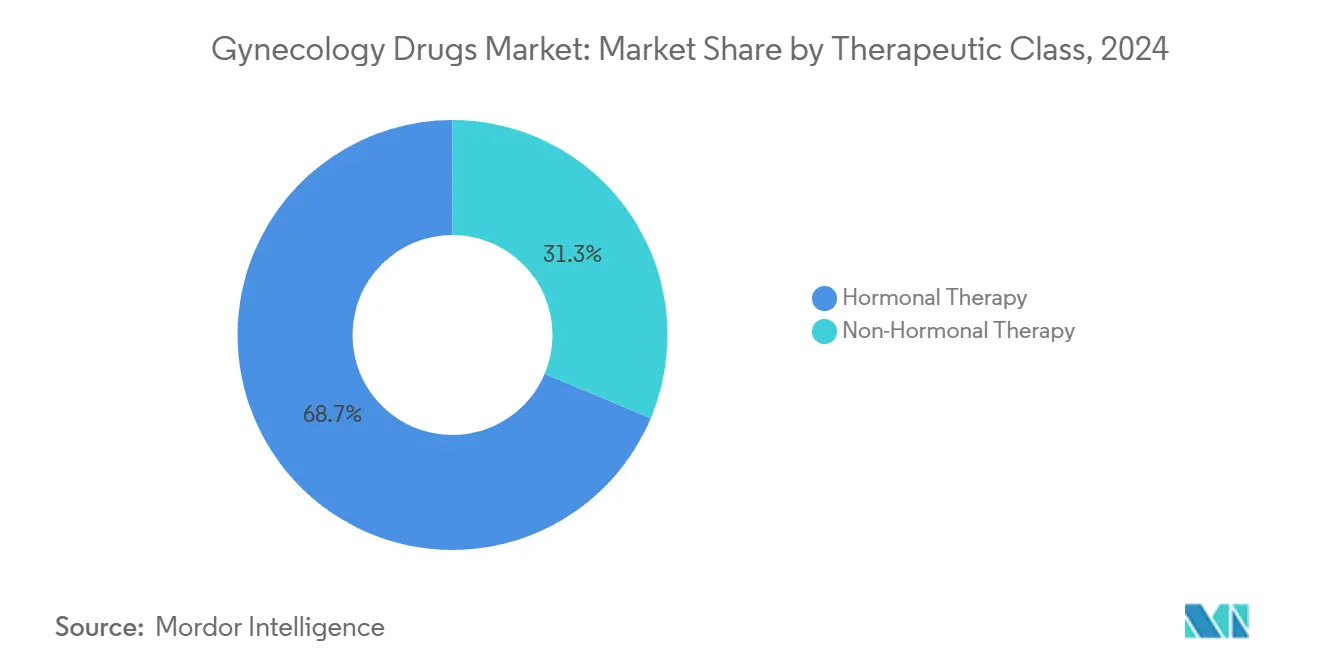

- By therapeutic class, hormonal therapies captured 68.67% of the gynecology drugs market share in 2024.

- By indication, contraception contributed 34.53% of the gynecology drugs market size in 2024, while gynecologic oncology is projected to expand at a 6.12% CAGR to 2030.

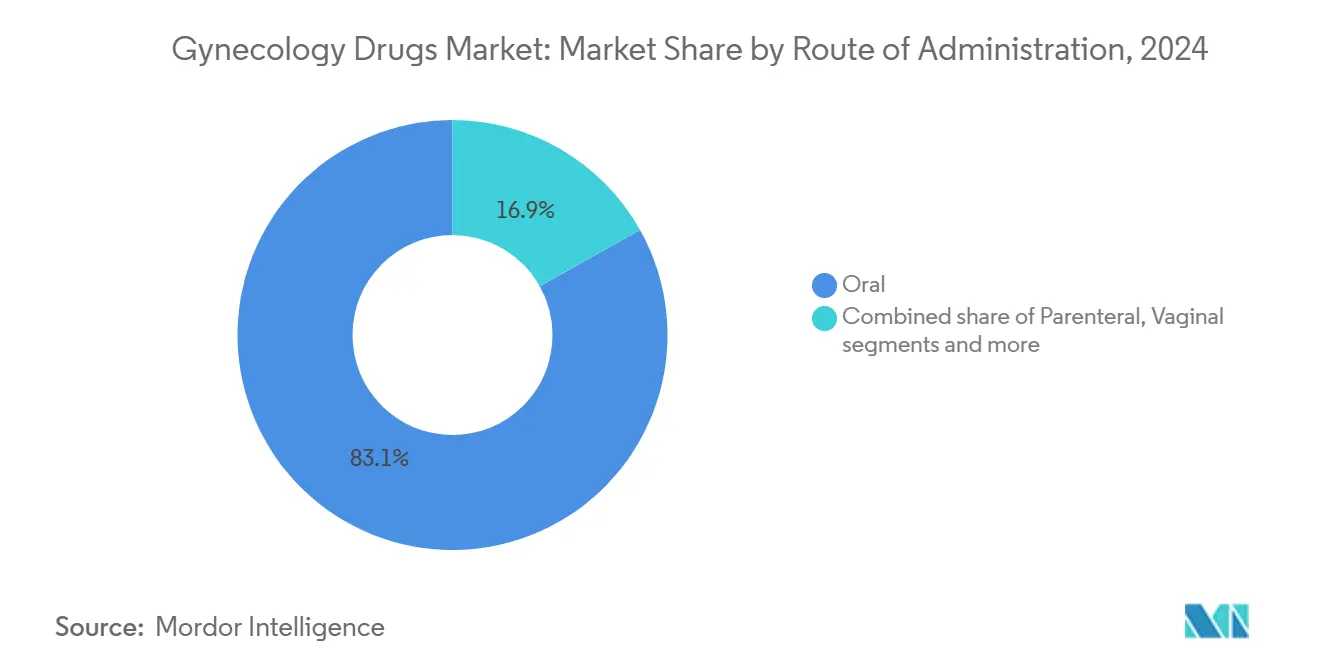

- By route of administration, oral products represented 83.12% of the gynecology drugs market size in 2024.

- By distribution channel, retail pharmacies held 46.23% revenue share in 2024; online pharmacies are forecast to advance at a 5.96% CAGR through 2030.

Global Gynecology Drugs Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for long-acting reversible contraceptives (LARCs) | +0.8% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Surging adoption of once-daily non-hormonal menopause therapies | +1.2% | North America & Europe primarily, expanding to APAC | Short term (≤ 2 years) |

| FDA fast-track approvals for antibody-drug conjugates in gynecologic oncology | +0.9% | Global, led by US regulatory precedence | Medium term (2-4 years) |

| Rapid expansion of online direct-to-consumer (DTC) fertility drug platforms | +0.7% | North America & Europe, emerging in urban APAC | Short term (≤ 2 years) |

| Rising investment in fem-tech start-ups targeting PCOS & endometriosis | +0.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Country-level reimbursement for osteoporosis biologics | +0.6% | Developed markets with established healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Long-Acting Reversible Contraceptives (LARCs)

Health-system cost analyses consistently favor LARCs over short-acting options, pushing payers to bolster reimbursement. CooperSurgical’s upgraded Paragard inserter, engineered for one-handed deployment, streamlines in-office placement workflows. Uptake is visible in low-resource clinics where copper IUDs reduce supply-chain dependency and follow-up visits. Policy makers now bundle counseling for LARCs into preventive-care visits, aligning with public-health objectives that target unintended pregnancies. These structural enablers stand to funnel recurrent demand into the gynecology drugs market over the medium term. As more Medicaid programs waive insertion fees, provider adoption is poised to quicken further.

Surging Adoption of Once-Daily Non-Hormonal Menopause Therapies

Phase III data for Bayer’s elinzanetant confirmed significant vasomotor symptom relief without estrogen exposure, validating neurokinin antagonism as an effective pathway. The FDA approval of fezolinetant set a regulatory precedent in 2024, although post-launch liver-monitoring requirements heightened pharmacovigilance expectations. An estimated 1.2 billion women will reach menopause by 2030, framing a sizeable patient pool for safer alternatives. Physicians report rising demand from individuals contraindicated for hormones, further stimulating the gynecology drugs market. Educational campaigns by industry groups now emphasize differentiation between systemic estrogens and selective neurokinin blockers to allay residual safety concerns.

FDA Fast-Track Approvals for Antibody-Drug Conjugates in Gynecologic Oncology

The agency’s rapid greenlight for mirvetuximab soravtansine demonstrated survival extension in folate-receptor-alpha-positive ovarian cancer, prompting oncologists to re-sequence chemotherapy lines. A robust pipeline targeting Nectin-4, TROP2, and tissue factor suggests sustained innovation currents. Companion diagnostics co-developed with ADCs strengthen precision-medicine paradigms and justify premium pricing. Academic cancer centers collaborate with biotech firms to run basket trials that compress development timelines. These dynamics expand parenteral volumes, enhancing the gynecology drugs market’s biologics mix through 2030.

Rapid Expansion of Online Direct-to-Consumer Fertility Drug Platforms

Integrated telehealth portals now bundle consultation, prescription, and home delivery under unified user interfaces. Companies leverage algorithmic treatment pathways to streamline refill adherence, a critical differentiator in the competitive fertility-benefits arena. HIPAA updates tightened reproductive-health data safeguards, raising the compliance bar for new entrants. The model gains further traction as state policies broaden insurance coverage for IVF medications, increasing digital pharmacy traffic.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hormone-therapy safety concerns (VTE, breast-cancer risk) | -1.1% | Global, particularly acute in developed markets | Short term (≤ 2 years) |

| Patent-cliff driven price erosion in oral contraceptives | -0.7% | Global, most pronounced in generic-friendly markets | Medium term (2-4 years) |

| Socio-cultural barriers to contraception in conservative economies | -0.5% | Emerging markets, particularly South Asia & Sub-Saharan Africa | Long term (≥ 4 years) |

| API supply-chain fragility for niche gynecologic oncology drugs | -0.4% | Global, with concentrated manufacturing vulnerabilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hormone-Therapy Safety Perceptions

Black-box warnings highlighting venous-thromboembolism and breast-cancer risk still dampen prescription volumes despite modern evidence favoring transdermal and natural-estrogen profiles. Specialist societies lobby for nuanced labeling, but behavior change among general practitioners progresses slowly. Patients over 65 remain a challenging subgroup where cardiovascular risk complicates benefit-risk dialogues. Transdermal patches offer a pharmacokinetic advantage yet struggle for formulary placement without long-term outcomes data. Until labeling updates materialize, hesitancy will cap the gynecology drugs market’s hormone-segment upside.

Patent-Cliff Price Erosion in Oral Contraceptives

Multiple branded pills lost exclusivity in 2025, unleashing a wave of low-cost generics that rebased average selling prices by double digits. Payers quickly shifted formularies, squeezing margins for innovators. Manufacturers responded with lifecycle-management tactics such as orally disintegrating tablets, but differentiation remains modest. Over-the-counter approval of a progestin-only pill added fresh competition while resetting price anchors for the entire category. Cost-sensitive emerging markets welcome the shift, yet aggregate revenue pressure tempers the gynecology drugs market’s near-term growth.

Segment Analysis

By Therapeutic Class: Portfolio Diversification Accelerates

Hormonal agents generated 68.67% revenue in 2024, sustained by entrenched physician familiarity and decades of efficacy data. Yet non-hormonal entrants grew at a robust 5.45% CAGR, carving niches in menopause and cancer care. Elevated safety profiles attract users who previously avoided hormones, broadening addressable populations. ADCs now create a hybrid sub-class blurring lines between cytotoxics and targeted biologics, pushing parenteral volumes upward. To protect incumbency, leading firms redesign progestins and estrogen analogs with improved metabolic impact. Generics crowd the low-dose contraceptive segment, but premium non-hormonal brands partially offset revenue attrition.

Forward-looking R&D increasingly incorporates sex-specific endpoints following updated FDA guidance, accelerating bench-to-clinic translation. Venture-backed biotechs exploit this opening with novel neurokinin and GnRH modulators. The gynecology drugs market consequently pivots toward a balanced mix where hormonal stalwarts coexist with innovation-driven non-hormonal franchises.

By Indication: Oncology Commands Premium Pricing

Contraception controlled 34.53% of revenue in 2024, reflecting broad public-health adoption. Nevertheless, oncology posted the fastest 6.12% CAGR as ADCs and targeted inhibitors gained traction. Infertility pharmacotherapy maintains mid-single-digit growth, fueled by rising maternal age and employer-funded IVF benefits. Postmenopausal disorders await broader hormone-safety consensus, but non-hormonal breakthroughs stimulate moderate uptake. PCOS therapies evolve beyond insulin sensitizers toward metabolic agents, expanding indication breadth. Endometriosis saw renewed interest after European endorsement of linzagolix, underscoring global unmet need.

Osteoporosis biologics achieve incremental gains as reimbursement widens. Infectious-disease antimicrobials remain stable, though topical innovations improve patient adherence. Collectively, the shifting indication mix recalibrates the gynecology drugs market toward higher biological complexity and differentiated value propositions.

By Route of Administration: Precision Therapies Propel Parenteral Growth

Oral dosing dominated with an 83.12% share in 2024, bolstered by daily contraceptives and menopause tablets. Yet parenteral formats advanced at a 5.78% CAGR, leveraging hospital infusion infrastructure for ADCs and long-acting injectables. Intravenous regimens enable controlled pharmacokinetics essential for tumor-targeting payloads, validating investment in cold-chain capacity. Subcutaneous depot injections extend contraceptive coverage up to three months, aligning with adherence-improvement strategies.

Vaginal gels and rings record steady uptake where localized delivery minimizes systemic exposure. Topical hormonal creams enjoy modest demand for urogenital atrophy, although formulary access varies. Transdermal patches gain momentum among thrombosis-risk patients, offering a bridge between convenience and safety. This evolving route distribution supports manufacturing diversification, strengthening resilience within the gynecology drugs market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Dispensing Gains Momentum

Retail pharmacies accounted for 46.23% of 2024 revenue, underpinned by insurance adjudication workflows and pharmacist counseling. However, online pharmacies accelerated at 5.96% CAGR as telemedicine prescriptions surged post-pandemic. Platform convenience, subscription refills, and discreet delivery resonate with younger demographics, especially for contraception. Hospital pharmacies retain a niche for high-complexity biologics requiring clinician oversight. Emerging omnichannel strategies now integrate digital ordering with same-day pickup at community stores, blurring channel boundaries.

Regulatory frameworks tighten cybersecurity around reproductive-health data, prompting investment in encryption and identity verification. As API tracking mandates strengthen, distributors deploy blockchain pilots for transparent provenance. These advances collectively modernize supply chains and bolster patient reach, sustaining the gynecology drugs market’s sales velocity.

Geography Analysis

North America generated 32.23% of 2024 sales, leveraging mature reimbursement and rapid FDA approvals to maintain therapeutic leadership. The region’s payer mix encourages swift formulary inclusion of innovations such as elinzanetant, although carboplatin shortages expose manufacturing fragility. Fem-tech investment ecosystems in Boston and San Francisco funnel capital into PCOS and endometriosis pipelines, invigorating competitive churn. Insurer coverage expansions for infertility drugs amplify prescription volumes, further enlarging the gynecology drugs market footprint.

Europe follows with steady uptake across contraceptive and menopause segments, supported by coordinated regulatory pathways. The European Commission’s nod for linzagolix broadened endometriosis options and underscored the continent’s receptivity to non-hormonal mechanisms. Divergent country reimbursement rules necessitate granular market-access strategies, yet centralized safety evaluations speed pan-regional launches. Aging demographics intensify demand for osteoporosis biologics, anchoring long-term growth.

Asia-Pacific is projected to deliver a 6.23% CAGR through 2030, powered by healthcare infrastructure upgrades and rising disposable incomes. Japanese and Australian markets show receptivity to advanced oncology biologics, whereas populous Southeast Asian nations concentrate on affordable contraceptives. Local API production hubs in India and China offer cost advantages yet also present geopolitical risk. Cultural barriers in certain economies moderate hormone-therapy uptake, but urban consumers increasingly prioritize evidence-based gynecological care. Government initiatives that subsidize LARC insertions invigorate segment penetration, expanding the gynecology drugs market across emerging settings.

Competitive Landscape

Market structure is moderately fragmented. Bayer, Pfizer, and Johnson & Johnson protect contraceptive franchises via incremental reformulations, while AbbVie and AstraZeneca advance oncology pipelines. Strategic acquisitions characterize 2024-2025; Insud Pharma’s USD 45 million buyout of Agile Therapeutics secured the Twirla patch, and Cosette Pharmaceuticals’ USD 430 million purchase of Mayne Pharma augmented a menopause-focused portfolio. Partnerships with digital pharmacies grow, as incumbents seek direct-to-consumer footholds without disrupting wholesaler ties. Biotechs leverage orphan-drug exclusivities for rare gynecologic cancers, commanding premium reimbursements that offset limited patient populations.

R&D spending gravitates toward non-hormonal menopause solutions and ADC payload optimization. Companies pilot AI-driven trial designs that stratify by hormone status, compressing development cycles. Manufacturing resilience gains board-level visibility after chemotherapeutic shortages; dual-sourcing of platinum APIs and fill-finish redundancy become standard. Sustainability narratives also surface, with firms trialing recyclable blister packs for oral contraceptives.

Competitive pressure intensifies as generics exploit post-2025 patent cliffs. Branded players counter through patient-support programs and loyalty apps that gamify adherence. Yet price ceilings imposed by government insurance in several markets constrain upside. Overall, diversified pipelines and omnichannel engagement strategies remain pivotal for share defense within the gynecology drugs market.

Gynecology Drugs Industry Leaders

Ferring Holding SA

TherapeuticsMD Inc.

AbbVie Inc.

Pfizer Inc.

GSK plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Viatris reported positive Phase III data for the low-dose Xulane LO patch and expects an FDA filing in late 2025

- March 2025: Final MIRASOL analysis confirmed a 32% mortality reduction with mirvetuximab soravtansine in platinum-resistant ovarian cancer

Global Gynecology Drugs Market Report Scope

Gynecological drugs are used to treat ailments related to the female reproductive system. A major shift in the lifestyles of women led to a rise in the prevalence of gynecological disorders affecting the functioning of the uterus, ovaries, and appendages.

The gynecology drugs market is segmented by therapeutics, indication, distribution channel, and geography. By therapeutics, the market is segmented as hormonal therapy and non-hormonal therapy). By indication, the market is segmented as gynecology cancers, menopausal disorder, polycystic ovary syndrome, contraception, and other indications. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America).

The report offers the value (USD) for the above segments.

| Hormonal Therapy |

| Non-Hormonal Therapy |

| Contraception |

| Gynecology Infections |

| Female Infertility |

| Postmenopausal Disorders |

| Polycystic Ovary Syndrome |

| Osteoporosis |

| Gynecology Cancer |

| Endometriosis |

| Others |

| Oral |

| Parenteral |

| Topical |

| Vaginal |

| Others |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Therapeutic Class (Value) | Hormonal Therapy | |

| Non-Hormonal Therapy | ||

| By Indication (Value) | Contraception | |

| Gynecology Infections | ||

| Female Infertility | ||

| Postmenopausal Disorders | ||

| Polycystic Ovary Syndrome | ||

| Osteoporosis | ||

| Gynecology Cancer | ||

| Endometriosis | ||

| Others | ||

| By Route of Administration (Value) | Oral | |

| Parenteral | ||

| Topical | ||

| Vaginal | ||

| Others | ||

| By Distribution Channel (Value) | Retail Pharmacies | |

| Hospital Pharmacies | ||

| Online Pharmacies | ||

| Others | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the gynecology drugs market in 2025?

The gynecology drugs market size reached USD 72.97 billion in 2025 and is projected to hit USD 92.25 billion by 2030.

Which therapeutic class generates most revenue?

Hormonal therapies continued to lead, accounting for 68.67% of 2024 sales.

What is the fastest growing regional market?

Asia-Pacific is forecast to expand at a 6.23% CAGR through 2030 as healthcare access improves.

Which indication is expected to grow the quickest?

Gynecologic oncology is projected to rise at a 6.12% CAGR, underpinned by new antibody-drug conjugates.

How are online pharmacies influencing distribution?

Online pharmacies, growing at a 5.96% CAGR, offer telehealth-enabled dispensing that broadens contraceptive and fertility drug access.

What safety issues affect hormone therapy uptake?

Persistent concerns about venous-thromboembolism and breast-cancer risk, coupled with boxed warnings, continue to limit physician prescribing.

Page last updated on: