Greenhouse Film Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

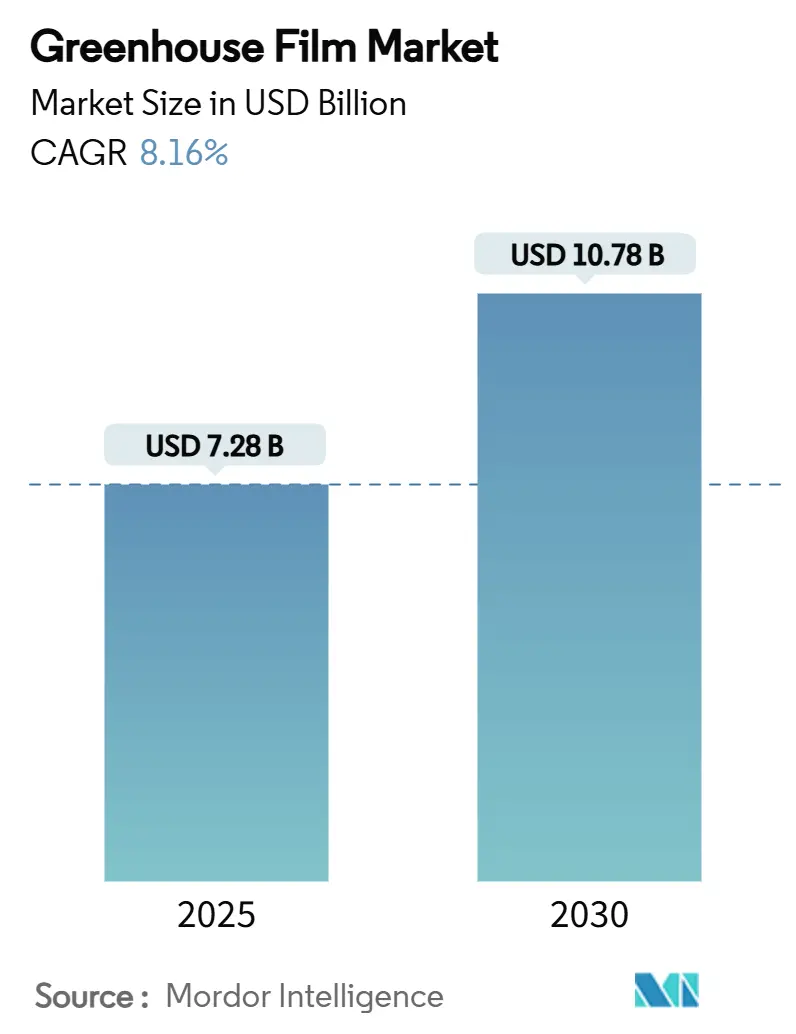

| Market Size (2025) | USD 7.28 Billion |

| Market Size (2030) | USD 10.78 Billion |

| Growth Rate (2025 - 2030) | 8.16% CAGR |

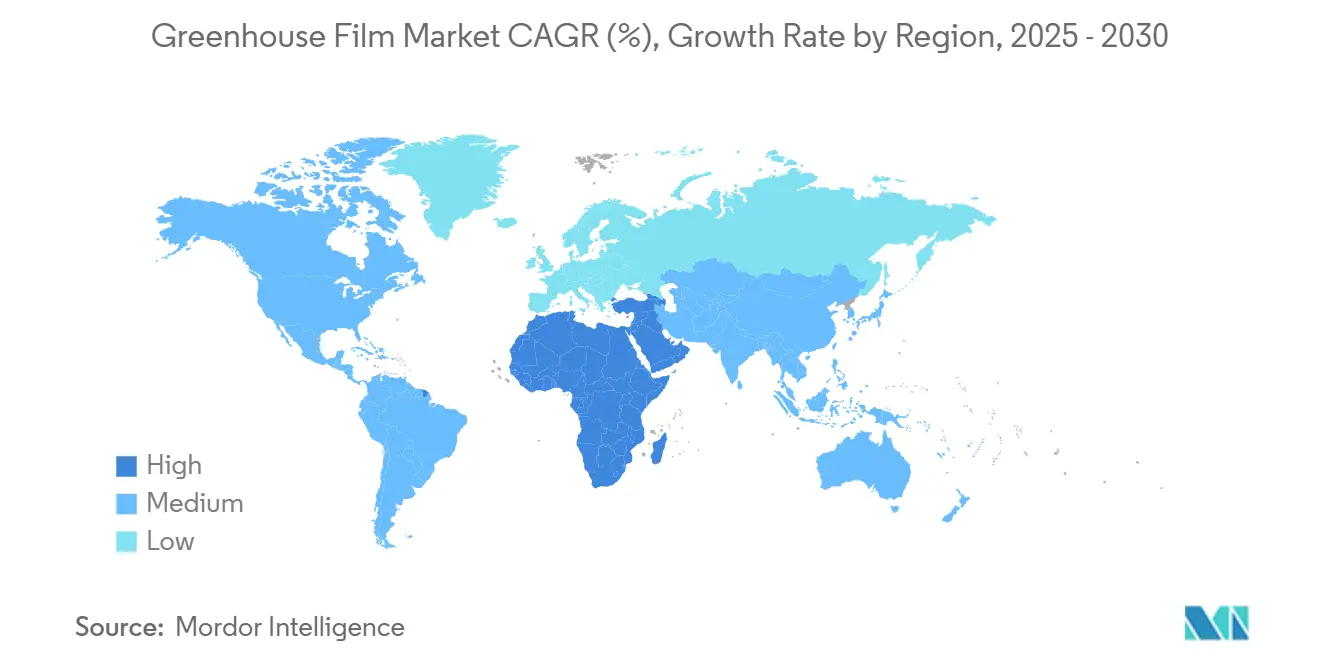

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Greenhouse Film Market Analysis by Mordor Intelligence

The Greenhouse Film Market size is estimated at USD 7.28 billion in 2025, and is expected to reach USD 10.78 billion by 2030, at a CAGR of 8.16% during the forecast period (2025-2030). Growth rests on the rising need for controlled-environment agriculture that shields crops from erratic weather, secures local supply chains, and supports year-round production. Demand accelerates as multilayer polyethylene films with UV stabilizers and spectral-shifting additives raise yields while lowering energy costs. Asia-Pacific keeps its lead on the strength of large-scale installations in China, India’s expanding protected-cultivation programs, and competitive regional resin supply. North America and Europe maintain technology leadership through investments in durable films that integrate sensors, antimicrobial compounds, and recycling-ready resins.

Key Report Takeaways

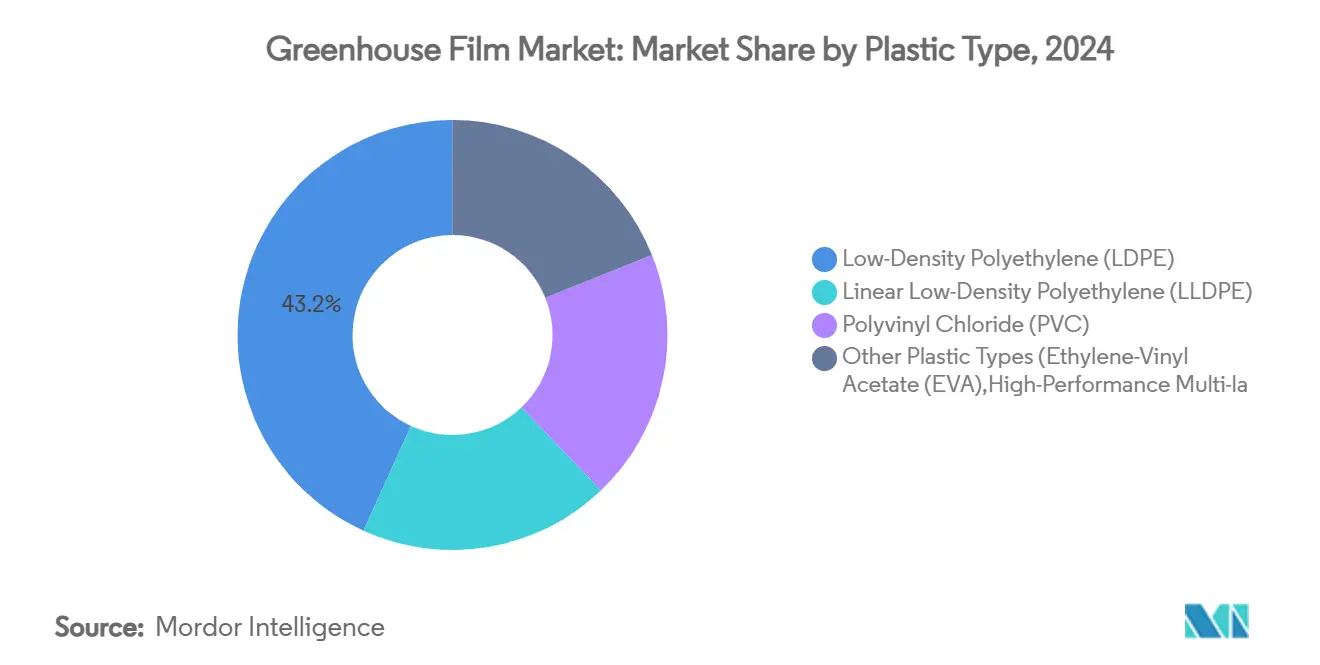

- By plastic type, Low-Density Polyethylene held a 43.19% greenhouse film market share in 2024, while high-performance “Other” plastics are set to grow at 8.79% CAGR to 2030.

- By thickness, films below 200 microns captured 47.45% of the greenhouse film market size in 2024; thicker films above 200 microns are forecast to expand at 8.64% CAGR through 2030.

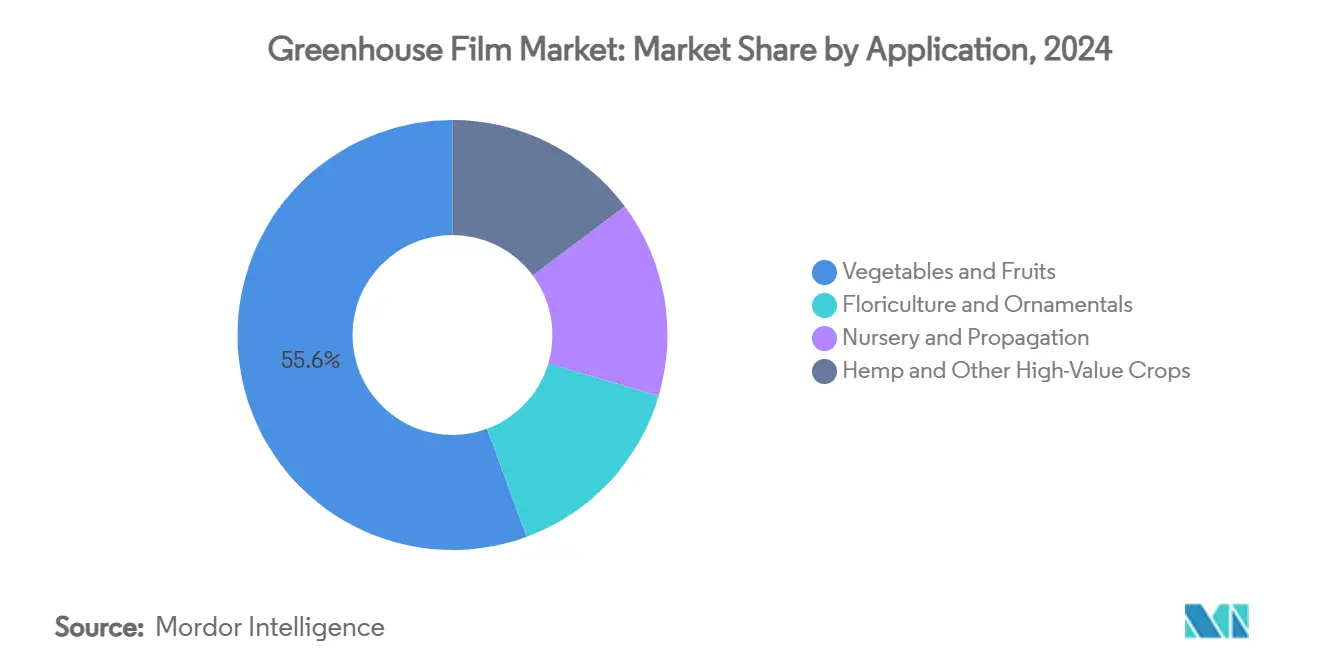

- By application, fruits and vegetables commanded 55.61% revenue share of the greenhouse film market in 2024; hemp and other high-value crops post the fastest CAGR at 9.07% to 2030.

- By geography, Asia-Pacific accounted for 48.83% of global revenue in 2024, while the Middle East & Africa segment is projected to register an 8.81% CAGR to 2030.

Global Greenhouse Film Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from fresh-produce supply chains | +2.1% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Expansion of greenhouse-protected cultivation acreage | +1.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Surge in controlled-environment agriculture investments | +1.5% | North America & EU, emerging in APAC | Short term (≤ 2 years) |

| Integration of luminescent spectral-shifting films | +0.9% | Global, early adoption in advanced markets | Medium term (2-4 years) |

| Adoption of antiviral and antimicrobial PE film additives | +0.7% | Global, accelerated in post-pandemic markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand from fresh-produce supply chains

Retailers and food-service operators prioritize supply continuity by locating greenhouses closer to urban centers. Proximity curbs freight costs, trims spoilage, and supports consumer expectations for traceable produce. Rabobank notes that Canadian and U.S. growers expanded vegetable greenhouse floor space by double digits in 2024. Crop yields are 15–30% higher than comparable field production, and shelf-life gains cut retailer waste—benefits that reinforce long-term contracts between growers and major grocers.

Expansion of greenhouse-protected cultivation acreage

Global protected-cultivation surface now exceeds 1.3 million ha, with China alone holding 60.4% of total area. Government subsidies for plastic-house construction in India, Vietnam, and Morocco lower adoption barriers for small farmers and spur local food security programs. Greenhouses show up to 90% water-use savings over open-field cultivation, a critical feature in arid Asia and MEA regions where water scarcity threatens staple food supplies.

Surge in controlled-environment agriculture investments

Venture capital and corporate investors injected more than USD 800 million into greenhouse hardware and automation startups during 2024. Hippo Harvest raised USD 21 million to scale robotic micro-greenhouses, while Ridder Drive Systems earmarked USD 70 million for climate-control and automation platforms. Funding accelerates R&D in advanced resins, thin-film coatings, and IoT-ready greenhouse envelopes that lower labor inputs and energy bills.

Integration of luminescent spectral-shifting films

Spectral-shifting layers convert UV/blue photons into red wavelengths that plants use more efficiently. Nature Food reports yield boosts above 20% in lettuce when luminescent films replace standard polyethylene covers[1]Yu Jiang et al., “Highly Efficient Luminescent Photonic Films for Greenhouse Agriculture,” Nature Food, nature.com. Quantum-dot films demonstrate comparable tomato yields with lower daily light integral, allowing operators to downsize supplemental lighting loads. Fiber-coupled concentrators tested in commercial trials funneled 10% extra photosynthetically active radiation into lower canopies, delivering a 7% production lift in vine crops.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short functional life versus rigid glazing sheets | -1.2% | Global, particularly in harsh climate regions | Medium term (2-4 years) |

| Escalating plastic-waste regulations and ESG pressures | -0.8% | North America & EU, expanding globally | Long term (≥ 4 years) |

| Volatile ethylene and EVA feedstock pricing | -0.6% | Global, concentrated in Asia-Pacific production | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Short functional life versus rigid glazing sheets

Single-layer LDPE films typically demand replacement every 3–5 years, adding downtime labor and waste-management costs. Multilayer co-extrusion and UV-block additives now stretch service life to 7–10 years under temperate conditions, yet rigid polycarbonate or glass panels still last 15–20 years. Operators weigh lower up-front costs against higher lifetime replacement cycles, especially in hail-prone or high-UV regions. The market responds with thicker (>200 micron) films that combine tensile strength with improved light diffusion, narrowing the durability gap.

Escalating plastic-waste regulations and ESG pressures

California’s extended producer responsibility law and the EU’s Packaging & Packaging Waste Regulation assign end-of-life costs to manufacturers. Berry Global boosted post-consumer recycled polyethylene usage by 36% in 2024 and targets 30% circular content across film lines by 2030[2]Berry Global, “2024 Sustainability Report,” berryglobal.com. Dow-Mitsui Polychemicals rolled out biomass-derived EVA and LDPE grades with ISCC PLUS certification to help greenhouse operators meet Scope 3 emission goals without sacrificing film performance. Research into fully degradable urea-formaldehyde/PVA composites shows promise for low-residue mulch and tunnel covers.

Segment Analysis

By Plastic Type: Premium Materials Gain on LDPE’s Scale Advantage

Low-Density Polyethylene remains the cornerstone of the greenhouse film market, accounting for a 43.19% 2024 share. Global resin capacity, ease of extrusion, and proven toughness keep LDPE price-competitive for multi-hectare greenhouses. The greenhouse film market size for LDPE based covers is projected to advance in lockstep with refurbishment cycles, yet cost instability tied to ethylene feedstock leaves margins thin for processors. Other plastic types—chiefly multilayer EVA copolymers, polyolefin blends, and nanocomposite laminates—are on an 8.79% CAGR trajectory through 2030. EVA’s higher clarity, adhesive compatibility, and elasticity enable thicker coatings that cut replacement frequency while accommodating smart-film sensor grids. Graphene-reinforced EVA laminates improved electrical conductivity by an order of magnitude in lab tests, opening routes to in-film heating or data transmission functions. This performance premium underpins broader adoption in high-value specialty crop houses willing to pay for longer life and greater yield gains.

Note: Segment shares of all individual segments available upon report purchase

By Thickness: Thin Films Dominate, Thick Films Accelerate

Films under 200 microns secured 47.45% of 2024 demand because they stretch over large spans, admit maximum light, and minimize resin usage. Their prevalence is higher in climates with mild wind loads and subsidy programs that offset frequent re-covers. The greenhouse film market size for this thickness bracket remains large; however, shorter lifespans raise total ownership costs where extreme heat or hail is common. Films above 200 microns are projected to post an 8.64% CAGR as growers in North America, MEA, and Northern China shift to thicker, UV-stabilized membranes to reduce downtime. Co-extruded five-layer products combine diffuse inner layers with IR-barrier outer layers that cut nighttime heat loss by 15%, trimming fuel bills. Higher puncture resistance also supports automated venting systems that flex covers repeatedly without tearing.

By Application: Traditional Produce Dominates, Hemp Leads Upside

Fruits and vegetables held 55.61% of revenue in 2024, reflecting entrenched supply chains for tomatoes, peppers, cucumbers, and leafy greens. Multi-span hydroponic complexes in Spain’s Almería basin and China’s Shandong province rely on cost-effective LDPE films to feed European and Asian supermarkets. The greenhouse film market size linked to this crop cluster scales with urban demand for pesticide-free, locally-sourced salads. Hemp and other high-value crops represent the breakout segment, forecast at 9.07% CAGR to 2030. U.S. industrial and cannabinoid hemp output benefits from controlled-environment yields that exceed open-field harvests by 2-3 cycles per year, with research showing cannabinoid concentration gains under precise photoperiod regimes. Specialty growers invest in EVA or multilayer PO films with superior light diffusion and odor control to maximize floral biomass and active compound production.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific’s 48.83% greenhouse film market share in 2024 stems from China’s 2 million ha greenhouse footprint and competitive resin production clusters. Government grants and low-interest loans under India’s Pradhan Mantri Krishi Sinchayee Yojana support a gradual shift from open-field vegetables toward protected cultivation. Japan and South Korea emphasize high-end film imports with anti-fog and IR-blocking layers to meet premium produce standards.

North America and Europe form a mature, regulation-intensive bloc that champions recyclable and recycled-content films. U.S. growers added 19% more greenhouse farms between 2012 and 2017 as retailers embraced “grown-near-me” sourcing models, and the trend is expected to continue through compact modular greenhouse projects. European operators deploy diffused-light covers combined with cogeneration heating systems to offset high energy tariffs, positioning thick multilayer films as part of their carbon-reduction strategies.

The Middle East & Africa segment is set for an 8.81% CAGR. Solar-rich Gulf states subsidize climate-controlled houses that pair IR-reflective roofs with photovoltaic canopies, conserving water while leveraging abundant sunlight. In East Africa, over 250 vegetable houses erected in Somalia demonstrate how modular designs can displace imports, create jobs, and stabilize local prices. South Africa and Morocco pursue export-oriented berry production, relying on UV-curable EVA films that tolerate high ultraviolet indices without yellowing.

Competitive Landscape

The greenhouse film market features a moderately concentrated field where the top five suppliers control roughly 50% of global volume. Vertically integrated resin-to-film majors such as Berry Global and RKW Group secure feedstock, extrusion capacity, and distribution in one chain, safeguarding margins during ethylene price swings. Specialty players carve niches through antimicrobial or luminescent technology licensing.

Strategic moves skew toward horizontal expansion: RKW’s buyout of Danafilms broadened its North-American footprint and added blown-film expertise for thick covers. Berry Global and Amcor entered an all-stock merger in January 2025 aiming for USD 650 million in synergies and a global R&D pool of USD 180 million. The deal pools circular-economy assets, including Berry’s Tulsa Circular Innovation Center and Amcor’s film recycling trials, to accelerate PCR-rich greenhouse cladding lines.

Greenhouse Film Industry Leaders

-

RKW Group

-

Polifilm

-

Ginegar

-

Berry Global Inc.

-

Armando Alvarez Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Uzbekistan, in partnership with China, will begin producing "smart" films to regulate greenhouse temperatures, according to the Uzbekistan Academy of Sciences. The Institute of Materials Science has developed a nano-composite particle for greenhouse films. These nanoparticles convert ultraviolet rays into near-infrared radiation, generating thermal energy to maintain stable internal temperatures.

- January 2024: Plastika Kritis, using nanotechnology, developed the Sunmaster EVO AC greenhouse polyethylene film with superior anti-drip and anti-mist properties. Unlike conventional polyethylene covers, which lose anti-condensate (AC) properties after 18-24 months, Sunmaster EVO AC; retains them for its entire four-year lifespan.

Global Greenhouse Film Market Report Scope

The greenhouse film market report includes:

| Low-Density Polyethylene (LDPE) |

| Linear Low-Density Polyethylene (LLDPE) |

| Polyvinyl Chloride (PVC) |

| Other Plastic Types (Ethylene-Vinyl Acetate (EVA),High-Performance Multi-layer, etc.) |

| Less than 200 |

| Equal to 200 |

| Greater than 200 |

| Vegetables and Fruits |

| Floriculture and Ornamentals |

| Nursery and Propagation |

| Hemp and Other High-Value Crops |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Plastic Type | Low-Density Polyethylene (LDPE) | |

| Linear Low-Density Polyethylene (LLDPE) | ||

| Polyvinyl Chloride (PVC) | ||

| Other Plastic Types (Ethylene-Vinyl Acetate (EVA),High-Performance Multi-layer, etc.) | ||

| By Thickness (Micron) | Less than 200 | |

| Equal to 200 | ||

| Greater than 200 | ||

| By Application | Vegetables and Fruits | |

| Floriculture and Ornamentals | ||

| Nursery and Propagation | ||

| Hemp and Other High-Value Crops | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Greenhouse Film Market size?

The greenhouse film market is valued at USD 7.28 billion in 2025 and is projected to reach USD 10.78 billion by 2030.

Which plastic type dominates greenhouse film demand?

Low-Density Polyethylene leads with a 43.19% share in 2024 thanks to its cost-effectiveness and proven durability in large installations.

Which application segment is expanding fastest?

Hemp and other high-value crops are forecast to grow at 9.07% CAGR through 2030 due to legalization trends and premium cannabinoid yields in controlled environments.

How are sustainability pressures influencing product innovation?

Manufacturers are increasing recycled content, launching biomass-based resins, and designing recyclable multilayer structures to comply with emerging regulations and brand ESG commitments.

Page last updated on: