Guidewires Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.18 Billion |

| Market Size (2030) | USD 2.81 Billion |

| Growth Rate (2025 - 2030) | 5.21% CAGR |

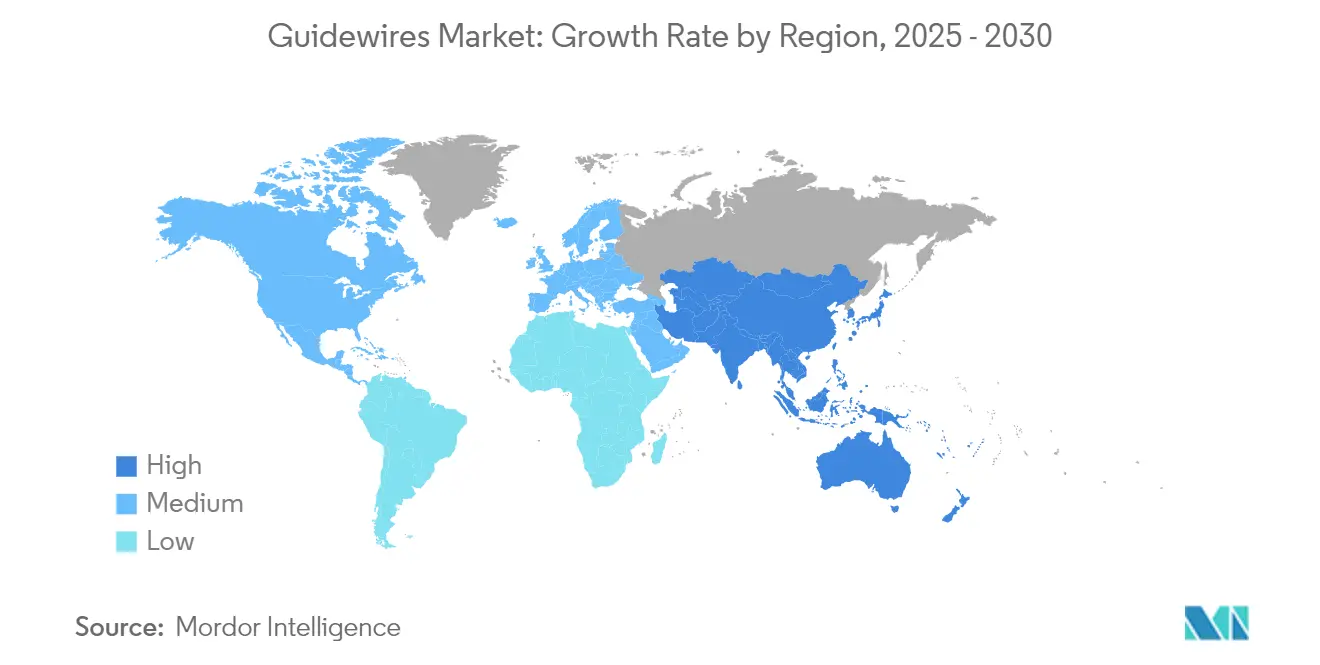

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

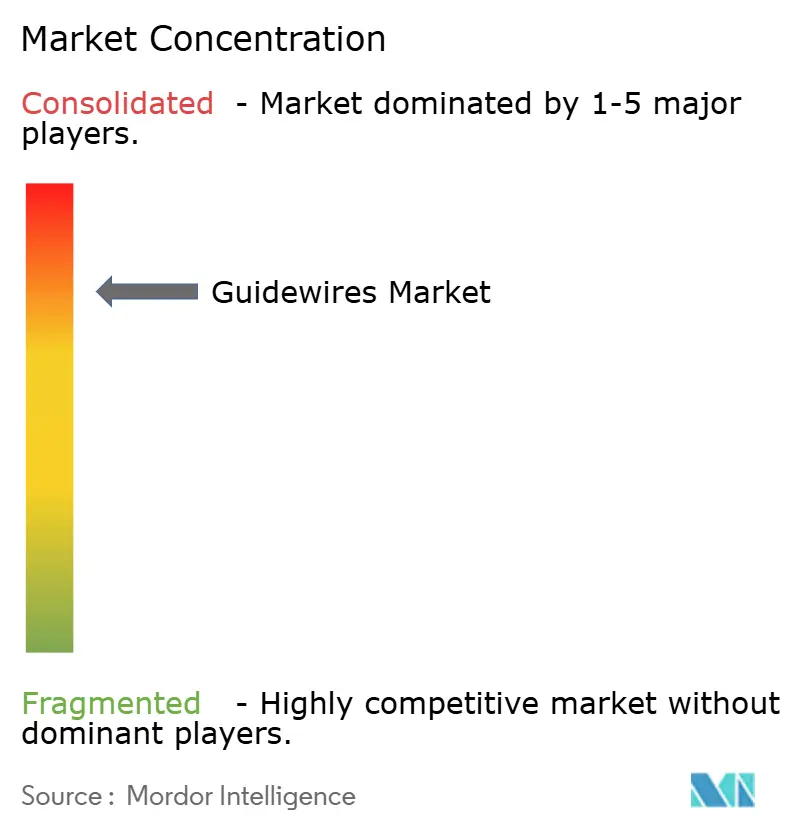

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Guidewires Market Analysis by Mordor Intelligence

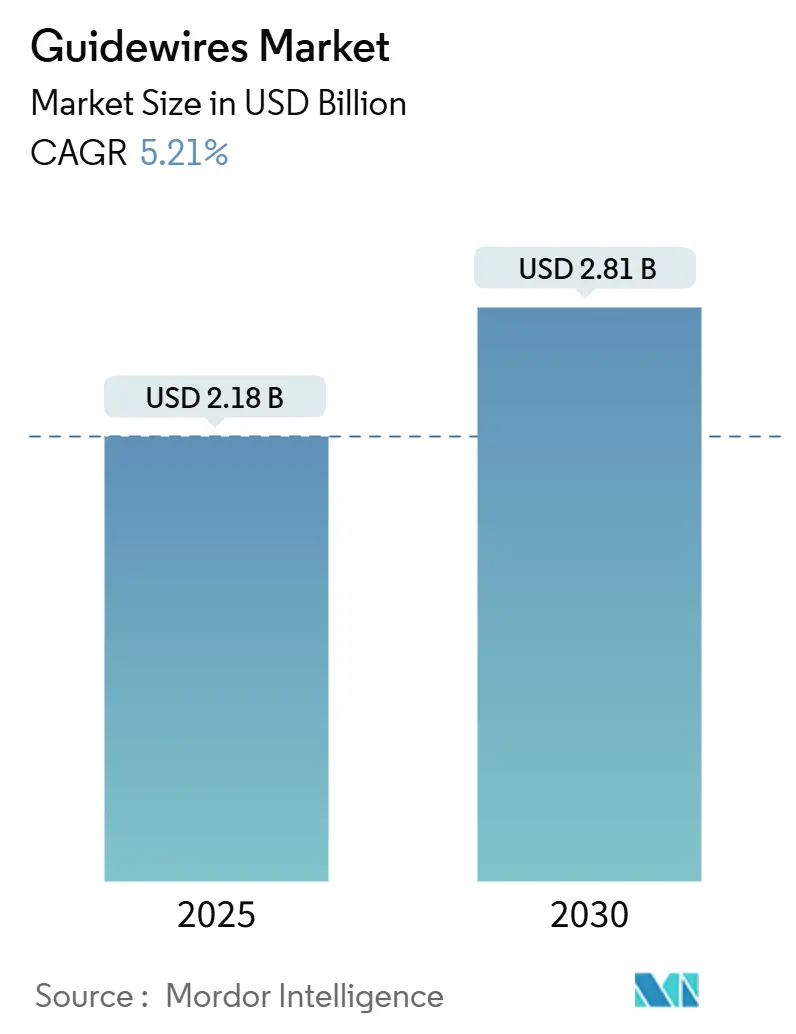

The Guidewires Market size is estimated at USD 2.18 billion in 2025, and is expected to reach USD 2.81 billion by 2030, at a CAGR of 5.21% during the forecast period (2025-2030).

Guidewires Market Overview

The guidewires industry is experiencing significant technological transformation driven by advances in material science and manufacturing processes. The integration of advanced biomaterials and smart technologies has revolutionized guidewire design, enabling enhanced navigation capabilities and improved patient outcomes. A notable development in this space was demonstrated in July 2024, when Haemonetics Corp. secured CE mark certification for its Savvywire, a pioneering sensor-guided, three-in-one guidewire tailored for transcatheter aortic valve implantation. Dubbed the world's sole sensor-guided 3-in-1 solution for Transcatheter Aortic Valve Implantation (TAVI), the SavvyWire is engineered to enhance procedural efficiency, boasting features like predictable wire performance, hemodynamic measurement, and left ventricular (LV) pacing. This advancement has set new benchmarks for innovation in cardiovascular interventions and has influenced the evolution of guidewire technology.

Strategic manufacturing initiatives and facility expansions by key industry players are reshaping the market landscape. For instance, in September 2024, Integer Holdings Corporation unveiled a significant expansion of its guidewire manufacturing facility in New Ross, County Wexford, Ireland. With a capital infusion of USD 60 million, the 80,000 sq. ft. expansion boosts the facility's manufacturing capacity by over 70%. The total footprint of the New Ross site now stands at 215,000 sq. ft., bolstered by cutting-edge manufacturing equipment to cater to the evolving needs of Integer’s clientele. This expansion has strengthened the industry's supply chain resilience and manufacturing capabilities, especially in areas such as neurovascular, structural heart, and peripheral vascular applications.

Industry consolidation and strategic partnerships are emerging as key trends shaping the competitive landscape. A significant development occurred in June 2023 when Sensome announced a partnership with Asahi Intecc to develop next-generation smart guidewires for stroke treatment. This collaboration exemplifies the industry's shift towards intelligent medical devices and demonstrates how partnerships between sensor technology experts and medical device manufacturers are driving innovation. The integration of sensing technologies and advanced materials has led to the development of guidewires that offer improved navigation and real-time feedback during procedures.

Global Guidewires Market Trends and Insights

Increasing Prevalence of Cardiovascular Diseases

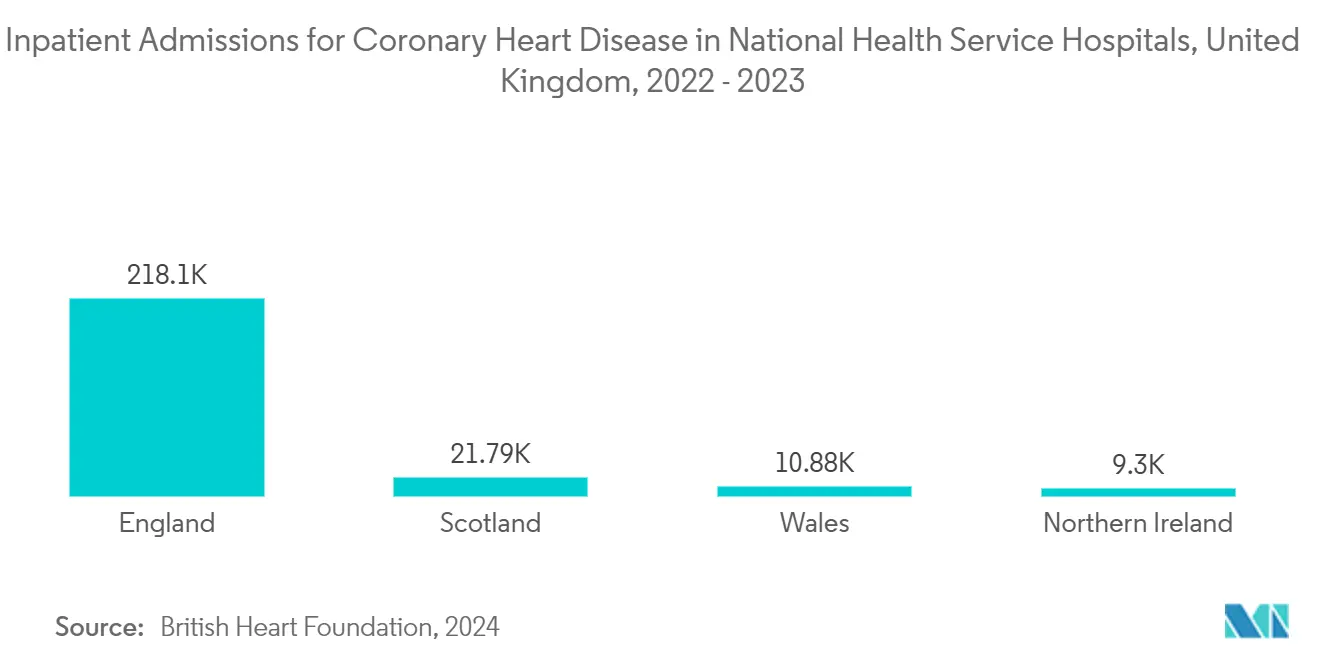

The rising incidence of cardiovascular diseases (CVD) continues to be a primary driver for the guidewires market. According to August 2023 statistics from the British Heart Foundation, approximately 620 million individuals worldwide were living with heart and circulatory diseases, representing a significant patient population requiring cardiovascular interventions. The high prevalence of angina pectoris, a leading indicator for cardiac procedures requiring guidewires, underscores the growing need for guidewire-assisted procedures in cardiac care.

Coronary heart disease (CHD) remains a critical concern in developed regions. The increasing burden of lifestyle-related risk factors, including smoking, obesity, and dietary irregularities, has contributed to the rising prevalence of cardiovascular conditions. This trend has directly influenced the demand for guidewires, as they are essential tools in diagnostic and therapeutic cardiac procedures, particularly in coronary interventions and catheterization procedures where precise navigation through blood vessels is crucial.

Increasing Demand for Minimally Invasive Surgeries

The healthcare industry has witnessed a significant shift toward minimally invasive procedures, driving the demand for specialized medical devices including guidewires. Recent studies indicate that majority of patients opt for minimally invasive treatments based on healthcare professional recommendations, highlighting the growing preference for these procedures among both medical practitioners and patients, indicating a substantial market opportunity for guidewire manufacturers.

The advantages of minimally invasive surgeries, including shorter hospital stays, reduced recovery time, and improved patient outcomes, have made them increasingly attractive to healthcare providers and patients alike. These procedures require sophisticated guidewire technology for precise navigation and placement of therapeutic devices. The integration of advanced materials and designs in guidewire manufacturing has enhanced their functionality in minimally invasive applications, particularly in complex procedures such as endovascular interventions, neurovascular treatments, and cardiac catheterizations. This technological evolution has enabled healthcare professionals to perform increasingly complex procedures with greater precision and safety, further driving the adoption of guidewires in minimally invasive surgeries.

Continuous Product Launches by Major Manufacturers

The guidewires market is characterized by ongoing innovation and frequent product launches from major manufacturers, driving market growth through enhanced technological capabilities. In April 2024, Teleflex expanded its structural heart portfolio, launching the limited market release of the Wattson temporary pacing guidewire. This innovative guidewire was designed to introduce and position catheters and other interventional devices within the heart's chambers. Additionally, it transmitted electrical signals from an external pulse generator directly to the heart. With its streamlined design, the Wattson temporary pacing guidewire enhanced procedural efficiency. Notably, the device presented a procedural alternative that mitigated potential complications, reduced steps, and lowered costs compared to traditional right ventricular pacing methods.

Similarly, in May 2024, Atraverse Medical, a medical device firm from San Diego, United States, specializing in left-heart technology, secured FDA clearance for its Hotwire radiofrequency (RF) guidewire. Designed for electrophysiologists, the Hotwire RF guidewire ensures precise access to the left heart and acts as a rail for catheter-based therapies. Atraverse touts its "universal sheath compatibility," enabling users to maintain their preferred technology during RF procedures. These continuous product innovations and launches have improved procedural outcomes and addressed specific clinical needs across various medical specialties, driving market growth through enhanced capabilities and expanded applications.

Favorable Medical Reimbursements for Guidewires in Developed Countries

The availability of favorable reimbursement policies in developed countries has significantly influenced the adoption of guidewire-assisted procedures. Healthcare systems in these regions have established comprehensive coverage frameworks for vascular and cardiovascular procedures, making advanced guidewire-based interventions more accessible to patients. The presence of specific reimbursement codes for guidewire-assisted procedures has encouraged healthcare providers to invest in these technologies, knowing that the costs can be effectively recovered through insurance and healthcare payment systems.

The reimbursement landscape has particularly benefited from the recognition of minimally invasive procedures as cost-effective alternatives to traditional surgical approaches. Insurance providers and healthcare systems have acknowledged the long-term economic benefits of these procedures, including reduced hospital stays, faster recovery times, and lower complication rates. This recognition has led to the development of more comprehensive reimbursement policies that cover a wider range of guidewire-assisted procedures. The supportive reimbursement environment has not only facilitated greater access to advanced medical procedures but has also encouraged healthcare facilities to adopt newer guidewire technologies, driving market growth through increased procedure volumes and technology adoption.

Guidewires Market Material Segment Analysis

Nitinol Segment in Guidewires Market

The Nitinol segment dominates the guidewires market, commanding approximately one-third of the market share in 2024, and is also emerging as the fastest-growing segment. This substantial market position is attributed to Nitinol's superior properties, including exceptional shape memory and superelasticity, which are crucial for navigating complex vascular anatomies. The material's ability to return to its predetermined shape when exposed to body temperature makes it particularly valuable in minimally invasive procedures. Healthcare providers increasingly prefer Nitinol guidewires due to their excellent kink resistance, biocompatibility, and fatigue resistance. The segment's growth is further supported by ongoing technological advancements in Nitinol processing techniques, enabling manufacturers to produce guidewires with enhanced performance characteristics. Recent developments in surface treatments and alloy compositions have also contributed to improved radiopacity and reduced friction, solidifying Nitinol's position as the material of choice for premium guidewires.

Guidewires Market Coating Segment Analysis

Coated Segment in Guidewires Market

The coated segment dominates the guidewires market and is also emerging as the fastest-growing segment in the guidewires market. This remarkable growth is driven by the increasing demand for guidewires with enhanced lubricity and reduced friction during complex interventional procedures. The segment's expansion is supported by technological innovations in coating materials that provide superior durability and consistent performance throughout procedures. Healthcare professionals are increasingly recognizing the benefits of coated guidewires, including reduced vessel trauma, improved maneuverability, and enhanced patient outcomes. The segment's growth is further accelerated by the rising adoption of minimally invasive procedures and the development of specialized coatings for specific applications. Recent advancements in coating technologies have also addressed previous limitations regarding coating adhesion and durability, contributing to increased market penetration.

Guidewires Market Application Segment Analysis

Cardiology Applications Segment in Guidewires Market

The cardiology applications segment dominated the guidewires market in 2024, commanding the largest market share. This substantial market position is primarily attributed to the rising prevalence of cardiovascular diseases globally and the increasing adoption of minimally invasive cardiac procedures. The segment's prominence is further strengthened by continuous technological advancements in coronary guidewire designs, enabling more precise navigation through complex vasculatures. The growing elderly population, coupled with lifestyle-related cardiac conditions, has significantly contributed to the segment's dominance. Additionally, the widespread availability of reimbursement policies for cardiac procedures in developed nations has supported market growth. The segment has also benefited from increasing investments in cardiac care infrastructure and the expanding network of catheterization laboratories worldwide. Moreover, the introduction of advanced hydrophilic coatings and improved radiopaque properties has enhanced the segment's market position.

Neurovascular Applications Segment in Guidewires Market

The neurovascular applications segment is projected to exhibit the highest growth rate from 2025 to 2030 in the guidewires market. This remarkable growth trajectory is driven by increasing cases of neurological disorders and the rising demand for minimally invasive neurovascular procedures. The segment's expansion is further fueled by technological innovations in neurovascular guidewire design, particularly in terms of flexibility and maneuverability for accessing intricate brain vessels. The growing adoption of interventional neurology procedures for stroke treatment and other cerebrovascular conditions has significantly contributed to this segment's rapid growth. Additionally, increased investment in neurovascular research and development has led to the introduction of more sophisticated guidewire products. The segment has also benefited from improving healthcare infrastructure in emerging markets and rising awareness about neurological interventions. Furthermore, the development of specialized coating technologies for neurovascular applications has enhanced the safety and efficacy of these procedures.

Guidewires Market End-User Segment Analysis

Hospitals Segment in Guidewires Market

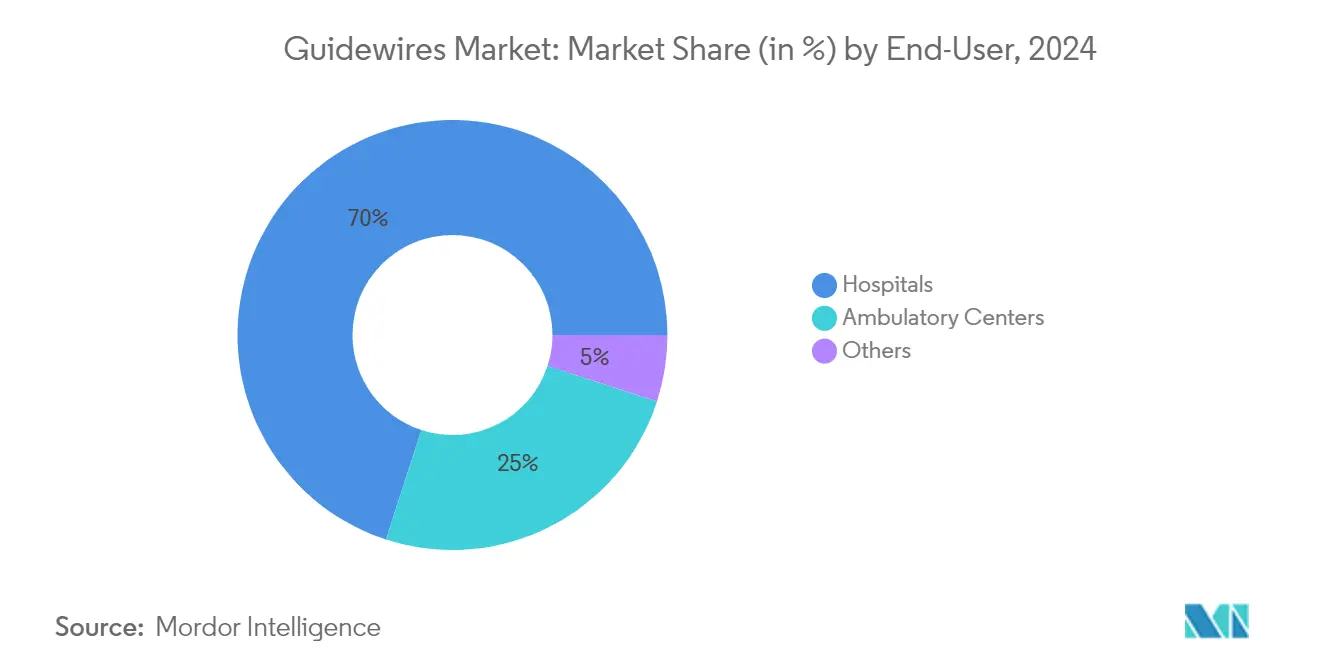

The hospitals segment dominated the guidewires market in 2024, with 70% market share. This substantial market position is primarily attributed to the sophisticated infrastructure and advanced medical facilities available in these healthcare institutions. The segment's dominance is further strengthened by the increasing volume of cardiovascular procedures, neurovascular interventions, and complex surgical operations performed in hospital settings. The presence of skilled healthcare professionals and state-of-the-art catheterization laboratories in these facilities drives the demand for various types of guidewires. Additionally, the segment benefits from favorable reimbursement policies and the ability to handle emergency procedures requiring immediate guidewire interventions. The concentration of high-risk procedures in hospital settings, coupled with the rising adoption of minimally invasive techniques, continues to solidify this segment's market leadership.

Ambulatory Centers Segment in Guidewires Market

The ambulatory centers segment is emerging as the fastest-growing segment in the guidewires market, projected to expand at a CAGR of approximately 8% from 2025 to 2030. This remarkable growth is driven by the increasing preference for outpatient procedures and the cost-effectiveness of ambulatory care settings. The segment's expansion is further fueled by technological advancements in guidewire design that enable more procedures to be performed in outpatient settings. Rising patient awareness about minimally invasive procedures and shorter recovery times associated with ambulatory care centers contributes significantly to this growth trajectory. The segment also benefits from the growing trend of same-day discharge procedures and the increasing adoption of advanced guidewire technologies in these facilities. Moreover, the expansion of ambulatory surgical centers in both urban and rural areas, coupled with improving reimbursement policies, supports this segment's rapid growth.

Guidewires Market Geography Segment Analysis

Guidewires Market in North America

North America maintains its dominant position in the global guidewires market, driven by the increasing availability of reimbursements, growing patient preference for minimally invasive surgical procedures, and strong market presence of key original equipment manufacturers (OEMs). The region's healthcare infrastructure, coupled with advanced medical facilities and high healthcare spending, creates a favorable environment for guidewire adoption. The United States, Canada, and Mexico comprise the key markets in this region, with each country contributing uniquely to the regional market dynamics through their healthcare policies and medical device regulations.

Guidewires Market in the United States

The United States leads the North American guidewires market, accounting for more than two-thirds of the market share in 2024. The country's market leadership is attributed to its sophisticated healthcare infrastructure, high healthcare expenditures, and presence of major medical device manufacturers. The growing prevalence of cardiovascular diseases, increasing adoption of minimally invasive procedures, and favorable reimbursement policies further strengthen the market position. The presence of key research institutions and continuous technological innovations in medical devices also contribute to the country's market dominance.

Guidewires Market in Canada

Canada emerges as the fastest-growing market in North America during 2025-2030. The growth is primarily driven by increasing healthcare expenditure, rising adoption of advanced medical technologies, and growing awareness about minimally invasive procedures. The country's universal healthcare system and supportive regulatory framework for medical devices create a conducive environment for market expansion. Canadian healthcare facilities' increasing focus on upgrading their medical infrastructure and adopting innovative medical devices further accelerates market growth.

Guidewires Market in Europe

Europe represents a significant market for guidewires, characterized by its advanced healthcare infrastructure, aging population, and strong presence of medical device manufacturers. The region's market is driven by the ongoing consolidation of healthcare providers, strengthening distribution capabilities of major OEMs, and increasing adoption of minimally invasive procedures. Key markets, including Germany, France, the United Kingdom, Italy, and Spain, contribute significantly to the regional market dynamics through their diverse healthcare systems and medical device regulations.

Guidewires Market in Germany

Germany maintains its position as the largest guidewires market in Europe, holding more than one fourth of the regional market share in 2024. The country's market leadership is supported by its robust healthcare system, high healthcare spending, and strong presence of medical device manufacturers. The growing prevalence of cardiovascular diseases, increasing geriatric population, and advanced medical infrastructure contribute to the market's strength. Germany's focus on healthcare innovation and adoption of advanced medical technologies further reinforces its market position.

Guidewires Market in France

France demonstrates the highest growth potential in the European region during 2025-2030. The country's market growth is driven by increasing investments in healthcare infrastructure, rising adoption of minimally invasive procedures, and growing awareness about advanced medical technologies. The French healthcare system's emphasis on quality care and innovation in medical devices supports market expansion. The presence of skilled healthcare professionals and increasing focus on specialized medical procedures further accelerates market growth.

Guidewires Market in Asia-Pacific

The Asia-Pacific region represents a rapidly evolving market for guidewires, characterized by improving healthcare infrastructure, increasing healthcare expenditure, and growing awareness about minimally invasive procedures. The region encompasses diverse markets, including China, Japan, India, South Korea, and Australia, each contributing uniquely to the market dynamics. The increasing prevalence of lifestyle-related diseases, growing medical tourism, and rising adoption of advanced medical technologies drive market growth across the region.

Guidewires Market in China

China emerges as the largest market for guidewires in the Asia-Pacific region, supported by its vast population base, improving healthcare infrastructure, and increasing healthcare expenditure. The country's focus on healthcare modernization, growing adoption of minimally invasive procedures, and rising prevalence of cardiovascular diseases drive market growth. The presence of domestic manufacturers and increasing investments in healthcare technology further strengthen China's market position.

Guidewires Market in India

India represents the fastest-growing market in the Asia-Pacific region, driven by its improving healthcare infrastructure, increasing medical tourism, and growing adoption of advanced medical technologies. The country's large patient pool, rising healthcare expenditure, and growing awareness about minimally invasive procedures contribute to market growth. The government's initiatives to improve healthcare accessibility and increasing investments in medical device manufacturing further accelerate market expansion.

Guidewires Market in Middle East and Africa

The Middle East and Africa guidewires market shows promising growth potential, driven by improving healthcare infrastructure, increasing healthcare tourism, and rising adoption of advanced medical technologies. The region's market is characterized by significant investments in healthcare infrastructure, particularly in Gulf Cooperation Council (GCC) countries. GCC emerges as the largest market in the region, while South Africa shows the fastest growth potential. The increasing focus on healthcare modernization, the rising prevalence of lifestyle diseases, and growing awareness about minimally invasive procedures contribute to market growth across the region.

Guidewires Market in South America

The South American guidewires market demonstrates significant growth potential, driven by improving healthcare infrastructure, increasing healthcare expenditure, and rising awareness about minimally invasive procedures. Brazil and Argentina emerge as the key markets in the region, with Brazil leading in terms of market size and also showing rapid growth potential. The region's market is characterized by increasing medical tourism, growing adoption of advanced medical technologies, and rising prevalence of cardiovascular diseases. Government initiatives to improve healthcare accessibility and increasing investments in medical infrastructure further support market growth.

Competitive Landscape

Top Companies in the Guidewires Market

Prominent players, including Abbott Laboratories, B Braun SE, Boston Scientific Corporation, Cardinal Health, Cook Group, Johnson & Johnson, Medtronic plc, Olympus Corporation, Stryker Corporation, and Terumo Corporation lead the global guidewires market. These companies demonstrate a strong market presence through continuous product innovation, particularly in developing advanced guidewire materials like nitinol and hybrid combinations that offer superior flexibility and maneuverability. The industry witnesses regular strategic collaborations between manufacturers and healthcare providers to enhance product development and distribution capabilities. Companies are increasingly focusing on expanding their geographical presence through regional manufacturing facilities and distribution networks, particularly in emerging markets. Operational agility is demonstrated through quick adaptation to changing healthcare needs and regulatory requirements while maintaining high-quality standards in manufacturing processes.

Market Consolidation Drives Industry Evolution Pattern

The guidewires market exhibits a moderately consolidated structure, with global medical device conglomerates holding significant market share alongside specialized manufacturers focusing on specific application areas. These major players leverage their extensive R&D capabilities, established distribution networks, and strong financial resources to maintain their market positions. The industry is characterized by a mix of vertically integrated companies that control the entire value chain from manufacturing to distribution and specialized players that focus on specific market segments or geographical regions.

The market has witnessed considerable merger and acquisition activity, primarily driven by large medical device companies seeking to expand their product portfolios and geographical reach. Strategic partnerships and licensing agreements are common, particularly for accessing new technologies and entering emerging markets. Regional players, especially in Asia-Pacific, are gradually gaining prominence through cost-effective manufacturing capabilities and growing domestic market presence, though global players continue to dominate in terms of technology leadership and market share.

Innovation and Adaptability Define Future Success

Success in the guidewires market increasingly depends on companies' ability to develop innovative products that address specific clinical needs while maintaining cost-effectiveness. Market leaders are investing heavily in research and development to create guidewires with enhanced properties such as improved torque transmission, better visibility under imaging, and reduced friction. Companies are also focusing on developing application-specific guidewires for different medical procedures while maintaining strong relationships with healthcare providers and ensuring comprehensive training and support services.

For new entrants and smaller players, success lies in identifying and serving niche market segments or specific geographical regions where they can build strong positions. The increasing focus on minimally invasive procedures and the growing demand for specialized guidewires in emerging markets present opportunities for market expansion. However, companies must navigate complex regulatory requirements, maintain high-quality standards, and build strong distribution networks to succeed. The ability to adapt to changing healthcare delivery models and maintain strong relationships with healthcare providers will be crucial for long-term success in this market.

Guidewires Industry Leaders

-

Abbott Laboratories

-

B Braun SE

-

Boston Scientific Corporation

-

Medtronic plc

-

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Sensome signed an exclusive commercial distribution agreement with Cosmotec to distribute its innovative clot-sensing guidewire in the Japanese market. This partnership aims to expand access to advanced medical devices across Japan.

- June 2024: Silk Road Medical announced a definitive agreement to be acquired by Boston Scientific. This strategic acquisition aims to expand Boston Scientific's portfolio of minimally invasive treatment options for cardiovascular diseases and leverage its commercial infrastructure to accelerate the adoption of TCAR technology.

- June 2024: Medtronic launched the Steerant Aortic Guidewire specifically designed for EVAR and TEVAR procedures to facilitate catheter placement and exchange during diagnostic or interventional procedures in the aorta.

- March 2024: Baylis Medical Technologies Inc. received 510(k) clearance and launched the PowerWire Pro Radiofrequency (RF) Guidewire in the U.S. This new device facilitates venous stent recanalization for total occlusions using radiofrequency technology.

- May 2023: EOSolutions Corp. introduced the Dr. Banner Balloon Guide Catheter (BGC) with the largest inner diameter of 0.091 inches, designed to complement their Thinline 8F Sheath for maximal compatibility.

Global Guidewires Market Report Scope

As per the scope of the report, guidewires are medical grade specialized wires made, which are inserted in the body, to introduce and position balloon catheters and other devices within the coronary system, and to perform surgeries or treat chronic diseases. They also facilitate the alignment of interventional devices and may function as measuring tools.

The guidewires market is segmented by material, coating, application, end-user, and geography. Based on material, the market is segmented into nitinol, stainless steel, and others. On the basis of coating, the market is bifurcated into coated and non-coated. Based on application, the market is segmented into cardiology, neurovascular, urology, and other applications. By end-user, the market is segmented into hospitals, ambulatory centers, and others. On the basis of geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Nitinol |

| Stainless Steel |

| Others |

| Coated |

| Non-Coated |

| Cardiology |

| Neurovascular |

| Urology |

| Other Applications |

| Hospitals |

| Ambulatory Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Nitinol | |

| Stainless Steel | ||

| Others | ||

| By Coating | Coated | |

| Non-Coated | ||

| By Application | Cardiology | |

| Neurovascular | ||

| Urology | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Ambulatory Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Guidewires Market?

The Guidewires Market size is expected to reach USD 2.18 billion in 2025 and grow at a CAGR of 5.21% to reach USD 2.81 billion by 2030.

What is the current Guidewires Market size?

In 2025, the Guidewires Market size is expected to reach USD 2.18 billion.

Which is the fastest growing region in Guidewires Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Guidewires Market?

In 2025, the North America accounts for the largest market share in Guidewires Market.

What years does this Guidewires Market cover, and what was the market size in 2024?

In 2024, the Guidewires Market size was estimated at USD 2.07 billion. The report covers the Guidewires Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Guidewires Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: